|

市場調査レポート

商品コード

1550201

GCC通信:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)GCC Telecom - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| GCC通信:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

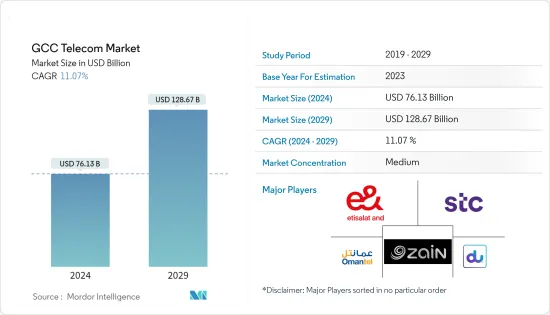

GCC通信市場規模は2024年に761億3,000万米ドルと推定され、2029年には1,286億7,000万米ドルに達し、予測期間中(2024-2029年)のCAGRは11.07%で成長すると予測されます。

主なハイライト

- 湾岸協力会議(GCC)地域の通信セクターは、主に都市人口の増加と3G、4G、5Gサービスを可能にする携帯電話の普及により拡大が見込まれています。有線・無線インターネットと接続するモノのインターネット(IoT)は、予測期間を通じて通信業界でより多く利用されると予測されます。

- 2023年11月のエリクソン・モビリティ・レポートによると、GCCのモバイル契約数は2023年の7,600万件から2029年には8,100万件に増加すると予想されています。2023年末までに、5G契約は全モバイル契約の34%を占め、合計2,600万契約になると予測されました。予測期間中、5G契約数は年率19%で成長し、2029年には7,500万契約に達し、総契約数の約90%を占めると予測されます。

- GCC通信市場は近年大きな変化を経験しています。こうした変化の背景には、インターネット・インフラとブロードバンド接続の強化を目指した政府の取り組み、企業と個人の双方によるデータ消費の増加、5G技術の普及、大手通信ベンダーが導入したイノベーションなどがあります。

- 2024年4月、サウジアラビアのリヤドで開催されたLEAP 2024において、エリクソンとエティハド・エティサラット(モビリー)は覚書に調印しました。この提携は、ネットワークの柔軟性を高めることに重点を置き、オープンな無線アクセスネットワーク(RAN)の原則を使用して、サウジアラビアのネットワークを強化・進化させることを目的としています。このイニシアチブの一環として、両社は専用RANやクラウドRANなど、柔軟なネットワーク・アーキテクチャにおけるさまざまな5G展開オプションを検討します。

- 例えば、サウジアラビアのビジョン2030にとって極めて重要なプラットフォームは、サウジアラビアの全国ブロードバンドネットワークです。サウジアラビアの中央政府は、包括的なファイバー・ネットワークを構築するため、多大な資源と政策に資金を提供することを目指しています。この地域は、ファイバーとブロードバンドネットワークの分野で多くのパートナーシップと開発しており、国の全体的な電気通信セクターを強化しています。

- 通信事業者は市場競争の激化に直面しています。そのため、通信事業者はコストと価格設定の最適化を図り、事業者間でタワーを共有するようになっています。このため、通信事業者の重点分野は、ネットワーク・カバレッジ、ブランド、サービス・デザインからタワー・シェアリングへと大きくシフトしています。タワーのシェアリングは、運用コストや資本コストを削減する可能性があり、通信事業者はマーケティングや顧客満足度により効果的に集中することができます。

- COVID-19の大流行後、GCC通信市場はデジタルサービスや遠隔接続ソリューションの需要増を原動力に著しい成長を遂げました。アラブ首長国連邦やサウジアラビアなどの国々では、eコマースやデジタル決済が急増し、通信料収入が増加しました。カタールやバーレーンも、5Gインフラへの投資による技術革新と市場競争力の拡大が見られました。全体として、パンデミックはデジタルトランスフォーメーションを加速させ、GCC通信セクターを新たな高みへと押し上げました。

GCC通信市場の動向

モバイルネットワークが市場を牽引

- サウジアラビア、アラブ首長国連邦、オマーンなどは、堅牢なインフラの恩恵を受けています。スマートシティを継続的に拡大するためには、テクノロジー主導の開発を構想し、革新することに主眼が置かれると予想されます。これらの国々では、人々はほとんどの時間をソーシャルアプリやコミュニケーションアプリに費やしています。スマートフォンの使用頻度や使用頻度を考えると、企業は無数の方法で顧客とつながっています。こうした要因が、同国でのスマートフォン普及を後押ししています。

