|

市場調査レポート

商品コード

1550195

アジア太平洋のデジタルトランスフォーメーション:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Asia Pacific Digital Transformation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋のデジタルトランスフォーメーション:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

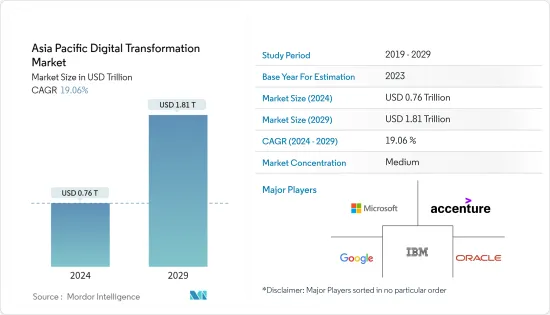

アジア太平洋のデジタルトランスフォーメーションの市場規模は2024年に7,600億米ドルと推計され、2029年には1兆8,100億米ドルに達すると予測され、予測期間中(2024年~2029年)のCAGRは19.06%で成長する見込みです。

技術的、経済的、社会政治的要因がアジア太平洋のデジタルトランスフォーメーション市場を牽引しています。

主なハイライト

- インターネットの急速な普及とスマートフォンの普及が、デジタルサービス拡大の強固な基盤となっています。同地域におけるデジタル製品・サービスの需要拡大は、特に発展途上国における通信インフラへの多額の投資によって支えられています。この需要は主に、可処分所得の増加とデジタルリテラシーの向上を特徴とする、この地域の中間層の拡大によって促進されています。

- 政府の取り組みは、この成長を推進する上で極めて重要です。例えば、インドのデジタルインディア・キャンペーンや中国のメイド・イン・チャイナ2025戦略は、複数のセクターにまたがるデジタルイノベーションと統合を強化するように設計されています。これらの政策は、デジタル機能の強化やスマートシティの開発に重点を置いた、官民双方からの多額の投資に支えられています。

- 企業は、クラウドコンピューティング、人工知能(AI)、モノのインターネット(IoT)などの先進技術に徐々に目を向け、業務効率を高め、イノベーションを促進し、カスタマーエクスペリエンスを向上させています。競争の激しいビジネス環境では、関連性と俊敏性を維持するためにデジタルトランスフォーメーションが必要となります。

- 2024年5月、製品エンジニアリング、データ/AI、企業向けソリューションのプロバイダーであるPeople Tech Groupは、製品エンジニアリングサービスを専門とする世界企業であるQuest Globalと提携し、世界中の顧客のデジタル変革イニシアチブを強化しました。この戦略的合併により、People Techのプロダクトエンジニアリング、データ/AI、エンタープライズソリューションにおける強力な能力と、Quest Globalの広範なリソース、専門知識、顧客リーチが組み合わされ、グローバルな顧客にサービスを提供するイノベーションとソリューションの力が生み出されます。

- 2024年3月、中国のデジタルトランスフォーメーション・サービス・プロバイダーであるデジタルチャイナ・グループは、バンコクのデジタル経済振興庁(DEPA)と覚書を交わしました。この合意は、クラウドコンピューティング、デジタルインフラ、ビッグデータセンター、デジタル人材の育成などの分野を含む、タイのデジタル経済諸国の発展における協力に焦点を当てています。両者は、特に人工知能を重視し、先進的なデジタル技術を推進することに専念しています。

- しかし、インフラの格差、高コスト、熟練した専門家の不足、規制の不整合、データプライバシーへの懸念、変化への抵抗、サイバーセキュリティの脅威といった要因が、市場の成長に大きなハードルとなっています。

