|

市場調査レポート

商品コード

1550157

北米の電子機器製造サービス:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)North America Electronic Manufacturing Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の電子機器製造サービス:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

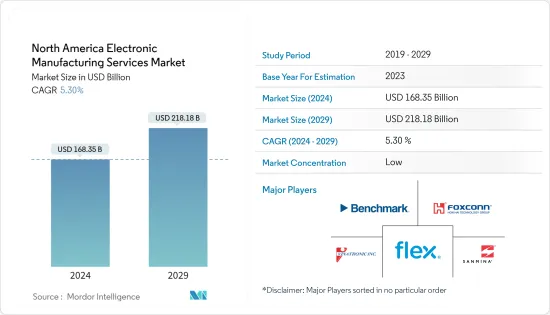

北米の電子機器製造サービスの市場規模は、2024年に1,683億5,000万米ドルと推定され、2029年には2,181億8,000万米ドルに達すると予測され、予測期間(2024年~2029年)のCAGRは5.30%で成長する見込みです。

電子機器製造に携わる企業は、OEM(相手先ブランド製造)メーカーに製品設計、エンジニアリング、製造などの幅広い付加価値サービスを提供することで、OEMメーカーは主に研究開発やマーケティング・販売などのその他の中核活動に専念できます。電子機器製造サービス(EMS)は、より一般的な用語である「受託製造」とも互換性があります。

産業モノのインターネット(IIoT)、電子部品の小型化の進展、5Gによる通信の強化など、新たな技術の普及が進む中、電子部品の設計と組み立てを革新する必要性は何年も前から感じられていました。また、北米では人件費の高騰によりEMSの需要が増加しており、電子機器業界で事業を展開するOEMは製造活動のアウトソーシングを余儀なくされています。

北米では、モノのインターネット(IIoT)とインダストリアル4.0が、スマートファクトリーオートメーションとして知られる物流チェーン全体の開発、生産、管理のための新しい技術的アプローチの中心となっています。これらは、機械やデバイスがインターネットを介して接続され、産業部門の動向を支配しています。

このような動向の結果、先進的な電子機器/部品に対する需要は大きく伸びています。このため、OEMが設計からエンジニアリング、生産に至るまで、電子機器生産プロセスのすべての側面をカバーすることが難しくなり、市場に有利なエコシステムが形成されています。そのため、専門的な製造サービスを提供するEMSプロバイダーに製造を委託するケースもあります。

消費者セグメントにおける電子機器需要の拡大も、同地域の市場成長を支える大きな要因です。電子機器/部品製造設備の開発がより複雑であることを考慮すると、大幅な需要増はOEMが事業を迅速に拡大することを困難にしています。そのため、一部のOEMは生産活動をEMS企業に委託しています。

しかし、電子機器製造設備の開発に必要な投資額が高いことなどは、市場の成長にとって大きな課題となっています。また、厳しい業界規制やガイドラインが存在するため、企業は製造工程や、これらの工程の副産物である有害廃棄物の保管、処理、排出、処分に関して、様々な地方、州、連邦、外国の環境法や規制に従わなければならず、この地域における市場の成長に課題があります。

また、電子機器の組み立て工程では鉛の粉塵が発生する可能性があり、企業は、製造施設の内部から鉛の粉塵を除去する責任があります。 企業はまた、建物内の空気中の鉛濃度も監視する必要があり、適用されるOSHAまたはその他の地域基準を超える重大な鉛濃度は認識されていません。

北米の電子機器製造サービス市場の動向

家電が大きな市場シェアを占める

- 北米は主要な消費者向け電子製品市場の1つです。米国やカナダなどの国々では、パソコン、スマートフォン、その他の家電製品などのデバイスの普及が発展途上国よりも著しく進んでおり、同国における電子機器製造サービスの成長に有利なエコシステムが形成されています。OEMは、市場の需要に応じた製品の供給を確保するため、サードパーティの受託製造業者からサポートを受けています。

- Consumer Technology Associationによると、米国の家電およびテクノロジー販売による収益は、2018年の4,130億米ドルに対し、2024年には5,120億米ドルに達すると推定されています。デジタル技術の受け入れ拡大がこの動向をさらに後押しし、この地域の家電製品需要を牽引しています。

