|

市場調査レポート

商品コード

1550509

日本のHVAC:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Japan HVAC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 日本のHVAC:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

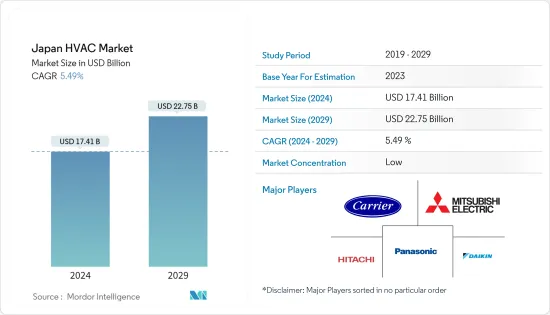

日本のHVAC市場規模は2024年に174億1,000万米ドルと推定され、2029年には227億5,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは5.49%で成長すると予測されます。

主なハイライト

- HVACは、アパート、一戸建て住宅、ホテル、高齢者施設などの住宅や、病院などの中規模から大規模の産業・オフィス構造物など、さまざまな環境で不可欠な役割を果たしています。HVACシステムは、温度と湿度を制御し、新鮮な外気を取り入れることで、安全で健康的な環境づくりに役立っています。

- 日本のHVAC市場の成長は、主に急速な工業化と都市化によって促進されています。工業用、商業用、住宅用ビルの建設急増が、HVAC市場の大幅な需要につながっています。

- 日本では、かなりの数の個人が地方から都市部に移転しており、その結果、住宅、商業建設、産業インフラへの投資が増加しています。新しく建設された建物に新しいHVAC機器を設置する必要性が、市場の成長をさらに後押ししています。

- 日本では、データセンターなどの用途で液冷システムの需要が高まっています。国内におけるデータセンターの拡大が、HVAC機器とサービスの需要をさらに押し上げると思われます。例えば、Amazon Web Services Inc.は2024年1月、2027年までに日本に152億4,000万米ドルを投資し、地域のデータセンター・ネットワークを強化する予定です。このインフラ拡充は、日本の国内総生産(GDP)に約380億米ドル寄与すると、Amazon.com Inc.の子会社は述べています。

- HVACサービス市場には、労働力不足という顕著な課題が見られます。とはいえ、こうした障害にもかかわらず、メーカーやその他のサービス・プロバイダーによる積極的な対策のおかげで、市場は繁栄してきました。

- 日本のHVAC市場は断片化されており、多数のプレーヤーが小さな市場シェアを占めています。この業界で事業を展開するベンダーは、高まる顧客需要に対応するため、新製品開発、戦略的提携、買収、事業拡大に注力しており、市場の成長をさらに後押ししています。

- 例えば、2024年6月、Carrier Corporationは、快適性とエネルギーソリューションのための新しいサービスベースのモデルの立ち上げを発表しました。Carrierが提供するCooling-as-a-Serviceにより、顧客はシステムや機器購入のための初期資本支出に直面する代わりに、拡張された性能と一貫した支払いを確保することができます。この革新的な財務アプローチにより、顧客は本来の業務に専念することができ、キャリアの総合的な専門知識を活用して快適性と業務効率を確保することができます。

- さらに、日本では公害レベルが上昇しており、環境にやさしい建物を重視する傾向が強まっています。

- 日本のHVAC市場は、政府の規制やエネルギー効率の高い機器の採用を後押しする新たな取り組みといったマクロ経済的要因の影響を強く受けています。例えば、日本は2030年までに温室効果ガス排出量を46%削減することを目指しており、さらに野心的な50%削減を達成することを確約しています。

日本のHVAC市場の動向

HVAC機器が大きな市場シェアを占める

- 屋内外の空気環境の改善に対するニーズの高まりが、日本におけるHVAC機器の拡大を促す主な要因となっています。空気の質の重要な役割に対する認識が高まり、住宅所有者や事業主は、室内の空気を効果的にろ過・浄化し、屋外の排気を最小限に抑えることのできるHVACシステムを購入するようになっています。

- エアハンドリングユニット(AHU)のような換気システムは、ショッピングセンターのような、多数の個人が頻繁に出入りする広々とした施設で頻繁に利用されます。このような施設では、空気の質やCO2レベルに関する厳しい規制を遵守することが求められます。エアハンドリングユニットは、外気を室内に導入することで、大規模施設で一般的に使用される複数の送風ファンの必要性を効果的に減らすことができます。