アジア太平洋のデジタルトランスフォーメーション市場動向

IoTセグメントが最大の市場シェアを占める見込み

- 同市場は、製造業、自動車、ヘルスケアなどの主要セクターでIoT技術の採用が増加していることに後押しされ、成長率が上昇しています。IoTはインテリジェントな接続性という次の産業革命の先陣を切るもので、従来の製造業はデジタル変革の最中にあります。このシフトは、産業界が複雑なシステムや機械に取り組む方法を再構築し、効率を高めてダウンタイムを最小化することを目指しています。

- 製造業界では、主にコネクテッドデバイスやセンサーの普及により、M2M通信が促進され、データポイントが急増しています。さらに、フィールドデバイス、センサー、ロボットが進歩するにつれて、市場の範囲は広がっています。企業は、ロボット工学によって人間の労働力を補完するだけでなく、プロセスの不具合に起因する産業事故を減らすことを目的とした技術を活用し、機敏で革新的なアプローチにますます目を向けるようになっています。この変化は、インダストリー4.0の登場と、製造業におけるIoTの広範な受け入れに大きく起因しています。

- 2024年7月、韓国の通信事業者であるSKテレコム、KT、LGユープラスは、韓国無線振興協会(RAPA)と共に協定を結びました。その目的は、通信ネットワークとシームレスに統合する5G IoT製品の設計における中小製造業者の能力を強化することです。

- さらに、スマートシティ構想は、今後数年間のIoTの成長を牽引する構えです。IoTデバイスとシステムは、特に交通機関、公共事業、インフラで普及が見込まれています。この傾向に沿った政府の取り組みが、導入率をさらに押し上げると予想されます。

- 2024年2月、BTは英国のスマートシティや産業の発展を強化することを目的としたNB-IoTネットワークを発表しました。このネットワークは、英国の人口の97%をカバーし、EEの堅牢なモバイルインフラを基盤としています。BTのNB-IoTネットワークの導入は、街灯や地下水センサーのようなデータ需要の少ない資産をスマートネットワークにシームレスに統合することを可能にします。この統合は、これらの資産のバッテリー寿命を延ばすだけでなく、効率を高め、コストを削減します。

日本が急成長市場になる見込み

- 「Society 5.0」などの政府の取り組みが、日本のデジタルトランスフォーメーション市場を後押ししています。この推進は、スマートテクノロジーを社会にシームレスに統合することを目的としています。さらに、AI、IoT、ロボティクスの著しい進歩に後押しされ、市場は急速なイノベーションを経験しています。

- 日本におけるインターネット加入者数の増加は、オンラインサービスへの需要を高め、デジタルプラットフォームの導入を促進し、IoT、AI、クラウド技術の幅広い導入を可能にすることで、デジタルトランスフォーメーション市場を強化し、それによって様々な産業におけるイノベーションと効率性を促進します。TRAIによると、2023年12月現在、インドの首都デリーはインターネット加入者の集中度が最も高く、住民100人あたり257人近くが加入しています。これは人口100人あたりの加入者数67.3人という全国平均をはるかに上回っています。

- さらに、高齢化が進む日本では、労働力不足に対処するための自動化とデジタルソリューションの必要性が高まっています。これに対応するため、日本企業は競争力を維持するだけでなく、グローバルな足跡を広げるべく、デジタルのオーバーホールに多額の投資を行っています。さらに、シームレスなデジタルインタラクションに対する消費者の要求が高まるにつれ、企業は先端技術を採用せざるを得なくなっています。こうした要因が重なり合うことで、日本はデジタル変革に積極的な姿勢を示しています。

- 2024年4月、国際労働機関(ILO)は情報通信技術省(DICT)および日本政府と協力し、デジタルトランスフォーメーションセンター(DTC)を設立・発足させました。このセンターは、フィリピンのパンパンガ州のMSME(零細・中小企業)やその他の利害関係者に対応するよう特別に設計されています。このイニシアチブにより、デジタル化が促進され、企業はトレーニングやテクノロジーへのアクセスが向上します。

