|

市場調査レポート

商品コード

1773260

エンタープライズモビリティ管理の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Enterprise Mobility Management Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| エンタープライズモビリティ管理の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月23日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

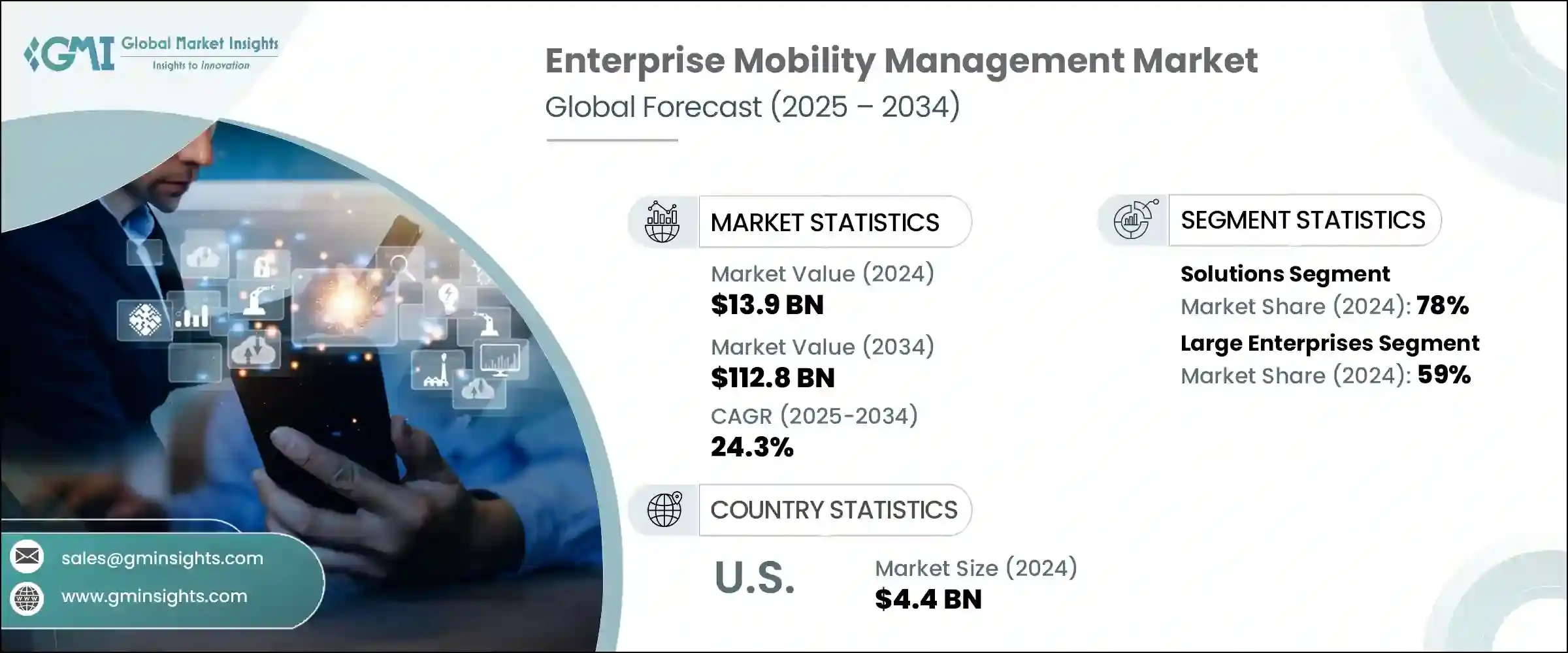

エンタープライズモビリティ管理の世界市場規模は、2024年に139億米ドルとなり、CAGR 24.3%で成長し、2034年には1,128億米ドルに達すると予測されています。

