モバイル暗号化:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Mobile Encryption - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 132 Pages

- 納期

- 2~3営業日

- 商品コード

- 1641912

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

モバイル暗号化の市場規模は、2025年に56億7,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは27.98%で、2030年には194億7,000万米ドルに達すると予測されます。

企業は、ますます浸透する規制やコンプライアンスに関する義務や、より厳格な社内ポリシーに適応しているため、暗号化の導入数は増加し、その範囲は重要な企業で拡大しています。

主なハイライト

- モバイル暗号化とは、正しい復号キーを持つ権限のある個人だけが解読できる言語やコードでデータを暗号化するプロセスです。データ・セキュリティとプライバシーに関する懸念の高まりにより、市場は急速に拡大しています。ほとんどの人がモバイル・デバイスを利用して財務データ、個人情報、企業機密情報などの機密情報を保存しているため、モバイル暗号化ソリューションの需要はますます重要になっています。

- 高度な脅威の増加と進化、クラウドサービスの採用強化、モバイルデバイスの普及、仮想化が、モバイル暗号化市場に破壊的な変化をもたらす主な要因となっています。厳格なコンプライアンスと規制要件の必要性、知的財産のセキュリティとプライバシーに対する関心の高まりは、市場を牽引する主な要因です。また、さまざまなエンドユーザーの間で「モノのインターネット(Internet of Things)」の動向が高まっていることも、モバイル暗号化市場の拡大を促進する重要な要因となっています。

- モバイル暗号化は、顧客データを部外者には分からないようにして保護し、プライベート性と安全性を確保します。スマートフォンによる決済利用が増加した結果、デジタル決済の件数は劇的に増加しています。現在の決済システムを改善するため、企業はモバイル決済にブロックチェーンを統合しています。ブロックチェーンの最大の特徴はその有効性であり、安全でセキュアな取引のベンチマークを確立します。

- BYOD(Bring Your Own Device)現象や、ほとんどすべての組織で信じられないほどの速さで浸透しているその採用は、セキュリティ・アプローチの根本的な再考を必要とし、組織が多くの異なる暗号化プラットフォームを導入していることが判明しています。その結果、ポリシーと鍵を効率的かつ安全に管理することは、ますます厄介な課題となっています。

- モバイル暗号化に対する需要は、組織がますますモバイル従業員を配備するようになるにつれて、ここ数年で劇的に高まっています。モバイル従業員には、生産性の向上、経費の削減、柔軟性の向上など、多くの利点があります。より多くの企業がモバイル・ワーカーを採用し続けているため、市場はここ数年で大幅に拡大しており、この動向は今後も続くと予測されています。

- 暗号化の包括的な使用は、業界セグメントによってかなり異なります。具体的には、金融サービスやITサービスなど、規制が厳しくモバイルに依存する業種の利用率が最も高く、製造業や消費者製品など規制が緩い業種の利用率が最も低いです。

- さらに、一つの大きな障壁は、組織がモバイル暗号化ソリューションの重要性を認識していないことです。暗号化ソリューションの複雑さ、暗号化技術の業界標準が存在しないこと、暗号化がデバイスの性能に及ぼす可能性のある影響に関する懸念は、さらなる制限のいくつかです。

- COVIDのロックダウンと制限により、モバイル技術の使用は通常よりも増加しました。セキュリティ・デバイスの相互運用性に対するニーズが高まり、それが新たな標準となるにつれ、モバイル暗号化に対する需要は大幅に増加すると思われます。

モバイル暗号化市場の動向

BFSIが大きな市場シェアを占める見込み

- モバイルアプリのセキュリティのために、銀行は多くの暗号化技術を採用しています。送信中のデータについては、TLS(Transport Layer Security)やSSL(Secure Sockets Layer)などが一般的な技術であり、保存中のデータについては、AES(Advanced Encryption Standard)やRSA(RSA)などが一般的な技術です。顧客情報をさらに保護するため、銀行はさらに、多要素認証やデバイスのフィンガープリンティングなどの追加的なセキュリティ対策を採用することもあります。銀行業界では、消費者により安全なサービスを提供するため、決済セキュリティ・ソリューションに対する要求が拡大しており、これが成長の要因となっています。

