|

|

市場調査レポート

商品コード

1549788

インドネシアの通信市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Indonesia Telecom - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドネシアの通信市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

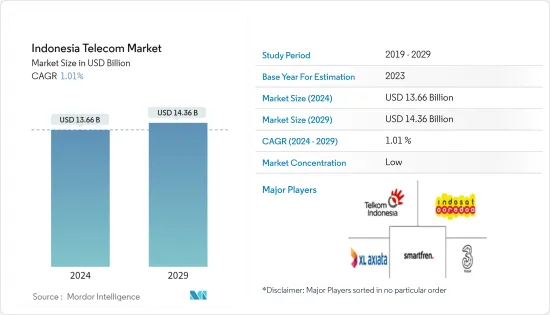

インドネシアの通信市場規模は2024年に136億6,000万米ドルと推定され、2029年には143億6,000万米ドルに達し、予測期間中(2024~2029年)のCAGRは1.01%で成長すると予測されます。

世界最大級の規模を誇るインドネシアの通信市場には、拡大の機会が豊富にあります。この成長は主に、利用者が増加する可能性があることに起因しています。しかし、国の収益が上昇するにつれて、ユーザー1人当たりの収益も増加する可能性があります。

主要ハイライト

- 顧客による高速接続サービスに対する需要の高まりと、5Gインフラの展開に向けた支出の増加は、インドネシアの通信市場の成長にプラスの影響を与えます。同国のデジタル時代への着実な移行に伴い、同産業は一貫して拡大する態勢を整えています。2023年1月までに、インドネシアの携帯電話接続数は約3億5,400万に達したとGSMA Intelligenceは報告しており、同国におけるモバイル技術の広範な浸透を浮き彫りにしています。

- インドネシアは、その変革アジェンダを支援するため、通信パートナーと積極的に連携しています。特に、5G革命で重要な役割を果たそうとしているパートナーは、通信ネットワークを強化することで、インドネシアの観光イニシアチブを支援しています。OpenGov Asiaのレポートに主要ハイライトがあるように、通信・情報大臣は5Gサービスの展開を賞賛し、バリでのG20サミットに合わせ、G20インドネシア議長国シリーズの重要なコンポーネントとしてマークしました。

- さらに2024年6月、PT Telkom IndonesiaはSingTelとMedco Power Indonesiaと共同で、大規模な投資計画を発表しました。この提携は、バタム島での先進的データセンター建設に1兆4,000億ルピア(約8,500万米ドル)を投入することを目的としていました。この施設は人工知能(AI)インフラを備えることを目的としており、プロジェクトは5年かけて完成する予定です。

- Telkomselは30 MHz、Indosatは20 MHzの5G帯域幅を割り当てられました。これらの割り当ては、最適な5G展開のために推奨される周波数帯よりも少ないです。GSMAによると、強固な周波数帯を確保するため、ミッドバンドに80~100MHzの初期割り当てが提案されています。Telkomselの2.3GHz帯に比べ、Indosatの1.8GHz帯にはより多くのスマートフォンモデルが対応していることが指摘されています。Indosatが1.8GHz帯に注力し、当初はB2Bセグメントに重点を置いていたことから、この帯域に対応するスマートフォンの需要は、緩やかなペースではあるが、増加すると予想されます。

- Ericssonの調査によると、2021年第3四半期までにインドネシアはモバイルネットワークのデータトラフィックが前年同期比42%増加し、固定無線アクセス(FWA)サービスのトラフィックを含む78エクサバイト(EB)に達しました。さらに、最近の予測によると、モバイル・ネットワークのデータトラフィック総量は2027年末までに370EBを超える見込みです。2021年末までに登録された8,800万件のFWA接続は、2027年には2億3,000万件を超えると予測されました。これらの接続の約半数が5Gネットワークを利用すると予想されています。

- しかし、デジタルの混乱はインドネシアの通信産業の成長軌道に大きな課題を突きつけた。技術の進歩とともに、より高速で信頼性の高い接続に対する消費者の需要が高まるにつれ、通信事業者はインフラ、IT、人材への投資を増やさざるを得なくなりました。さらに、産業の大幅なIT改革には多額の資本支出(CAPEX)が必要であり、リードタイムも長かったため、市場の成長はさらに阻害されました。

