アフリカのプラスチック包装:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Africa Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 179 Pages

- 納期

- 2~3営業日

- 商品コード

- 1683827

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

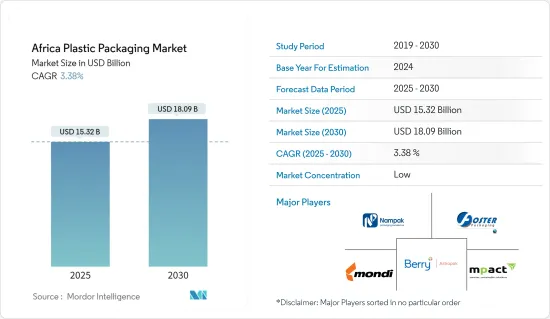

アフリカのプラスチック包装市場規模は2025年に153億2,000万米ドルと推計され、予測期間(2025年~2030年)のCAGRは3.38%で、2030年には180億9,000万米ドルに達すると予測されます。

アフリカでは近年、急速な人口増加と都市化が進んでいます。人口が増加し、都市に移り住む人が増えるにつれて、包装された商品に対する需要が高まり、プラスチック包装製品に対するニーズが生まれています。さらに、経済成長によって中産階級が拡大し、この地域のさまざまな国で可処分所得が増加しました。人々の購買力が高まるにつれ、包装商品の需要も高まり、プラスチック包装業界の成長を牽引しています。

主なハイライト

- この地域の多くの国々は、経済発展のために工業化と製造業に力を入れており、これには食品、飲食品、医薬品、パーソナルケア製品など様々な産業向けの工場設立が含まれます。プラスチック包装はこれらの産業にとって多用途で便利なソリューションであるため、同地域ではその需要が継続的に伸びています。

- 人口の増加に伴い、アフリカ諸国では飲食品の需要が継続的に増加しています。世界銀行によると、アフリカの食品産業の総額は2030年までに1兆米ドル(約8,415億ユーロ)に増加する可能性があります。

- 同市場は、主に環境問題への関心の高まりによる規制基準のダイナミックな変化により、厳しい課題に直面することが予想されます。この地域の各国政府は、プラスチック包装廃棄物に関する国民の懸念に対応し、環境廃棄物を最小限に抑え、廃棄物管理プロセスを改善するための規制を実施しています。

- 国際的な食品製造企業は、製品需要の高まりを受けてアフリカでの事業を拡大しています。2022年10月、クッキーメーカーのBritannia Industries Ltdは、アフリカでの事業拡大計画の一環として、ケニアでの事業に関する契約を締結しました。

- 同市場は、主に環境問題への関心の高まりによる規制基準のダイナミックな変化により、課題が予想されます。この地域の各国政府は、プラスチック包装廃棄物に関する国民の懸念に対応し、環境廃棄物を最小限に抑え、廃棄物管理プロセスを改善するための規制を実施しています。

アフリカのプラスチック包装市場の動向

食品産業が硬質・軟質プラスチック包装市場の主要シェアを占める

- プラスチック製食品保存容器は、効果的な密封によって保存中の食品の保存や鮮度保持に役立ちます。これらの容器は、カフェ、食料品店、あるいはあらゆる食品ビジネスでの使用に適しています。包装は西アフリカの重要な市場です。この産業は、主に農業と食品産業の成長に対応してサブリージョンで発展してきました。ナイジェリア、南アフリカ、ケニアは、この地域のプラスチック包装市場でかなりのシェアを占めています。

- 東部・南部アフリカの食品部門は2050年までに800%の成長が見込まれ、加工食品の取引は最大90%増加します。アフリカ全体では2030年までに1兆米ドルの食品産業になると予想されており、都市部の消費がより多くの製品に対する需要を牽引しています。食品包装はアフリカで最も重要なエンドユーザー・プラスチック産業のひとつです。食品業界では硬質プラスチック包装が増えています。同産業は、軽量でコスト削減が可能といった特性からこれを使用しています。