- アラブ首長国連邦では現在、統一ライセンスを持つ3社が大きなシェアを占めている:Mobile Telecommunication Company Saudi Arabia、Etihad Etisalat Company、Saudi Telecom Company(STC)です。

- その他のインターネット・サービス・プロバイダー(ISP)、モバイル・バーチャル・ネットワーク・オペレーター(MVNO)、固定回線サービス・プロバイダーも市場に存在しています。先進的なインフラや技術に対応した透明性の高い競争市場の形成は、政府によって実現された部分が大きいです。

- さらに、e&EtisalatやSaudi Telecom Company(STC)といった企業が主要企業であり、データ、音声、メッセージングに対する需要の高まりに応えるモバイル・サービスを提供しています。これらの企業は、この拡大する市場で顧客を引き付け、維持するために、競争力のある価格、より良いカバレッジ、改善されたサービスを提供するために継続的に技術革新を行っています。新興プレーヤーや技術の進歩もまた、GCC通信業界のダイナミックな情勢に貢献しています。

- 2024年2月、パワー・インターナショナル・ホールディング(PIH)は、カザフスタンのモバイル・テレコム・サービス(MTS)を買収することで合意に達しました。MTSは現在、国営通信会社カザフテレコムが所有しています。

- オマーンでは、5G技術が市場で利用可能になるにつれて、モバイル・エコシステムがこれまで以上に大規模に変化しています。5Gによって新たな機能が導入され、通信事業者は消費者、ビジネス、その他の分野や市場で新たな使用事例、アプリケーション、サービス、収益源を開発できるようになります。

著しい成長が期待されるサウジアラビア

- 2030年ビジョンの国家変革プログラムの一環として、サウジアラビア通信情報技術省はFTTH超高速ブロードバンドネットワークの展開を奨励する政策を発表しました。政府は通信会社に対し、サービスが行き届いていない地域に光ファイバーを敷設するよう補助金を出しています。

- Saudi Data and Artificial Intelligence Authorityは、データとAIを活用した新興経済諸国を発展させることで、サウジアラビアを世界の技術提供国として確立したいと考えています。サウジアラビアは人工知能に一定の投資を行っており、政府は国家のデジタル化に力を注いでいます。この投資は主に、同国の政府系ファンドを中心とする地元の資金源によって推進されています。

- サウジテレコム(STC)、ザイン(Zain)、モビリー(Mobily)の大手モバイルサービスプロバイダーも5G拡張プログラムを継続しており、サウジアラビアでは効率的で低遅延、広帯域のモバイルデータ・音声サービスへの需要が高まっています。

- 2024年4月、サウジアラビアの政府系ファンドであるThe Public Investment Fund(PIF)は、モバイルネットワーク事業者であるSaudi Telecommunications Company(stcグループ)と、PIFがstcグループからTelecommunication Towers Company(TAWAL)の株式51%を取得する契約を締結しました。

- 通信・宇宙・技術委員会によると、サウジアラビアのインターネット速度は2021年の96.4Mbpsから2023年には153.1Mbpsへと大幅に向上し、通信市場の大幅な成長を促しています。この高速化により、より高速なデータトランスミッションが可能になり、ユーザーエクスペリエンスが向上し、ストリーミングやクラウドコンピューティングのような帯域幅を必要とするサービスの導入が促進されます。その結果、通信事業者は高速インターネット・パッケージに対する需要の高まりを目の当たりにし、市場の競争と技術革新を促進しています。

- 全体として、この成長は電気通信、金融、政府、石油・ガス分野が牽引しています。電子政府構想や通信業界の自由化など、サウジアラビア政府のITインフラを近代化するための積極的なITプロジェクトが、競争、サービスレベル、利用率を高めています。

GCC通信業界の概要

GCC通信市場は緩やかに統合されつつあります。同市場の主要企業には、e&Etisalat、Saudi Telecom Company(STC)、Oman Telecommunications Company(Omantel)などがあります。また、インターネット・サービス・プロバイダー(ISP)、MVNO、固定回線サービス・プロバイダーも市場に進出しています。これらのプレーヤーは、市場競争力を維持するために、5Gネットワークの展開と地域全体のネットワーク容量の増加に注力しています。例えば