- 現在確認されているこの市場セグメントに影響を与える動向の中で、暗号化されたOTP SMSの使用は、フィッシング、中間者攻撃、マルウェア型トロイの木馬などの可能性のある攻撃を回避するためのPINとともに、その1つです。顧客の銀行口座情報やパスワードの多くがモバイル・デバイス上にあるため、個人的な写真(オンラインでローンを申し込んでいる間)でさえも、セキュリティ上の大きな懸念事項となっています。SSL/TLSは、クレジットカード情報、パスワード、機密性の高い個人情報など、インターネット上での個人データの安全なトランスミッションを可能にします。

- 銀行や金融機関はSSL/TLSを使用してトラフィックを暗号化することで、アクセスの制御、機密性の保護、プロトコル固有の攻撃への暴露の低減など、これらの複数の問題に対処しています。オンライン取引が高度化するにつれて、決済プロバイダーはより優れたセキュリティを提供するための技術に追いつこうとしています。現在、オンライン決済の大半はモバイルまたはアプリ内決済であるため、従来のPCI-DSS基準を適切にアップグレードする必要があります。

- さらに、人工知能(AI)が加わることで、金融暗号化ソフトウェアの効率性と有効性が高まると予測されています。同時に、データ保護に対する需要の高まりに対応する組織や顧客を支援します。その結果、人工知能を搭載した暗号化ソフトウェアが銀行・金融セクターで急速に採用されることが予想されます。

- データの完全性は、データの寿命を通じて銀行によって維持されなければならないです。そのため、銀行にとっては、ニーズに応じた適切な脅威の検知と対応手順を導入することが不可欠です。このように、銀行がデータマスキングや暗号化ソフトウェアなど様々なセキュリティ基準を課すことで、データの完全性を維持することができます。その結果、銀行・金融・保険(BFSI)業界では、金融暗号化ソフトウェアの需要が増加すると予想されます。

- 旧式のSSL標準は、EMVスリー・ドメイン・セキュア(3DS)のような新しいイニシアチブの使用を妨げています。暗号化のために2つのアルゴリズムを並行して使用する通信は、現在最も強力な暗号化と考えられており、暗号学者はダブルセル暗号が予測期間中もそうであると予測しています。

北米が大きな市場シェアを占める見込み

- 北米地域では、米国のビジネス部門が日常業務を遂行するためにコンピュータ・ネットワークや電子データへの依存度を高めており、個人情報や財務情報も携帯電話を使ってクラウドに転送・保存されるケースが増えています。さらに、BYOD傾向の大幅な高まりは、機密情報へのアクセスやクライアント・サーバーへのログインに、スマートカード、物理的トークン、KPIなどの高度な認証方法が必要とされる状況も後押ししています。

- この優位性は、カナダや米国のような国々で、銀行に対してデータ・プライバシーの向上を義務付ける規制基準が厳しくなっていることに起因しています。プライバシーを保護するため、公的銀行も民間銀行も暗号ソフトウェアへの需要を高めています。さらに、サイバー攻撃の急増とビジネス・クリティカルな情報への脅威が、この地域の市場拡大に拍車をかけると予想されています。

- 米国では、モバイル機器の約51%がフルディスク暗号化を導入していると推定されており、今後数年間でさらに増加する見込みです。しかし、フルディスク暗号化の普及に伴い、これらのデバイスのほとんどすべてが法執行機関によってアクセス不能になる可能性があります。そのため、政府は暗号化市場を規制しています。グーグルや他のハイテク大手のような企業は、制限や障害に直面しています。

- AAG ITサービスは、2021年にはアメリカのインターネットユーザーの2人に1人がアカウントを侵害されたと推定しています。米国企業の10社に1社は、サイバー攻撃に対する防御策を講じていないです。さらに、サイバー犯罪は2022年上半期に5,335万人の米国個人に影響を与えました。そのため、個人情報保護法の高まりとモバイル決済技術は、この分野で新たな産業の展望を開くと予想されます。

- アップルはモバイル・フルディスク暗号化の最大手であり、米国のモバイル・デバイスの約55%はiOSで動作しています。北米地域では悪質なデータ漏洩が増加しており、暗号化サービスの最大市場となっています。

