|

市場調査レポート

商品コード

1550149

アジア太平洋の電子機器製造サービス:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Asia-Pacific Electronic Manufacturing Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋の電子機器製造サービス:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

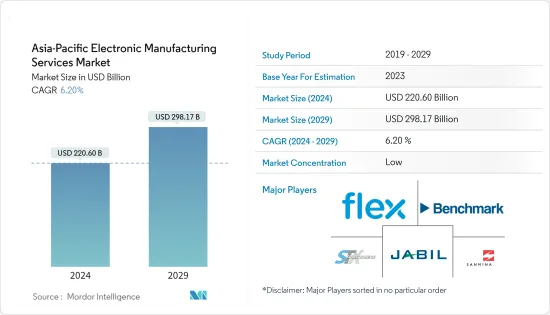

アジア太平洋の電子機器製造サービスの市場規模は、2024年に2,206億米ドルと推定され、2029年には2,981億7,000万米ドルに達すると予測され、予測期間中(2024年~2029年)のCAGRは6.20%で成長すると予測されます。

世界の大手電子機器ブランドは、中国やインドをはじめとするアジア太平洋諸国への製造拠点の移転を加速させています。同地域の費用対効果の高い労働力、確立されたサプライチェーン、政府による支援政策などがその理由です。その結果、アジア太平洋における電子機器製造サービス(EMS)プロバイダーのニーズが高まっています。これらのプロバイダーは、家電や幅広い電子製品の生産を強化する上で極めて重要です。

小型化の動向は、技術革新の急増を促進しました。より小型で強力な部品の台頭は、モノのインターネット(IoT)を実現する上で極めて重要です。小型化されたコンポーネントを搭載したデバイスは、コンパクトな設計によりサイズを縮小でき、機能性とユーザー体験を向上させることができます。さらに、小型化されたコンポーネントは一般的に消費電力が少なく、その魅力はさらに高まります。消費者の需要は、スマートフォン、ウェアラブル端末、IoTガジェットなど、より小型で持ち運び可能な電子機器へとシフトしています。この動向は、EMSプロバイダーがこれらの複雑な電子部品やアセンブリに対応できるよう、製造プロセスと能力を強化することを課題としています。

さらに、製造部門ではIIoT技術の採用が急増しています。これらの技術は、自動化、データ主導の意思決定、業務効率の向上を後押しします。EMSプロバイダーは、この地域でスマートセンサー、クラウドベースの分析、予知保全などのIIoTソリューションを活用しています。EMSプロバイダーは、製造プロセスを改善し、製品品質を向上させ、運用コストを抑制しています。IIoTを中核として、EMSプロバイダーは先進的な統合サービスの提供に乗り出し、世界の電子機器サプライチェーンにおける有力なパートナーとしての地位を固めています。

地域全体の政府の取り組みが市場成長を後押ししています。2023年8月、インド政府は、ノートパソコン、タブレット端末、パソコン、サーバーなど、さまざまな製品の輸入にライセンスを確保することを企業に義務付ける新たな規制を可決しました。これらの規制は、輸入ハードウェアの信頼性を高め、輸入依存度を下げ、国内製造を活性化することを目的としています。電子機器の国内生産を拡大することで、インドは技術的な自給率を高め、重要なサプライチェーンを確保し、電子機器製造の一大拠点になるという目標を達成しようとしています。

しかし、アジア太平洋市場の成長を妨げる主な課題のひとつは、規制の影響の数々です。この地域の企業は、地方、州、連邦、さらには外国の領域にまたがる広範な環境法規制を遵守しなければなりません。これらの規制は製造工程をカバーし、有害廃棄物の貯蔵、処理、排出、放出、廃棄にまで及びます。さらに、鉛の粉塵は電子機器の組み立て時に副産物として発生する可能性があるため、主要企業は施設の退去時でさえも鉛の粉塵に対処する必要があり、市場の成長を妨げる可能性があります。

さらに、アジア太平洋は、異なる規制の枠組み、貿易政策、コンプライアンス指令を持つ多様な国々で構成されています。この地域のEMSプロバイダーは、こうした様々な規格を理解し、遵守することに苦労しています。これらの基準は、製品の安全性や環境規制からデータプライバシー法まで多岐にわたるため、時間とリソースの両面で多大な投資が必要となります。

アジア太平洋の電子機器製造サービス市場動向

家電用途セグメントが大幅な成長を遂げる見込み

- 家電セグメントは、その拡大を推進するため、電子機器製造サービス(EMS)への依存度が高まっています。家電が高度な技術や機能を取り入れるにつれ、高度な製造の必要性が最も重要になります。コスト効率と適応性を重視するEMSは、消費者の期待に効果的に応える業界の能力を裏付けています。

