中東・アフリカのプラスチック包装:市場シェア分析、産業動向、成長予測(2025~2030年)

Middle East And Africa Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 102 Pages

- 納期

- 2~3営業日

- 商品コード

- 1629770

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

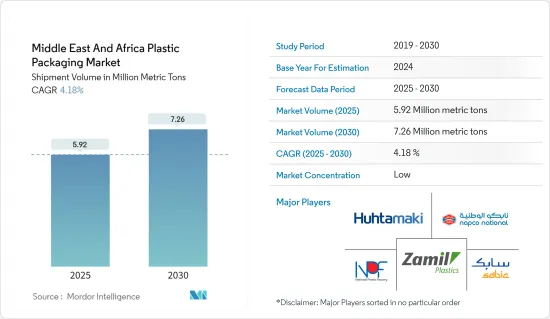

中東・アフリカのプラスチック包装市場規模は、出荷量ベースで2025年の592万トンから2030年には726万トンに拡大し、予測期間(2025~2030年)のCAGRは4.18%と予測されます。

主要ハイライト

- 消費者の嗜好がますます健康志向やサステイナブル製品に傾き、中東・アフリカでは規制が進化しているため、プラスチック包装の専門家は技術革新のプレッシャーを感じています。こうした需要の変化に合わせて、材料、デザイン、技術を調整しています。

- ボトル入り飲料水や清涼飲料水の消費増に支えられた飲料セクターは、プラスチック包装の主要なエンドユーザーとして浮上しています。アラブ首長国連邦とエジプトの研究者による最近の調査では、顕著な傾向が明らかになりました。アラブ首長国連邦では自治体の水質基準が厳しいにもかかわらず、参加者の80%以上がボトル入りの普通の飲料水を選んでいます。

- 酸化分解性プラスチックは増加傾向にあります。アラブ首長国連邦、サウジアラビア、イエメン、コートジボワール、南アフリカ、ガーナ、トーゴといった中東やアフリカの国々は、オキソ分解性プラスチックを推奨しているだけでなく、その使用を義務化している国さえあります。

- 東アフリカと西アフリカでは、国内経済が活況を呈し、消費市場が急拡大し、所得が上昇し、若年層が増加しているため、この大陸はプラスチック包装産業の極めて重要な拠点として台頭しつつあります。

- 地域政府機関は、二酸化炭素排出とエネルギー消費の抑制を目指したプロジェクトを支援しており、市場の明るい展望を示しています。例えば2024年2月、カタールの自治体省(MoM)は地元のリサイクル工場にリサイクル可能な材料を無償で提供し始め、持続可能性と循環型経済へのコミットメントを強調しました。

- もう一つの動きとして、2023年12月、プラスチック廃棄物撲滅同盟は、ドバイのSaudi Investment Recycling Company(SIRC)と覚書を交わしました。この戦略的提携は、サウジアラビアで効果的な廃棄物管理ソリューションを展開し、特に特定のプラスチックに関連する課題に取り組むことを目的としています。

- 新材料は徐々に従来のプラスチックに取って代わろうとしており、市場ベンダーにとって課題となっています。さらに、環境に対する懸念の高まりや、紙から作られたものなどサステイナブル包装に対する需要の高まりが、市場成長の障害となる可能性があります。

中東・アフリカのプラスチック包装市場の動向

軟包装が著しい成長を遂げる見込み

- 中東・アフリカでは、サウジアラビア、アラブ首長国連邦、エジプトといった国々が主に医薬品包装の需要増加に拍車をかけています。このような重点的な取り組みと、様々な産業における軟質プラスティックソリューション、特にパウチに対する需要の高まりが、市場の拡大を後押ししています。

- 構造化された包装に対する需要の高まりにより、このセグメントは予測期間中に大幅な数量成長が見込まれています。さらに、食肉と乳製品の消費が増加するにつれて、プラスチック包装の需要も増加します。これらすべての要因が、軟質プラスチック包装市場の急成長に寄与しています。

- 中東のプラスチック袋・パウチメーカーは、原油やポリプロピレンといったコスト効率の高い原料や原料を入手できるという利点があります。この利点は、プラスチック製パウチの現地生産とeコマースでの利用を後押しします。

- アラブ首長国連邦における消費者の食の嗜好の変化は、包装産業、特に飲食品産業に大きな成長機会をもたらしています。アラブ首長国連邦の金融機関Alpen Capitalのレポートによると、中東・アフリカの食品産業は、その戦略的立地と地域の人口増加により成長すると推定されています。パンデミック後のオンライン食品宅配の急増は、ラップ、スリーブ、ラベルなどの軟質包装の需要を高め、産業の成長を牽引しています。