インドネシア通信市場の動向

5G展開のペースが市場を牽引

- Telecom Review Reportによると、政府は5Gネットワークをサポートするために様々な周波数帯を積極的に開発しています。これには、低周波数帯域から超高周波数帯域まで、さまざまな周波数帯域のファーミングとリファーミングが含まれます。2023年11月、インドネシア初の5Gパークであるソロ・テクノパークに産業利害関係者が集まり、5Gエコシステム加速サミットが開催されました。このサミットは、インドネシアの2030年と2045年のデジタルビジョンに沿ったもので、新たなビジネス動向に関する詳細な洞察を提供し、消費者、家庭、企業向けの5Gソリューションの展開に関連する課題と機会を明らかにしました。

- 政府はデジタル経済を強化するためにインターネットインフラを活用しています。2023年12月、5Gソフトウェア・プロバイダであるVirtual Internetは、PT.ABCと提携し、同社のバーチャル5G技術をインドネシア全土に展開しました。この契約により、PT.ABCはバーチャル5Gアプリケーションを無制限に配布できます。これがフルに活用されれば、最大で5億ライセンス(各ライセンスの年間平均利用料は4米ドル)に達する可能性があります。

- Ericssonのモビリティ・レポートによると、通信会社は製造、エネルギー、公共事業、メディアなどの産業に5Gソリューションを提供することで大きな利益を得ました。同レポートは、インドネシアの通信会社は、国内での5G技術導入に課題があるにもかかわらず、企業間(B2B)5Gサービスに注力することで、2030年までに収入が35%増加し、82億米ドルに達する可能性があると示唆しました。

- さらに、バリ島は、スラカルタ、ジャカルタ、スラバヤ、マカッサル、バリクパパンに続き、5Gのサービスを受ける6番目の都市となりました。

OTTサービスに対する需要の高まりが市場を牽引

- インドネシアでは、ストリーミング・ビデオ、VoIP(Voice over Internet Protocol)、メッセージングアプリケーションなどのOTT(Over-The-Top)サービスが大きな人気を集めています。通信事業者は市場競合を維持するため、バンドルサービスの提供、OTTプロバイダーとの提携、独自のOTTサービスの開拓により、この動向に適応しました。

- 2024年5月、インドネシアを拠点とし、現地のコングロマリットEmtek Groupが所有するストリーミングプラットフォームVidioは、今後2~3年以内に有料加入者数を800万人に増やす計画を発表しました。この目標は、2023年時点で410万人だった加入者数を約2倍に増やすことになります。

- さらに2024年5月、統合情報通信技術ソリューションの世界的プロバイダーであるZTE Corporationとインターネットサービス・プロバイダーのMyRepublicは、ZTE Day 2024でインドネシア初のWi-Fi 7製品の発売を発表しました。このイベントは、ZTEとMyRepublicの重要な協力関係を示すもので、技術革新の推進とWi-Fi 7の商業的導入の促進に対する両社の献身を強調するものです。Wi-Fi 7 CPEを導入することで、MyRepublicはユーザーに前例のない高速かつ低遅延のネットワーク体験を提供することを目指しました。

- The Trade DeskによるFuture of TVの分析によると、OTTストリーミングはCOVID-19の大流行後に人気が急上昇しました。OTTは、いつでもどこでも好きなときに好きな番組を好きなデバイスで視聴できるエンターテインメントの人気形態となったため、インドネシアではすでに3人に1人以上がOTTストリーミングを利用しています。インドネシアは、OTT消費が前年比40%増と好調で、東南アジア地域で首位に立った。

- スマートフォンのコストが下がり、モバイルブロードバンドのカバー率が向上し、インターネットアクセスがよりリーズナブルな価格になりました。インドネシアにおけるOTTの拡大は、こうした動向と連動していました。OTTプラットフォームは、消費者の嗜好を考慮し、これらの顧客を引き付けるためにオファーを調整しました。インドネシアのPlayストアのエンタテインメント・カテゴリーでは、上位3つのプラットフォームで、他のどのプラットフォームよりも多くのローカルとアジアのコンテンツが利用可能でした。Vidioのスポーツ放送サービスの加入形態では、週払いのオプションが利用可能でした。

インドネシア通信産業概要

インドネシアの通信市場は非常に細分化されています。調査対象となった主要参入企業は、Telkom Indonesia、Indosat Ooredoo、XL Axiata、Smartfren Telecom、Tri Indonesiaです。同市場には、その他のインターネットサービス・プロバイダー(ISP)、MVNO、固定回線サービス・プロバイダーも存在します。インドネシアの通信企業の中には、国際的な競合を持ち、世界の通信市場で確固たる地位を築いている企業もあります。

