|

市場調査レポート

商品コード

1850203

製造業におけるエンタープライズモビリティ:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Enterprise Mobility In Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 製造業におけるエンタープライズモビリティ:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月23日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

概要

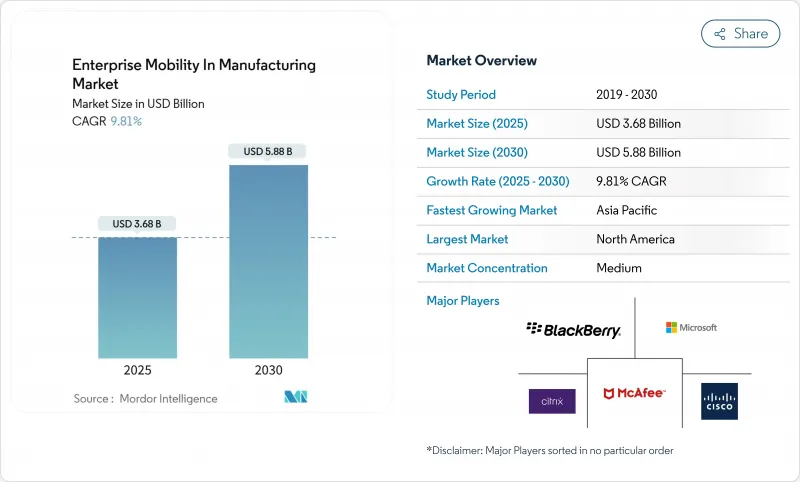

製造業におけるエンタープライズモビリティ市場規模は2025年に36億8,000万米ドル、2030年には58億8,000万米ドルに達し、CAGR 9.8%で拡大すると予測されています。

この増加傾向は、モバイル対応のワークフローが応答時間を短縮し、資産の可視性を高め、運用の回復力を強化するインダストリー4.0への急速な移行を反映しています。プライベート5Gネットワークの導入拡大、モバイルデバイスと製造実行システム(MES)の統合強化、エッジベースの拡張現実アプリケーションの普及は、総体として現場のモビリティのユースケースを広げています。しかし、リアルタイムの生産可視性を享受している製造業者はわずか16%に過ぎず、長年の情報サイロを解消するデジタルツールには大きな余地があることが浮き彫りになっています。サイバー・フィジカル・セキュリティのギャップとデータ主権に関する制約が採用を抑制し、ベンダーをゼロトラスト・アーキテクチャと地域固有のクラウド戦略へと押しやっています。

世界の製造業におけるエンタープライズモビリティ市場の動向と洞察

加速するインダストリー4.0とIIoTの採用

製造業者は、センサー、マシン、モバイルエンドポイントを統合データループにリンクさせることで、産業用モノのインターネットの展開を概念実証プロジェクトから工場全体への展開へと拡大しています。製造業者の83%が、2024年中に意思決定支援にジェネレーティブAIを組み込む意向を示しており、モバイルダッシュボードがエッジで複雑な分析を運用できるという自信を反映しています。モバイルサイバーフィジカルシステムにより、オペレーターが数時間ではなく数分で遠隔操作でパラメーターを微調整できるプロセス工場では、その影響が顕著に表れています。アジアの工場は準備をリードしており、管理者の53%が2040年までに自律的なオペレーションを目標としているのに対し、欧米の施設では半数以下です。IIoTの成熟度が高まるにつれて、スキャン、視覚化、音声を1つのデバイスに統合し、メンテナンスと品質タスクを合理化する堅牢なスマートフォンへの需要が高まる。ハードウェアとローコード・アプリ・ビルダーを事前統合するベンダーは、導入サイクルを短縮し、ITオーバーヘッドを削減します。

BYOD/CYODポリシーがコネクテッドワークフォースを拡大

工場のポリシーは、制限的なデバイス・ルールから、従業員のデジタル・ツールへのアクセスを拡大する構造化されたBring-Your-Own-DeviceおよびChoose-Your-Own-Deviceプログラムへと移行しています。製造業者の63%は、すでに個人所有のデバイスを容認していますが、正式なBYODフレームワークを実施しているのはわずか17%に過ぎず、導入ギャップが大きいことを示しています。正式なスキームを導入すれば、新入社員が使い慣れた機器を使用できるため、人手不足時の敏捷性が向上します。サムスンの8段階のCYOD青写真は、生産性を維持しながらデータを保護するために、経営幹部のスポンサーシップ、リスクベースのセグメンテーション、およびユーザー・トレーニングの必要性を強調しています。成功したロールアウトでは、企業認証情報を安全なコンテナに組み込み、トラフィックをゼロ・トラスト・ゲートウェイを経由させ、MESやERPのバックエンドと同期させています。また、MESやERのバックエンドと同期させます。早期導入企業では、企業専用のハードウェア・フリートと比較して、シフトの引き継ぎが短期間で済み、プロビジョニング・コストも低く抑えられると報告しています。

