|

|

市場調査レポート

商品コード

1550004

北米の業務用暖房・換気・空調(HVAC)機器:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)North America Commercial Heating, Ventilation, And Air Conditioning (HVAC) Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の業務用暖房・換気・空調(HVAC)機器:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

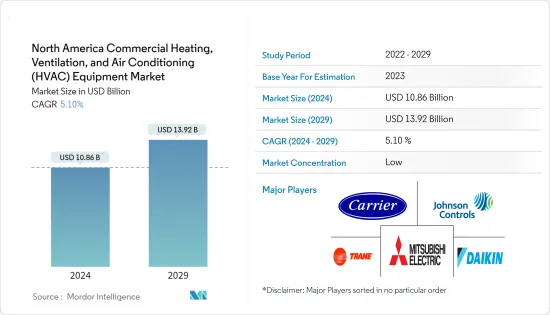

北米の業務用暖房・換気・空調(HVAC)機器の市場規模は、2024年に108億6,000万米ドルと推定され、2029年には139億2,000万米ドルに達し、予測期間(2024年~2029年)のCAGRは5.10%で成長すると予測されます。

主なハイライト

- 北米のHVAC市場の成長を牽引しているのは、ヒートポンプ導入に対する政府支援の増加、地球温暖化に関する懸念の高まり、HVAC機器の技術進歩です。さらに、改修工事への支出の増加が市場成長を牽引しています。

- 現在の世界のエネルギー危機は、より安価で信頼性が高く、よりクリーンな建物暖房の方法への移行が急務であることを示唆しています。北米の小売スペース、オフィススペース、学校、大学などの商業ビルの多くは、いまだに化石燃料(主に天然ガス)に依存しており、その結果、大量の温室効果ガスが排出されています。そのため、ヒートポンプは、商業スペースに効率的に暖房を供給することができ、暖房をより安全で持続可能なものにするための重要な技術の1つであるとして、支持を集めています。

- 米国とカナダの政府は、ヒートポンプの導入を義務付ける厳しい規制を導入し、市場にプラスの影響を与えることを期待しています。2023年9月、25の州知事で構成される米国気候同盟とバイデン政権は、2030年までに米国の住宅におけるヒートポンプの数を4倍に増やすことを目指し、470万台から2,000万台に達すると表明しました。これは、世界の温室効果ガス排出量の30%以上を建物が占めているためです。

- 北米では気候が寒冷化しているため、暖房機器の需要が増加すると予想されています。気候研究者は、米国における突然の極端な寒波は、地球規模の暖房によって引き起こされる可能性があると理論化しています。北極圏は地球の他の地域より4倍の速さで温暖化しており、極渦として知られる風の円形パターンに変化をもたらし、通常、寒気は極域に集中します。

- さらに2024年には、カナダのノースウエスト準州からアルバータ州に極寒の北極空気が流れ込み、カナダ環境省は極寒警報を発令しました。この寒冷前線は、ロッキー山脈から米国北部の平原に向かった後、南下し、複数の場所で日中の低気温の記録を更新する可能性があります。

- 現代のHVAC業界は、AIとモノのインターネット(IoT)技術の統合により、インテリジェント技術に向かっています。現代のヒートポンプは「90年代のヒートポンプ」とは大きく異なります。AIを搭載した冷暖房技術は、室内温度、設定温度、室外温度を自動的に管理することができます。主要なHVACシステム・プロバイダーは最新の先端技術を取り入れており、今後数年間の市場成長を後押しします。

- さらに、ロシア・ウクライナ戦争は世界のサプライチェーンを停止させ、北米のHVAC機器の販売に直接影響を与えています。また、米国労働省のデータによると、米国のインフレ率は鈍化したものの、1年間は高止まりしています。米国の1月までの12ヵ月間の年間インフレ率は3.1%で、前回の3.4%から低下しました。米国とカナダ全体でインフレ率が低下していることが、今後数年間の市場成長の原動力となると思われます。