- 2024年4月、マレーシアのコングロマリットAxiata GroupとインドネシアのグループPT Sinar Masは、両社の電気通信事業であるXL AxiataとSmartfrenを35億米ドルの事業体に統合する計画により、市場での地位を強化する計画を発表しました。この合併により、両社の顧客基盤が統合され、約9,400万人の携帯電話加入者が誕生します。XL Axiataは約5,800万人の顧客を獲得し、Smartfrenは約3,600万人の顧客を獲得します。この戦略的な動きは、2023年9月時点で1億5,800万人以上のモバイルユーザーを持つTelkomselに対するより強力な競争相手を作るためのものです。さらに、約1億人の携帯加入者を持つIndosat Ooredoo Hutchisonと密接に対抗する位置づけとなりました。

- 2024年4月、Scala Inc.とインドネシアのバンドンに本社を置く国営通信会社PT Telkom Indonesia(Persero)Tbk(Telkom)が戦略的業務提携を発表。この提携は、農業セグメントにおける技術革新と開発を促進することを目的としています。両社の強みを組み合わせることで、この重要な産業における重要な課題に取り組み、機会をつかむことを目指します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- エコシステム分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- マクロ経済動向の市場への影響

- インドネシアの規制状況

第5章 市場力学

- 市場促進要因

- 5G展開のペースアップ

- 通信を後押しするデジタル変革

- 市場抑制要因

- セキュリティ関連の課題

- 接続性別の市場分析(詳細な動向分析を含む対象範囲)

- 固定ネットワーク

- ブロードバンド(ケーブルモデム、有線ファイバー、有線DSL、固定Wi-Fi、ADSL/VDSL、FTTP/B、ケーブルモデム、FWA、5G FWAに関する動向)

- ナローバンド

- モバイルネットワーク

- スマートフォンとモバイルの普及

- モバイルブロードバンド

- 2G、3G、4G、5G接続

- スマートホームIoTとM2M接続

- 固定ネットワーク

- 通信タワーの分析(ラティスタワー、ガイダースタワー、モノポールタワー、ステルスタワーなど、各種タワーの動向分析を含む)

第6章 市場セグメンテーション

- サービス別セグメンテーション(サービス全体のユーザー当たり平均収益分析、2020~2027年の各セグメント市場規模・推定、動向分析など)

- 音声サービス

- 有線

- ワイヤレス

- データとメッセージングサービス(インターネット、端末データパッケージ、パッケージ割引を含む)

- OTTと有料テレビサービス

- 音声サービス

第7章 競合情勢

- 企業プロファイル

- Telkom Indonesia

- Indosat Ooredoo

- XL Axiata

- Smartfren Telecom

- Tri Indonesia

- Net1 Indonesia

- Emtek

- Bakrie Telecom

- First Media

- Transvision

- Optiva Inc.

第8章 投資分析

第9章 市場機会と今後の動向

The Indonesia Telecom Market size is estimated at USD 13.66 billion in 2024, and is expected to reach USD 14.36 billion by 2029, growing at a CAGR of 1.01% during the forecast period (2024-2029).

The telecom market in Indonesia, which is among the biggest in the world, has plenty of opportunities to expand. This growth has been mainly caused by a possible increase in users. However, it may also be fueled by more revenue per user as the nation's earnings rise.

Key Highlights

- The growing demand for high-speed connectivity services by customers and increasing spending on the deployment of 5G infrastructure positively influence the growth of the Indonesian telecom market. With the nation's steady transition into the digital age, the industry has been poised for consistent expansion. By January 2023, GSMA Intelligence reported that the number of cellular mobile connections in Indonesia had reached approximately 354 million, highlighting the extensive penetration of mobile technology within the country.

- Indonesia actively engages with its telecommunications partners to support its transformation agenda. Notably, those aiming to play a significant role in the 5G revolution also supported the nation's tourism initiatives by enhancing its telecommunications networks. As highlighted in an OpenGov Asia report, the Minister of Communication and Information praised the rollout of 5G services, marking it as a key component of the G20 Indonesia Presidency series, aligning with the G20 Summit in Bali.

