北米のデータセンター建設:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

North America Data Center Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)- 発行日

- ページ情報

- 英文 181 Pages

- 納期

- 2~3営業日

- 商品コード

- 2044274

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

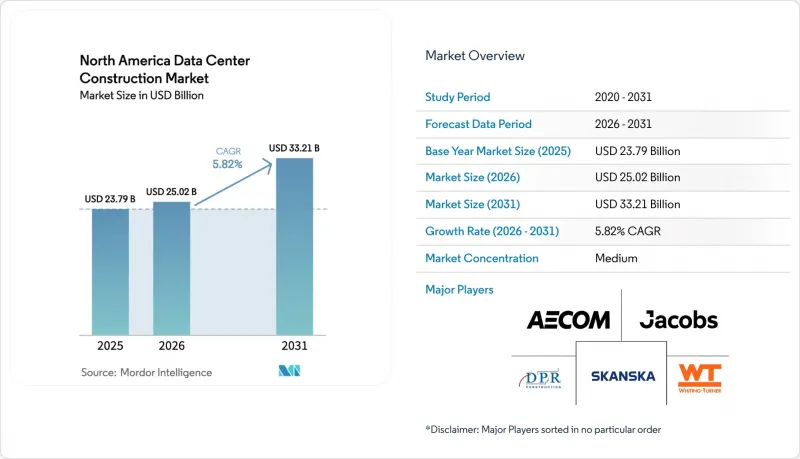

北米のデータセンター建設市場規模は、2025年に237億9,000万米ドル、2026年に250億2,000万米ドルとなり、2031年までに332億1,000万米ドルに達すると予測されており、2026年から2031年にかけてCAGR5.82%で成長すると見込まれています。

クラウドおよび生成AIのワークロードの増加により、100kW以上のラック密度に対応可能なハイパースケール対応キャンパスへの投資が促進されています。一方、風力や太陽光資源への近接性は、ライフサイクルにおける電力コストを低減し、ネットゼロの公約とも合致します。現在2年に及ぶトランスフォーマーのリードタイムにより、早期調達戦略が促されており、建設業者は熟練労働者の不足を補うため、プレハブ式の電気・冷却モジュールに目を向けています。競争上の優位性は、特に待機期間がすでに18ヶ月を超えているバージニア州、テキサス州、アリゾナ州において、系統連系待ちリストに先んじて送電網へのアクセスを確保できるかどうかにかかっています。持続可能性に関する規制要件も立地選定をさらに変容させており、既存の送電線と即座に締結可能な再生可能エネルギー電力購入契約(PPA)を組み合わせることができるため、廃止された石炭火力発電所の跡地が好まれるようになっています。

北米データセンター建設市場の動向と洞察

クラウドアプリケーション、AI、ビッグデータの普及拡大

1万6,000台以上のNvidia H100 GPUを搭載したトレーニングクラスターは、現在1ラックあたり20~100kWの電力を消費しており、従来の企業用データセンターで見られた5~10kWを大幅に上回っています。マイクロソフトの1,000億米ドル規模の「スターゲート」プロジェクトは、敷地内に変電所を備え、チップレベルでサーバー熱の80%を除去する液体冷却システムを備えた専用キャンパスへの移行を浮き彫りにしています。コロケーション施設のオーナーは高密度化に向けた改修を進めていますが、多くのTier 3シェル(未完成のデータセンター施設)では追加の床荷重に対応できず、電力供給が豊富な地域での新規建設が促進されています。AI中心の成長は設計基準も変え、冗長化された中電圧電源供給や800V DCバックボーンを優先するようになっています。その結果、建設費が構造的に増加し、北米のデータセンター建設市場は今後数年にわたり拡大を続ける見通しです。

ハイパースケールデータセンターの展開拡大

コンパス・データセンターズ、センタースクエア、パワーハウスは、2026年までに計4.8GW以上の計画容量を発表しました。これらは、土地の購入から試運転までの全工程において自給自足を確保する、数ギガワット規模のキャンパスに賭けたものです。これらの事業者は、米国エネルギー省が指摘したサプライチェーンのボトルネックを回避するため、大型変圧器を2年前に前倒しで発注しています。用地整備、MEP(機械・電気・配管)工事、設備設置を単一契約で統合するプロジェクトデリバリー方式により、工期を最大12ヶ月短縮しています。また、ハイパースケーラーの進出は、光ファイバー事業者や再生可能エネルギー開発業者を同じ地域に呼び込み、長期的な需要を強化する地域エコシステムを活性化させています。このような資本集約的な性質こそが、北米のデータセンター建設市場の主要な推進力となっています。

高騰する電力・不動産コスト

ラウドン郡の優良地は2025年に1エーカーあたり100万米ドルを突破し、ERCOTの卸電力価格は平均8.2セント/kWhとなり、前年比34%上昇しました。PJMの系統連系待ちリストは現在200GWを超え、開発業者は送電網への接続までに最大36ヶ月待たされる事態となっています。保有コストの上昇により、2024年以前に締結された固定価格リース契約に縛られたコロケーション事業の利益率が圧迫されています。多くの建設業者はセカンダリー市場へとシフトしていますが、これらの地域では光ファイバー回線の密度が低いことが多く、土地や電力コストの節約分を相殺してしまいます。こうした短期的な逼迫状況が、本来堅調な北米データセンター建設市場の成長見通しを鈍らせています。