- 硬質プラスチックや使い捨て容器は、テイクアウト、フード・チェーン、レストランに不可欠です。しかし、この地域全体では環境への懸念があります。この地域全体で複数の食品チェーンがオープンしたことで、アフリカではプラスチック包装の需要が急増しています。2022年5月、ドバイを拠点とするハラル・ファーストフード・チェーンのChicKingは、今後5年間でケニアに30店舗をオープンする意向を発表しました。

- 典型的なフレキシブル食品包装の用途には、チーズ、肉、パン、野菜などの食品を包装するフィルムやパウチがあります。ほとんどの場合、フレキシブル包装は一次包装として使用されるが、場合によっては二次包装として使用されることもあります。

- これらのフィルムはラミネート加工されたものとされていないものがあり、冷凍庫のような過酷な環境にも耐えることができます。その衝撃強度、引裂強度、耐屈曲亀裂性、優れた密封性は、食品用途で広く使われています。こうした要因がアフリカの軟包装市場を牽引しています。

- アフリカでは都市化が進んでいるため、都市に住む人が増え、新鮮な農産物を手に入れる機会が減っています。さらに、消費者の持続可能性への関心の高まりは、リサイクルが容易なリサイクル材料から作られた包装につながり、それゆえ軟包装の需要を支えています。

南アフリカが大きな市場シェアを占める

- お弁当の人気の高まり、レストランやスーパーマーケットの数の拡大、ボトル入り飲料水と飲料の消費量の増加は、すべて同国の市場拡大の主な要因です。

- 南アフリカのホームケア製品市場は、より健康的なライフスタイルを維持しようとする個人の動向の高まりにより、近年かなりの成長を遂げています。このため、飲料ボトル、トイレタリーボトル、ビニール袋などの製品に対する需要が高まり、同地域のプラスチック包装市場の成長を高めています。

- 同国のプラスチックゴミの量は膨大であるため、政府の動向と消費者の強い意識により、リサイクル傾向は健全な速度で拡大しています。さらに、南アフリカのコカ・コーラのような企業は、国内で生産されるよりも多くのPETを回収し、リサイクルしています。

- 需要面では、モバイル接続の発達に伴い、南アフリカの顧客はeコマースに移行しつつあります。この傾向は、COVID-19の大流行や、国内での非接触型取引への関心の高まりの結果、加速しています。これにより、いくつかの市場買収が可能になりました。例えば、2021年7月、オーストリアのプラスチック包装会社ALPLAグループは、南部アフリカでの足跡を拡大するため、南アフリカの包装メーカーVerigreen Packagingを買収しました。

- 外的な経済変動要因の影響にもかかわらず、全体として同国の飲料消費量は急速に増加しています。ソフトドリンクの消費は、気候条件の結果として同国で増加しており、人々はより多くの炭酸飲料を飲んでいます。過去2年間の深刻な水不足により、ボトル入り飲料水の使用量も劇的に増加しています。ペットボトルが市場の主流となり、ペットボトルの需要も増加しています。したがって、これらの要因が同国のプラスチック包装市場の成長を促進しています。

アフリカのプラスチック包装業界の概要

アフリカのプラスチック包装市場は非常に断片化されており、モンディ、ナンパック、ベリー・アストラパックといった市場の既存企業と、いくつかの地域の包装会社で構成されています。環境に対する懸念が各国で高まる中、大手企業は環境問題に取り組み、プラスチックボトルをより安全なものにするため、研究開発への投資を強化しています。

- 2023年1月、Phatisaは、ケニアとナイジェリアの子会社を通じてサハラ以南のアフリカで印刷・包装事業を展開し、飲食品部門に強いエクスポージャーを持つMHL International Holdingsの大幅な少数株主持分の取得を発表しました。

- 2022年8月、アルプラはOTC包装製造技術を拡大しました。ALPLAグループの医薬品パッケージング事業であるAlplapharmaは、OTCボトルの製造技術を拡張し、フレキシブル押出ブロー成形(EBM)を導入することで、この分野における持続可能で顧客に特化したパッケージング・ソリューションを実現しました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- エコシステム分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- ペットボトル需要の増加が同地域における硬質包装のニーズを促進する見込み