- Furthermore, in June 2024, PT Telkom Indonesia, in collaboration with SingTel and Medco Power Indonesia, announced plans for a substantial investment. The collaboration aimed to inject IDR 1.4 trillion (about USD 85 million) into the construction of an advanced data center in Batam. This facility was intended to be equipped with Artificial Intelligence (AI) infrastructure, with the project scheduled for completion over a five-year period.

- Telkomsel has been granted a 5G bandwidth of 30 MHz, while Indosat allocated 20 MHz. These allocations are less than the recommended spectrum for an optimal 5G deployment. According to GSMA, an initial allotment of 80-100 MHz for the mid-band was suggested to ensure a robust spectrum. It was noted that more smartphone models were compatible with Indosat's 1.8 GHz band compared to Telkomsel's 2.3 GHz. Given Indosat's focus on the 1.8 GHz band and its initial emphasis on the B2B sector, the demand for smartphones supporting this band is expected to rise, albeit at a moderate pace.

- By the third quarter of 2021, Indonesia experienced a 42% Y-o-Y increase in mobile network data traffic, reaching 78 exabytes (EB), which included traffic from fixed wireless access (FWA) services, according to research conducted by Ericsson. Moreover, recent projections indicated that the total mobile network data traffic was expected to exceed 370 EB by the end of 2027. By the end of 2021, the 88 million registered FWA connections were projected to surpass 230 million by 2027. It is anticipated that approximately half of these connections will utilize 5G networks.

- However, digital disruptions posed significant challenges to the growth trajectory of Indonesia's telecommunications industry. As consumer demands for faster and more reliable connectivity evolved alongside technological advancements, telecommunications operators were compelled to increase infrastructure, IT, and talent investments. Furthermore, the industry's substantial IT overhaul required significant capital expenditure (CAPEX) and involved extended lead times, further impeding market growth.

Indonesia Telecom Market Trends

Increased Pace of 5G Roll-out Driving the Market

- According to the Telecom Review Report, the government has been actively developing various spectrum bands to support the 5G network. This includes farming and refarming the frequency spectrum across different bands, ranging from low to super high. In November 2023, industry stakeholders convened at Solo Techno Park, Indonesia's first 5G park, for the 5G Ecosystems Acceleration Summit. This summit aligned with Indonesia's Digital Vision for 2030 and 2045, provided detailed insights into emerging business trends, and elucidated the challenges and opportunities associated with deploying 5G solutions for consumers, homes, and businesses.

- The government is using its internet infrastructure to enhance its digital economy. In December 2023, Virtual Internet, a 5G software provider, partnered with PT. ABC to deploy its Virtual 5G technology across Indonesia. This agreement permitted PT. ABC to distribute an unlimited number of Virtual 5G applications. If fully utilized, this could result in up to 500 million licenses, each with an average annual subscription cost of USD 4.

- As per the Ericsson Mobility Report, telecom companies benefited significantly from offering 5G solutions to industries such as manufacturing, energy, utilities, and media. The report suggested that Indonesian telecom firms could have seen a 35% increase in income, amounting to USD 8.2 billion by 2030, by focusing on business-to-business (B2B) 5G services, despite the challenges in implementing 5G technology in the country.

- Furthermore, Bali had become the sixth city to receive 5G coverage, following Surakarta, Jakarta, Surabaya, Makassar, and Balikpapan.

Higher Demand for OTT Services Driving the Market

- Over-the-top (OTT) services, including streaming video, Voice over Internet Protocol (VoIP), and messaging applications, have gained significant popularity in Indonesia. Telecom operators adapted to this trend by offering bundled services, partnering with OTT providers, or developing their own OTT offerings to remain competitive in the market.

- In May 2024, Vidio, a streaming platform based in Indonesia and owned by the local conglomerate Emtek Group, announced plans to increase its number of paid subscribers to 8 million within the next two to three years. This target would have approximately doubled its subscriber base, which was 4.1 million as of 2023.

- Furthermore, in May 2024, ZTE Corporation, a global provider of integrated information and communication technology solutions, and MyRepublic, an internet service provider, announced the launch of Indonesia's first Wi-Fi 7 product at ZTE Day 2024. This event marked a significant collaboration between ZTE and MyRepublic, highlighting their dedication to advancing technological innovation and facilitating the commercial implementation of Wi-Fi 7. By introducing the Wi-Fi 7 CPE, MyRepublic aimed to provide users with a network experience that offered unprecedented high speeds and low latency.