- さらに、国内の食品加工産業の成長がプラスチック包装の需要を牽引しています。アラブ首長国連邦では約568の飲食品加工業者が操業しており、年間596万トンを生産し、同国のプラスチック包装需要を押し上げています。また、観光客の増加、消費者の嗜好の変化、人口の消費能力の増加により、同国では外食産業が増加しており、今後数年間の市場成長を後押しする可能性が高いです。

サウジアラビアが著しい成長を遂げる見込み

- サウジアラビアは、中東の包装産業で圧倒的な存在感を示しています。有名な石油・ガス部門だけでなく、多様な産業活動を誇り、プラスチック包装の年間需要を急増させています。

- 世界の原油価格の下落を受け、サウジアラビアは非石油部門の強化が急務であると認識しています。このため、サウジアラビアは国家産業開発・物流プログラム(NIDLP)やビジョン2030など、工業生産の拡大を目指すいくつかの構想や規制改革を展開しています。

- サウジアラビアはプラスチック消費でGCCをリードしています。最近のGPCAの推定によると、一人当たりのプラスチック消費量は95kgを超えており、GCCでトップのプラスチック消費国であることが強調されています。加えて、観光や教育目的によって西洋文化の受け入れが拡大しており、市場をさらに活性化させる態勢が整っています。フードモールやフードコートの人気が急上昇していることも、この成長軌道をさらに強調しています。

- さらに、調理済み食品と冷凍食品のセグメントは、消費前に最小限の準備しか必要としない、あるいは準備不要の調理済み食品を記載しています。中東諸国、特にアラブ首長国連邦とサウジアラビアでは、ペースの速い都市生活と多様な文化の影響を受けて、このセグメントの人気が高まっている

- サウジアラビアの加工肉、水産物、代替肉市場は成長を遂げています。2023年の市場規模は約1,499.10トンでした。2027年には約1,839.50トンに増加すると予測されており、加工肉に対する消費者の嗜好の変化と増加を反映しています。

中東・アフリカのプラスチック包装産業概要

中東・アフリカのプラスチック包装市場は細分化されており、複数の企業が地域別に事業を展開しています。市場の主要ベンダーは、製品革新やパートナーシップなどの戦略を採用し、市場参入を拡大し競合を維持しています。市場の主要参入企業としては、SABIC、Zamil Plastic Industries Co.、Huhtamaki Flexibles UAE(Huhtamaki Oyj)、National Plastic Factory LLC、Napco Group(Napco National)などが挙げられます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- リサイクルと持続可能性の情勢

- 産業の規制と施策と基準

- 輸出入分析

第5章 市場力学

- 市場促進要因

- 酸化分解性プラスチックの需要

- 加工食品需要の着実な増加

- 市場課題

- リサイクルと安全な廃棄をめぐる環境への懸念

- 高い原料コストと限られたリサイクルインフラ

第6章 市場セグメンテーション

- 硬質プラスチック包装

- 材料タイプ別

- ポリエチレン(PE)

- ポリエチレンテレフタレート(PET)

- ポリプロピレン(PP)

- ポリスチレン(PS)と発泡ポリスチレン(EPS)

- ポリ塩化ビニル(PVC)

- その他

- 製品タイプ別

- ボトルとジャー

- トレイ・容器

- キャップ・クロージャー

- その他

- エンドユーザー産業別

- 食品

- 飲料

- 医療

- 化粧品・パーソナルケア

- 家庭用ケア

- その他のエンドユーザー産業(産業、eコマース、その他)

- 材料タイプ別

- 軟質プラスチック包装

- 材料タイプ別

- ポリエチレン(PE)

- 二軸延伸ポリプロピレン(BOPP)

- キャストポリプロピレン(CPP)

- ポリ塩化ビニル(PVC)

- エチレンビニルアルコール(EVOH)

- その他

- 製品タイプ別

- パウチ

- バッグ

- フィルム&ラップ

- その他

- エンドユーザー産業別

- 食品

- 飲料

- 医療

- 化粧品・パーソナルケア

- 家庭用ケア

- その他のエンドユーザー産業(産業、eコマース、その他)

- 材料タイプ別

- 国別

- アラブ首長国連邦

- サウジアラビア

- エジプト

- 南アフリカ

第7章 競合情勢

- 企業プロファイル

- Zamil Plastic Industries Co.