- EMSは、プリント基板(PCB)のエンジニアリングと設計、アセンブリ、サブアセンブリ、機能テスト、製品と部品の設計を含みます。これらのサービスは、最新の消費者向け機器の需要に応えるものです。また、EMS企業は、付加価値の高いエンジニアリングや製造サービスを相手先ブランド製造業者(OEM)に提供しています。これにより、OEMは業務効率を高め、R&Dなどの重要な機能に集中できるようになり、進化する市場動向への適応が促進されます。

- 近年、中国やインドなどでは急速な都市化と経済成長が進み、中産階級が拡大しています。このような人口動態の急増により、スマートフォン、ノートパソコン、テレビ、家庭用製品など、家電製品に対する需要が高まっています。GSMAは、2030年までに同地域のスマートフォン普及率が90%を超えると予測し、同地域のハイテク意欲を裏付けています。特にスマートフォンは、家電分野の収益を牽引する極めて重要な存在です。その結果、同地域のEMSプロバイダーは、この消費者需要の高まりに対応する戦略的立場にあります。

- 政府はアジア太平洋の電子機器製造セクターを強化する政策を実施しています。こうした取り組みには、インセンティブを提供し、電子機器群や製造ハブの成長を促進することが含まれます。例えば、インドのPLI(Production Linked Incentive:生産連動型奨励金)制度は、電子機器産業の特定分野に的を絞って、現地生産品の販売増に対して4%~6%の奨励金を支給するものです。こうした的を絞った戦略は、EMSプロバイダーがこの地域で事業を立ち上げ、規模を拡大することを大いに後押ししています。

著しい成長が期待されるインド

- 予測期間中、インドは国内需要の高まりと輸出競争力の強化に後押しされ、電子機器製造における支配的な勢力として台頭する準備が整っています。急成長するインドの電子機器製造の中核には、電子機器製造サービス(EMS)があります。

- この産業の可能性を認識したインド政府は、電子機器製造を強化するためにいくつかの制度を導入しました。インド政府は、デジタルインディア構想の重要な柱として、電子機器のハードウェア製造を優先しています。また、生産連動奨励金(PLI)制度は、インドの高い資本コストに直接対応するものです。2023年11月、生産連動奨励金(PLI)制度は1兆300億インドルピー(約123億米ドル)を超える投資を集めました。

- 技術の導入、購入しやすい価格の拡大、持続可能性の推進が、国内の電子機器生産の成長に拍車をかけています。インダストリー4.0の出現は、AI、自動化、データ分析などのデジタルツールを企業が採用することで、この急成長を顕著に増幅させています。これらのテクノロジーは業務を合理化し、効率性と生産性を維持しています。

- 国内需要の急増と並行して、数多くの国際的な電子機器メーカーが、サプライチェーンを保護するためにインドのような国から製造委託先を移転しています。インド準備銀行とDGCI&Sによると、2023会計年度、インドの電子製品輸出は急増し、1兆8,990億インドルピー(約227億米ドル)を突破しました。これは前年度から大幅に増加しました。この変化は、外国投資を誘致するインド政府のイニシアチブによって後押しされ、主にインドのEMS市場に利益をもたらしています。

アジア太平洋の電子機器製造サービス産業の概要

アジア太平洋の電子機器製造サービス市場は競争が激しく、複数の企業が参入しています。各社は新製品の投入、事業の拡大、戦略的M&A、提携、協力関係の締結などにより、市場での存在感を高めようと絶えず努力しています。主な企業には、Benchmark Electronics Inc.、Flex Ltd.、Sanmina Corporationなどがあります。

2024年4月、製造サービスプロバイダーのZetworkは、様々なハイテク製品の生産能力強化を計画しています。同社は、ノートパソコン、サーバー、スマートフォン、ヒアラブル、テレビ、通信機器の設備増強に約100億インドルピー(約1億2,000万米ドル)の投資を計画しています。Zetworkは、インドと主要輸出市場である米国において、既存の電子機器製造サービスプロバイダーに対抗するためのポジショニングをとっています。

2024年2月、半導体業界の有力企業であるTaiwan Semiconductor Manufacturing Co.(TSMC)は、日本で初のチップ製造施設を稼働させ、同社の世界的成長戦略における重要な一歩を踏み出しました。TSMCは、約3年後に操業を開始する予定の日本第2工場の構想を発表しました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度:ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 市場のマクロ経済要因の評価

第5章 市場力学

- 市場促進要因

- 小型化の動向の高まり

- IIoT(産業用モノのインターネット)、ブロックチェーン、通信強化における新技術の採用

- 市場の課題

- 競合激化と厳しい政府・環境規制

- 知的財産権の侵害

第6章 市場セグメンテーション

- サービスタイプ別

- 電子機器設計・エンジニアリング

- 電子機器アセンブリ

- 電子機器製造

- その他のサービスタイプ

- 用途別

- 家電

- 自動車

- 産業用

- 航空宇宙・防衛

- ヘルスケア

- IT・通信

- その他の用途

- 国別

- 中国

- 日本

- インド

- 韓国

- 台湾

- オーストラリアとニュージーランド

第7章 競合情勢

- 企業プロファイル

- Benchmark Electronics Inc.