- According to a Future of TV analysis by The Trade Desk, OTT streaming experienced a meteoric rise in popularity after the COVID-19 pandemic. Over one in three Indonesians already streamed material over the top (OTT) as OTT became a popular form of entertainment where people could watch their favorite shows across devices whenever and wherever they wanted. Indonesia led in the Southeast Asian region with a strong 40% Y-o-Y rise in OTT consumption.

- Smartphone costs decreased, mobile broadband coverage improved, and internet access became more reasonably priced. The expansion of OTT in Indonesia was linked to these trends. OTT platforms adjusted their offers to attract these customers by considering consumer preferences. More local and Asian content was available on the top three platforms than on any other platform in Indonesia's Play Store entertainment category. A weekly payment option was available in Vidio's subscription configuration for its sports broadcasting service.

Indonesia Telecom Industry Overview

The Indonesian telecom market is highly fragmented in nature. Some major players in the market studied are Telkom Indonesia, Indosat Ooredoo, XL Axiata, Smartfren Telecom, and Tri Indonesia. The market also hosts other internet service providers (ISPs), MVNOs, and fixed-line service providers. Some Indonesian telecommunication companies are competitive internationally and hold strong ground in the global telecom space.

- April 2024: Malaysian conglomerate Axiata Group and Indonesian group PT Sinar Mas announced plans to strengthen their position in the market by planning to merge their telecom operations, XL Axiata and Smartfren, into a USD 3.5 billion entity. This merger intends to combine their customer bases, resulting in approximately 94 million mobile subscribers. XL Axiata contributed around 58 million customers, while Smartfren added about 36 million. This strategic move was designed to create a stronger competitor to Telkomsel, which had over 158 million mobile users as of September 2023. Furthermore, it positioned the merged entity to closely rival Indosat Ooredoo Hutchison, which had approximately 100 million mobile subscribers.

- April 2024: Scala Inc. and PT Telkom Indonesia (Persero) Tbk (Telkom), Indonesia's state-owned telecommunications company based in Bandung, announced a strategic business alliance. This partnership will be dedicated to fostering innovation and development within the agricultural sector. By combining their strengths, both organizations aim to address significant challenges and seize opportunities in this crucial industry.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Ecosystem Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of Macroeconomic Trends on the Market

- 4.5 Regulatory Landscape in Indonesia

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Pace of 5G Roll Out

- 5.1.2 Digital Transformation Boosting Telecom

- 5.2 Market Restraints

- 5.2.1 Security Related Challenges

- 5.3 Analysis of the Market based on Connectivity (Coverage to Include In-depth Trend Analysis)

- 5.3.1 Fixed Network

- 5.3.1.1 Broadband (Cable Modem, Wireline-fiber, Wireline DSL, Fixed Wi-Fi and Trends Regarding ADSL/VDSL, FTTP/B, Cable Modem, FWA, and 5G FWA)

- 5.3.1.2 Narrowband

- 5.3.2 Mobile Network

- 5.3.2.1 Smartphone and Mobile Penetration

- 5.3.2.2 Mobile Broadband

- 5.3.2.3 2G, 3G, 4G, and 5G Connections

- 5.3.2.4 Smart Home IoT and M2M Connections

- 5.3.1 Fixed Network

- 5.4 Analysis of Telecom Towers (Coverage to Include In-depth Trend Analysis of Various Types of Towers, like Lattice, Guyed, Monopole, and Stealth Towers)

6 MARKET SEGMENTATION

- 6.1 Segmentation by Services (Coverage to Include Average Revenue Per User for Overall Services Segment, Market Sizes and Estimates for Each Segment for the Period of 2020-2027, and In-depth Trend Analysis)

- 6.1.1 Voice Services

- 6.1.1.1 Wired

- 6.1.1.2 Wireless

- 6.1.2 Data and Messaging Services (Coverage to Include Internet and Handset Data Packages and Package Discounts)

- 6.1.3 OTT and Pay TV Services

- 6.1.1 Voice Services

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Telkom Indonesia

- 7.1.2 Indosat Ooredoo

- 7.1.3 XL Axiata

- 7.1.4 Smartfren Telecom

- 7.1.5 Tri Indonesia

- 7.1.6 Net1 Indonesia

- 7.1.7 Emtek

- 7.1.8 Bakrie Telecom

- 7.1.9 First Media

- 7.1.10 Transvision

- 7.1.11 Optiva Inc.