- 2024年5月、Zain KSAはインフラ、5Gネットワーク、デジタルサービスのエコシステムの拡大に16億SAR(4億3,000万米ドル)を投資しました。この動きは、Zain KSAの国全体のデジタル・インクルージョンを達成するための戦略に沿った統合的な拡大計画の一環です。目標は、5Gネットワークを現在の66都市から122都市・州をカバーするまでに拡大することで、デジタルインフラを強化し、卓越した顧客体験を提供することです。

- 2024年3月、エリクソンとEmirates Integrated Telecommunication CompanyのDuは戦略的提携を結び、エリクソンに無線ネットワーク製品を提供し、アラブ首長国連邦の企業部門と政府へのインテリジェントサービスを実現します。エリクソンとデュは、先進的なプライベート4Gおよび5Gネットワークを構築するための戦略的パートナーシップを結びました。両社の提携は、政府機関や企業顧客の接続性を強化し、同国におけるインダストリー4.0の導入を可能にすることを目的としています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19が業界に与える影響の評価

第5章 市場力学

- 市場促進要因

- 5Gに対する莫大な需要

- インターネットとスマートフォンの大幅な普及

- 産業界におけるデジタルトランスフォーメーションの高まり

- 市場抑制要因

- セキュリティ上の脅威と個人情報の漏えい

- 高度な通信インフラに伴う多額の設備投資

- エコシステム分析

- タワー企業

- OEMS(スモールセル、DASなど)

- MNO

- MVNO

- OTT/PayTV

- GCC通信セクターの進化

- 2G、3G、4G、5G接続

- GCCテレコムの主要指標

- 人口

- 固定ブロードバンド契約数

- 携帯電話契約数

- ベンダーの市場参入戦略の分析

第6章 市場セグメンテーション

- 通信収入全体

- 通信契約数

- ユーザー1人当たりの平均収入

- 通信サービス

- 音声サービス

- 有線

- ワイヤレス

- データ通信サービス

- ペイTVサービス

- 音声サービス

- テレコム接続

- 固定ネットワーク

- モバイルネットワーク

- 国名

- サウジアラビア

- クウェート

- カタール

- オマーン

- アラブ首長国連邦

- バーレーン

第7章 競合情勢

- 主要ベンダーの市場シェア分析

- 企業プロファイル

- e&(Etisalat and)

- Saudi Telecom Company(STC)

- Ooredoo Group

- Zain Group

- Oman Telecommunications Company(Omantel)

- Emirates Integrated Telecommunications Company(Du)

- Mobily(Etihad Etisalat Company)

- Batelco(Bahrain Telecommunication Company)

第8章 *リストは暫定的なものであり、実際の調査過程で変更される可能性があります。

第9章 投資分析

第10章 市場機会と今後の動向

The GCC Telecom Market size is estimated at USD 76.13 billion in 2024, and is expected to reach USD 128.67 billion by 2029, growing at a CAGR of 11.07% during the forecast period (2024-2029).

Key Highlights

- The telecom sector in the Gulf Cooperation Council (GCC) region is anticipated to expand primarily due to the growing urban population and the widespread use of cell phones that enable 3G, 4G, and 5G services. The Internet of Things (IoT), which connects with wired and wireless internet, is predicted to be used more in the telecom industry throughout the forecast period.

- According to the November 2023 Ericsson Mobility Report, mobile subscriptions in GCC are expected to increase from 76 million in 2023 to 81 million by 2029. By the end of 2023, 5G subscriptions were projected to constitute 34% of all mobile subscriptions, totaling 26 million subscriptions. Over the forecast period, 5G subscriptions are projected to grow annually at 19%, reaching 75 million by 2029 and accounting for approximately 90% of total subscriptions.

- The GCC telecommunications market has experienced substantial changes in recent years. These shifts are attributed to government efforts aimed at enhancing internet infrastructure and broadband connectivity, increased data consumption by both businesses and individuals, widespread adoption of 5G technology, and innovations introduced by major telecom vendors.