モバイル暗号化産業の概要

モバイル暗号化のエコシステムは様々なモバイル暗号化ソリューションとサービスプロバイダで構成されているため、世界のモバイル暗号化市場は断片化されています。主要企業は、新製品の発売や臨床試験など、さまざまな戦略を展開し、また、この市場での足跡を増やすために、研究開発、合弁事業、パートナーシップ、買収などに多額の支出を通じて、市場イニシアティブとイノベーションをとっています。同市場の主要企業としては、IBM Corporation、HP Enterprises、Dell、Symantec、Checkpoint Softwareなどが挙げられます。

- 2022年10月- サイバー・セキュリティ・ソリューションのトップ・世界・プロバイダであるCheck Point Software Technologies Ltd.は、開発者による開発者のための開発者ファーストのセキュリティ・ツールの重要なイノベーターであったイスラエルの新興企業Spectralを買収しました。この買収により、チェック・ポイントのクラウド・ソリューション「Check Point CloudGuard」の開発者ファーストのセキュリティ機能が強化され、Infrastructure as Code(IaC)スキャンやハードコードされたシークレットの検出など、最も幅広いクラウド・アプリケーション・セキュリティのユースケースを提供できるようになると期待されています。

- 2022年12月-RingCentral, Inc.は、同社の主力製品であるRingCentral MVPのEnd-to-End Encryption(E2EE)機能を拡張し、ビデオに加えて電話とメッセージングの両方に対応させると発表しました。E2EEテクノロジーは、ユーザーのコミュニケーション・コンテンツを不正アクセスから保護します。これにより、外部からの侵入や攻撃から保護されるだけでなく、セキュリティを重視する組織にとっては、特権的なディスカッションのプライバシーも保護されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因と市場抑制要因のイントロダクション

- 市場促進要因

- 企業における安全な通信に対する需要の高まり

- データセキュリティと知的財産のプライバシーに対する関心の高まり

- 市場抑制要因

- 認識と熟練労働力の不足

- バリューチェーン/サプライチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- コンポーネント別

- ソリューション

- サービス

- アプリケーション別

- ディスク暗号化

- ファイル/フォルダ暗号化

- ウェブ通信暗号化

- クラウド暗号化

- その他のアプリケーション

- 展開タイプ別

- オンプレミス

- クラウド

- 企業規模別

- 中小企業

- 大企業

- エンドユーザー別

- BFSI

- 航空宇宙・防衛

- ヘルスケア

- 政府・公共機関

- 電気通信

- 小売

- その他のエンドユーザー

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第6章 競合情勢

- 企業プロファイル

- Dell

- Check Point Software Technologies, Ltd

- Hewlett Packard Enterprise

- IBM Corporation

- KoolSpan, Inc.

- MobileIron, Inc.

- SecurStar GmbH

- Silent Circle, LLC

- Sophos Ltd.

- Symantec Corporation

- T-Systems International GmbH

第7章 投資分析

第8章 市場機会と今後の動向

目次

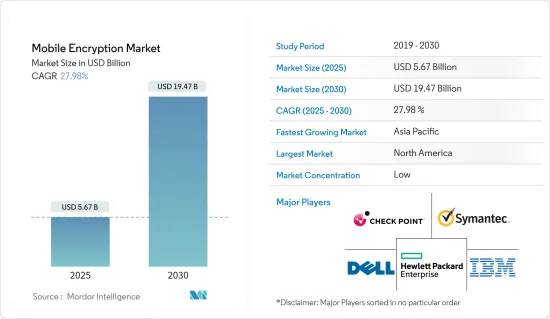

The Mobile Encryption Market size is estimated at USD 5.67 billion in 2025, and is expected to reach USD 19.47 billion by 2030, at a CAGR of 27.98% during the forecast period (2025-2030).

As organizations have adapted to increasingly pervasive regulatory and compliance mandates and more stringent internal policies, encryption deployments have increased in number and scope in significant enterprises.

Key Highlights

- Mobile encryption is the process of encoding data in a language or code only authorized individuals with the right decryption key can decipher. Due to increased worries about data security and privacy, the market is expanding quickly. The demand for mobile encryption solutions is becoming increasingly critical as most people utilize mobile devices to store sensitive information like financial data, personal information, and confidential corporate information.

- Increasing and evolving advanced threats, the enhanced adoption of cloud services, mobile device proliferation, and virtualization are the major factors creating disruptive changes in the mobile encryption market. The need for stringent compliance and regulatory requirements and increasing concern for the security and privacy of intellectual property are the major factors driving the market. Also, the rising trend of the Internet of Things among various end-user verticals is a crucial factor facilitating the expansion of the mobile encryption market.