- Takween Advanced Industries

- Packaging Products Company(PPC)

- PrimePak Industries Nigeria Ltd(Enpee Group)

- Constantia Flexibles Afripack

- Huhtamaki South Africa(Pty)Ltd

- Al Bayader International(H&H Group of Companies)

- Napco National

- Falcon Pack

- Arabian Flexible Packaging LLC

- Hotpack Packaging Industries LLC

- ENPI Group

- Gulf East Paper and Plastic Industries LLC

- ヒートマップ分析

第8章 投資分析

第9章 市場機会と今後の動向

目次

The Middle East And Africa Plastic Packaging Market size in terms of shipment volume is expected to grow from 5.92 million metric tons in 2025 to 7.26 million metric tons by 2030, at a CAGR of 4.18% during the forecast period (2025-2030).

Key Highlights

- As consumer preferences increasingly lean towards health-conscious and sustainable products, and with evolving regulations in the Middle East and Africa, professionals in plastic packaging are feeling the pressure to innovate. They are adjusting materials, designs, and technologies to align with these shifting demands.

- The beverage sector, buoyed by a rise in bottled water and soft drink consumption, emerges as the dominant end-user of plastic packaging. A recent study by researchers from the UAE and Egypt unveiled a striking trend: even with the UAE's stringent municipal water quality standards, over 80% of participants opted for bottled plain drinking water.

- Oxo-degradable plastics are on the rise. Countries in the Middle East and Africa, such as the UAE, Saudi Arabia, Yemen, Ivory Coast, South Africa, Ghana, and Togo, are not only endorsing oxo-degradable plastics but some have even made their use mandatory.

- With East and West Africa witnessing booming domestic economies, a surge in consumer markets, rising incomes, and a youthful demographic, the continent is emerging as a pivotal hub for the plastic packaging industry.

- Regional government agencies are backing projects aimed at curbing carbon emissions and energy consumption, signaling a positive outlook for the market. For example, in February 2024, Qatar's Ministry of Municipality (MoM) began offering recyclable materials at no cost to local recycling factories, underscoring their commitment to sustainability and a circular economy.

- In another move, December 2023 saw the Alliance to End Plastic Waste ink a Memorandum of Understanding (MoU) with Saudi Investment Recycling Company (SIRC) in Dubai. This strategic collaboration is set to roll out effective waste management solutions in Saudi Arabia, specifically addressing challenges linked to certain plastics.

- New materials, set to gradually take the place of conventional plastics, present a challenge for market vendors. Furthermore, growing environmental concerns and a rising demand for sustainable packaging, such as those crafted from paper, could pose hurdles to the market's growth.

Middle East And Africa Plastic Packaging Market Trends

Flexible Packaging is Expected to Witness Significant Growth

- Countries like Saudi Arabia, the United Arab Emirates and Egypt are primarily fueling the rising demand for pharmaceutical packaging in the Middle East and Africa. This emphasis and a growing demand for flexible plastic solutions, particularly pouches across various industries, propel the market's expansion.

- With a rising demand for structured packaging, the sector is poised for significant volume growth during the forecast period. Furthermore, as meat and dairy consumption increases, so will the demand for plastic packaging. All these factors contribute to the burgeoning market for flexible plastic packaging.

- Middle Eastern manufacturers of plastic bags and pouches are expected to benefit from access to cost-effective feedstock and raw materials, such as crude oil and polypropylene. This advantage bolsters the local production of plastic pouches and their use in e-commerce.

- The changing consumer food preferences in the United Arab Emirates have created significant growth opportunities in the packaging industry, especially for the food and beverage industry. According to report by Alpen Capital, a financial institute in United Arab Emirates, the food industry in the Middle East and African region is estimated to grow due to its strategic location and region's growing population. Post-pandemic, the surge in online food delivery has enhanced the demand for flexible packaging such as wraps, sleeves , labels and others, which is driving industry growth.

- Additionally, growth in the food processing industry in the country drives the demand for plastic packaging. Around 568 food and beverage processors operate across the United Arab Emirates, producing 5.96 million metric tonnes annually, boosting the demand for plastic packaging in the country. Also, the rise in the food service industry in the country due to a boost in tourism, changing consumer preferences, and the growing spending capacity of the population is likely to boost the market growth in the coming years.

Saudi Arabia is Expected to Witness Significant Growth

- Saudi Arabia stands out as a dominant player in the Middle Eastern packaging industry. Beyond its renowned oil and gas sector, the nation boasts a diverse array of industrial activities, fueling a surging annual demand for plastic packaging.

- In light of declining global crude oil prices, Saudi Arabia recognizes the imperative to bolster its non-oil sector. To this end, the nation has rolled out several initiatives and regulatory reforms, including the National Industrial Development and Logistics Program (NIDLP) and Vision 2030, aiming to amplify industrial production.

- Saudi Arabia leads the GCC in plastic consumption. Recent GPCA estimates highlight a per capita plastic consumption exceeding 95 kg, underscoring its position as the GCC's top plastic consumer. Additionally, a growing embrace of Western culture, spurred by tourism and educational pursuits, is poised to further energize the market. The burgeoning popularity of food malls and courts further underscores this growth trajectory.