北米の業務用暖房・換気・空調(HVAC)機器市場の動向

空調設備は予測期間中に著しい成長が見込まれる

- 北米では、セントラル空調システムが商業ビルで普及しています。もう一つの人気オプションは、ダクトレス・ミニスプリット・システムです。これらはゾーン冷房を提供し、家のさまざまなエリアの温度を独立して制御できます。セントラル空調は、冷媒を使って室内の空気から熱を吸収し、それを室外に移動させることで、より涼しい室内環境を作り出します。北米では、可変速コンプレッサーを搭載した高効率のセントラル空調が、その省エネ効果と価格による温度制御のためにますます支持されています。

- AHRIによると、2023年の米国における空調機器の出荷台数は504万台で、2022年の水準(605万台)よりは減少していますが、2010年以来一貫して増加しています。ダイキン工業は、2023年に発表した低価格空調を販売することで、米国でトップの空調システムサプライヤーになることを計画しています。このような主要ベンダーの成長戦略が市場成長を押し上げると思われます。

- EIAによると、商業ビルは面積ベースで34%成長する見込みです。オフィスビルは、他のタイプのビルに比べて空調に多くのエネルギーを使用します。2050年には、米国の商業部門で空調に消費されるエネルギーの25%が商業ビルで消費されることになります。

- ダクトレス・ミニスプリット・システムは、その柔軟性から人気を集めています。ダクトレス・ミニスプリットは、ダクトを使わずにゾーンや部屋ごとに個別の温度制御が可能なため、既存の建物の改修や特定のエリアへの冷房能力の追加に最適です。

- また、米国エネルギー省(DOE)やエネルギースタープログラムなどのエネルギー基準や規制が、商業ビルにおけるエネルギー効率の高い空調機器の採用を後押ししています。ビルの所有者や運営者は、環境への影響や運営コストを最小限に抑えるため、高い季節エネルギー効率比(SEER)や省エネ機能を備えた機器を優先的に採用しています。

大きな市場シェアを占める米国

- 米国は、政府の規制、ヒートポンプ導入へのインセンティブ、CO2や温室効果ガスの排出を回避するための重要な取り組みにより、年間成長率が大きく伸びると予想されています。例えば、2023年11月、電気ヒートポンプの採用を強化し、化石燃料への依存を減らすためのバイデン政権の最近のイニシアチブには、米国エネルギー省による1億6,900万米ドルの多額の投資が含まれています。この資金は、ヒートポンプ製造施設の拡張と、コンプレッサーや冷媒のような重要部品の生産を促進します。政府機関によるこのような投資の増加は、ヒートポンプ需要を促進すると予想されます。

- IEAの報告書によると、北米は建物の暖房用に設置されるヒートポンプの能力が最も高いです。米国では、ヒートポンプの販売台数が、ほぼ同じ伸びを続けてきたガス炉の販売台数を2022年に上回りました。ヒートポンプは、1部屋に1台が一般的なアジアでよく使われているものと比べると、大型になる傾向があります。米国では、空気対空気ヒートポンプの販売台数は、同様の成長パターンが何年も続いた後、ガス炉の販売台数を上回り、2022年には約11%の成長を遂げました。

- さらに、米国では新たな病気やがん患者の増加により、患者や手術、病院内の空気を清浄に保つためのヘルスケア施設のHVACシステムの需要が高まっています。米国には2022年に6,120の病院があり、入院患者数は3,370万人を超えています。

- Carrier CorporationやJohnson Controlsなどの主要ベンダーは、病院内の空気を清浄に保つ製品を提供しています。例えば、Carrier Corporationが開発したOptiCleanポータブル負圧空気清浄機は、空気を清浄に保ち、ウイルスによって汚染された空気を除去するのに役立ちます。

- また、ACメーカー各社は、米国で高まるデータセンター用途の消費者需要を満たすため、製品範囲を拡大しています。これは、Metaの21のデータセンターのように、確立されたデータセンターの数が増加しており、アリゾナ州メサを含む7つのデータセンターの建設が進行中であることに対応しています。業界の急成長を考慮し、これらのメーカーはデータセンターから発生する余剰熱を効率的に利用するソリューションの開発に注力しています。