- 飲料用包装は今後数年で牽引力を増す見込み

- 市場の課題

- 原材料価格の変動

- COVID-19と最近の地政学的変化がアフリカ包装産業の成長に与える影響

- アフリカの主要新興市場の分析

- 関連HSコードに基づくアフリカへの主要原材料輸入の分析

- プラスチック包装市場における技術革新

- 包装産業における広範なROI対策の分析

第6章 市場セグメンテーション

- 硬質包装

- 材料

- ポリエチレン(PE)

- ポリエチレンテレフタレート(PET)

- ポリプロピレン(PP)

- ポリスチレン(PS)および発泡ポリスチレン(EPS)

- ポリ塩化ビニル(PVC)

- その他の材料

- エンドユーザー

- 食品

- 飲料

- ヘルスケアと医薬品

- パーソナルケアと化粧品

- その他のエンドユーザー

- 材料

- 軟包装

- 材料

- ポリエチレン(PE)

- 二軸延伸ポリプロピレン(BOPP)

- キャストポリプロピレン(CPP)

- ポリ塩化ビニル(PVC)

- エチレンビニルアルコール(EVOH)

- その他の材料

- エンドユーザー

- 食品

- 飲料

- パーソナルケアと化粧品

- その他のエンドユーザー

- 材料

- 国名

- 南アフリカ

- ナイジェリア

- エジプト

- ケニア

- モロッコ

- ガーナ

- エチオピア

- タンザニア

- ザンビア

第7章 競合情勢

- 企業プロファイル

- Berry Astrapak(Berry Global Group Inc.)

- Nampak Ltd

- Mondi PLC

- Mpact Pty Ltd

- Foster International Packaging

- Constantia Flexibles

- Tetra Pak SA

- Amcor PLC

- LIQUIBOX(Sealed Air Corporation)

- Sonoco Products Company

- Toppan Inc.

- Huhtamaki Oyj

- ALPLA Group

- Plastipak Holdings Inc.

- Polyoak Packaging

第8章 アフリカの国別主要ベンダーリスト

- 南アフリカ

- ナイジェリア

- エジプト

- ケニア

- モロッコ

- ガーナ

- エチオピア

- タンザニア

- ザンビア

第9章 市場の将来展望

第10章 投資分析

目次

The Africa Plastic Packaging Market size is estimated at USD 15.32 billion in 2025, and is expected to reach USD 18.09 billion by 2030, at a CAGR of 3.38% during the forecast period (2025-2030).

Africa has experienced rapid population growth and urbanization in recent years. As the population increases and more people move to cities, there is a rising demand for packaged goods, creating the need for plastic packaging products. Furthermore, economic growth resulted in an expansion of the middle class and increased disposable income in various countries of the region. As purchasing power of people increases, the demand for packaged goods also rises, driving the growth of the plastic packaging industry.

Key Highlights

- Many countries in the region are focusing on industrialization and manufacturing for their economic development, which includes the establishment of factories for various industries, such as food, beverage, pharmaceuticals, personal care products, and more. As plastic packaging is a convenient solution for these industries in multiple applications, its demand is growing continuously in the region.

- With a growing population, demand for food and beverages is continuously increasing in the countries of Africa. According to World Bank, the total value of the African food industry could rise to USD one trillion (approx. EUR 841.5 billion) by 2030.

- The market is expected to be challenged owing to dynamic changes in regulatory standards, primarily due to increasing environmental concerns. Governments across the region have been responding to public concerns regarding plastic packaging waste and implementing regulations to minimize environmental waste and improve waste management processes.

- International food manufacturing companies are expanding their operations in Africa due to rising product demand. In October 2022, cookie manufacturer Britannia Industries Ltd finalized a deal for operations in Kenya as part of its plan to expand in Africa.

- The market is expected to be challenged owing to dynamic changes in regulatory standards, primarily due to increasing environmental concerns. Governments across the region have been responding to public concerns regarding plastic packaging waste and implementing regulations to minimize environmental waste and improve waste management processes.