- Hon Hai Precision Industry Co. Ltd(Foxconn)

- Flex Ltd

- Sanmina Corporation

- Jabil Inc.

- SIIX Corporation

- Nortech Systems Incorporated

- Celestica Inc.

- Integrated Micro-electronics Inc.

- Creation Technologies LP

- Wistron Corporation

- Plexus Corporation

- Sumitronics Corporation

第8章 投資分析

第9章 市場の将来

The Asia-Pacific Electronic Manufacturing Services Market size is estimated at USD 220.60 billion in 2024, and is expected to reach USD 298.17 billion by 2029, growing at a CAGR of 6.20% during the forecast period (2024-2029).

Several leading electronics brands worldwide are increasingly moving their manufacturing bases to countries in Asia-Pacific, notably China and India. They are drawn by the region's cost-effective labor, well-established supply chains, and supportive governmental policies. Consequently, this migration fuels a rising need for electronics manufacturing services (EMS) providers in Asia-Pacific. These providers are crucial in bolstering the production of consumer electronics and a wide array of electronic goods.

The trend toward miniaturization has catalyzed a surge in technological innovation. The rise of smaller, more potent components has been pivotal in enabling the Internet of Things (IoT). With these compact designs, devices housing these miniaturized components can shrink in size, enhancing functionality and user experience. Additionally, smaller components typically demand less energy, further bolstering their appeal. Consumer demand is shifting toward smaller, more portable electronic devices, including smartphones, wearables, and IoT gadgets. This trend challenges EMS providers to enhance their manufacturing processes and capabilities to accommodate these intricate electronic components and assemblies.

Further, the manufacturing sector is witnessing a surge in the adoption of IIoT technologies. These technologies empower automation, data-driven decision-making, and heightened operational efficiency. EMS providers are capitalizing on IIoT solutions in the region, including smart sensors, cloud-based analytics, and predictive maintenance. They refine their manufacturing processes, elevate product quality, and curb operational expenses. With IIoT at its core, EMS providers are stepping up to deliver advanced, integrated services, solidifying their stance as favored partners in the worldwide electronics supply chain.

Government initiatives across the region are propelling market growth. In August 2023, India's government passed new regulations requiring companies to secure licenses for importing various products, including laptops, tablets, personal computers, and servers. These regulations aim to enhance trust in imported hardware, reduce import dependence, and stimulate local manufacturing. By ramping up domestic electronics production, India is striving to enhance its technological self-sufficiency, secure critical supply chains, and further its objective of becoming a major electronics manufacturing hub.

However, one of the primary challenges impeding the growth of the Asia-Pacific market is the array of regulatory implications. Businesses in this region must adhere to a spectrum of environmental laws and regulations spanning local, state, federal, and even foreign domains. These regulations cover the manufacturing processes and extend to the storage, treatment, discharge, emission, and disposal of hazardous waste byproducts. Furthermore, lead dust can be a byproduct during the electronics assembly, necessitating companies to address it, even during facility vacating, potentially stalling market growth.

Moreover, Asia-Pacific comprises diverse nations with distinct regulatory frameworks, trade policies, and compliance mandates. EMS providers in this region grapple with comprehending and complying with these varied standards. These standards range from product safety and environmental regulations to data privacy laws, necessitating substantial investments in both time and resources.

Asia-Pacific Electronic Manufacturing Services Market Trends

The Consumer Electronics Application Segment is Expected to Witness Significant Growth

- The consumer electronics segment increasingly relies on electronics manufacturing services (EMS) to drive its expansion. As consumer electronics embrace advanced technology and features, the need for sophisticated manufacturing becomes paramount. Its focus on cost efficiency and adaptability underscores the industry's ability to meet consumer expectations effectively.

- EMS involves the engineering and design of printed circuit boards (PCBs), assembly, sub-assemblies, functional testing, and product and component design. These services cater to the demand for modern consumer devices. Also, EMS firms provide value-added engineering and manufacturing services to original equipment manufacturers (OEMs). This allows OEMs to boost operational efficiencies and focus on critical functions like R&D, aiding their adaptation to evolving market trends.

- In recent years, rapid urbanization and economic growth in countries such as China and India have driven the expansion of the middle class. This demographic surge has increased demand for consumer electronics, spanning smartphones, laptops, TVs, and home appliances. GSMA projected that smartphone adoption in the region would surpass 90% by 2030, underlining the region's tech appetite. Smartphones, in particular, are pivotal in driving revenue within the consumer electronics sector. As a result, EMS providers in the region are strategically positioned to cater to this growing consumer demand.