- Mobile encryption safeguards customer data by making it unintelligible to outsiders, ensuring it remains private and secure. The number of digital payments has increased dramatically as a result of the rise in smartphone payment usage. To improve the present payment system, businesses are integrating blockchain with mobile payment. The most important feature of blockchain is its effectiveness, which establishes a benchmark for safe and secure transactions.

- The "bring your own device" (BYOD) phenomenon and its incredibly fast and pervasive adoption by almost every organization necessitated a fundamental rethinking of security approaches, and it has been found that organizations are deploying many disparate encryption platforms. As a result, managing policies and keys efficiently and securely is an increasingly troublesome challenge.

- The demand for mobile encryption has grown dramatically over the years as organizations increasingly deploy a mobile workforce. A mobile workforce has many advantages, including increased productivity, lower expenses, and more flexibility. As more businesses continue to employ a mobile workforce, the market has consequently experienced considerable expansion over the past few years, and this trend is projected to continue in the years to come.

- The comprehensive use of encryption varies considerably by industry segment. Specifically, heavily regulated and mobile-dependent industries, such as financial services and IT services, have the highest use rate, and less regulated industries, such as manufacturing and consumer products, have the lowest use rate.

- Additionally, one major barrier is that organizations do not recognize the importance of mobile encryption solutions. Concerns regarding the complexity of encryption solutions, the absence of industry standards for encryption technology, and the possible effects of encryption on device performance are some further limitations.

- COVID Lockdowns and limitations increased mobile technology use more than usual. As the need for security device interoperability grows and becomes the new standard, there will be a significant rise in demand for mobile encryption.

Mobile Encryption Market Trends

BFSI is Expected to Hold a Major Market Share

- For the security of their mobile apps, banks employ a number of encryption techniques. For data in transit, common techniques include Transport Layer Security (TLS) and Secure Sockets Layer (SSL), whereas for data at rest, common techniques include Advanced Encryption Standard (AES) or RSA. To further safeguard customer information, banks may additionally employ extra security measures like multi-factor authentication and device fingerprinting. The banking industry's expanding requirement for payment security solutions to offer its consumers a more secure service is what is causing the growth.

- Among the current identified trends influencing this segment of the market, the usage of encrypted OTP SMS is one of them, along with a PIN to avoid any possible attacks like phishing, man-in-the-middle attacks, and malware Trojans. As more of the bank account information and passwords of customers come on mobile devices, even personal pictures (while applying for loans online) have become a major security concern. SSL/TLS enables secure transmissions of private data over the internet, including credit card details, passwords, and sensitive personal information.

- Banks and financial institutions use SSL/TLS to encrypt their traffic to address these multiple issues, including controlling access, protecting confidentiality, and reducing exposure to protocol-specific attacks. With the increased sophistication of online transactions, payment providers are catching up with the technologies to provide better security. The majority of online payments are now mobile or in-app payments; the traditional PCI-DSS standards have to be suitably upgraded.

- Moreover, it is projected that the efficiency and effectiveness of financial encryption software would grow with the addition of artificial intelligence (AI). At the same time, it helps organisations and customers meet the growing demand for data protection. As a result, it is anticipated that encryption software powered by artificial intelligence would be quickly adopted by the banking and finance sector.

- The integrity of the data must be maintained by the banks throughout the life of the data. As a result, it is essential for banks to put in place the appropriate threat detection and response procedures in accordance with their needs. Thus, by imposing various security standards, such as data masking and encryption software by banks, the data integrity can be preserved. As a result, it is anticipated that the banking, finance, and insurance (BFSI) industry will see an increase in demand for financial encryption software.

- The outdated SSL standards prevent the use of new initiatives like EMV Three-Domain Secure (3DS), a messaging mechanism that enables customers to authenticate themselves with their card issuer when making card-not-present online purchases.. Communication that uses two algorithms for encryption that work side-by-side is currently considered the strongest encryption, with cryptologists predicting double-cell encryption to remain so over the forecast period.

North America is Expected to Hold a Major Market Share

- In the North American region, the United States business sector increasingly depends on computer networks and electronic data to conduct its daily operations, and growing pools of personal and financial information are also transferred and stored in the cloud using phones. Furthermore, a significant increase in the BYOD trend is also favoring the conditions for advanced authentication methods, such as smart cards, physical tokens, and KPIs, to access sensitive information or log in to client servers.

