|

市場調査レポート

商品コード

1850194

サービスとしての分析:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Analytics As A Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| サービスとしての分析:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月19日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

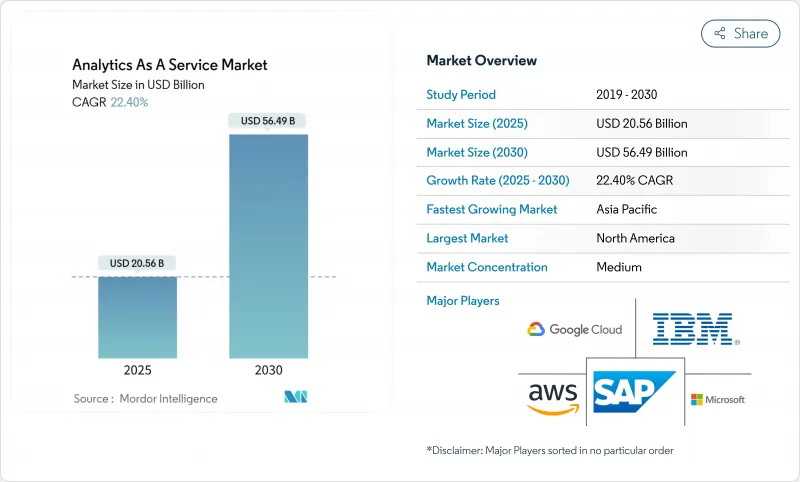

サービスとしての分析市場規模は、2025年に205億6,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは22.40%で、2030年には564億9,000万米ドルに達すると予測されます。

クラウドファーストのデータ近代化プログラムにより、企業はオンプレミスのアナリティクススタックを廃止し、従量課金サービスに移行できるため、需要が高まっています。また、ベクトルネイティブデータストアの急速な普及により、ジェネレーティブAI向けの非構造化データのリアルタイム処理も可能になりつつあります。現在、パブリッククラウドの導入がリードしているが、企業がコスト管理とデータ主権ルールのバランスを取りながら、ハイブリッド戦略が進んでいます。ハイパースケールプラットフォームがAI機能を強化する一方で、専門プロバイダーは垂直ソリューションと組み込みアナリティクスに注力するため、競争は激化しています。しかし、人材不足とデータ進出の経済性は、導入スケジュールとROI計算に影響を与え続けています。

世界のサービスとしての分析市場の動向と洞察

クラウドファーストの企業データ近代化プログラム

近代化プロジェクトは、サイロ化されたデータをAI対応パイプラインをサポートするクラウドネイティブプラットフォームに統合する動機付けとなっています。IBMの報告によると、大企業の大半は2025年までにほとんどのワークロードをクラウドで実行する計画であり、レガシーデータウェアハウスからの脱却を強調しています。ベンダーは、ワークロードのポータビリティを簡素化し、スキーマ変換を自動化し、マルチリージョン環境でセキュリティ管理を維持するためのフルスタックの移行ツールキットを提供しています。金融サービス、ヘルスケア、小売業がデータウェアハウスを導入する主なメリットとして、洞察を得るまでの時間の短縮とインフラストラクチャーのオーバーヘッドの削減を挙げています。支出が設備投資から運用支出にシフトする中、サービス・プロバイダーは、透明性の高い価格設定、統合ガバナンス、導入加速のための事前構築済みAIサービスで差別化を図っています。

AIに対応したベクターネイティブデータストアの普及

ベクター・データベースは、ジェネレーティブなAI検索、レコメンデーション、チャット体験のための非構造化コンテンツの解放に役立っています。オラクルはHeatWave GenAIに自動ベクターストアを組み込みました。Salesforceは、Data Cloudでベクトル機能を利用可能にしました。これらの統合により、個別のインデックス作成レイヤーを使用することなく、大規模な類似性クエリが簡素化されます。企業は単一のプラットフォーム内でテキスト、音声、画像のエンベッディングとトランザクションデータを組み合わせる能力を獲得し、待ち時間と運用の複雑さを軽減します。小売業やメディア業界では、パーソナライズされたエクスペリエンスを実現するためにこのアプローチをいち早く採用し、産業界では品質検査モデルを改良するためにベクトル検索を採用しています。市場参入企業は、オープンソースの互換性と、モデルの再トレーニングを容易にするオーケストレーテッド・パイプラインを重視しています。