北米のHVAC機器産業の概要

北米の業務用暖房・換気・空調(HVAC)機器市場は断片化されており、複数の企業で構成されています。各社は新製品の投入、事業の拡大、戦略的M&A、提携、協力関係の締結などにより、市場での存在感を高めようと絶えず努力しています。主な企業には、三菱電機ハイドロニクス&ITクーリングシステムズ、キャリア・コーポレーション、ミデアグループ、Rheem Manufacturing Company Inc.、ダイキン工業、ジョンソンコントロールズ、富士通株式会社、LG Corporationなどがあります。

2024年2月:リームは最新のヒートポンプ、エンデバーラインクラシックプラスシリーズユニバーサルヒートポンプ RD17AZを発表しました。ENERGY STAR認証を取得したRheem RD17AZは、2024年、寒冷地でも最も効率的なユニットとして認められました。このヒートポンプは、ほとんどすべてのHVACシステムと互換性があり、最小限の改造でユニバーサル交換品として使用することもできます。

2024年1月:キャリアは、ヴィースマングループからヴィースマン・クライメート・ソリューションズを買収すると発表。この買収により、インテリジェント気候・エネルギーソリューションにおける同社の地位が強化されます。

2023年12月:ダイキンは、ダイキンDX(Direct eXpansion)室外機をエアハンドリングユニットに接続するための新しい膨張弁キットとコントロールボックスを発売しました。冷媒R-32およびR410aに対応し、冷暖房および新鮮空気制御のためのエネルギー効率に優れた低炭素ソリューションを提供します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- COVID-19後遺症およびその他のマクロ経済要因が市場に与える影響

- 業界の魅力度:ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 技術の進化

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- 成長する建設活動

- 老朽化した商業ビルの空調システムとそれを支える政策

- 市場の課題

- 効率的なシステムを導入するための初期コストの高さ

- サプライチェーンの混乱

第6章 市場セグメンテーション

- 設備別

- 空調/換気機器

- シングルスプリット/マルチスプリット(ダクト/ダクトレス)

- VRF

- エアハンドリングユニット

- チラー

- 屋内パッケージ/ルーフトップ

- その他のタイプ

- 暖房機器

- ボイラー/ラジエーター/暖炉およびその他の暖房

- ヒートポンプ

- 空調/換気機器

- エンドユーザー別

- 公共施設

- オフィス

- 小売スペース

- 教育機関

- ヘルスケア

- ホスピタリティ

- その他のエンドユーザー

- 国別

- 米国

- カナダ

第7章 競合情勢

- 企業プロファイル

- Carrier Global Corporation

- Trane Technologies Company LLC

- Daikin Industries Ltd

- Mitsubishi Electric Corporation

- Johnson Controls

- Lennox International Inc.

- Rheem Manufacturing Company

- Midea Group

- Fujitsu Limited

- Samsung Electronics Co. Ltd

- GREE Electric Appliances Inc.

- LG Corporation

第8章 市場展望

The North America Commercial Heating, Ventilation, And Air Conditioning Equipment Market size is estimated at USD 10.86 billion in 2024, and is expected to reach USD 13.92 billion by 2029, growing at a CAGR of 5.10% during the forecast period (2024-2029).

Key Highlights

- The North American HVAC market growth is driven by the increased government support to adopt heat pumps, growing concerns related to global warming, and technological advancement in HVAC equipment. Further, the increased spending on retrofit construction drives the market growth.

- The current global energy crisis implies an urgent need to move to more affordable, reliable, and cleaner ways of heating buildings. Many how commercial buildings around North America, such as retail spaces, office spaces, schools, and universities, still depend on fossil fuels, mainly natural gas, resulting in large amounts of greenhouse gas emissions. Thus, heat pumps are gaining traction as they can efficiently provide heating to commercial spaces and are one the key technologies to make heating more secure and sustainable.

- Governments of the United States and Canada look forward to introducing stringent regulations, thus mandating the incorporation of heat pumps and positively impacting the market. In September 2023, a group of 25 state governors forming the US Climate Alliance and the Biden administration stated that it aims to quadruple the number of heat pumps in the United States homes by 2030 and will reach 20 million from 4.7 million. This is because buildings account for over 30% of global greenhouse gas emissions.