- The dominance can be attributed to the more stringent regulatory standards in nations like Canada and the United States, which oblige banks to increase data privacy. In order to protect privacy, both public and private banks have increased their demand for cryptographic software. Additionally, the regional market expansion is anticipated to be fueled by the surge in cyberattacks and the threat to business-critical information.

- It is estimated that around 51% of mobile devices in the United States have full disk encryption, which is expected to increase in the coming years. However, with the growth in the adoption of full disk encryption, almost all these devices could become inaccessible to law enforcement. As a result, the government is regulating the encryption market. Companies like Google and other tech giants are facing restrictions and obstacles.

- AAG IT Services estimates that in 2021, 1 in 2 American internet users had their accounts breached. One in ten US businesses do not have any protection against cyberattacks. In addition, cybercrime had an impact on 53.35 million US individuals in the first half of 2022. Therefore, rising privacy laws and mobile payment technology are anticipated to open up new industry prospects in the area.

- Apple is the largest provider of mobile full-disk encryption, and around 55% of the mobile devices in the United States run on iOS. With increased malicious data breaches occurring in the North American region, it has become the largest market for encryption services.

Mobile Encryption Industry Overview

The Global Mobile Encryption Market is fragmented, as the mobile encryption ecosystem comprises various mobile encryption solutions and service providers. The major players deploy various strategies, such as new product launches and clinical trials, and are also taking market initiatives and innovations through high expenditure on research and development, joint ventures, partnerships, acquisitions, and others to increase their footprints in this market. Some of the major players in the market are IBM Corporation, HP Enterprises, Dell, Symantec, and Checkpoint Software, among others.

- October 2022 - Check Point Software Technologies Ltd., a top global provider of cyber security solutions, acquired Spectral, an Israeli startup that was a key innovator in developer-first security tools created by developers for developers. With this purchase, Check Point was expected to increase the developer-first security capabilities of its cloud solution, Check Point CloudGuard, and offer the broadest range of cloud application security use cases, including infrastructure as code (IaC) scanning and hardcoded secret detection.

- December 2022 - RingCentral, Inc. announced that it is extending End-to-End Encryption (E2EE) capabilities in its flagship RingCentral MVP product to encompass both phone and messaging in addition to video. E2EE technology shields users' communication content from being accessed by unauthorised parties. This offers protection against infiltration and attacks from outside parties as well as privacy for privileged discussions for security-conscious organisations.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Introduction to Market Drivers and Restraints

- 4.3 Market Drivers

- 4.3.1 Growing demand for secure communication in enterprises

- 4.3.2 Increasing concern for data security and privacy of intellectual property

- 4.4 Market Restraints

- 4.4.1 Lack of awareness and skilled workforce

- 4.5 Value Chain / Supply Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers/Consumers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 Application

- 5.2.1 Disk Encryption

- 5.2.2 File/Folder Encryption

- 5.2.3 Web Communication Encryption

- 5.2.4 Cloud Encryption

- 5.2.5 Other Applications

- 5.3 Deployment Type

- 5.3.1 On-premise

- 5.3.2 Cloud

- 5.4 Enterprise Size

- 5.4.1 SMEs

- 5.4.2 Large Enterprises

- 5.5 End Users

- 5.5.1 BFSI

- 5.5.2 Aerospace and Defense

- 5.5.3 Healthcare

- 5.5.4 Government and Public Sector

- 5.5.5 Telecom

- 5.5.6 Retail

- 5.5.7 Other End Users

- 5.6 Geography

- 5.6.1 North America

- 5.6.2 Europe

- 5.6.3 Asia Pacific

- 5.6.4 Latin America

- 5.6.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Dell

- 6.1.2 Check Point Software Technologies, Ltd

- 6.1.3 Hewlett Packard Enterprise

- 6.1.4 IBM Corporation

- 6.1.5 KoolSpan, Inc.

- 6.1.6 MobileIron, Inc.

- 6.1.7 SecurStar GmbH

- 6.1.8 Silent Circle, LLC

- 6.1.9 Sophos Ltd.

- 6.1.10 Symantec Corporation

- 6.1.11 T-Systems International GmbH

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 132 Pages

- 納期

- 2~3営業日