Africa Plastic Packaging Market Trends

Food Industry to Hold Major Share in Both Rigid and Flexible Plastic Packaging Markets

- Plastic food storage containers help preserve food during storage or keep them fresh by effective sealing. These containers are suitable for use in cafes, grocery shops, or any food business. Packaging is an important market in West Africa. This industry has developed in the sub-region largely in response to farming and the growth of the food industry. Nigeria, South Africa, and Kenya have a substantial share of the plastic packaging market in the region.

- The food sector in Eastern and Southern Africa is expected to grow by 800% by 2050, with trade in processed foods increasing by up to 90%. Africa as a whole is anticipated to be a USD 1 trillion food industry by 2030, with urban consumption driving demand for more products. Food packaging is one of Africa's most significant end-user plastic industries. Rigid plastic packaging is increasing in the food industry. The industry uses it for its properties, such as lightweight and reduced cost.

- Rigid plastic and disposable containers are integral to takeouts, food chains, and restaurants. However, there are environmental concerns across the region. The opening of several food chains across the region has spiked the demand for plastic packaging in Africa. In May 2022, the Dubai-based halal fast-food chain ChicKing announced its intentions to open 30 outlets in Kenya over the next five years.

- Typical flexible food packaging applications include films and pouches to package food products like cheeses, meats, bread, and vegetables, among others. In most cases, flexible packaging is used as the primary packaging, but it can also be used as the secondary packaging in some cases.

- These films can be laminated or nonlaminated and withstand harsh environments like freezers. Their impact strength, tear strength, flex-crack resistance, and excellent sealing properties are extensively used in food applications. Such factors are driving the flexible packaging market in the country.

- Due to increasing urbanization in Africa, more people are living in cities and having less access to fresh produce, which is driving the demand for flexible packaging. Additionally, the growing focus of consumers toward sustainability is leading to packaging made from recycled materials that can be easily recycled, hence supporting the demand for flexible packaging.

South Africa to Hold Significant Market Share

- The rising popularity of packed meals, the expanding number of restaurants and supermarkets, and rising bottled water and beverage consumption are all key drivers of the country's market expansion.

- The South African home care products market has seen considerable growth in recent years owing to a growing trend among individuals to maintain a healthier lifestyle. This has driven demand for products like beverage bottles, toiletry bottles, plastic bags, and others, thereby increasing the growth of the region's plastic packaging market.

- With the country's enormous volume of plastic garbage, the recycling trend is expanding at a healthy rate, owing to government restrictions and strong consumer awareness. Moreover, companies like Coca-Cola in South Africa collected and recycled more PET than was produced within the country.

- On the demand side, customers in South Africa are migrating to e-commerce as mobile connectivity develops. This tendency has accelerated as a result of the COVID-19 pandemic as well as a spike in interest in contactless transactions inside the country. This has permitted several market acquisitions. For instance, in July 2021, Austrian plastic packaging firm ALPLA Group purchased South African packaging producer Verigreen Packaging to extend its footprint in southern Africa.

- Overall, beverage consumption in the country is increasing rapidly, despite the impact of external economic variables. Soft drink consumption is increasing in the country as a result of climatic conditions, with people drinking more carbonated beverages. Due to severe water scarcity in the country over the previous two years, the usage of bottled water has also increased dramatically. With PET bottles becoming the market norm, the demand for plastic bottles has also increased. Therefore, these factors are driving the growth of the plastic packaging market in the country.

Africa Plastic Packaging Industry Overview

The African plastic packaging market is highly fragmented, comprising market incumbents such as Mondi, Nampak, and Berry Astrapak and several regional packaging firms. With environmental concerns rising across countries, major players have boosted their investments in research and development to tackle environmental concerns and make plastic bottles safer.

- In January 2023, Phatisa announced the acquisition of a significant minority stake in MHL International Holdings, a printing and packaging provider operating in Sub-Saharan Africa through subsidiaries in Kenya and Nigeria with strong exposure to the food and beverage sector.

