|

市場調査レポート

商品コード

1628708

日本のプラスチック包装:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Japan Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 日本のプラスチック包装:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

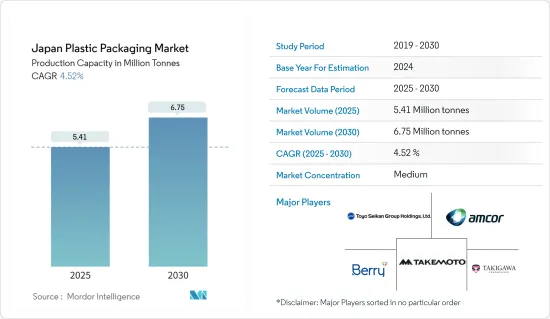

生産能力で見た日本のプラスチック包装市場規模は、予測期間中(2025~2030年)にCAGR 4.52%で、2025年の541万トンから2030年には675万トンに成長すると予測されます。

日本のプラスチック包装市場を牽引しているのは飲食品産業です。プラスチック包装は軽量で割れにくく、取り扱いが容易なため、消費者に支持されています。

主要ハイライト

- 日本では、耐久性、柔軟性、費用対効果の面でプラスチック包装が消費者に支持されています。この包装形態は、プラスチックフィルム、容器、その他のポリマー系材料を使用し、外的要因に対するバリアを形成します。この汎用性により、様々な商品を包装するための軽量なソリューションとなっています。飲食品、化粧品、医薬品などの産業では、プラスチック容器包装への依存度が高まっており、これが製品需要の原動力となっています。

- 日本のプラスチック容器包装メーカーは、多様な最終用途産業に合わせた硬質と軟質包装ソリューションの開発に注力することで、大幅な成長を遂げる態勢を整えています。2024年10月、Toppan Inc.はRM Tohcello、Mitsui Chemicals Inc.と共同で、量産に向けた再生BOPPフィルムの開発に成功しました。2024年10月よりサンプル配布を開始します。

- 新しい充填技術と耐熱性PETボトルの登場は、国内市場の可能性を広げました。需要の高まりを受けて、飲料メーカーは日本でのPETボトル生産を強化しています。

- 2024年9月、Coca-Cola Bottlers Japan Inc.(CCBJI)は、愛知県の東海工場で新しい無菌生産ラインを発表しました。このラインは毎分約600本の小型ペットボトル生産能力を誇り、CCBJIの需要急増への対応力を強化します。

- しかし、プラスチック廃棄物の急増により、日本の消費者はガラスや金属など、より環境に優しい包装材を求めるようになっています。同地域では、リサイクル可能で環境に優しいとされるアルミやガラスの採用が顕著に増加しています。このようなプラスチック離れが、将来の製品需要に課題をもたらす可能性があります。

日本のプラスチック包装市場の動向

ボトルと瓶が市場を独占する展望

- プラスチックの軽量性が需要の増加を後押し。日本では、ペットボトルと瓶への飲食品セクターの依存度が高まっていることが、プラスチック包装のニーズを後押ししています。

- ペットボトルの用途は飲料以外にも広がり、日本の化粧品や医薬品セグメントで脚光を浴びています。市場力学は、先進的充填技術や耐熱性PETボトルの発売といったイノベーションによって進化しています。PETボトルはさまざまなセグメントでリードしているが、ポリエチレン(PE)ボトルは飲料、化粧品、衛生用品、洗剤などの家庭用品に好んで選ばれています。

- 日本企業は飲料用PETボトルの生産を増やしており、この動向は市場成長を後押しします。2024年3月、日本の大手企業であるOtsuka Foodsは、炭酸ビタミン飲料「MATCH」シリーズの新製品2種を発売する計画を発表した:500mlペットボトルの「MATCHパイナップルソーダ」と260gペットボトルの「MATCHゼリー」です。