- 2024年7月、東京で日越デジタルトランスフォーメーション協会(VADX JAPAN)が正式に発足しました。同協会の目標は、日本のITセクターで活動するベトナム企業を結びつけ、先進的な技術イニシアチブとソリューションを交換するためのコラボレーションを促進することです。

アジア太平洋のデジタルトランスフォーメーション産業の概要

アジア太平洋のデジタルトランスフォーメーション市場は、アクセンチュアPLC、IBMコーポレーション、マイクロソフトコーポレーションなどの大手企業が存在するため、競争は緩やかです。市場企業は、戦略的パートナーシップや製品展開を通じてポートフォリオを強化し、持続的な競争力を追求しています。

- 2024年6月:データストリームは、マレーシアのシステムインテグレーターであるMRIC Alliance Sdn Bhdとの戦略的合弁事業(JVC)を通じて、マレーシアのデジタル変革を推進しました。このJVCは、複数のセクターに革命を起こそうとしています。ヘルスケアでは、個別化医療サービスの展開、ソリューションへのAIの活用、感染症への対応強化に重点が置かれています。

- 2024年4月:シンガポールとフィリピンは、人工知能(AI)とデジタルトランスフォーメーションを中心とした大きな成長機会を活用するために提携しました。さらに、再生可能エネルギーへの取り組み、炭素クレジット市場の設立、スマートシティなどの産業振興に共同で注力し、共通の関心を示しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度:ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 業界エコシステム分析(詳細範囲:デジタルトランスフォーメーション産業製品/ソリューションプロバイダーの主要利害関係者、システムインテグレーター/VAR、コネクティビティプロバイダー、規制機関、エンドユーザー、サービスプロバイダーなど)

- 現在の市場シナリオとデジタルトランスフォーメーション実践の進化

第5章 市場セグメンテーション

- タイプ別

- 人工知能と機械学習

- 現在の市場シナリオと予測期間の市場予測

- 主要成長影響要因(促進要因、課題、機会)

- タイプ別の市場内訳(需要予測/動向/市場展望)

- 機械学習

- 自然言語処理(NLP)

- コンテキスト対応コンピューティング

- コンピュータビジョン

- その他のタイプ

- エンドユーザー別の市場内訳(製造、石油・ガス、公益事業、自動車・運輸、小売、BFSI、プロセス産業、その他)

- 国別の市場内訳

- 主要市場の既存企業と新興企業の分析

- 市場展望

- 産業用途の拡張現実(VRとAR)

- 現在の市場シナリオと予測期間の市場予測

- 主要成長影響要因(促進要因、課題、機会)

- 使用事例別の市場内訳(トレーニング・シミュレーション、生産・組立、3Dモデリング、販売・マーケティング、その他)

- VRとARの相対成長予測分析

- 国別の市場内訳

- 主要市場の既存企業と新興企業の分析

- 市場の展望

- IoT

- 現在の市場シナリオと予測期間の市場予測

- 主要成長影響要因(促進要因、課題、機会)

- タイプ別の市場内訳(ソリューション、プラットフォーム、サービス)

- 使用事例別の市場内訳(予知保全、ビジネスプロセス最適化、資産追跡・サプライチェーン管理、その他)

- エンドユーザー別の市場内訳(自動車、プロセス産業、石油・ガス、自動車・航空宇宙、製造、その他)

- 国別の市場内訳

- 主要市場の既存企業と新興企業の分析

- 市場展望

- 産業用ロボット

- 現在の市場シナリオと予測期間の市場予測

- 主要成長影響要因(促進要因、課題、機会)

- タイプ別の市場内訳(多関節、リニア、円筒、パラレル、スカラ、その他)

- エンドユーザー別の市場内訳(金属・機械、電気・電子、自動車、化学・製造、その他)

- 国別の市場内訳

- 主要市場の既存企業と新興企業の分析

- 市場の展望

- ブロックチェーン

- 現在の市場シナリオと予測期間の市場予測

- 主要成長影響要因(促進要因、課題、機会)