- In August 2022, ALPLA expanded its OTC packaging manufacturing technology. Alplapharma, the pharma packaging business of the ALPLA group, accomplished this by expanding its manufacturing technology for OTC bottles with the inclusion of flexible extrusion blow molding (EBM), which allows for sustainable and customer-specific packaging solutions in this field.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Ecosystem Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand for Pet Bottles is Expected to Drive the Need for Rigid Packaging in the Region

- 5.1.2 Beverage Packaging is Expected to Gain Traction over the Coming Years

- 5.2 Market Challenges

- 5.2.1 Fluctuating Raw Material Prices

- 5.3 Impact of COVID -19 and the Recent Geopolitical Changes on the Growth of the African Packaging Industry

- 5.4 Analysis of the Key Emerging Markets in Africa

- 5.5 Analysis of the Key Raw Material Imports into Africa Based on Relevant HS Codes

- 5.6 Technological Innovations in the Plastic Packaging Market

- 5.7 Analysis of the Broader ROI Measures within the Packaging Industry

6 MARKET SEGMENTATION

- 6.1 Rigid Packaging

- 6.1.1 Material

- 6.1.1.1 Polyethylene (PE)

- 6.1.1.2 Polyethylene Terephthalate (PET)

- 6.1.1.3 Polypropylene (PP)

- 6.1.1.4 Polystyrene (PS) and Expanded Polystyrene (EPS)

- 6.1.1.5 Polyvinyl Chloride (PVC)

- 6.1.1.6 Other Materials

- 6.1.2 End User

- 6.1.2.1 Food

- 6.1.2.2 Beverage

- 6.1.2.3 Healthcare and Pharmaceutical

- 6.1.2.4 Personal Care and Cosmetics

- 6.1.2.5 Other End Users

- 6.1.1 Material

- 6.2 Flexible Packaging

- 6.2.1 Material

- 6.2.1.1 Polyethylene (PE)

- 6.2.1.2 Bi-orientated Polypropylene (BOPP)

- 6.2.1.3 Cast Polypropylene (CPP)

- 6.2.1.4 Polyvinyl Chloride (PVC)

- 6.2.1.5 Ethylene Vinyl Alcohol (EVOH)

- 6.2.1.6 Other Materials

- 6.2.2 End User

- 6.2.2.1 Food

- 6.2.2.2 Beverage

- 6.2.2.3 Personal Care and Cosmetics

- 6.2.2.4 Other End Users

- 6.2.1 Material

- 6.3 Country

- 6.3.1 South Africa

- 6.3.2 Nigeria

- 6.3.3 Egypt

- 6.3.4 Kenya

- 6.3.5 Morocco

- 6.3.6 Ghana

- 6.3.7 Ethiopia

- 6.3.8 Tanzania

- 6.3.9 Zambia

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Berry Astrapak (Berry Global Group Inc.)

- 7.1.2 Nampak Ltd

- 7.1.3 Mondi PLC

- 7.1.4 Mpact Pty Ltd

- 7.1.5 Foster International Packaging

- 7.1.6 Constantia Flexibles

- 7.1.7 Tetra Pak SA

- 7.1.8 Amcor PLC

- 7.1.9 LIQUIBOX (Sealed Air Corporation)

- 7.1.10 Sonoco Products Company

- 7.1.11 Toppan Inc.

- 7.1.12 Huhtamaki Oyj

- 7.1.13 ALPLA Group

- 7.1.14 Plastipak Holdings Inc.

- 7.1.15 Polyoak Packaging

8 LIST OF KEY VENDORS IN AFRICA BY COUNTRY

- 8.1 South Africa

- 8.2 Nigeria

- 8.3 Egypt

- 8.4 Kenya

- 8.5 Morocco

- 8.6 Ghana

- 8.7 Ethiopia

- 8.8 Tanzania

- 8.9 Zambia

9 FUTURE OUTLOOK OF THE MARKET

10 INVESTMENT ANALYSIS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 179 Pages

- 納期

- 2~3営業日