職場全体におけるスマートフォン、タブレット、ノートPCの利用が急増し、堅牢なEMMソリューションの必要性が高まっています。従業員が個人用デバイスと企業用デバイスの両方を使用してリモートで仕事をすることが増えているため、企業はモバイル・ファースト戦略を採用しており、各エンドポイントのシームレスな管理とセキュリティが求められています。EMMプラットフォームは、デバイスの監視を一元化し、接続を合理化し、ポリシーを適用して、円滑な運用を確保しながら機密データを保護します。BYOD(Bring-your-own-device)プログラムの普及は、多様なデバイスを安全かつ効率的に扱える包括的で手頃な価格のEMMツールに対する需要をさらに加速させています。

フィッシング、ランサムウェア、データ漏洩などのサイバー脅威の増加に伴い、組織は重要な情報を保護するためにモバイル・セキュリティを強化する必要があります。GDPR、HIPAA、CCPAなどの規制への対応により、データ・プライバシーはこれまで以上に重要になっており、企業は強力な認証、暗号化、リモート・ワイプ機能、早期侵入検知を提供するソリューションの採用を余儀なくされています。EMMシステムは、企業データへのアクセスを制御し、詳細な監査証跡を維持することで、情報漏えいのリスクを低減し、コンプライアンスの負担を軽減します。セキュリティに対する懸念の高まりと、高額な法的処罰の可能性が、統合された広範なEMMプラットフォームの世界の普及を後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 139億米ドル |

| 予測金額 | 1,128億米ドル |

| CAGR | 24.3% |

2024年、ソリューション分野は78%のシェアを占め、2025年~2034年のCAGRは23%と予測されます。最新のモビリティ管理プラットフォームは、人工インテリジェンスを活用してデバイスのセットアップを自動化し、リアルタイムでポリシーを適用し、新たな脅威を検出して、最も必要なところにサポートを誘導します。これらのプラットフォームはバックグラウンドで静かに動作し、パッチを自動的に展開し、手動で介入することなくコンプライアンスを実施し、不審なアクティビティが発生するとフラグを立てます。この自動化により、ITチームは日常的なトラブルシューティングではなく、戦略的な取り組みに集中できるようになり、組織全体の効率が向上します。

大企業セグメントの2024年のシェアは59%で、2034年までのCAGRは23%を維持すると予想されています。多くのトップ企業は、統合エンドポイント管理(UEM)をモビリティ戦略の基盤としており、ITスタッフはノートパソコン、スマートフォン、IoTデバイスを単一のダッシュボードから監視できるようになっています。遠隔地の従業員がさまざまな場所から接続し、プロジェクトごとにデバイスを頻繁に切り替えるようになったため、需要が急増しました。数多くのEMM機能を1つのプラットフォームに統合することで、UEMはヘルプデスクの作業負荷を軽減しながら生産性を向上させました。セキュリティの簡素化と手作業によるIT作業の軽減を約束するUEMは、ガバナンスの強化とオペレーションの俊敏性の向上に重点を置く企業にとって、特に魅力的なものとなっています。

米国のエンタープライズモビリティ管理市場は2024年に83%のシェアを占め、44億米ドルを創出。米国企業は、従業員が使用するデバイスの複雑な組み合わせを管理するBYODポリシーの普及とともに、クラウドベースのEMMソリューションを急速に採用しました。これらのツールは、個人データと業務データを効果的に分離し、ユーザー権限を制御し、EMMプラットフォームの中核的な強みである異常を検出します。このような動きにより、米国ではリモートワーク技術の導入が急速に進んでおり、他の地域はそのキャッチアップに追われています。

世界のエンタープライズモビリティ管理業界を牽引する主要企業は、IBM、SAP SE、VMware、Microsoft、Cisco Systems、Jamf、SOTI Inc.などです。EMM市場における足場を固めるため、各社は脅威検知の強化やルーチンタスクの自動化を目的とした人工知能や機械学習の統合に注力しています。戦略的提携や買収により、製品ポートフォリオや地理的範囲が拡大し、企業は多様な企業ニーズにより効果的に対応できるようになりました。