- In April 2024, Ericsson and Etihad Etisalat (Mobily) signed a memorandum of understanding (MoU) during LEAP 2024 in Riyadh, Saudi Arabia. The collaboration aims to enhance and evolve the network in Saudi Arabia using open radio access network (RAN) principles, with a focus on boosting network flexibility. As part of this initiative, they will explore different 5G deployment options within a flexible network architecture, including purpose-built RAN and Cloud RAN.

- For instance, a crucial platform for Saudi Arabia's Vision 2030 is the National Broadband Network of Saudi Arabia. The central government aims to finance significant resources and policies to create an all-encompassing fiber network. The region is witnessing many partnerships and developments in the fiber and broadband network area, strengthening the nation's overall telecom sector.

- Telecom operators face intensifying market competition. Thus, they are looking to optimize costs and pricing, giving rise to tower sharing amongst the operators. This has led to a significant shift in the focus area of telecom operators from network coverage, branding, and service design to tower sharing. Tower sharing provides potential reductions in operating and capital costs, which helps the telecom operator focus more effectively on marketing and customer satisfaction, thereby increasing the network reach.

- After the COVID-19 pandemic, the GCC telecom market experienced notable growth driven by increased demand for digital services and remote connectivity solutions. Countries like the United Arab Emirates and Saudi Arabia saw a surge in e-commerce and digital payments, boosting telecom revenues. Qatar and Bahrain also witnessed expansion, with investments in 5G infrastructure driving innovation and market competitiveness. Overall, the pandemic accelerated digital transformation, propelling the GCC telecom sector to new heights.

GCC Telecom Market Trends

Mobile Network is Expected to Drive the Market

- Saudi Arabia, the United Arab Emirates, and Oman, among other countries, benefit from a robust infrastructure. To continuously extend their smart cities, the main emphasis is expected to be on envisioning and innovating technology-driven development. In these countries, the population spends most of their time using social and communication apps. Businesses connect with their customers in countless ways, given how frequently and intensely they use their smartphones. Such factors are boosting smartphone adoption in the country.

- In the United Arab Emirates, three companies with unified licenses presently hold a significant market share: Mobile Telecommunication Company Saudi Arabia, Etihad Etisalat Company, and Saudi Telecom Company (STC).

- Other internet service providers (ISPs), mobile virtual network operators (MVNOs), and fixed-line service providers are also present in the market. The creation of a transparent, competitive market that keeps up with advanced infrastructure and technologies has been made possible in large part by the government.

- Moreover, companies like e& Etisalat and Saudi Telecom Company (STC) are key players, providing mobile services to meet the rising demand for data, voice, and messaging. These companies continuously innovate to offer competitive pricing, better coverage, and improved services to attract and retain customers in this expanding market. The emerging players and advancements in technology also contribute to the dynamic landscape of the GCC telecom industry.

- In February 2024, Power International Holding (PIH) reached an agreement to acquire Mobile Telecom Services (MTS) in Kazakhstan. MTS is currently owned by Kazakhtelecom, the National Telecommunications Company.

- In Oman, the mobile ecosystem is transforming at an ever greater scale as 5G technologies become available in the market. New capabilities will be introduced by 5G that enable operators to develop new use cases, applications, services, or revenue streams in consumer, business, and other sectors and markets.

Saudi Arabia is Expected to Witness Significant Growth

- As part of the 2030 Vision's National Transformation Program, the Saudi Ministry of Communications and Information Technology issued policies to encourage the rollout of FTTH ultra-fast broadband networks. The government has subsidized telecom companies to install fiber in underserved areas.

- The Saudi Data and Artificial Intelligence Authority wants to establish Saudi Arabia as a global provider of technology by developing a data and AI-driven economy. The country has made some investments in artificial intelligence, and the government is dedicated to transforming the nation digitally. The investments are primarily driven by local sources, particularly the nation's sovereign wealth fund.

- The major mobile service providers, Saudi Telecom Company (STC), Zain, and Mobily, also continued 5G expansion programs, thus driving the demand for effective, low latency, and high bandwidth mobile data and voice services in Saudi Arabia.

- In April 2024, Saudi Arabia's sovereign wealth fund, The Public Investment Fund (PIF), signed an agreement with mobile network operator Saudi Telecommunications Company (stc Group) for PIF to acquire a 51% stake in Telecommunication Towers Company (TAWAL) from stc Group.

