|

市場調査レポート

商品コード

1550148

欧州の電子機器製造サービス:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Europe Electronic Manufacturing Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の電子機器製造サービス:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

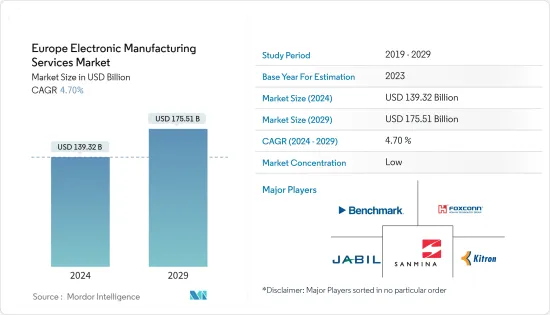

欧州の電子機器製造サービス市場規模は、2024年に1,393億2,000万米ドルと推定され、2029年には1,755億1,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは4.70%で成長すると予測されます。

欧州には数多くのイノベーション拠点があり、イノベーションと強力な研究開発能力に対する評判を維持しています。コンシューマーエレクトロニクスが急速に進歩する中、欧州のEMSプロバイダーはこうしたイノベーションセンターに近いという利点を活かし、最新技術へのアクセスを確保しています。

モノのインターネット(IoT)や人工知能(AI)のような技術の導入に後押しされ、業界全体でデジタル化が急速に進んでいるため、電子部品や製造サービスのニーズが高まっています。欧州委員会によると、欧州におけるIoT支出は大幅に増加しています。デジタル化に軸足を置き、包括的なソリューションを提供することで、地域のEMSプロバイダーはこうした動向を活用することができます。

さらに、パーソナライズされた電子機器に対する消費者の嗜好の高まりが、俊敏な製造に長けたEMSプロバイダーの需要を促進しています。EMS企業はこの需要に応えるため、3Dプリンティング、フレキシブルエレクトロニクス、モジュール設計などの最先端技術を取り入れています。これらの技術革新により、EMSプロバイダーは様々な顧客ニーズに対応したオーダーメイド・ソリューションを提供できるようになり、競合情勢の中で一歩抜きん出た存在となっています。

さらに、いくつかの地域では政府の取り組みが活発化しており、市場の成長を後押ししています。例えば、欧州委員会は2023年4月、電化製品のエネルギー消費を抑制するための厳しい規制を導入しました。この規制は外部電源を備えた機器にも適用され、特に小型ネットワーク機器(Wi-Fiルーターやモデムなど)やワイヤレススピーカー(特に「スタンバイ」モード時)をターゲットとしています。委員会は、アイドル状態での消費電力削減を義務付けることにより、2030年までに累積4TWhの削減が見込まれるとし、大幅な省エネの可能性を予測しています。これらの基準は、エネルギー効率を高め、温室効果ガスの排出を抑制することを目的としています。

同様に、英国はインダストリー4.0の導入で大きく前進し、企業、消費者、労働者が広く参加しています。産業戦略省は、イノベーションを加速させ、インダストリー4.0ソリューションを取り入れることで、英国の製造業は今後10年間で大きな成長を遂げ、産業用電子機器の需要を生み出し、市場にチャンスをもたらすと予測しています。

しかし、IoT、5G、EVなどの技術に対する需要の急増は、電子部品に対するかつてないニーズを煽り、しばしば利用可能な供給を上回っています。チップやコンデンサーのような重要な原材料や部品の不足は、生産の遅れを引き起こしています。この問題をさらに深刻にしているのは、部品サプライヤーの滞留がリードタイムを数週間から数カ月に延ばしていることです。こうした混乱はEMSメーカーの組立工程を妨げ、タイムリーな製品納入を複雑にしています。

エレクトロニクス製造業界は急速に進化しており、生産者がそれに追いつくための課題となっています。主なハードルには、労働力のスキルアップや生産設備の近代化が含まれ、製造コストの増加や遅延につながることが多いです。

欧州電子機器製造サービス市場動向

エレクトロニクス設計・エンジニアリングサービスタイプが大きな市場シェアを占める見込み

- コンピュータ支援エンジニアリング、IC物理設計、検証を含む電子設計ツールは、よりスマートな設計時代の到来を告げています。設計時間とエラーを削減することで、これらのツールは大きな人気を集めています。電子設計自動化(EDA)ツールの採用は、特に自動車や航空宇宙などの分野で着実に増加しています。しかし、EDAツールの顕著な欠点は、過去の設計から洞察を引き出す能力が限られていることです。