- タイプ別の市場内訳(物流・サプライチェーン、偽造品管理、品質管理・コンプライアンス、その他)

- 使用事例別の市場内訳(自動車、航空宇宙・防衛、産業、小売、その他)

- 国別の市場内訳

- 主要市場の既存企業と新興企業の分析

- 市場展望

- デジタルツイン

- 現在の市場シナリオと予測期間の市場予測

- 主要成長影響要因(促進要因、課題、機会)

- タイプ別の市場内訳(製造、エネルギー・電力、航空宇宙、石油・ガス、その他)

- 国別の市場内訳

- 主要市場の既存企業と新興企業の分析

- 市場の展望

- 積層造形

- 現在の市場シナリオと予測期間の市場予測

- 主要成長影響要因(促進要因、課題、機会)

- タイプ別の市場内訳(装置、材料、サービス、ソフトウェア)

- エンドユーザー別の市場内訳(自動車、製造、ヘルスケア、その他)

- 国別の市場内訳

- 主要市場の既存企業と新興企業の分析

- 市場の展望

- 産業用サイバーセキュリティ

- 現在の市場シナリオと予測期間の市場予測

- 主要成長影響要因(促進要因、課題、機会)

- タイプ別の市場内訳(ネットワーク、アプリケーション、エンドポイント、クラウド、その他)

- エンドユーザー別の市場内訳(電力、公益事業、運輸、化学、製造)

- 国別の市場内訳

- 主要市場の既存企業と新興企業の分析

- 市場展望

- ワイヤレスコネクティビティ

- 現在の市場シナリオと予測期間の市場予測

- 主要成長影響要因(促進要因、課題、機会)

- タイプ別の市場内訳(Wi-Fi、NFC、ZigBee、Z-Wave、LTE Cat-M1、NB-IoT、Sigfox、その他)

- エンドユーザー別の市場内訳(自動車・運輸、産業、通信、ヘルスケア、その他)

- 産業用3Dプリント

- 現在の市場シナリオと予測期間の市場予測

- 主要成長影響要因(促進要因、課題、機会)

- マシン・サービス別の市場内訳

- エッジコンピューティング

- 現在の市場シナリオと予測期間の市場予測

- 主要成長影響要因(促進要因、課題、機会)

- ハードウェア、プラットフォーム、ソフトウェア、サービス別の市場内訳

- エンドユーザー別の市場内訳

- スマートモビリティ

- 現在の市場シナリオと予測期間の市場予測

- 主要成長影響要因(促進要因、課題、成長機会)

- タイプ別の市場内訳(交通管理、スマートチケット、モビリティライドシェアリング、ライドヘイリング、Mobility-as-a-Service、スマートハイウェイ)

- スマートマテリアル

- インテリジェント・プロセス・オートメーション

- 人工知能と機械学習

- 国別

- 中国

- インド

- 日本

- インドネシア

- フィリピン

- マレーシア

- シンガポール

- その他アジア太平洋

第6章 競合情勢

- 企業プロファイル

- Accenture PLC

- Google LLC(Alphabet Inc.)

- IBM Corporation

- Microsoft Corporation

- Oracle Corporation

- Hewlett Packard Enterprise

- SAP SE

- EMC Corporation(Dell EMC)

- Cognex Corporation

- Adobe Inc.

- Siemens AG

第7章 主要な変革技術

- 量子コンピューティング

- Manufacturing-as-a-Service(MaaS)

- コグニティブ・プロセス・オートメーション

- ナノテクノロジー

The Asia Pacific Digital Transformation Market size is estimated at USD 0.76 trillion in 2024, and is expected to reach USD 1.81 trillion by 2029, growing at a CAGR of 19.06% during the forecast period (2024-2029).

Technological, economic, and socio-political factors are driving the digital transformation market in Asia-Pacific.