多くのプロバイダーはクラウドネイティブなソリューションを優先し、分散したワークフォースにおける拡張性と柔軟性の高いモバイル管理に対する需要の高まりに対応しています。直感的なユーザー・インターフェースやシームレスなクロスプラットフォーム互換性など、顧客中心のイノベーションが採用率の向上に貢献しています。ベンダーは、コンプライアンスへの対応や高度なセキュリティ機能を重視することで、データ保護における信頼できるパートナーとしての地位を確立しています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 企業全体でのモバイルデバイスの普及

- リモートおよびハイブリッドモデルへの移行

- サイバーセキュリティの懸念とデータ保護規制の高まり

- クラウドベースのインフラストラクチャとSaaSアプリケーションとの統合

- 業界の潜在的リスク&課題

- レガシーシステムとの統合の複雑さ

- ユーザーの抵抗と導入障壁

- 市場機会

- 統合エンドポイント管理の需要の高まり

- 規制産業の成長にはコンプライアンス対応のソリューションが必要

- BYODとクラウド導入による新興市場への拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

- ユースケース

- 最良のシナリオ

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ソリューション

- モバイルデバイス管理

- モバイルアプリケーション管理

- モバイルコンテンツ管理

- アイデンティティとアクセス管理

- サービス

- 専門サービス

- コンサルティング

- 統合と展開

- サポートとメンテナンス

- 専門サービス

5.3.2.マネージドサービス

第6章 市場推計・予測:展開モード別、2021年~2034年

- 主要動向

- オンプレミス

- クラウドベース

第7章 市場推計・予測:企業規模別、2021年~2034年

- 主要動向

- 中小企業

- 大企業

第8章 市場推計・予測:オペレーティングシステム別、2021年~2034年

- 主要動向

- iOS

- アンドロイド

- ウィンドウズ

- その他

第9章 市場推計・予測:業界別、2021年~2034年

- 主要動向

- ITおよび通信

- BFSI

- ヘルスケア

- 小売・Eコマース

- 製造業

- 政府および公共部門

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- 42Gears Mobility Systems

- Baramundi Software

- BlackBerry Limited

- Cisco Systems

- Citadel

- Citrix Systems

- IBM

- Jamf

- ManageEngine

- Matrix42

- Microsoft

- Mitsogo

- MobileIron

- SAP SE

- Scalefusion

- Snow Software

- Sophos

- SOTI

- VMware

The Global Enterprise Mobility Management Market was valued at USD 13.9 billion in 2024 and is estimated to grow at a CAGR of 24.3% to reach USD 112.8 billion by 2034. The surge in smartphone, tablet, and laptop usage across workplaces is driving the need for robust EMM solutions. Companies are embracing mobile-first strategies as employees increasingly rely on both personal and corporate devices to work remotely, demanding seamless management and security for every endpoint. EMM platforms centralize device oversight, streamline connectivity, and enforce policies to safeguard sensitive data while ensuring smooth operations. The proliferation of bring-your-own-device (BYOD) programs has further accelerated demand for comprehensive, affordable EMM tools that can handle diverse devices securely and efficiently.

With the rise in cyber threats such as phishing, ransomware, and data breaches, organizations must strengthen mobile security to protect critical information. Compliance with regulations like GDPR, HIPAA, and CCPA has made data privacy more critical than ever, forcing businesses to adopt solutions that offer strong authentication, encryption, remote wiping capabilities, and early intrusion detection. EMM systems control access to corporate data and maintain detailed audit trails, reducing breach risks and easing compliance burdens. Growing security concerns and the potential for costly legal penalties have driven global adoption of unified, wide-ranging EMM platforms.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.9 Billion |

| Forecast Value | $112.8 Billion |

| CAGR | 24.3% |

In 2024, the solutions segment held a 78% share and is projected to grow at a CAGR of 23% during 2025-2034. Modern mobility management platforms leverage artificial intelligence to automate device setup, enforce policies in real-time, detect emerging threats, and direct support where it's needed most. These platforms operate quietly in the background, deploying patches automatically, enforcing compliance without manual intervention, and flagging suspicious activities as they arise. This automation frees IT teams to focus on strategic initiatives rather than routine troubleshooting, increasing overall organizational efficiency.