サイバーセキュリティの脆弱性とモバイルマルウェア

ITとOTの融合により、生産資産はより危険にさらされており、昨年OTへの侵入を記録した企業は93%に上る一方、統合監視を享受している企業はわずか13%に過ぎないです。モバイル・エンドポイントは、従来のウイルス対策やパッチ・サイクルが継続的な運用にほとんど合致しないため、攻撃対象領域を拡大しています。ランサムウェアのキャンペーンは、ヒューマン・マシン・インターフェースのタブレットを標的とするようになっており、制御システムから監督者を締め出すようになっています。メーカー各社は、マイクロセグメンテーション、モバイル脅威防御エージェント、厳格な最小権限ポリシーで対抗しているが、デュアルスキルを持つセキュリティ専門家の不足がプログラムの成熟を遅らせています。保険の引受保険会社は、サイバーリスクの補償を更新する前にゼロトラストのフレームワークの証明を要求することで対応し、弱点を是正するための財務的圧力を強めています。

セグメント分析

このセグメントは2024年に総売上の48.7%を占め、スマートフォンが工場スタッフの主要なモバイルゲートウェイであることが確認されました。スキャン、音声、データのオールインワン機能により、ハードウェア数が削減され、ITプロビジョニングの負担が軽減されます。レビュー期間中、ベンダーはMIL-STD-810H筐体、ホットスワップ対応バッテリー、手袋をはめたままでも使えるタッチスクリーンなど、フォームファクターを堅牢化し、過酷な現場環境にも対応できるようになりました。オペレーターは、遠隔支援やAIによる欠陥認識のために内蔵カメラを評価し、監督者はゲンバウォーク中のKPIダッシュボードのために高解像度ディスプレイを活用しています。

ウェアラブルサブセグメントは、ハンズフリーピッキング、ヘッドアップメンテナンス、人間工学に基づく負荷分散に後押しされ、CAGR 9.9%を記録しています。デジタルツインと組み合わせたスマートグラスは、作業者の視界に修理ステップやセンサーの動向を重ね合わせることで、認知的労力を軽減します。タブレット端末は、品質保証ベンチやエンジニアリング・ワークセルを支え、より大きなスクリーンがCAD図面や偏差ログをサポートします。ノートパソコンは、フルキーボードを必要とするシミュレーションやMESの管理作業など、ニッチな用途にとどまっています。新興のスマートリングや産業用ハンドヘルドは「その他」に分類されるが、タスクに特化したフォームファクタの継続的な実験を示唆しており、2030年が近づくにつれてデバイスの階層が再編成される可能性があります。

モバイル・デバイス管理は2024年に46.2%の売上を占めたが、これは企業が所有する携帯電話のコンプライアンス・バックボーンとして長い間使われてきたことを反映しています。MDMスイートは、パスワード衛生、リモートワイプ、アプリケーションのホワイトリストを実施し、ISO 27001やNIST CSFガイドラインの監査要件に合致しています。しかし、ラップトップ、スキャナ、IoTセンサを含む異機種混在のフリートへのシフトにより、統合エンドポイント管理のCAGRは10.1%に上昇しています。UEMは、Windows、Android、iOS、Linuxにまたがるポリシーオーケストレーションとパッチステータスを統合し、重複する管理作業を削減します。

製造業の顧客は、デバイスがジオフェンスを越えたり、異常なトラフィックがゼロトラスト・ルールに引っかかったりした場合に是正措置を発動するUEMの自動化フックに熱中しています。モバイル・アプリケーション管理は、個人のデバイスがBYODスキームに参加する際のコンテナ化を実現し、ハードウェアを所有することなく企業データを分離します。スタンドアローン・モバイル・セキュリティ・プラグインは、機械学習ベースの脅威ハントを追加します。すべてのソリューションタイプにおいて、プロジェクトスコープに柔軟に対応し、財務チームのROIを実証するネイティブ分析コンソールを統合したモジュラー・サブスクリプション・バンドルが支持されています。