Key Highlights

- The rapid rise in internet penetration and smartphone adoption has set a robust foundation for the expansion of digital services. The growth in demand for digital products and services in the region is bolstered by substantial investments in telecommunications infrastructure, particularly in developing nations. This demand is primarily fueled by the region's expanding middle class, marked by increasing disposable incomes and a growing digital literacy.

- Government initiatives are pivotal in driving this growth. For instance, India's Digital India campaign and China's Made in China 2025 strategy are designed to bolster digital innovation and integration, spanning multiple sectors. These policies are backed by significant investments from both the public and private sectors, with a focus on bolstering digital capabilities and developing smart cities.

- Businesses are gradually turning to advanced technologies like cloud computing, artificial intelligence (AI), and the Internet of Things (IoT) to boost operational efficiency, foster innovation, and elevate customer experiences. The competitive business environment necessitates digital transformation to maintain relevance and agility.

- In May 2024, People Tech Group, a provider of product engineering, data/AI, and enterprise solutions, partnered with Quest Global, a global company specializing in product engineering services, to enhance digital transformation initiatives for their worldwide clientele. Through this strategic merger, People Tech's strong capabilities in product engineering, data/AI, and enterprise solutions and Quest Global's extensive resources, expertise, and client reach are combined to create a force for innovation and solutions that serves clients globally.

- In March 2024, Digital China Group, a Chinese digital transformation service provider, inked a memorandum of understanding (MOU) with Bangkok's Digital Economy Promotion Agency (DEPA). The agreement focuses on collaborating in the development of Thailand's digital economy, including areas such as cloud computing, digital infrastructure, big data centers, and nurturing digital talent. Both parties are dedicated to pushing forward with advanced digital technologies, particularly emphasizing artificial intelligence.

- However, factors like infrastructure disparities, high costs, a shortage of skilled professionals, regulatory inconsistencies, data privacy concerns, resistance to change, and cybersecurity threats pose significant hurdles to the growth of the market.

Asia Pacific Digital Transformation Market Trends

The IoT Segment is Expected to Occupy the Largest Market Share

- The market is witnessing a rise in growth, propelled by the increasing embrace of IoT technology in key sectors like manufacturing, automotive, and healthcare. The traditional manufacturing sector is undergoing a digital transformation, with IoT spearheading the next industrial revolution of intelligent connectivity. This shift is reshaping how industries tackle their intricate systems and machines, aiming to boost efficiency and minimize downtime.

- The manufacturing industry is witnessing a surge in data points, mainly due to the widespread adoption of connected devices and sensors, facilitating M2M communication. Furthermore, as field devices, sensors, and robots advance, the market's scope is set to broaden. Enterprises are increasingly turning to agile, innovative approaches, leveraging technologies that not only complement human labor with robotics but also aim to reduce industrial accidents stemming from process failures. This shift is largely attributed to the advent of Industry 4.0 and the widespread acceptance of IoT in manufacturing.

- In July 2024, the Korean operators SK Telecom, KT, and LG Uplus, alongside the Radio Promotion Association of Korea (RAPA), inked a pact. The aim is to bolster the capacity of small and medium-sized manufacturers in designing 5G IoT products that seamlessly integrate with telecom networks.

- Moreover, smart city initiatives are poised to lead the growth of IoT in the coming years. IoT devices and systems are set to proliferate, especially in transportation, utilities, and infrastructure. Government initiatives aligning with this trend are anticipated to drive adoption rates further.

- In February 2024, BT unveiled its NB-IoT network, aimed at bolstering the advancement of smart cities and industries in the United Kingdom. This network, covering 97% of the UK populace, is built upon EE's robust mobile infrastructure. BT's NB-IoT network introduction enables the seamless integration of low-data-demand assets, like street lighting and underground water sensors, into smart networks. This integration not only prolongs the battery life of these assets but also boosts efficiency and cuts costs.