- Furthermore, the ready-to-eat meals and frozen food segment offers prepared food that requires minimal or no preparation before consumption. This segment is gaining popularity in Middle Eastern countries, particularly in the United Arab Emirates and Saudi Arabia, due to the fast-paced urban lifestyle and diverse cultural influences.

- The Saudi Arabian market for processed meat, seafood, and meat alternatives is experiencing growth. In 2023, the market volume was approximately 1,499.10 metric tons. Projections indicate an increase to about 1,839.50 metric tons by 2027, reflecting the country's changing and growing consumer preferences for processed meat.

Middle East And Africa Plastic Packaging Industry Overview

The Middle East and Africa Plastic Packaging Market is fragmented in nature, with multiple players in the market operating regionally. The major vendors in the market adopt strategies such as product innovation and partnerships, among others, to expand their reach and stay competitive in the market. Some of the major players in the market are SABIC, Zamil Plastic Industries Co., and Huhtamaki Flexibles UAE (Huhtamaki Oyj), National Plastic Factory LLC, Napco Group (Napco National), among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Recycling and Sustainability Landscape

- 4.5 Industry Regulation, Policy and Standards

- 4.6 Import-Export Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Demand for Oxo-Degradable Plastics

- 5.1.2 Steady Rise in Demand for Processing Food

- 5.2 Market Challenges

- 5.2.1 Environmental Concerns over Recycling and Safe Disposal

- 5.2.2 High Raw Material Costs and Limited Recycling Infrastructure

6 MARKET SEGMENTATION

- 6.1 Rigid Plastic Packaging

- 6.1.1 By Material Type

- 6.1.1.1 Polyethylene (PE)

- 6.1.1.2 Polyethylene Terephthalate (PET)

- 6.1.1.3 Polypropylene (PP)

- 6.1.1.4 Polystyrene (PS) and Expanded Polystyrene (EPS)

- 6.1.1.5 Polyvinyl Chloride (PVC)

- 6.1.1.6 Other Material Types

- 6.1.2 By Product Type

- 6.1.2.1 Bottles and Jars

- 6.1.2.2 Trays and containers

- 6.1.2.3 Caps and Closures

- 6.1.2.4 Other Product Types

- 6.1.3 By End-User Industry

- 6.1.3.1 Food

- 6.1.3.2 Beverage

- 6.1.3.3 Healthcare

- 6.1.3.4 Cosmetics and Personal Care

- 6.1.3.5 Household Care

- 6.1.3.6 Other End-User Industries (Industrial, E-Commerce, Among Others)

- 6.1.1 By Material Type

- 6.2 Flexible Plastic Packaging

- 6.2.1 By Material Type

- 6.2.1.1 Polyethylene (PE)

- 6.2.1.2 Bi-Orientated Polypropylene (BOPP)

- 6.2.1.3 Cast Polypropylene (CPP)

- 6.2.1.4 Polyvinyl Chloride (PVC)

- 6.2.1.5 Ethylene Vinyl Alcohol (EVOH)

- 6.2.1.6 Other Material Types

- 6.2.2 By Product Type

- 6.2.2.1 Pouches

- 6.2.2.2 Bags

- 6.2.2.3 Films & Wraps

- 6.2.2.4 Other Product Types

- 6.2.3 By End-User Industry

- 6.2.3.1 Food

- 6.2.3.2 Beverage

- 6.2.3.3 Healthcare

- 6.2.3.4 Cosmetics and Personal Care

- 6.2.3.5 Household Care

- 6.2.3.6 Other End-User Industries (Industrial, E-Commerce, Among Others)

- 6.2.1 By Material Type

- 6.3 By Country

- 6.3.1 United Arab Emirates

- 6.3.2 Saudi Arabia

- 6.3.3 Egypt

- 6.3.4 South Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Zamil Plastic Industries Co.

- 7.1.2 Takween Advanced Industries

- 7.1.3 Packaging Products Company (PPC)

- 7.1.4 PrimePak Industries Nigeria Ltd (Enpee Group)

- 7.1.5 Constantia Flexibles Afripack

- 7.1.6 Huhtamaki South Africa (Pty) Ltd

- 7.1.7 Al Bayader International (H&H Group of Companies

- 7.1.8 Napco National

- 7.1.9 Falcon Pack

- 7.1.10 Arabian Flexible Packaging LLC

- 7.1.11 Hotpack Packaging Industries LLC

- 7.1.12 ENPI Group

- 7.1.13 Gulf East Paper and Plastic Industries LLC

- 7.2 Heat Map Analysis

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 102 Pages

- 納期

- 2~3営業日