- ヒートポンプは、冷凍サイクルを通じて、寒いエリアから暑いエリアへ熱を移動させる必要不可欠なHVAC機器です。その結果、寒い地域は冷やされ、暑い地域は暖められます。気温が低いときには、ヒートポンプは外部環境から熱を取り込んで家を暖め、気温が高いときには、家の中の熱を屋外に排出することができます。ヒートポンプは、熱を発生させるのではなく、熱を移動させることができることから、住宅用の代替冷暖房システムよりもエネルギー効率が高いと考えられています。

- 日本会員国レポートでは、日本におけるヒートポンプの進歩にも焦点を当て、2050年のネット・ゼロを目標とする最新の法律に焦点を当てています。政府は、脱炭素化のための重要な技術として、産業用HP(IHP)および業務用・家庭用ヒートポンプ給湯機(HPWH)の具体的な目標を設定し、ヒートポンプの利用を積極的に推進しています。

- エアコン(AC)市場は、家庭用ルームエアコンの成長が見込まれますが、この目標を効果的に達成するためには、産業用HPとHPWHの普及を加速させることが急務です。したがって、国内での建設活動の活発化は、HVAC機器の採用を促進すると思われます。国土交通省によると、2023年に日本では約9,580件のオフィス建設プロジェクトが開始され、その総床面積は前年と同じでした。

住宅部門が大きな市場シェアを占めています。

- 地方から都心への人口移動の増加に伴い、住宅開発が急増しています。その結果、HVAC機器のニーズにも直接的な影響が及んでいます。こうした建物では、拡大する都市人口に対応するため、効果的な冷房および空気品質管理システムが必要とされるからです。

- 国土交通省によると、2023年には日本で約81万9,600戸の住宅建設が開始されます。民間部門による住宅建設投資は、2023年度には17兆4,000億円に増加すると予測されました。同様に、日本では2023年度に約36万6,800戸の戸建住宅が着工されます。

- 日本の住宅部門では、空調・換気システムの需要が増加しています。空調・換気システムは、濾過と換気を用いて室内の空気の質を保つ上で重要な役割を果たします。大気汚染レベルの上昇とウィルスの蔓延が、空気質の改善を実現するためのより高度なHVACシステムの必要性を後押ししています。

- 住宅産業におけるHVAC機器の定期的なメンテナンスと修理は、HVACシステムのピーク性能を保証するため、国内のHVACサービスの需要を増加させます。定期的なHVACの維持管理と修理の一つの重要な利点は、システムの有効性を高める能力です。適切なメンテナンスが行われない場合、システムは運用上の課題に直面し、エネルギー使用量の増加や長期的な出費の増加につながる可能性があります。住宅分野での効率的な慣行に対する需要の高まりに伴い、HVACサービスに対する要求も高まると思われます。

- 国内のプレーヤーは、大きな市場シェアを獲得するために存在感の拡大に注力しており、市場の成長をさらに後押ししています。例えば、Daikin Industries Ltdは2023年8月、茨城県つくばみらい市に土地を購入し、エアコンの新製造施設を建設すると発表しました。この戦略的移転は、同社の現地生産能力を強化し、日本市場でのプレゼンス拡大という目標をサポートするものです。

日本のHVAC産業の概要

日本のHVAC市場は断片化されており、複数のプレーヤーで構成されています。各社は、新製品の導入、事業の拡大、戦略的M&A、提携、協業への参入によって、市場での存在感を高めようと絶えず努力しています。主なプレーヤーには、Carrier Corporation、Daikin Industries Ltd、Mitsubishi Electric Corporation、Hitachi Ltd、Panasonic Corporationなどがあります。

- 2024年5月、Daikin Industries Ltdと産業用ボイラーメーカーのMiuraは、資本・業務提携の計画を明らかにしました。全国の工場向けに、暖房、換気、空調、蒸気ボイラー、水処理システムなど総合的なソリューション提案を目指します。

- 2024年5月、Carrier Corporationは、大型施設向けHVACソリューションを拡充するため、ターボ冷凍機「Carrier AquaEdge 19DV」シリーズを日本に導入しました。この新シリーズ「AquaEdge 19DV」は、日本で好評のモジュール式チラー「Universal Smart X」シリーズに加わる貴重な製品です。AquaEdge 19DVシリーズは、日本の商業施設のお客様のご要望にお応えするよう設計されており、効率性と快適性の両方を保証する最先端で信頼性の高いシステムを提供します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 業界バリューチェーン分析

- COVID-19の副作用とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- 税額控除プログラムによる省エネ奨励を含む政府の支援規制

- エネルギー効率の高い機器に対する需要の増加

- 需要を支える建設と改修活動の増加

- 市場の課題

- エネルギー効率の高いシステムの初期コストの高さ

第6章 市場セグメンテーション

- 部品タイプ別

- HVAC機器

- 暖房機器

- 空調・換気機器

- HVACサービス

- HVAC機器

- エンドユーザー産業別

- 住宅

- 商業

- 産業用

第7章 競合情勢

- 企業プロファイル

- Johnson Controls International PLC

- Carrier Corporation

- Robert Bosch GmbH

- Daikin Industries Ltd

- Midea Group Co. Ltd

- System Air AB

- LG Electronics Inc.