Japan is Expected to be the Fastest-growing Market

- Government initiatives, such as "Society 5.0," are propelling the Japanese digital transformation market. This push aims to seamlessly integrate smart technologies into society. Furthermore, the market is witnessing rapid innovation, buoyed by significant strides in AI, IoT, and robotics.

- The rising number of internet subscribers in Japan enhances the digital transformation market by increasing demand for online services, driving the adoption of digital platforms, and enabling the broader implementation of IoT, AI, and cloud technologies, thereby fostering innovation and efficiency across various industries. According to TRAI, as of December 2023, Delhi, the capital of India, boasted the highest concentration of internet subscribers, with an overall count of nearly 257 subscribers for every 100 residents. This far surpassed the national average of 67.3 subscribers per 100 people.

- Moreover, Japan's aging population is driving the imperative for automation and digital solutions to combat labor shortages. In response, Japanese firms are heavily investing in digital overhauls to not only stay competitive but also to broaden their global footprint. Moreover, as consumer demands for seamless digital interactions escalate, businesses are compelled to embrace advanced technologies. This confluence of factors underscores Japan's proactive stance in digital transformation.

- In April 2024, the International Labour Organization (ILO), in partnership with the Department of Information and Communications Technology (DICT) and the government of Japan, joined forces to establish and inaugurate the Digital Transformation Center (DTC). This center is specifically designed to cater to MSMEs (micro, small, and medium-sized enterprises) and other stakeholders in the region of Pampanga. This initiative will boost digitalization, granting enterprises improved access to training and technology.

- In July 2024, in Tokyo, the Vietnam-Japan Digital Transformation Association (VADX JAPAN) was officially launched, indicating a fresh era of digital collaboration between the two countries. The association's goal is to link Vietnamese businesses operating in Japan's IT sector, facilitating collaboration to exchange advanced technology initiatives and solutions.

Asia Pacific Digital Transformation Industry Overview

The Asia-Pacific digital transformation market is moderately competitive due to the presence of major players like Accenture PLC, IBM Corporation, and Microsoft Corporation. Market players are bolstering their portfolios and pursuing lasting competitive edges via strategic partnerships and product rollouts.

- June 2024: Marking a pivotal moment, Datastreams propelled Malaysia's digital transformation through a strategic joint venture (JVC) with MRIC Alliance Sdn Bhd, a Malaysian systems integrator. The JVC is set to revolutionize multiple sectors. In healthcare, its focus lies on rolling out personalized health services, leveraging AI for solutions, and enhancing responses to infectious diseases.

- April 2024: Singapore and the Philippines joined forces to harness significant growth opportunities, particularly in artificial intelligence (AI) and digital transformation. Moreover, they are jointly focusing on initiatives in renewable energy, establishing a carbon credit market, and advancing industries like smart cities, showcasing shared interests.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 INDUSTRY ECOSYSTEM ANALYSIS (Detailed Coverage of Key Stakeholders in Digital Transformation Industry Product/Solution Providers, System Integrators/VARs, Connectivity Providers, Regulatory Bodies, End-users, Service Providers, etc.)

- 4.4 CURRENT MARKET SCENARIO AND EVOLUTION OF DIGITAL TRANSFORMATION PRACTICES

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Artificial Intelligence and Machine Learning

- 5.1.1.1 Current Market Scenario and Market Projections for the Forecast Period

- 5.1.1.2 Key Growth Influencers (Drivers, Challenges, and Opportunities)

- 5.1.1.3 Market Breakdown by Type (Demand Forecasts | Trends | Market Outlook)

- 5.1.1.3.1 Machine Learning

- 5.1.1.3.2 Natural Language Processing (NLP)

- 5.1.1.3.3 Context-aware Computing

- 5.1.1.3.4 Computer Vision

- 5.1.1.3.5 Other Types

- 5.1.1.4 Market Breakdown by End-user (Manufacturing, Oil and Gas, Utilities, Automotive and Transportation, Retail, BFSI, Process Industries, and Others)