The large enterprises segment held 59% share in 2024 and is expected to maintain a CAGR of 23% through 2034. Many top corporations have made unified endpoint management (UEM) the foundation of their mobility strategies, allowing IT staff to monitor laptops, smartphones, and IoT devices from a single dashboard. Demand surged as remote employees connected from various locations and frequently switched devices for different projects. By consolidating numerous EMM functions into one platform, UEM has improved productivity while reducing helpdesk workloads. Its promise of simplified security and reduced manual IT work has particularly appealed to firms focused on tightening governance and improving operational agility.

United States Enterprise Mobility Management Market held an 83% share in 2024, generating USD 4.4 billion. American companies rapidly adopted cloud-based EMM solutions alongside widespread BYOD policies to manage the complex mix of devices employees use. These tools effectively segregate personal and work data, control user permissions, and detect anomalies - core strengths of EMM platforms. This dynamic has fueled the rapid adoption of remote work technologies across the U.S., leaving other regions working to catch up.

Key players driving the Global Enterprise Mobility Management Industry include IBM, SAP SE, VMware, Microsoft, Cisco Systems, Jamf, and SOTI Inc. To strengthen their foothold in the EMM market, companies have focused on integrating artificial intelligence and machine learning to enhance threat detection and automate routine tasks. Strategic partnerships and acquisitions have expanded product portfolios and geographical reach, enabling firms to serve diverse enterprise needs more effectively.

Many providers prioritize cloud-native solutions, catering to the growing demand for scalable and flexible mobile management across distributed workforces. Customer-centric innovation, such as intuitive user interfaces and seamless cross-platform compatibility, helps improve adoption rates. By emphasizing compliance readiness and advanced security features, vendors position themselves as trusted partners in data protection.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Deployment mode

- 2.2.4 Enterprise size

- 2.2.5 Operating system

- 2.2.6 Industry vertical

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factors affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Proliferation of mobile devices across enterprises

- 3.2.1.2 Shift towards remote and hybrid models

- 3.2.1.3 Rising cybersecurity concerns and data protection regulations

- 3.2.1.4 Integration with cloud-based infrastructure & SaaS application

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Integration complexity with legacy systems

- 3.2.2.2 User resistance and adoption barriers

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for unified endpoint management

- 3.2.3.2 Growth in regulated industries needs compliance-ready solutions

- 3.2.3.3 Expansion across emerging markets with BYOD and cloud adoption

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Use cases

- 3.12 Best-case scenario

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Solutions

- 5.2.1 Mobile device management

- 5.2.2 Mobile application management

- 5.2.3 Mobile content management

- 5.2.4 Identity and access management

- 5.3 Services

- 5.3.1 Professional services

- 5.3.1.1 Consulting

- 5.3.1.2 Integration & deployment

- 5.3.1.3 Support & maintenance

- 5.3.1 Professional services

5.3.2. Managed services

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 On-premises

- 6.3 Cloud-based

Chapter 7 Market Estimates & Forecast, By Enterprise Size, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Small & medium-sized enterprises

- 7.3 Large enterprises

Chapter 8 Market Estimates & Forecast, By Operating System, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 iOS

- 8.3 Android

- 8.4 Windows

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Industry Vertical, 2021 -2034 (USD Million)

- 9.1 Key trends

- 9.2 IT & Telecom

- 9.3 BFSI

- 9.4 Healthcare

- 9.5 Retail & E-commerce

- 9.6 Manufacturing

- 9.7 Government & public sector

- 9.8 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 42Gears Mobility Systems

- 11.2 Baramundi Software

- 11.3 BlackBerry Limited

- 11.4 Cisco Systems

- 11.5 Citadel

- 11.6 Citrix Systems

- 11.7 IBM

- 11.8 Jamf

- 11.9 ManageEngine

- 11.10 Matrix42

- 11.11 Microsoft

- 11.12 Mitsogo

- 11.13 MobileIron

- 11.14 SAP SE

- 11.15 Scalefusion

- 11.16 Snow Software

- 11.17 Sophos

- 11.18 SOTI

- 11.19 VMware