地域分析

北米が製造業におけるエンタープライズモビリティ市場をリードし、2024年の世界売上高の39.1%を占めました。自動化文化が定着し、デジタル化ロードマップに十分な資金が投入されていることが要因です。米国の自動車産業と航空宇宙産業は、既存のモビリティパイロットをエンタープライズスコープにアップグレードし、5GキャンパスネットワークをブラウンフィールドのPLCに重ねて、自律的なマテリアルハンドリングと予測サービスをサポートします。カナダの食品加工セクターはニッチな採用企業として台頭し、アレルゲン管理とコールドチェーンの文書化にタブレットを活用します。

欧州は、ドイツのインダストリー4.0プログラムと、レガシー・マシン・パークをモバイル・ダッシュボードでレトロフィットするミッテルスタンドのチャンピオンに支えられています。フランスの製薬会社はクリーンルームの文書化に本質安全防爆仕様のスマートフォンを採用し、イタリアの機械会社は遠隔フィールドサービスに拡張現実のウェアラブルを導入しています。EUの一般データ保護規則は、デバイス上の暗号化とデータソブリンなクラウドオプションに対する高い需要を促進し、ブロック全体で調達基準を形成しています。

アジア太平洋地域は、中国、インド、東南アジアの経済がレガシーシステムを駆逐し、CAGR 10.4%を記録し、最も急成長している地域です。中国の大手エレクトロニクス企業は、人間とロボットのタスクを調整するため、巨大工場にプライベート5Gスライスを導入しています。インドでは、生産連動インセンティブ制度に基づく政府の優遇措置により、中小企業によるクラウドベースのモビリティ・ダッシュボードの導入が加速。シンガポールと韓国は、スマートグラスを装着した技術者が主権クラウドにホストされたデジタル・ツインとインターフェイスするパイロットゾーンを先導しています。この地域の勢いは、工場がモバイル労働力の増強と組み合わせた高密度自動化を採用することで、2030年以降に収益のリーダーシップが転換する可能性を示唆しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- インダストリー4.0とIIoTの導入を加速

- BYOD/CYODポリシーにより接続された労働力が拡大

- プライベート5GとWi-Fi 6が低遅延モビリティを実現

- モバイルデバイスとMESおよびクラウドPLMの統合

- エッジコンピューティングによるARとデジタルツインが耐久性の高いタブレットの需要を押し上げる

- ペーパーレスESGコンプライアンスがモバイル電子ログブックを推進

- 市場抑制要因

- サイバーセキュリティの脆弱性とモバイルマルウェア

- レガシーOT統合の複雑さ

- モバイルクラウドにおけるデータ主権の障壁

- ATEX認証の本質安全防爆機器の供給が限られている

- バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- マクロ経済動向の市場への影響評価

第5章 市場規模と成長予測

- デバイスタイプ別

- スマートフォン

- タブレット

- ノートパソコン

- ウェアラブル

- その他のデバイスタイプ

- ソリューション別

- モバイルデバイス管理(MDM)

- モバイルアプリケーション管理(MAM)

- モバイルセキュリティと脅威防御

- 統合エンドポイント管理(UEM)

- その他の解決策

- 展開モード別

- オンプレミス

- クラウド

- 組織規模別

- 大企業

- 中小企業

- 製造業の垂直分野別

- ディスクリート製造業

- 自動車

- エレクトロニクスおよび半導体

- 航空宇宙および防衛

- 産業機械

- その他

- プロセス製造

- 食品・飲料

- 医薬品およびライフサイエンス

- 化学薬品

- 石油・ガス

- 金属および鉱業

- その他

- ディスクリート製造業

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- ナイジェリア

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中分析

- 戦略的動きと展開

- 市場シェア分析

- 企業プロファイル

- VMware, Inc.

- Microsoft Corporation

- Cisco Systems, Inc.

- Blackberry Limited

- Citrix Systems, Inc.

- IBM Corporation

- SAP SE

- Oracle Corporation

- Broadcom Inc.(Symantec)

- MobileIron(Ivanti)

- SOTI Inc.

- Zebra Technologies Corporation

- Honeywell International Inc.

- Samsung SDS Co., Ltd.

- Infosys Limited

- Tata Consultancy Services Limited

- Tech Mahindra Limited

- McAfee, LLC

- Workspot, Inc.

- Tylr Mobile, Inc.