- 5.1.1.5 Market Breakdown by Country (United States and Canada)

- 5.1.1.6 Analysis of the Key Market Incumbents and Emerging Players

- 5.1.1.7 Market Outlook

- 5.1.2 Extended Reality (VR and AR) for Industrial Applications

- 5.1.2.1 Current Market Scenario and Market Projections for the Forecast Period

- 5.1.2.2 Key Growth Influencers (Drivers, Challenges, and Opportunities)

- 5.1.2.3 Market Breakdown by Use-cases (Training & Simulation, Production & Assembly, 3D Modeling, Sales & Marketing, and Others)

- 5.1.2.4 Relative Growth Forecast Analysis for VR & AR

- 5.1.2.5 Market Breakdown by Country (United States and Canada)

- 5.1.2.6 Analysis of the Key Market Incumbents and Emerging Players

- 5.1.2.7 Market Outlook

- 5.1.3 IoT

- 5.1.3.1 Current Market Scenario and Market Projections for the Forecast Period

- 5.1.3.2 Key Growth Influencers (Drivers, Challenges, and Opportunities)

- 5.1.3.3 Market Breakdown by Type (Solutions, Platforms, and Services)

- 5.1.3.4 Market Breakdown by Type (Solutions, Platforms, and Services)

- 5.1.3.5 Market Breakdown by Use-case (Predictive Maintenance, Business Process Optimization, Asset Tracking & Supply Chain Management, and Others)

- 5.1.3.6 Market Breakdown by End User (Automotive, Process Industries, Oil and Gas, Automotive and Aerospace, Manufacturing, and Others)

- 5.1.3.7 Market Breakdown by Country (United States and Canada)

- 5.1.3.8 Analysis of the Key Market Incumbents and Emerging Players

- 5.1.3.9 Market Outlook

- 5.1.4 Industrial Robotics

- 5.1.4.1 Current Market Scenario and Market Projections for the Forecast Period

- 5.1.4.2 Key Growth Influencers (Drivers, Challenges, and Opportunities)

- 5.1.4.3 Market Breakdown by Type (Articulated, Linear, Cylindrical, Parallel, SCARA, and Others)

- 5.1.4.4 Market Breakdown by End User (Metal and Machinery, Electrical and Electronics, Automotive, Chemical and Manufacturing, and Others)

- 5.1.4.5 Market Breakdown by Country (United States and Canada)

- 5.1.4.6 Analysis of the Key Market Incumbents and Emerging Players

- 5.1.4.7 Market Outlook

- 5.1.5 Blockchain

- 5.1.5.1 Current Market Scenario and Market Projections for the Forecast Period

- 5.1.5.2 Key Growth Influencers (Drivers, Challenges, and Opportunities)

- 5.1.5.3 Market Breakdown by Type (Logistics & Supply Chain, Counterfeit Management, Quality Control & Compliance, and Others)

- 5.1.5.4 Market Breakdown by Use-case (Automotive, Aerospace and Defense, Industrial, Retail and Others)

- 5.1.5.5 Market Breakdown by Country (United States and Canada)

- 5.1.5.6 Analysis of the Key Market Incumbents and Emerging Players

- 5.1.5.7 Market Outlook

- 5.1.6 Digital Twin

- 5.1.6.1 Current Market Scenario and Market Projections for the Forecast Period

- 5.1.6.2 Key Growth Influencers (Drivers, Challenges, and Opportunities)

- 5.1.6.3 Market Breakdown by Type (Manufacturing, Energy and Power, Aerospace, Oil & Gas, Others)

- 5.1.6.4 Market Breakdown by Country (United States and Canada)

- 5.1.6.5 Analysis of the Key Market Incumbents and Emerging Players

- 5.1.6.6 Market Outlook

- 5.1.7 Additive Manufacturing

- 5.1.7.1 Current Market Scenario and Market Projections for the Forecast Period

- 5.1.7.2 Key Growth Influencers (Drivers, Challenges, and Opportunities)