- Governments have implemented policies to bolster the electronics manufacturing sector in Asia-Pacific. These initiatives involve providing incentives and fostering the growth of electronics clusters and manufacturing hubs. For example, India's Production Linked Incentive (PLI) scheme offers a 4% to 6% incentive on the augmented sales of locally made goods, with a targeted focus on specific segments within the electronics industry. Such targeted strategies have significantly encouraged EMS providers to set up and scale their operations in the region.

India is Expected To Witness Significant Growth

- During the forecast period, India is poised to emerge as a dominant force in electronics manufacturing, propelled by a rising domestic appetite and enhanced export competitiveness. At the core of India's burgeoning electronics manufacturing landscape lies electronics manufacturing services (EMS).

- Recognizing the industry's potential, the Indian government has introduced several schemes to bolster electronics manufacturing. The Indian government has prioritized electronics hardware manufacturing as an essential pillar of the Digital India initiative. In addition, the Production Linked Incentive (PLI) scheme directly addresses India's high capital costs. In November 2023, the Production Linked Incentive (PLI) scheme attracted investments exceeding INR 1.03 lakh crore (~USD 12.3 billion).

- Technology adoption, rising affordability, and a push for sustainability are set to fuel the growth of domestic electronics production in the country. The advent of Industry 4.0 is notably amplifying this surge, with businesses embracing digital tools like AI, automation, and data analytics. These technologies are streamlining operations and maintaining efficiency and productivity.

- Alongside surging domestic demand, numerous international electronics manufacturers are relocating their outsourced manufacturing from countries like India to safeguard their supply chains. According to the Reserve Bank of India and DGCI&S, in fiscal year 2023, India's exports of electronic products surged, surpassing INR 1,899 billion (~USD 22.7 billion). This marked a substantial increase from the preceding year. This shift is bolstered by the Indian government's initiatives to lure foreign investments, mainly benefiting the Indian EMS market.

Asia-Pacific Electronic Manufacturing Services Industry Overview

The Asia-Pacific electronic manufacturing services market is highly competitive and has several players. Companies continuously try to increase their market presence by introducing new products, expanding their operations, or entering into strategic mergers and acquisitions, partnerships, and collaborations. Some significant players include Benchmark Electronics Inc., Flex Ltd, and Sanmina Corporation.

In April 2024, Zetwork, a manufacturing service provider, planned to enhance its production capabilities for various tech products. The company plans to invest approximately INR 1,000 crore (~USD 120 million) in enhancing its laptops, servers, smartphones, hearables, televisions, and telecom equipment facilities. Zetwork is positioning itself to rival established electronics manufacturing services providers in India and its key export market, the United States.

In February 2024, Taiwan Semiconductor Manufacturing Co., a prominent player in the semiconductor industry, inaugurated its inaugural chip manufacturing facility in Japan, marking a significant stride in its worldwide growth strategy. TSMC unveiled intentions for a second Japanese plant, slated to commence operations in approximately three years.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 An Assessment of Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Trends of Miniaturization

- 5.1.2 Adoption of Emerging Technologies in IIoT (Industrial Internet of Things), Blockchain, and Enhanced Communication

- 5.2 Market Challenges

- 5.2.1 Intensifying Competition and Rigorous Government and Environmental Regulations

- 5.2.2 Intellectual Property Rights Infringements

6 MARKET SEGMENTATION

- 6.1 By Service Type

- 6.1.1 Electronics Design and Engineering

- 6.1.2 Electronics Assembly

- 6.1.3 Electronics Manufacturing

- 6.1.4 Other Service Types

- 6.2 By Application

- 6.2.1 Consumer Electronics

- 6.2.2 Automotive

- 6.2.3 Industrial

- 6.2.4 Aerospace and Defense

- 6.2.5 Healthcare

- 6.2.6 IT and Telecom

- 6.2.7 Other Applications

- 6.3 By Country

- 6.3.1 China

- 6.3.2 Japan

- 6.3.3 India

- 6.3.4 South Korea

- 6.3.5 Taiwan

- 6.3.6 Australia and New Zealand

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Benchmark Electronics Inc.

- 7.1.2 Hon Hai Precision Industry Co. Ltd (Foxconn)

- 7.1.3 Flex Ltd

- 7.1.4 Sanmina Corporation

- 7.1.5 Jabil Inc.

- 7.1.6 SIIX Corporation

- 7.1.7 Nortech Systems Incorporated

- 7.1.8 Celestica Inc.

- 7.1.9 Integrated Micro-electronics Inc.

- 7.1.10 Creation Technologies LP

- 7.1.11 Wistron Corporation

- 7.1.12 Plexus Corporation

- 7.1.13 Sumitronics Corporation