- As per the Communications, Space & Technology Commission, there is a substantial increase in internet speed in Saudi Arabia, from 96.4 Mbps in 2021 to 153.1 Mbps in 2023, which has catalyzed significant growth in the telecom market. This boost enables faster data transmission, enhancing user experience and facilitating the adoption of bandwidth-intensive services like streaming and cloud computing. As a result, telecom providers are witnessing heightened demand for high-speed internet packages, driving competition and innovation in the market.

- Overall, this growth is led by the telecom, finance, government, and oil/gas sectors. Aggressive IT projects to modernize the Saudi Arabian government's IT infrastructure, including an e-government initiative and the telecom industry's liberalization, are increasing competition, service levels, and usage.

GCC Telecom Industry Overview

The GCC telecom market is becoming moderately consolidated. Some major players in the market include e& Etisalat, Saudi Telecom Company (STC), and Oman Telecommunications Company (Omantel), among others. The market also hosts several internet service providers (ISPs), MVNOs, and fixed-line service providers. These players focus on deploying 5G networks and increasing network capacity across the region to remain competitive in the market. For instance,

- In May 2024, Zain KSA invested SAR 1.6 billion (USD 0.43 billion) in expanding its infrastructure, 5G network, and digital services ecosystem. This move is part of an integrated expansion plan aligned with Zain KSA's strategy for achieving digital inclusion across the country. The goal is to enhance the digital infrastructure and provide an exceptional customer experience by expanding the 5G network to cover 122 cities and governorates, up from the current 66 cities.

- In March 2024, Ericsson and Du, from Emirates Integrated Telecommunication Company, entered into a strategic alliance to provide Ericsson with wireless network products, enabling intelligent services to the enterprise sectors and government in the United Arab Emirates. Ericsson and du have formed a strategic partnership to create advanced private 4G and 5G networks. Their collaboration aims to enhance connectivity for government and enterprise customers, enabling Industry 4.0 adoption in the country.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 An Assessment of the impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Huge demand for 5G

- 5.1.2 Significant penetrations of internet and smart phones

- 5.1.3 Rising digital transformation in the industries

- 5.2 Market Restraints

- 5.2.1 Security threats and leaks of private data

- 5.2.2 Heavy Capex associated with advanced telecom infrastructure

- 5.3 Ecosystem Analysis

- 5.3.1 Tower companies

- 5.3.2 OEMS (small cells, DAS etc.)

- 5.3.3 MNOs

- 5.3.4 MVNOs

- 5.3.5 OTT/PayTV

- 5.4 Evolution of GCC Telecom Sector

- 5.4.1 2G, 3G, 4G and 5G connections

- 5.5 Key metrics of GCC Telecom

- 5.5.1 Population

- 5.5.2 Fixed Broadband Subscriptions

- 5.5.3 Cellular Subscriptions

- 5.6 Analysis of Market Entry Strategy Of Vendors

6 MARKET SEGMENTATION

- 6.1 Overall telecom revenue

- 6.1.1 Telecom Subscriptions

- 6.1.2 Average revenue per user

- 6.2 Telecom services

- 6.2.1 Voice Services

- 6.2.1.1 Wired

- 6.2.1.2 Wireless

- 6.2.2 Data and Messaging Services

- 6.2.3 PayTV Services

- 6.2.1 Voice Services

- 6.3 Telecom connectivity

- 6.3.1 Fixed Network

- 6.3.2 Mobile Network

- 6.4 Country

- 6.4.1 Saudi Arabia

- 6.4.2 Kuwait

- 6.4.3 Qatar

- 6.4.4 Oman

- 6.4.5 United Arab Emirates

- 6.4.6 Bahrain

7 COMPETITIVE LANDSCAPE

- 7.1 Market Share Analysis Of Key Vendors

- 7.2 Company Profiles

- 7.2.1 e& (Etisalat and)

- 7.2.2 Saudi Telecom Company (STC)

- 7.2.3 Ooredoo Group

- 7.2.4 Zain Group

- 7.2.5 Oman Telecommunications Company (Omantel)

- 7.2.6 Emirates Integrated Telecommunications Company (Du)

- 7.2.7 Mobily (Etihad Etisalat Company)

- 7.2.8 Batelco (Bahrain Telecommunication Company)