セグメント分析

金融サービスやクラウド大手が99.995%の可用性を求める中、Tier 4は予測期間中にCAGR 6.42%で成長すると見込まれています。一方、Tier 3は2025年においても北米データセンター建設市場シェアの41.64%を占め、ECやSaaSテナント向けに稼働時間と予算のバランスを保つことで依然として主導的な地位を維持しています。リチウムイオンUPSモジュールは設置面積を40%削減し、ティア3の事業者が1平方フィートあたりの収益ラック数を増やすことを可能にしています。一方、ティア4プロジェクトでは、ロータリー式UPSや二重電源供給を採用しており、これらは土地要件を増加させるもの、ティア3とのコスト差を縮小させます。より高いティアへの移行は、プロジェクトの平均価値を高める技術的な複雑さを伴い、請負業者が参入できる北米データセンター建設市場の規模を拡大させます。

予測期間を通じて、銀行および医療分野のコンプライアンス規制により、Tier 4の成長率は市場全体のCAGRを上回り続ける一方、レイテンシーに敏感なサービス向けにはエッジ指向のTier 1~2サイトが引き続き存在します。進行中の構成変化により、発電機、ATS(自動転送スイッチ)、開閉装置のベンダーは、複数の冗長化スキームに対応した製品ラインの拡充を迫られています。その結果、北米のデータセンター建設業界は、フォールトトレラントな新規建設からモジュラー式のTier 2エッジポッドに至るまで、サービススタックの多様化を図る態勢にあります。

2025年には、10~50MW規模の大型施設が54.43%のシェアを占めましたが、100MWを超えるサイトはCAGR 6.76%で拡大しています。単一のハイパースケール・キャンパスは200エーカーの面積を占有し、郡のゾーニングパターンを変え、変圧器の供給を3年間確保する必要がある独立した変電所を必要とします。こうしたメガプロジェクトを対象とした北米のデータセンター建設市場規模は、従来の企業予算をはるかに上回り、世界のEPCコンソーシアムを惹きつけています。しかし、特に都市部の不動産事情により拡張が制限される地域においては、5Gエッジや災害復旧の役割を担う小規模(5MW未満)な施設の建設が依然として不可欠です。

ハイパースケールの成長に伴い、事業者がディーゼル代替案を模索する中で、溶融塩や水素対応のバックアップシステムが注目を集めています。同時に、モジュール型サプライヤーは、10MWまで積み重ね可能な2MWブロックを標準化しており、これにより中規模の参入企業も広大な土地を購入することなく競争できるようになっています。この二極化した需要パターンにより、北米のデータセンター建設市場全体でバランスの取れたビジネスチャンスが確保されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- マクロ経済要因が市場に与える影響

- 市場促進要因

- クラウドアプリケーションの拡大、AIおよびビッグデータの導入

- ハイパースケール・データセンターの展開拡大

- 5Gハブ周辺におけるエッジコンピューティングの需要

- 企業のサステナビリティとネットゼロ義務

- 廃止された石炭火力発電所跡地の余剰送電容量

- 米国湾岸地域の港湾周辺におけるAI専用GPUのサプライチェーン集積

- 市場抑制要因

- 電力コストおよび不動産コストの高騰

- 熟練した電気・機械技術者の不足

- 大型電力変圧器の複数年にわたるリードタイム

- 乾燥地域における高水使用量冷却システムに対する地域社会の反対

- 業界のサプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 主要なデータセンター統計

- 北米のデータセンター事業者一覧(MW単位)

- 北米における主要な今後のデータセンタープロジェクト一覧

- 北米データセンター建設におけるCAPEXおよびOPEX

- 北米におけるデータセンター電力容量の吸収量(MW単位)、2023年および2024年

- 北米におけるデータセンター建設への人工知能(AI)の導入

- 規制およびコンプライアンスの枠組み

- マクロ経済要因が市場に与える影響

第5章 市場規模と成長予測

- ティアタイプ別

- ティア1および2

- Tier 3

- Tier 4

- データセンター規模別

- スモール

- 中

- 大規模

- ハイパースケール

- データセンターの種類別

- コロケーションデータセンター

- ハイパースケーラー/クラウドサービスプロバイダー(CSP)

- エンタープライズおよびエッジデータセンター

- インフラストラクチャ別

- 電気インフラ

- 配電ソリューション

- 電源バックアップソリューション

- 機械インフラ

- 冷却システム

- ラックおよびキャビネット

- サーバーおよびストレージ

- その他の機械インフラ

- 一般建設

- サービス- 設計・コンサルティング、統合、サポートおよび保守

- 電気インフラ

- 国別

- 米国

- カナダ

- メキシコ

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- Data Center Infrastructure Investment Based on Megawatt(MW)Capacity, 2024 vs 2030

- Data Center Construction Landscape(Key Vendors Listings)

- 企業プロファイル

- AECOM

- Whiting-Turner Contracting Company

- Turner Construction Company

- Jacobs Solutions Inc.

- DPR Construction Inc.

- Skanska USA

- Balfour Beatty US

- Hensel Phelps

- McCarthy Building Companies Inc.

- Gilbane Building Company

- Brasfield and Gorrie LLC

- Holder Construction

- Mortenson Construction

- Fluor Corporation

- Clark Construction Group

- Walsh Construction

- JE Dunn Construction

- Webcor Builders

- Kiewit Corporation

- Layton Construction

- Compass Datacenters

- STACK Infrastructure

- Digital Realty

- Equinix Inc.

- CyrusOne Inc.

- List of Data Center Construction Companies

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 181 Pages

- 納期

- 2~3営業日