- 5.1.7.3 Market Breakdown by Type (Equipment, Materials, Services and Software)

- 5.1.7.4 Market Breakdown by End User (Automotive, Manufacturing, Healthcare, Others)

- 5.1.7.5 Market Breakdown by Country (United States and Canada)

- 5.1.7.6 Analysis of the Key Market Incumbents and Emerging Players

- 5.1.7.7 Market Outlook

- 5.1.8 Industrial Cyber security

- 5.1.8.1 Current Market Scenario and Market Projections for the Forecast Period

- 5.1.8.2 Key Growth Influencers (Drivers, Challenges, and Opportunities)

- 5.1.8.3 Market Breakdown by Type (Network, Application, Endpoint, Cloud, Others)

- 5.1.8.4 Market Breakdown by End User (Power, Utilities, Transportation, Chemicals & Manufacturing)

- 5.1.8.5 Market Breakdown by Country (United States and Canada)

- 5.1.8.6 Analysis of the Key Market Incumbents and Emerging Players

- 5.1.8.7 Market Outlook

- 5.1.9 Wireless Connectivity

- 5.1.9.1 Current Market Scenario and Market Projections for the Forecast Period

- 5.1.9.2 Key Growth Influencers (Drivers, Challenges, and Opportunities)

- 5.1.9.3 Market Breakdown by Type (Wi-Fi, NFC, ZigBee, Z-Wave, LTE Cat-M1, NB-IoT, Sigfox, Others)

- 5.1.9.4 Market Breakdown by End User (Automotive and Transportation, Industrial, Telecommunication, Healthcare, Others)

- 5.1.10 Industrial 3D Printing

- 5.1.10.1 Current Market Scenario and Market Projections for the Forecast Period

- 5.1.10.2 Key Growth Influencers (Drivers, Challenges, and Opportunities)

- 5.1.10.3 Breakdown by Machine & Services

- 5.1.11 Edge Computing

- 5.1.11.1 Current Market Scenario and Market Projections for the Forecast Period

- 5.1.11.2 Key Growth Influencers (Drivers, Challenges, and Opportunities)

- 5.1.11.3 Market Breakdown by Hardware, Platforms, Software and Services

- 5.1.11.4 Market Breakdown by End User

- 5.1.12 Smart Mobility

- 5.1.12.1 Current Market Scenario and Market Projections for the Forecast Period

- 5.1.12.2 Key Growth Influencers (Drivers, Challenges, and Opportunities)

- 5.1.12.3 Market Breakdown by Type (Traffic Management, Smart Ticketing, Mobility Ridesharing, Ride Hailing, Mobility-as-a-Service, and Smart Highway)

- 5.1.12.4 Smart Materials

- 5.1.12.5 Intelligent Process Automation

- 5.1.1 Artificial Intelligence and Machine Learning

- 5.2 By Country

- 5.2.1 China

- 5.2.2 India

- 5.2.3 Japan

- 5.2.4 Indonesia

- 5.2.5 Philippines

- 5.2.6 Malaysia

- 5.2.7 Singapore

- 5.2.8 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Accenture PLC

- 6.1.2 Google LLC (Alphabet Inc.)

- 6.1.3 IBM Corporation

- 6.1.4 Microsoft Corporation

- 6.1.5 Oracle Corporation

- 6.1.6 Hewlett Packard Enterprise

- 6.1.7 SAP SE

- 6.1.8 EMC Corporation (Dell EMC)

- 6.1.9 Cognex Corporation

- 6.1.10 Adobe Inc.

- 6.1.11 Siemens AG

7 KEY TRANSFORMATIVE TECHNOLOGIES

- 7.1 Quantum Computing

- 7.2 Manufacturing-as-a-Service (MaaS)

- 7.3 Cognitive Process Automation

- 7.4 Nanotechnology