- Mitsubishi Electric Corporation

- Danfoss A/S

- Lennox International Inc.

- Hitachi Ltd

- Panasonic Corporation

第8章 投資分析

第9章 市場の将来

The Japan HVAC Market size is estimated at USD 17.41 billion in 2024, and is expected to reach USD 22.75 billion by 2029, growing at a CAGR of 5.49% during the forecast period (2024-2029).

Key Highlights

- HVAC plays an essential role in various settings, including residential buildings like apartments, single-family homes, hotels, and senior living facilities, as well as in medium-to-large industrial and office structures such as hospitals. HVAC systems help create safe and healthy environments by controlling temperature and humidity and incorporating fresh outdoor air.

- Japan's HVAC market growth is primarily fueled by swift industrialization and urbanization. The surge in industrial, commercial, and residential building construction is leading to a substantial demand for the HVAC market.

- In Japan, a significant number of individuals have relocated from rural to urban areas, resulting in increased investments in housing, commercial construction, and industrial infrastructure. The need to install new HVAC equipment in newly constructed buildings further propels the market growth.

- Japan has been witnessing a demand for liquid cooling systems for applications such as data centers. The increasing expansion of data centers in the country will further drive the demand for HVAC equipment and services. For instance, in January 2024, Amazon Web Services Inc. plans to invest USD 15.24 billion in Japan by 2027 to enhance its local data center network. The expansion of infrastructure is expected to contribute approximately USD 38 billion to Japan's gross domestic product, as stated by the Amazon.com Inc. subsidiary.

- The HVAC services market has seen a notable challenge in the form of a labor shortage. Nevertheless, despite these obstacles, the market has thrived thanks to the proactive measures taken by manufacturers and other service providers.

- The HVAC market in Japan is fragmented, with a large number of players occupying a small market share. Vendors operating in the industry are focusing on new product development, strategic partnership, acquisition, and expansion to meet the rising customer demand, further supporting the market growth.

- For instance, in June 2024, Carrier Corporation announced the launch of a new service-based model for comfort and energy solutions. Carrier's cooling-as-a-service offering enables customers to secure extended performance and consistent payments instead of facing an initial capital expense for system or equipment acquisitions. This innovative financial approach empowers customers to concentrate on their primary operations, leveraging Carrier's comprehensive expertise to ensure comfort and operational effectiveness.

- Additionally, the rising pollution levels in Japan are driving the nation to enhance its emphasis on eco-friendly buildings, potentially opening up numerous opportunities for businesses to invest and grow in the Japanese HVAC market.

- The HVAC market in Japan is highly affected by macroeconomic factors such as government regulations and new initiatives to boost the adoption of energy-efficient equipment. For instance, Japan aims to cut its greenhouse gas emissions by 46% by 2030, steadfastly committed to achieving an even more ambitious 50% reduction.

Japan HVAC Market Trends

HVAC Equipment Holds Significant Market Share

- The increasing need for better indoor and outdoor air quality is a major factor fueling the expansion of HVAC equipment in Japan. Growing recognition of the crucial role of air quality encourages homeowners and business owners to purchase HVAC systems that can effectively filter and purify indoor air and minimize outdoor emissions.

- Ventilation systems, such as air handling units (AHUs), are frequently utilized in spacious establishments that numerous individuals, such as shopping centers, frequently access. These establishments are required to adhere to strict regulations concerning air quality and CO2 levels. By introducing outside air into the rooms, air handling units can effectively decrease the necessity for multiple blower fans typically used in large facilities.

- Heat pumps are essential HVAC equipment that moves heat from a colder area to a hotter area through a refrigeration cycle. This results in cooling the colder area and warming the hotter area. During colder temperatures, a heat pump is able to draw heat from the external environment to warm a home, whereas during hotter temperatures, it can expel heat from the house to the outdoors. Heat pumps are considered more energy-efficient than alternative heating or cooling systems for residential use, considering the capability of heat pumps to transfer heat rather than produce it.

- The Japan Member Country Report also focused on the advancement of heat pumps in Japan, highlighting the latest legislation targeting 2050 net zero. The government is actively promoting the use of heat pumps by setting specific targets for industrial HPs (IHP) and commercial and household heat pump water heaters (HPWH) as crucial technologies for decarbonization.