- 同地域の家電産業の成長を支えるもう1つの主な要因は、サポートするインフラの利用可能性が高まっていることです。例えば、米国とカナダでは、5GやIoT、LoRaなどの接続ネットワークの拡大が顕著であり、市場成長に有利なエコシステムが形成されています。

- 高い需要と将来の成長見通しを考慮し、この地域で電子機器製造サービスを提供するベンダーの数も増加しています。例えば、August ElectronicsやAvalon Technologies Ltdは、カナダで電子機器製造サービスを提供しているベンダーです。同様に、米国にも同分野で事業を展開するベンダーが複数存在し、同地域の市場成長を支えています。

著しい成長を遂げる米国

- 米国は、北米における電子機器製造サービスの主要市場の1つであり続けると予想されます。その主な要因は、電子機器や電子部品の研究・設計に携わるOEMが多数存在することです。

- また、同国の電子製品に対する需要の高さも、電子機器製造サービスの需要に影響を与える大きな要因となっています。例えば、米国は産業オートメーション・ソリューションの主要市場の1つです。国際ロボット連盟によると、米国は産業用ロボットの主要な導入国の1つであり、毎年、かなりの数の産業用ロボットが国内に設置されています。

- 米国はまた、主要な自動車市場の1つでもあります。同国では、国内需要と輸出を満たすため、年間数百万台の自動車が生産されています。国内の各自動車メーカーの自動車製造施設は、精度と効率を維持するために高度に自動化されています。これが電子製品の需要を支え、同国の市場成長に有利なエコシステムを生み出しています。

- 先進的な電子機器の採用は、消費者分野でも増加しています。Consumer Technology Associationの推計によると、米国におけるスマートホームデバイスの売上高は、2018年の197億米ドルから2023年には235億米ドルに達する見込みです。こうした動向は、同国の電子機器製造サービス産業も促進すると思われます。

- さらに、パンデミックの余波を受けて、米国政府は、アウトソーシングに大きく依存していた電子機器・チップ製造業界の成長を支援するため、いくつかのイニシアチブを取りました。Chips and Science Law(チップと科学法)やBipartisan Infrastructure Law(超党派インフラ法)といったイニシアチブの開始には、半導体チップ生産を回復させるためのいくつかの条項があります。したがって、こうした動向も予測期間中の同国市場の成長を支えるものと予想されます。

北米の電子機器製造サービス産業の概要

北米の電子機器製造サービス市場は競争が激しく、複数の企業が参入しています。各社は新製品の投入、事業の拡大、戦略的M&A、提携、協力関係の締結などにより、市場での存在感を高めようと絶えず努力しています。主な企業には、Vinatronic Inc.、Benchmark Electronics Inc.、Flex Ltd.、Sanmina Corporationなどがあります。

2024年4月:インターナショナル・ビジネス・マシーンズ・コーポレーション(IBM)は、今後5年間で10億カナダドル(約7億3,000万米ドル)以上を投資し、カナダの半導体パッケージングとテスト施設を強化する意向を明らかにしました。初期段階として、IBMはパートナーのMiQro Innovation Collaborative Centreと共同で、2億2,700万カナダドル(約1億6,500万米ドル)をプロジェクトに投入します。この投資により、現在のケベック工場が拡張され、専用の研究開発ラボが設立されます。

2024年1月:エンド・ツー・エンドの電子機器製造サービスを提供するクリエーション・テクノロジーズが、米国ニューヨークに最新鋭の製造施設を新設しました。米国と中国に13の拠点を持つ同社は、米国でのプレゼンスをさらに強化し、顧客の進化する要求に応えるため、新たな施設を開設しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度:ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- COVID-19およびその他のマクロ経済要因が電子機器製造サービス市場に与える影響

第5章 市場力学

- 市場促進要因

- 小型化の動向の高まり

- IIoT(モノの産業インターネット)、ブロックチェーン、通信強化における新技術の採用

- 市場の課題

- 競合激化と厳しい政府・環境規制

- 知的財産権の侵害

第6章 市場セグメンテーション

- サービスタイプ別

- 電子機器設計・エンジニアリング

- 電子機器アセンブリ

- 電子機器製造

- その他のサービスタイプ

- 用途別

- 家電

- 自動車

- 産業用

- 航空宇宙・防衛

- ヘルスケア

- IT・通信

- その他の用途

- 国別

- 米国

- カナダ

第7章 競合情勢

- 企業プロファイル

- Vinatronic Inc.