- 日本清涼飲料協会は、2030年までにボトルからボトルへのリサイクルを50%達成するという野心的な目標を掲げています。産業各社は、PET樹脂の使用量を減らすため、PETボトルの軽量化を進めています。日本清涼飲料協会(JSDA)のデータによると、日本のノンアルコール飲料部門では、PETボトルが鉄やガラスを追い越しました。さらに、政府の厳しい規制により、日本はPETボトルの回収とリサイクルの世界的リーダーとして位置づけられており、これが市場成長を刺激する要因となっています。

- 経済産業省の報告によると、日本の2023年のプラスチック包装生産量は前年比10万トン減(9.01%減)となりました。しかし、予測では2024年には109万トンに回復し、潜在的な市場成長を示唆しています。

著しい成長を遂げる飲料産業

- 日本の飲料産業は、健康志向の飲料に対する需要の高まりに後押しされて大きく拡大しています。消費者は、免疫力の向上、消化の改善、認知機能の鋭敏化など、健康上のメリットを約束する飲料にますます引き寄せられつつあります。この動向は、特に高齢者や、ライフスタイルに関連した健康課題に直面している人々の間で顕著です。

- 日本では、ペットボトルや容器によく見られる硬質プラスチック包装が、飲食品用途に広く支持されています。これらの製品の需要は、ジュース、炭酸清涼飲料、その他の飲料を包装するためのHDPEボトルやPETボトルの使用によって顕著に牽引されています。特筆すべきは、東洋製罐のようなメーカーが、飲料用途に特化した耐熱・耐圧PETボトルを生産していることです。

- 天然材料と科学的進歩の融合に焦点を当てた技術革新が、日本の飲料産業を再構築しています。2024年には、清涼飲料、スポーツドリンク、エナジードリンクといったセグメントが、機能性飲料に対する消費者の多様な嗜好を示すことになります。イノベーション、対象を絞ったマーケティング、持続可能性を優先することで、企業は急成長する日本の機能性飲料セグメントで骨格を固めることができます。

- さらに、米国農務省(USDA)のデータによると、日本のノンアルコール飲料市場は2023年に約400億米ドルと評価され、輸入が約10億米ドルを占めています。米国は日本のノンアルコール飲料の主要供給国であり、輸出は主にミネラルウォーターとジュースです。健康飲料とノンアルコール・ビールが主要な消費動向として台頭してきており、プラスチック包装の需要に大きな影響を及ぼしています。

- 日本のノンアルコール飲料に対する旺盛な購買意欲は、プラスチック包装セグメントを強化しています。日本の大手企業であるAsahi Group Holdingsの報告によると、2023年にはRTD(レディトゥドリンク)紅茶がソフトドリンクセグメントをリードし、売上高の約30%を占める。日本ではノンアルコール飲料タイプが多様なため、硬質包装と軟質包装の両方のソリューションに対する需要が高まっている

日本のプラスチック包装産業概要

日本のプラスチック包装市場は、Amcor Group、Takemoto Yohki、Toyo Seikan Group Holdings Ltd、Berry Global Inc.、Takigawa Corporationといった企業で主に構成され、事業拡大と市場シェアの拡大を目指し、製品イノベーション、コラボレーション、M&A、投資などの戦略を積極的に推進しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- 日本における複数のエンドユーザー産業向けプラスチック包装ソリューションの需要拡大

- 日本における飲料用プラスチックボトルの人気上昇

- 市場課題

- 日本におけるプラスチック包装のリサイクルに関する環境問題の高まり

第6章 産業の規制と施策と基準

第7章 市場内訳

- 包装タイプ別

- 軟質プラスチック包装

- 硬質プラスチック包装

- 製品タイプ別

- ボトルとジャー

- トレイと容器

- パウチ

- 袋

- フィルム・ラップ

- その他

- 産業別

- 食品

- 飲料

- 医療

- パーソナルケアと家庭用品

- その他

第8章 競合情勢

- 企業プロファイル

- Amcor Group

- Takemoto Yohki Co. Ltd.

- Berry Global

- Takigawa Corporation

- Toyo Seiken Group Holdings Ltd.