- 大量の複雑なチップ、特にコンシューマー・エレクトロニクス向けの需要が高まっていることから、エレクトロニクス設計企業は、EDAツールセットで機械学習を利用するようになっています。機械学習は、モデリングとシミュレーションを通じて半導体業界に対する深い洞察を提供し、精度と効率の向上を約束することで、エンジニアをより自動化へと向かわせる。電子デバイスメーカーは、機械学習によって強化されたEDAツールの利点を目の当たりにすると、これらの先進的なソリューションを迅速に採用します。このシフトは、設計とチップのイノベーションを促進し、EDAツールの普及を後押しします。

- さらに、AI主導の設計自動化ツールは、回路設計、PCBレイアウト、システムアーキテクチャを、設定された要件や制約に従って自律的に作成します。これらのツールは手作業を凌駕し、より広範な設計領域を迅速にナビゲートし、新しいトポロジーやアーキテクチャの発見につながります。生成的敵対ネットワーク(GAN)や強化学習などの最先端技術は、斬新な設計コンセプトを生み出すために活用されています。さらに、欧州ではいくつかの産業でAI技術が広く採用されつつあり、これは市場成長にとって好材料となり得る。Eurostatによると、2023年、欧州ではデンマークがAIを15.2%導入しており、この地域全体で最も高いです。

- 欧州政府が半導体製造を強化するために行っているイニシアチブも、同地域の市場成長に好影響を与えています。例えば、2023年、欧州連合(EU)は、半導体ファブを開発し、欧州全体の半導体生産エコシステムを支援するChips Actと呼ばれる430億ユーロ(~475億USD)計画を承認しました。

ドイツが大きな市場シェアを占める見込み

- 製造部門は、自動車、化学、エンジニアリング、耐久消費財、医薬品などの重要産業により、ドイツの経済成長に不可欠です。連邦統計局によると、2023年第4四半期のドイツの製造業のGDPは193兆7,360億ユーロで、2022年第4四半期の183兆6,970億ユーロから大幅に増加しました。これは、同国が自動化とプロセス主導の製造業へと着実に移行していることを反映しており、効率性の向上と生産性の強化が見込まれています。

- 同国には、多くの自動化製造設備がある著名な分野のひとつ、自動車産業があります。精度と効率を維持するため、さまざまな自動車メーカーの製造設備が自動化されていることが確認されています。また、従来の自動車をEVに置き換える傾向が強まっていることから、自動車産業における需要の拡大が見込まれています。例えば、KBAによると、ドイツでは電気自動車の新規登録が大幅に増加しています。2023年には、52万4,219台の電気自動車が新たに登録されました。最新のEVにはより多くの電子ユニットが搭載されているため、こうした動向はこの地域の市場成長にとって有利なエコシステムを生み出しています。

- 自動車産業の電動化動向の変化はエンジンだけにとどまらず、自動電動窓、パワーステアリング、ADASといった機能を自動車に浸透させています。こうした進歩が自動車産業を最前線に押し上げ、エレクトロニクス製造サービス市場の需要を牽引しています。

- ドイツはまた、熟練したエンジニア、技術者、製造要員の豊富な蓄積を誇り、EMSプロバイダーに豊富な人材プールを提供しています。継続的なトレーニングとスキルアップの取り組みは、従業員が進化する技術に後れを取らず、革新的な気風を培うのに役立っています。このような技術力は、最先端の設計、プロトタイピング、製造サービスの提供に役立っています。

欧州の電子機器製造サービス産業の概要

欧州の電子機器製造サービス市場は競争が激しく、複数の地域および世界プレーヤーが存在します。重要なプレーヤーは、新製品の導入、事業の拡大、戦略的M&A、提携、協力関係の締結などにより、市場での存在感を高めようと絶えず努力しています。

- 2024年5月、地域の著名なプライベート・エクイティおよびインフラ投資マネージャーであるForesight Groupは、Assembly Contracts Limitedへの450万英ポンド(~570万米ドル)の投資を公表しました。電子機器用プリント基板アセンブリ(PCBA)製造の主要企業であるACLは、フォーサイトの支援により事業を拡大し、さらなる熟練工の雇用機会を創出する予定です。

- 2024年5月、TSMC欧州の社長は、ドイツ東部のドレスデンに同社初のチップ工場を建設する計画を確認しました。建設は2024年第4四半期に着工し、2027年に生産を開始する予定です。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 市場のマクロ経済要因の評価

第5章 市場力学

- 市場促進要因

- デジタル化とインダストリー4.0統合の進展

- 複数の地域政府規制による持続可能性とグリーン製造への志向の高まり

- 市場抑制要因

- 原材料コストの上昇

- 地域的な規制とコンプライアンス問題の増加

第6章 市場セグメンテーション

- サービスタイプ別

- エレクトロニクス設計とエンジニアリング

- エレクトロニクス組立

- エレクトロニクス製造

- その他のサービスタイプ

- 用途別

- コンシューマーエレクトロニクス

- 自動車

- 産業

- 航空宇宙・防衛

- ヘルスケア

- ITおよび電気通信

- その他の用途

- 国別

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- オランダ

第7章 競合情勢

- 企業プロファイル

- Benchmark Electronics Inc.