- Benchmark Electronics Inc.

- Hon Hai Precision Industry Co. Ltd(Foxconn)

- Flex Ltd

- Sanmina Corporation

- Jabil Inc.

- SIIX Corporation

- Nortech Systems Incorporated

- Celestica Inc.

- Integrated Micro-electronics Inc.

- Creation Technologies LP

- Wistron Corporation

- Plexus Corporation

- TRICOR Systems Inc.

- Sumitronics Corporation

第8章 投資分析

第9章 市場の将来

The North America Electronic Manufacturing Services Market size is estimated at USD 168.35 billion in 2024, and is expected to reach USD 218.18 billion by 2029, growing at a CAGR of 5.30% during the forecast period (2024-2029).

Companies engaged in electronic manufacturing provide a wide range of value-added services such as product designing, engineering, and manufacturing for original equipment manufacturers (OEMs), allowing them to focus primarily on R&D and other core activities like marketing and sales. Electronic manufacturing services (EMS) are also interchangeably used with a more generic term, "contract manufacturing."

With the growing proliferation of emerging technologies such as the Industrial Internet of Things (IIoT), increasing miniaturization of electronic components, and enhanced communication posed by 5G, the need for revolutionizing electronic component design and assembly has been felt for years. Also, the demand for EMS in North America has been increasing owing to the higher labor cost, forcing OEMs operating in the electronics industry to outsource manufacturing activities.

In North America, the Industrial Internet of Things (IIoT) and Industrial 4.0 are central to the new technological approaches for developing, producing, and managing the entire logistics chain, otherwise known as smart factory automation. They dominate the industrial sector trends, with machinery and devices being connected via the Internet.

As a result of such trends, the demand for advanced electronic devices/components has been growing significantly. This creates a favorable ecosystem in the market as it becomes difficult for OEMs to cover all aspects of the electric device production process, ranging from design to engineering to production. Hence, some outsource the manufacturing to EMS providers offering specialized manufacturing services.

The growing demand for electronic devices in the consumer segment is another major factor supporting the market's growth in the region. Significant demand growth makes it hard for OEMs to scale their operations quickly, considering the higher complexity of developing electronic device/component manufacturing facilities. Hence, some OEMs outsource the production activities to EMS companies.

However, factors such as higher investment required in developing electronics manufacturing facilities are among the significant challenges for the market's growth. Also, the presence of stringent industry regulations and guidelines challenges the market's growth in the region as companies must follow various local, state, federal, and foreign environmental laws and regulations for manufacturing processes, as well as the storage, treatment, discharge, emission, and disposal of hazardous waste by-products of these processes.

Also, the electronics assembly process can generate lead dust, and companies are responsible for remediating lead dust from the interior of the manufacturing facility while vacating the space. Companies must also monitor for airborne lead concentrations in the buildings and are unaware of any significant lead concentrations over the applicable OSHA or other local standards.

North America Electronic Manufacturing Services Market Trends

Consumer Electronics to Hold a Significant Market Share

- North America is among the major consumer electronic goods markets. The proliferation of devices such as personal computers, smartphones, and other electronic home appliances is significantly higher in countries such as the United States and Canada than in developing countries, which creates a favorable ecosystem for the growth of electronic manufacturing services in the country. OEMs take support from third-party contract manufacturers to ensure the availability of products as per market demand.

- According to the Consumer Technology Association, revenue from consumer electronics and technology sales in the United States is estimated to reach USD 512 billion in 2024, compared to USD 413 billion in 2018. The growing acceptance of digital technologies further supports this trend, driving the region's demand for consumer electronic products.

- Another major factor supporting the growth of the consumer electronics industry in the region is the growing availability of supporting infrastructure. For instance, the United States and Canada have witnessed a notable increase in the expansion of 5G and other connectivity networks such as IoT and LoRa, creating a favorable ecosystem for the market's growth.

- Considering a higher demand and future growth prospects, the number of vendors offering electronic manufacturing services in the region is also increasing. For instance, August Electronics and Avalon Technologies Ltd are some vendors providing electronic manufacturing services in Canada. Similarly, several vendors operating in the same domain are present in the United States, which supports the market's growth in the region.

The United States To Witness Significant Growth

- The United States is expected to continue to be one of the leading markets for electronic manufacturing services in the North American region. The primary factor behind this is the presence of many OEMs engaged in the research and design of electronic devices and components.