- Due to the colder climatic conditions in North America, there is expected to be an increase in the demand for heating equipment. Climate researchers have theorized that sudden extreme blasts of cold weather in the United States could be fueled by global heating. The Arctic is warming up four times faster than the rest of the planet, leading to changes in the circular pattern of winds known as the polar vortex, which typically concentrates cold air in the polar region.

- Additionally, in 2024, frigid Arctic air from the Northwest Territories is descending into the province of Alberta in Canada, prompting Environment Canada to issue an extreme cold warning. This cold front is also expected to move from the Rockies toward the northern US plains before advancing south, potentially breaking daily cold records in multiple locations.

- The modern HVAC industry is moving towards intelligent technologies due to the integration of AI and Internet of Things (IoT) technology. The modern heat pump differs greatly from the '90s heat pump'. AI-powered heating and cooling technologies can automatically manage indoor, set, and outdoor temperatures. The leading HVAC system providers are incorporating the latest advanced technologies, boosting market growth in the coming years.

- Further, the Russia-Ukrainian war has suspended the global supply chain, directly impacting the sales of HVAC equipment in North America. Also, the US inflation slowed but remained elevated for a year (December 2023-January 2024), according to the US Labor Department data. The annual inflation rate for the United States was 3.1% for the 12 months ending January, compared to the previous rate of 3.4%. The declining inflation rate across the United States and Canada will drive market growth in the coming years.

North America Commercial Heating, Ventilation, and Air Conditioning (HVAC) Equipment Market Trends

Air Conditioning Equipment is Expected to Witness Remarkable Growth During Forecast Period

- In North America, central air conditioning systems are prevalent in commercial buildings. Another popular option is ductless mini-split systems. They provide zoned cooling, allowing you to control the temperature in different areas of the house independently. Central air conditioners use refrigerants to absorb heat from indoor air and transfer it outside, creating a cooler indoor environment. In North America, high-efficiency central air conditioning units with variable-speed compressors are increasingly favored for their energy-saving benefits and price temperature control.

- According to AHRI, 5.04 million units of air conditioning equipment were shipped in 2023 in the United States, which is a fall with respect to 2022 levels (6.05 million) but a consistent rise since 2010. Daikin Industries plans to become the top air conditioner system supplier in the US by selling lower-priced air conditioners, announced in 2023. Such growth strategies by key vendors will boost the market growth.

- According to EIA, commercial buildings will grow by 34% based on square footage. Office buildings use more energy for AC compared to other types of buildings. Commercial buildings will account for 25% of the energy consumed for AC in the United States commercial sector in 2050.

- Ductless mini-split systems are gaining popularity due to their flexibility. Ductless mini splits allow for individualized temperature control in different zones or rooms without ductwork, making them ideal for retrofitting existing buildings or adding cooling capacity to specific areas.

- Also, energy standards and regulations, such as those set by the US Department of Energy (DOE) and Energy Star, drive the adoption of energy-efficient air conditioning equipment in commercial buildings. Building owners and operators prioritize equipment with high seasonal energy efficiency ratios (SEER) and energy-saving features to minimize environmental impact and operating costs.

The United States to Hold Significant Market Share

- The United States is expected to grow with a significant annual growth rate due to government regulations, incentives for heat pump adoption, and significant efforts to avoid CO2 and greenhouse gas emissions. For instance, in November 2023, the Biden administration's recent initiative to enhance the adoption of electric heat pumps and decrease the dependency on fossil fuels involved a substantial investment of USD 169 million by the US Department of Energy. This funding will facilitate the expansion of heat pump manufacturing facilities and the production of crucial components like compressors and refrigerants. Such increasing investments by government agencies are expected to drive the heat pump demand.

- Based on the IEA report, North America has the highest capacity for heat pumps installed for heating buildings. In the United States, heat pump sales surpassed gas furnace sales in 2022, following a period of nearly identical growth. These units tend to be larger compared to those commonly used in Asia, where it is more common to have one unit per room. In the United States, sales of air-to-air heat pumps experienced an approximately 11% growth in 2022, surpassing gas furnace sales after years of similar growth patterns.