- Hon Hai Precision Industry Co. Ltd(Foxconn)

- Kitron ASA

- Sanmina Corporation

- Jabil Inc.

- SIIX Corporation

- Celestica Inc.

- Integrated Micro-electronics Inc.

- Wistron Corporation

- Plexus Corporation

- BMK Group

第8章 投資分析

第9章 市場の将来

The Europe Electronic Manufacturing Services Market size is estimated at USD 139.32 billion in 2024, and is expected to reach USD 175.51 billion by 2029, growing at a CAGR of 4.70% during the forecast period (2024-2029).

Europe's numerous innovation hubs maintain its reputation for innovation and robust R&D capabilities. With consumer electronics advancing swiftly, European EMS providers leverage their proximity to these innovation centers, ensuring access to the latest technologies.

The surge in digitalization across industries, fueled by the adoption of technologies like the Internet of Things (IoT) and artificial intelligence (AI), strengthens the need for electronic components and manufacturing services. According to the European Commission, IoT spending in Europe has grown significantly. By pivoting toward digitalization and providing comprehensive solutions, regional EMS providers stand to capitalize on such trends.

In addition, the rising consumer preference for personalized electronics is fueling the demand for EMS providers adept at agile manufacturing. EMS firms are embracing cutting-edge technologies like 3D printing, flexible electronics, and modular designs to meet this demand. These innovations empower EMS providers to deliver bespoke solutions, catering to various customer needs and setting themselves apart in a competitive landscape.

Further, rising government initiatives in several regional countries drive the market's growth. For instance, in April 2023, the European Commission introduced stringent regulations to curb energy consumption in electrical appliances. These rules extend to devices with external power supplies, notably targeting small network equipment (like Wi-Fi routers and modems) and wireless speakers, especially when in 'standby' mode. The commission projects a substantial energy-saving potential by mandating lower power consumption during idle states, estimating a cumulative 4 TWh reduction by 2030. These standards are designed to boost energy efficiency and curb greenhouse gas emissions.

Similarly, the United Kingdom made significant strides in embracing Industry 4.0, with widespread participation from businesses, consumers, and the workforce. The Department of Industrial Strategy projects that by accelerating innovations and embracing Industry 4.0 solutions, the UK's manufacturing sector could see significant growth in the coming decade, creating demand for industrial electronic devices and driving opportunities in the market.

However, surging demand for technologies such as IoT, 5G, and EVs is fueling an unprecedented need for electronic components, often surpassing available supply. Shortages of crucial raw materials and components like chips and capacitors are causing production delays. Compounding the issue, backlogs at component suppliers have stretched lead times from weeks to months. These disruptions hamper EMS manufacturers' assembly processes and complicate timely product deliveries.

The electronics manufacturing industry is rapidly evolving, posing challenges for producers to keep pace. Key hurdles include upskilling the workforce and modernizing production facilities, frequently leading to increased production costs and delays.

Europe Electronic Manufacturing Services Market Trends

Electronics Design and Engineering Service Type is Expected to Hold Significant Market Share

- Electronic design tools, including computer-aided engineering, IC physical design, and verification, have ushered in a smarter design era. By reducing design time and errors, these tools have garnered significant popularity. The adoption of electronic design automation (EDA) tools has steadily risen, especially in sectors like automotive and aerospace. However, a notable drawback of EDA tools is their limited ability to draw insights from past designs.

- Given the rising demand for large volumes of complex chips, particularly for consumer electronics, electronics design firms increasingly turn to machine learning in their EDA toolsets. Machine learning offers profound insights into the semiconductor industry through modeling and simulation and promises heightened accuracy and efficiency, nudging engineers toward greater automation. As electronic device manufacturers witness the benefits of EDA tools enhanced by machine learning, they swiftly embrace these advanced solutions. This shift fosters innovation in designs and chips and fuels the widespread adoption of EDA tools.

- Further, AI-driven design automation tools autonomously create circuit designs, PCB layouts, and system architectures, adhering to set requirements and constraints. They outpace manual methods, swiftly navigating a broader design spectrum, leading to the discovery of novel topologies and architectures. Cutting-edge techniques, including generative adversarial networks (GANs) and reinforcement learning, are harnessed to birth fresh design concepts. In addition, Europe is widely adopting AI technologies for several industries, which can be a boon for market growth. According to Eurostat, in 2023, Denmark, in Europe, had 15.2% of AI adoption, the highest across the region.