- Also, a higher demand for electronic products in the country is another major factor influencing the demand for electronic manufacturing services. For instance, the United States is one of the major markets for industrial automation solutions. According to the International Federation of Robotics, the United States is among the primary adopters of industrial robots; each year, a significant number of industrial robots are installed in the country, which drives the demand for electronic devices/components.

- The United States is also among the major automotive markets. Millions of automobiles are produced annually in the country to fulfill local demand and export. The automotive manufacturing facilities of various car manufacturers in the country are highly automated to maintain accuracy and efficiency. This supports the demand for electronic products, creating a favorable ecosystem for the market's growth in the country.

- The adoption of advanced electronic devices is also increasing in the consumer segment. According to the Consumer Technology Association estimates, sales revenue from smart home devices in the United States was expected to reach USD 23.5 billion in 2023, up from USD 19.7 billion in 2018. Such trends will also promote the electronic manufacturing services industry in the country.

- Moreover, in the aftermath of the pandemic, the United States government has taken several initiatives to support the growth of the electronics and chip manufacturing industry, which was highly dependent on outsourcing. The launch of initiatives such as the Chips and Science Law and Bipartisan Infrastructure Law has several provisions to restore semiconductor chip production. Hence, such trends are also anticipated to support the country's market growth during the forecast period.

North America Electronic Manufacturing Services Industry Overview

The North American electronic manufacturing services market is highly competitive and has several players. Companies continuously try to increase their market presence by introducing new products, expanding their operations, or entering into strategic mergers and acquisitions, partnerships, and collaborations. Some of the major players include Vinatronic Inc., Benchmark Electronics Inc., Flex Ltd, and Sanmina Corporation.

April 2024 - International Business Machines Corp. (IBM) unveiled its intentions to bolster its Canadian semiconductor packaging and testing facility with over CAD 1 billion (~USD 730 million) investments over the next five years. In the initial phase, IBM, in collaboration with its partner, the MiQro Innovation Collaborative Centre, is injecting CAD 227 million (~USD 165 million) into the project. This investment will expand the current Quebec plant and establish a dedicated research and development lab.

January 2024 - Creation Technologies, an end-to-end electronic manufacturing service provider, opened a new state-of-the-art manufacturing facility in New York, United States. The company, with 13 locations in the United States and China, has opened a new facility to strengthen its presence in the United States further and meet the evolving requirements of its customers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 and Other Macroeconomic Factors on the Electronic Manufacturing Services Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Trends of Miniaturization

- 5.1.2 Adoption of Emerging Technologies in IIoT (Industrial Internet of Things), Blockchain, and Enhanced Communication

- 5.2 Market Challenges

- 5.2.1 Intensifying Competition and Rigorous Government and Environmental Regulations

- 5.2.2 Intellectual Property Rights Infringements

6 MARKET SEGMENTATION

- 6.1 By Service Type

- 6.1.1 Electronics Design and Engineering

- 6.1.2 Electronics Assembly

- 6.1.3 Electronics Manufacturing

- 6.1.4 Other Service Types

- 6.2 By Application

- 6.2.1 Consumer Electronics

- 6.2.2 Automotive

- 6.2.3 Industrial

- 6.2.4 Aerospace and Defense

- 6.2.5 Healthcare

- 6.2.6 IT and Telecom

- 6.2.7 Other Applications

- 6.3 By Country

- 6.3.1 United States

- 6.3.2 Canada

7 COMPETITIVE LANDSCAPE*

- 7.1 Company Profiles

- 7.1.1 Vinatronic Inc.

- 7.1.2 Benchmark Electronics Inc.

- 7.1.3 Hon Hai Precision Industry Co. Ltd (Foxconn)

- 7.1.4 Flex Ltd

- 7.1.5 Sanmina Corporation

- 7.1.6 Jabil Inc.

- 7.1.7 SIIX Corporation

- 7.1.8 Nortech Systems Incorporated

- 7.1.9 Celestica Inc.

- 7.1.10 Integrated Micro-electronics Inc.

- 7.1.11 Creation Technologies LP

- 7.1.12 Wistron Corporation

- 7.1.13 Plexus Corporation

- 7.1.14 TRICOR Systems Inc.

- 7.1.15 Sumitronics Corporation