- Sonoco Products Company

- Sealed Air Corporation

- Hosokawa Yoko Co. ltd.

- Toppan Inc.

- Kodama Plastics Co. Ltd.

- ヒートマップ分析

- 競合他社分析-新興企業と既存企業

第9章 投資分析

第10章 市場の将来

The Japan Plastic Packaging Market size in terms of production capacity is expected to grow from 5.41 million tonnes in 2025 to 6.75 million tonnes by 2030, at a CAGR of 4.52% during the forecast period (2025-2030).

The food and beverage industry drives the plastic packaging market in Japan. Consumers favor plastic packaging for its lightweight and unbreakable nature, enhancing ease of handling.

Key Highlights

- In Japan, consumers favor plastic packaging for its durability, flexibility, and cost-effectiveness. This packaging form employs plastic films, containers, and other polymer-based materials, creating a barrier against external elements. This versatility makes it a lightweight solution for packaging various goods. Industries such as beverage, food, cosmetics, and pharmaceuticals increasingly rely on plastic container packaging, which drives the product demand.

- Japanese manufacturers of plastic packaging are poised for substantial growth by focusing on the development of both rigid and flexible packaging solutions tailored to diverse end-use industries. In October 2024, Toppan Inc., in collaboration with RM Tohcello Co. Ltd. and Mitsui Chemicals Inc., has successfully created a recycled BOPP film primed for mass production. Starting October 2024, these companies will commence the distribution of samples for this innovative film.

- New filling technologies and the advent of heat-resistant PET bottles have broadened market possibilities in the country. In response to rising demand, beverage manufacturers are ramping up PET bottle production in Japan.

- In September 2024, Coca-Cola Bottlers Japan Inc. (CCBJI) unveiled a new aseptic production line at its Tokai Plant in Aichi Prefecture. This line boasts a production capacity of around 600 small PET bottles per minute, bolstering CCBJI's ability to meet surging demand.

- However, a surge in plastic waste has led Japanese consumers to gravitate towards eco-friendlier packaging materials such as glass and metal. The region has seen a notable uptick in the adoption of aluminum and glass, celebrated for their recyclability and eco-friendly attributes. This shift away from plastic could pose challenges for product demand in the future.

Japan Plastic Packaging Market Trends

Bottles and Jars Segment is Expected to Dominate the Market

- The lightweight nature of plastics fuels their rising demand. In Japan, the food and beverage sector's increasing reliance on plastic bottles and jars propels the need for plastic packaging.

- Plastic bottles extend their utility beyond beverages, finding prominence in Japan's cosmetics and pharmaceuticals sectors. Market dynamics are evolving with innovations like advanced filling technologies and the launch of heat-resistant PET bottles. While PET bottles lead in various sectors, polyethylene (PE) bottles are the preferred choice for beverages, cosmetics, sanitary items, and household items such as detergents.

- Japanese companies are increasingly producing PET bottles for beverages, a trend poised to fuel market growth. In March 2024, Otsuka Foods Co., Ltd., a prominent player based in Japan, unveiled its plans to launch two new products in its MATCH line of carbonated vitamin drinks: MATCH Pineapple Soda in a 500-ml PET bottle and MATCH Jelly in a 260-gram PET bottle in the Japanese market.

- The Japan Soft Drink Association has set an ambitious goal of achieving 50% bottle-to-bottle recycling by 2030. Industry players are lightening the weight of PET bottles to reduce the amount of PET resin used. Data from the Japan Soft Drink Association (JSDA) highlights that PET bottles have overtaken steel and glass in the country's non-alcoholic beverage sector. Furthermore, stringent government regulations have positioned Japan as a global leader in PET bottle collection and recycling, a factor poised to stimulate market growth.

- As reported by the Ministry of Economy, Trade and Industry (METI) Japan, the country's plastic packaging production saw a dip of 0.1 million tons (-9.01 percent) in 2023 compared to the prior year. However, projections indicate a rebound to 1.09 million tons in 2024, signaling potential market growth.