- Although the air conditioners (AC) market will witness growth in residential room ACs, there is a pressing need for accelerated deployment of industrial HPs and HPWHs to effectively achieve the outlined goals. Thus, the growing construction activities in the country will propel the adoption of HVAC equipment. According to MLIT (Japan), in 2023, Japan initiated approximately 9,580 office construction projects, the total floor area of which remained consistent with the previous year.

Residential Segment Holds Significant Market Share

- The rise in rural populations moving to urban centers has resulted in a surge in the development of residential structures. Consequently, there has been a direct impact on the need for HVAC equipment, as these buildings necessitate effective cooling and air quality management systems to cater to the expanding urban populace.

- According to MLIT Japan, in 2023, approximately 819.6 thousand housing units were initiated in Japan. Residential construction investment by the private sector was forecasted to increase to JPY 17.4 trillion in fiscal year 2023. Similarly, in Japan, construction began on approximately 366.8 thousand detached houses in 2023.

- The demand for air conditioning and ventilation systems in Japan's residential sector is increasing. AC and ventilation systems play a crucial role in preserving indoor air quality using filtration and ventilation. The rising levels of air pollution and the spread of viruses drive the need for more advanced HVAC systems to deliver improved air quality.

- Regular maintenance and repairs of the HVAC equipment in the residential industry guarantee peak performance of HVAC systems, thus increasing demand for HVAC services in the country. One key benefit of routine HVAC upkeep and repairs is the capacity to enhance the system's effectiveness. In the absence of proper maintenance, the system could encounter operational challenges, leading to heightened energy usage and greater expenses over time. With the growing demand for efficient practices in the residential sector, the requirement for HVAC services will also grow.

- The players in the country are focusing on expanding their presence to capture a significant market share, further supporting the market growth. For instance, in August 2023, Daikin Industries Ltd announced that it would purchase land in Tsukubamirai City, Ibaraki Prefecture, Japan, to create a new manufacturing facility for air conditioners. This strategic move will enhance the company's local production capabilities and support its goal of expanding its presence in the Japanese market.

Japan HVAC Industry Overview

The Japanese HVAC market is fragmented and consists of several players. Companies continuously try to increase their market presence by introducing new products, expanding their operations, or entering strategic mergers and acquisitions, partnerships, and collaborations. Some of the major players include Carrier Corporation, Daikin Industries Ltd, Mitsubishi Electric Corporation, Hitachi Ltd, Panasonic Corporation, and many more.

- May 2024: Daikin Industries Ltd and Miura Co. Ltd, an industrial boiler manufacturer, revealed their plans to establish a capital and business alliance. This collaboration aims to offer comprehensive solution proposals encompassing heating, ventilation, air conditioning, steam boilers, and water treatment systems for factories throughout Japan.

- May 2024: Carrier Corporation introduced the Carrier AquaEdge 19DV centrifugal chiller series in Japan, expanding its HVAC solutions for large-scale facilities. This new series, AquaEdge 19DV, will be a valuable addition to the popular Universal Smart X series of modular chillers in Japan. The AquaEdge 19DV series is designed to meet the demands of commercial customers in Japan, providing a cutting-edge and reliable system that guarantees both efficiency and comfort.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Supportive Government Regulations Including Incentives for Saving Energy through Tax Credit Programs

- 5.1.2 Increasing Demand For Energy Efficient Devices

- 5.1.3 Increased Construction And Retrofit Activity To Aid Demand

- 5.2 Market Challenges

- 5.2.1 High Initial Cost of Energy Efficient Systems

6 MARKET SEGMENTATION

- 6.1 By Type of Component

- 6.1.1 HVAC Equipment

- 6.1.1.1 Heating Equipment

- 6.1.1.2 Air Conditioning /Ventilation Equipment

- 6.1.2 HVAC Services

- 6.1.1 HVAC Equipment

- 6.2 By End-user Industry

- 6.2.1 Residential

- 6.2.2 Commercial

- 6.2.3 Industrial

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Johnson Controls International PLC

- 7.1.2 Carrier Corporation

- 7.1.3 Robert Bosch GmbH

- 7.1.4 Daikin Industries Ltd

- 7.1.5 Midea Group Co. Ltd

- 7.1.6 System Air AB

- 7.1.7 LG Electronics Inc.

- 7.1.8 Mitsubishi Electric Corporation

- 7.1.9 Danfoss A/S

- 7.1.10 Lennox International Inc.

- 7.1.11 Hitachi Ltd

- 7.1.12 Panasonic Corporation