- Initiatives taken by European governments to strengthen semiconductor manufacturing are also favoring the market's growth in the region. For instance, in 2023, the European Union (EU) approved a EUR 43 billion (~USD 47.5 billion) plan called the Chips Act to develop semiconductor fabs and support Europe's overall semiconductor production ecosystem.

Germany is Expected To Hold Significant Market Share

- The manufacturing sector is integral to Germany's economic growth, owing to critical industries like automotive, chemicals, engineering, consumer durables, and pharmaceuticals. In Q4 2023, Germany's manufacturing sector reported a GDP of EUR 193,736 billion, reflecting a significant increase from EUR 183,697 billion in Q4 2022, according to the Federal Statistical Office. This reflects that the country is steadily moving toward automation and process-driven manufacturing, which are projected to improve efficiency and enhance productivity.

- The country has one of the prominent sectors with many automation manufacturing facilities: the automobile industry. To maintain accuracy and efficiency, it was observed that the manufacturing facilities of various car manufacturers were automated. In addition, the demand in the automobile industry is expected to grow due to an increasing trend toward replacing traditional vehicles with EVs. For instance, according to KBA, Germany has witnessed a substantial surge in registering new electric cars. In 2023, the country registered a notable 524,219 new electric vehicles. As modern EVs contain more electronic units, such trends create a favorable ecosystem for the market's growth in the region.

- The shift in the automotive industry's electrification trend extends beyond the engines, permeating the vehicles with features like automated electric windows, power steering, and ADAS. These advancements have propelled the automotive industry to the forefront, making it a key driver of demand in the electronics manufacturing services market.

- Germany also boasts a substantial reservoir of skilled engineers, technicians, and manufacturing personnel, providing EMS providers with a rich talent pool. Ongoing training and upskilling initiatives help employees stay abreast of evolving technologies and cultivate an innovative ethos. This technical prowess is instrumental in offering cutting-edge design, prototyping, and manufacturing services.

Europe Electronic Manufacturing Services Industry Overview

The European electronic manufacturing services market is competitive and has several regional and global players. Significant players continuously try to increase their market presence by introducing new products, expanding their operations, or entering into strategic mergers and acquisitions, partnerships, and collaborations.

- In May 2024, Foresight Group, a prominent regional private equity and infrastructure investment manager, disclosed a GBP 4.5 million (~USD 5.70 million) investment in Assembly Contracts Limited. ACL, a key player in manufacturing printed circuit board assemblies (PCBAs) for electronic devices, is set to expand its operations and generate additional skilled employment opportunities courtesy of Foresight's backing.

- In May 2024, the President of TSMC Europe confirmed the company's plans to build its inaugural chip plant in Dresden, eastern Germany. Construction is set to kick off in the fourth quarter of 2024, with production slated to commence in 2027.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 An Assessment of Macroeconomic Factors on The Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Digitalization and Industry 4.0 Integration

- 5.1.2 Increasing Inclination Towards Sustainability and Green Manufacturing Owing to Several Regional Government Regulations

- 5.2 Market Restraints

- 5.2.1 Rising Cost of Raw Materials

- 5.2.2 Increasing Regional Regulatory and Compliance Issues

6 MARKET SEGMENTATION

- 6.1 By Service Type

- 6.1.1 Electronics Design and Engineering

- 6.1.2 Electronics Assembly

- 6.1.3 Electronics Manufacturing

- 6.1.4 Other Service Types

- 6.2 By Application

- 6.2.1 Consumer Electronics

- 6.2.2 Automotive

- 6.2.3 Industrial

- 6.2.4 Aerospace and Defense

- 6.2.5 Healthcare

- 6.2.6 IT and Telecom

- 6.2.7 Other Applications

- 6.3 By Country

- 6.3.1 United Kingdom

- 6.3.2 Germany

- 6.3.3 France

- 6.3.4 Italy

- 6.3.5 Spain

- 6.3.6 Netherlands

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Benchmark Electronics Inc.

- 7.1.2 Hon Hai Precision Industry Co. Ltd (Foxconn)

- 7.1.3 Kitron ASA

- 7.1.4 Sanmina Corporation

- 7.1.5 Jabil Inc.

- 7.1.6 SIIX Corporation

- 7.1.7 Celestica Inc.

- 7.1.8 Integrated Micro-electronics Inc.

- 7.1.9 Wistron Corporation

- 7.1.10 Plexus Corporation

- 7.1.11 BMK Group