Beverage Industry Set for Significant Growth

- Japan's beverage industry is expanding significantly, fueled by a rising demand for health-oriented drinks. Consumers are increasingly gravitating towards beverages that promise health benefits, including immunity enhancement, better digestion, and sharper cognitive functions. This trend is especially evident among the elderly and those facing health challenges linked to their lifestyles.

- In Japan, rigid plastic packaging, commonly found in plastic bottles and containers, is widely favored for food and beverage applications. The demand for these products is notably driven by the use of HDPE and PET bottles for packaging juices, carbonated soft drinks, and other beverages. Notably, manufacturers such as Toyo Seikan Co. Ltd. are producing heat and pressure-resistant PET bottles tailored specifically for beverage applications.

- Innovations are reshaping Japan's beverage landscape, with a focus on merging natural ingredients and scientific advancements. In 2024, segments such as soft drinks, sports drinks, and energy drinks are poised to showcase the varied consumer preferences for functional beverages. By prioritizing innovation, targeted marketing, and sustainability, companies can cement their foothold in Japan's burgeoning functional beverage arena.

- Additionally, data from the US Department of Agriculture (USDA) reveals that Japan's non-alcoholic beverage market was valued at approximately USD 40 billion in 2023, with imports accounting for about USD 1 billion. The U.S. stands as Japan's chief supplier of non-alcoholic drinks, with exports predominantly comprising mineral water and juices. Healthy beverages and non-alcoholic beers are emerging as leading consumer trends, significantly influencing the demand for plastic packaging.

- Japan's surging appetite for non-alcoholic drinks is bolstering its plastic packaging sector. As reported by Asahi Group Holdings, a prominent Japanese firm, Ready-to-Drink (RTD) tea led the soft drinks segment in 2023, capturing roughly 30% of sales. The diverse range of non-alcoholic beverages in Japan is driving a heightened demand for both rigid and flexible packaging solutions in the nation.

Japan Plastic Packaging Industry Overview

The Japanese plastic packaging market is moderately consolidated with the presence of global and domestic players such as Amcor Group, Takemoto Yohki Co. Ltd, Toyo Seikan Group Holdings Ltd, Berry Global Inc. and Takigawa Corporation. These companies are actively pursuing strategies such as product innovations, collaborations, mergers and acquisitions, and investments to expand their business and capture a larger market share.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand of Plastic Packaging Solutions for Multiple End-User Industries in Japan

- 5.1.2 Rising Popularity of Plastic Bottles for Beverage Industry in Japan

- 5.2 Market Challenges

- 5.2.1 Increasing Environmental Concerns Regarding Plastic Packaging Recycling in Japan

6 INDUSTRY REGULATION, POLICY AND STANDARDS

7 MARKET SEGEMENTATION

- 7.1 By Packaging Type

- 7.1.1 Flexible Plastic Packaging

- 7.1.2 Rigid Plastic Packaging

- 7.2 By Product Type

- 7.2.1 Bottles and Jars

- 7.2.2 Trays and containers

- 7.2.3 Pouches

- 7.2.4 Bags

- 7.2.5 Films and Wraps

- 7.2.6 Other Product Types

- 7.3 By End-User Vertical

- 7.3.1 Food

- 7.3.2 Beverage

- 7.3.3 Healthcare

- 7.3.4 Personal Care and Household

- 7.3.5 Other End-Users

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Amcor Group

- 8.1.2 Takemoto Yohki Co. Ltd.

- 8.1.3 Berry Global

- 8.1.4 Takigawa Corporation

- 8.1.5 Toyo Seiken Group Holdings Ltd.

- 8.1.6 Sonoco Products Company

- 8.1.7 Sealed Air Corporation

- 8.1.8 Hosokawa Yoko Co. ltd.

- 8.1.9 Toppan Inc.

- 8.1.10 Kodama Plastics Co. Ltd.

- 8.2 Heat Map Analysis

- 8.3 Competitor Analysis - Emerging vs. Established Players