高騰するハイパースケーラのイグレスフィーの経済性

データ転送料金は、一般的なクラウド請求の10%~15%を占めることがあります。これらの料金は、プラットフォーム間でテラバイトを移行することで総所有コストが増加するため、マルチクラウド分析アーキテクチャを阻害します。英国市場競争庁は、移行手数料をスイッチングの障壁として指摘しています。一部のプロバイダーは特定の条件下での料金免除を導入しているが、顧客は依然として契約上のハードルに直面しています。サービスインテグレーターは現在、大容量のデータセットをニュートラルなストレージ階層に保持するアーキテクチャや、最大85%のコスト削減を謳うRackspaceのData Freedomのようなデータ・イン・モーション最適化を採用するアーキテクチャを推進しています。

セグメント分析

大企業は、企業規模のデータレイクや高度なモデリングツールの導入に多額の予算を活用しており、2024年の売上高の64%を占めています。大企業のアナリティクス施設は、多くの場合、長年のERPやCRMシステムと統合され、部門横断的なダッシュボードやAI主導の予測を可能にしています。また、多国籍企業は主権管理を優先するため、プライベート・バックボーン・ネットワーク経由で相互接続する地域固有の導入を進めています。

中小企業の現在のシェアは小さいが、2030年までのCAGRは24.3%と最も高いです。従量制の価格設定とターンキー・テンプレートが、データサイエンス専門チームを持たない企業の障壁を下げます。ノーコード・インターフェイス、自動MLサービス、パッケージ化されたバーティカル・アナリティクスは、創業者が迅速に洞察を引き出し、在庫の最適化やターゲット・マーケティングをサポートするのに役立ちます。中小企業の導入が拡大するにつれて、ベンダーは、ワークロードのコストをビジネスKPIにマッピングし、財務チームとオペレーションチーム全体で透明性の高い予算編成を促進する、簡素化されたFinOpsコンソールを試験的に導入しています。中小企業の流入により、サービスとしての分析市場の顧客基盤は拡大し、プロバイダーは軽量なサービス層やコミュニティ主導の教育をリリースするようになります。

パブリッククラウドが2024年の売上高の48.3%を維持したのは、共有インフラが即時の弾力性、グローバルリーチ、継続的な機能アップグレードを可能にするためです。新興企業やデジタルネイティブ企業は、最新のAIアクセラレータにアクセスしながらデータセンターへの出費を避け、フルマネージド分析スタックを利用しています。しかし、規制業界の企業は、居住義務や社内のリスクポリシーを満たすために、機密性の高いワークロードをプライベート環境に保持しています。

ハイブリッドアーキテクチャはCAGR 26.7%で拡大し、パブリックなスケーラビリティとプライベートクラウドの制御が融合します。IBMは、ハイブリッドのデプロイメントによって、チームがデータとコンピュートそれぞれを最適な場所に配置できるようになり、柔軟性が向上すると指摘しています。企業は通常、生のデータをプライベート・オブジェクト・ストアに置き、大規模なモデル・トレーニングのためにパブリック・クラスターにバーストします。このトポロジーはイグレス費用を軽減し、階層化された災害復旧態勢をサポートします。ソブリン要件が高まるにつれ、プロバイダーは地域別のソブリン・クラウド・ゾーンやクラウド間ネットワーキング・サービスを導入し、サービスとしての分析市場におけるハイブリッドの魅力をさらに高めています。

サービスとしての分析市場は、企業規模別(中小企業、大企業)、展開モデル別(パブリッククラウド、プライベートクラウド、ハイブリッドクラウド)、分析タイプ別(記述的分析、診断的分析、その他)、エンドユーザー産業別(IT・通信、BFSI、ヘルスケア・ライフサイエンス、その他)、地域別に分類されています。市場予測は金額(米ドル)で提供されます。