- Further, new diseases and increasing cancer cases in the United States create demand for HVAC systems in healthcare facilities to maintain clean air inside the patient, operation, and hospital areas. There were 6,120 hospitals in the United States in 2022, with over 33.7 million hospital admissions.

- Key vendors such as Carrier Corporation and Johnson Controls offer products to keep indoor air clean and pure in hospitals. For example, the OptiClean portable negative air machine developed by the Carrier Corporation helps to keep the air clean and remove air contaminated by the virus.

- Also, AC manufacturers are expanding their product range to fulfill the growing consumer demand for data center applications in the United States. This is in response to the growing number of established data centers, such as Meta's 21 data centers, and the ongoing construction of seven more, including one in Mesa, Arizona. Considering the industry's rapid growth, these manufacturers are focusing on developing solutions to utilize the excess heat generated by these data centers efficiently.

North America HVAC Equipment Industry Overview

The North American commercial heating, ventilation, and air conditioning (HVAC) equipment market is fragmented and consists of several players. Companies continuously try to increase their market presence by introducing new products, expanding their operations, or entering into strategic mergers and acquisitions, partnerships, and collaborations. Some of the major players include Mitsubishi Electric Hydronics & IT Cooling Systems, Carrier Corporation, Midea Group, Rheem Manufacturing Company Inc., Daikin Industries Ltd, Johnson Controls, Fujitsu Limited, and LG Corporation.

February 2024: Rheem introduced its latest heat pump, the Endeavor Line Classic Plus Series Universal Heat Pump RD17AZ. The Rheem RD17AZ, which is ENERGY STAR certified, has been recognized as the most efficient unit for 2024, even in cold weather conditions. This heat pump is compatible with almost any HVAC system or can be used as a Universal Replacement with minimal modifications.

January 2024: Carrier announced acquiring Viessmann Climate Solutions from the Viessmann Group. This acquisition will strengthen its position in intelligent climate and energy solutions.

December 2023: Daikin launched new expansion valve kits and a control box to connect Daikin DX (Direct eXpansion) outdoor units with air handling units. Operating with refrigerant R-32 and R410a, these kits offer an energy-efficient and low-carbon solution for heating, cooling, and fresh air control to ensure optimal comfort in any commercial space.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Technology Evolution

- 4.5 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Construction Activities

- 5.1.2 Aging Commercial Building with Obsolete HVAC Systems and Supporting Policies

- 5.2 Market Challenges

- 5.2.1 High Initial Cost of Installation for Efficient Systems

- 5.2.2 Supply Chain Disruptions

6 MARKET SEGMENTATION

- 6.1 By Equipment

- 6.1.1 Air Conditioning/Ventilation Equipment

- 6.1.1.1 Single Splits/Multi-Splits (Ducted and Ductless)

- 6.1.1.2 VRF

- 6.1.1.3 Air Handling Units

- 6.1.1.4 Chillers

- 6.1.1.5 Indoor Packaged/Roof Tops

- 6.1.1.6 Other Types

- 6.1.2 Heating Equipment

- 6.1.2.1 Boilers/Radiators/Furnaces and Other Heaters

- 6.1.2.2 Heat Pumps

- 6.1.1 Air Conditioning/Ventilation Equipment

- 6.2 By End User

- 6.2.1 Public Utilities

- 6.2.2 Office Spaces

- 6.2.3 Retail Spaces

- 6.2.4 Education

- 6.2.5 Healthcare

- 6.2.6 Hospitality

- 6.2.7 Other End Users

- 6.3 By Country

- 6.3.1 United States

- 6.3.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Carrier Global Corporation

- 7.1.2 Trane Technologies Company LLC

- 7.1.3 Daikin Industries Ltd

- 7.1.4 Mitsubishi Electric Corporation

- 7.1.5 Johnson Controls

- 7.1.6 Lennox International Inc.

- 7.1.7 Rheem Manufacturing Company

- 7.1.8 Midea Group

- 7.1.9 Fujitsu Limited

- 7.1.10 Samsung Electronics Co. Ltd

- 7.1.11 GREE Electric Appliances Inc.

- 7.1.12 LG Corporation