地域分析

北米は2024年の売上高の42.8%を占め、クラウドの普及、成熟したAI人材プール、圧倒的なハイパースケーラによる絶え間ない製品革新がその要因となっています。ヘルスケア、小売、メディアの米国企業は、大規模アナリティクスを適用して、体験のパーソナライズ、ロジスティクスの最適化、精密医療の推進を行っています。政府機関もまた、分析ワークロードを促進するデータ共有イニシアチブを拡大しています。カナダの企業は、公共部門のデータ居住に関する法律を満たすソブリン・クラウド・ゾーンの迅速な導入でこれに追随しています。メキシコの製造業回廊では、輸出志向のサプライチェーンにクラウド・アナリティクスを統合し、業務上の洞察力のギャップを解消しています。

アジア太平洋地域は、中国、日本、インド、東南アジアの積極的なデジタル経済アジェンダに牽引され、CAGRが25.4%と最も高くなると予測されています。急速に拡大するeコマース・プラットフォームは毎日テラバイト単位の行動データを取り込み、フィンテックは十分なサービスを受けていない人々をターゲットとした信用モデルを展開しています。現地のクラウド・プロバイダーは多国籍のハイパースケーラーと提携し、地域に準拠したインフラを構築することで、レイテンシーを下げ、主権に対応したサービスとしての分析市場提供を可能にしています。スマート・ファクトリー展開のための政府刺激策が需要をさらに刺激し、中小企業は低コストのサービス・バンドルを活用してレガシー・システムから飛躍します。

欧州は、プライバシーとAIガバナンスの枠組みによって形成された大きなシェアを占めています。GDPRの厳格な施行と今後予定されているEUのAI法規則は、説明可能なモデル、監査レイヤー、主権クラウド制御の導入を企業に促しています。AWSはドイツを拠点とする企業体を設立し、2025年後半を目標に独立した欧州ソブリン・クラウドを運営すると発表しました。金融機関はマルチリージョンの冗長性を導入してオペレーションの回復力を維持し、製造業はIoTデータをアナリティクス・パイプラインに接続してエネルギー効率目標をサポートします。欧州のサービスとしての分析市場は、このようにイノベーションとコンプライアンスのバランスを取り、ビジネスと規制の両方の必要性を満たすハイブリッドパターンを推進しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- クラウドファーストのエンタープライズデータ近代化プログラム

- Gen-AI対応のベクトルネイティブデータストアの普及

- SMBのクラウド移行による従量課金制の需要増加

- コンプライアンス主導のリアルタイム監査分析(例:DORA、SEC)

- 垂直SaaS「ミニクラウド」における組み込み分析

- ソブリンクラウドの義務化により、地域的なAaaSの構築が促進される

- 市場抑制要因

- ハイパースケーラーのエグレス料金の経済性が高まる

- FinOpsとデータ運用の人材不足

- モデルの説明可能性に関する規制が導入を遅らせる

- 非グリーンデータセンターの利用を制限する炭素強度割当

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- 主要業績評価指標(KPI)

- 業界の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- マクロ経済要因の市場への影響

第5章 市場規模と成長予測

- 企業規模別

- 中小企業

- 大企業

- 展開モデル別

- パブリッククラウド

- プライベートクラウド

- ハイブリッドクラウド

- 分析タイプ別

- 記述的分析

- 診断分析

- 予測分析

- 処方的分析

- エンドユーザー業界別

- IT・通信

- BFSI

- ヘルスケアとライフサイエンス

- 小売業とeコマース

- 製造業

- エネルギーと公益事業

- 政府および公共部門

- その他のエンドユーザー産業

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- チリ

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- シンガポール

- マレーシア

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- エジプト

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Amazon Web Services

- Microsoft Corporation

- Google Cloud(Alphabet Inc.)

- IBM Corporation

- SAP SE

- Oracle Corporation

- Hewlett Packard Enterprise

- SAS Institute

- Accenture PLC

- Teradata Corporation

- Snowflake Inc.

- Databricks, Inc.

- Salesforce, Inc.

- Tableau Software, LLC

- QlikTech International AB

- MicroStrategy Incorporated

- TIBCO Software, Inc.

- Alteryx, Inc.

- Splunk Inc.

- Domo, Inc.

- Sisense Ltd.

- ThoughtSpot, Inc.

- Looker Studio(Google)

- GoodData, Inc.

- Zoho Analytics(Zoho Corporation)

第7章 市場機会と将来の動向

- ホワイトスペースと未充足ニーズの評価