|

市場調査レポート

商品コード

1643017

ワイヤレスコネクティビティ:市場シェア分析、産業動向と統計、成長予測(2025~2030年)Wireless Connectivity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ワイヤレスコネクティビティ:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

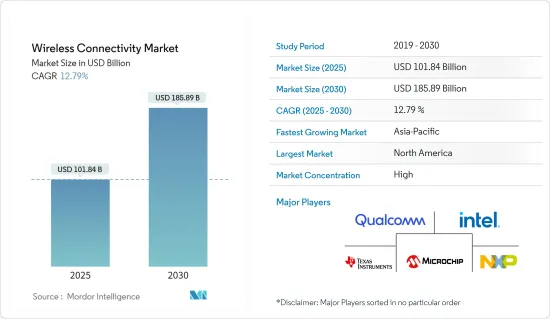

ワイヤレスコネクティビティの市場規模は2025年に1,018億4,000万米ドルと推定され、2030年には1,858億9,000万米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは12.79%です。

主なハイライト

- ワイヤレスコネクティビティ市場は、シームレスなインターネットアクセスや、Wi-Fi、Bluetooth、Zigbeeなど、ケーブルを必要としないデータ伝送を可能にする様々な技術を包含する相互接続機器への需要の高まりにより、大きな成長を遂げています。

- ヘルスケアやスマートホームなど様々な分野でのコネクテッドデバイスの普及は、BluetoothやZigbeeなどの低消費電力、短距離接続ソリューションの需要を促進しています。例えば、アマゾンのスマートスピーカー「エコー」は、Wi-FiとBluetooth技術を活用して接続性を高めています。さらに、スマートサーモスタット、照明、セキュリティシステムなどのスマートホームデバイスに対する消費者の関心の高まりが、ワイヤレスコネクティビティの需要を押し上げています。

- 民生用電子機器に対する需要の高まりが、市場の成長を後押ししています。AI、IoT、AR、VRのような先進技術の採用も、さまざまな産業分野でワイヤレスコネクティビティの需要を加速しています。スマートインフラの世界の開発も、ワイヤレスコネクティビティの需要増加の大きな要因となっています。

- さらに、さまざまなアプリケーションにワイヤレスコネクティビティを使用するスマートシティプロジェクトへの政府による投資が世界的に増加していることも、市場の成長を後押ししています。例えば、2023年10月、情報技術・電子通信省(DITE&C)は、無料でシームレスなインターネットサービスを提供するため、州内に100カ所以上のWi-Fiホットスポットを設置し、運用する計画を発表しました。ホットスポットは、政府機関、バススタンド、公共公園、市民サービスセンターなど、人通りの多い場所に設置される予定です。

- しかし、無線ネットワークはサイバー攻撃に弱いため、セキュリティ上の懸念がワイヤレスコネクティビティ市場の成長を抑制しています。ワイヤレス通信が業界や用途を問わず成長を続ける中、データ漏洩やマルウェア攻撃を防ぐには強力なセキュリティ対策が不可欠です。不十分な暗号化プロトコル、脆弱な認証メカニズム、脆弱なネットワーク構成は、機密情報を漏えいさせ、無線システムのセキュリティを損なう可能性があります。

- 例えば、WBA(ワイヤレス・ブロードバンド・アライアンス)がWBA Annual Industry Report 2023の一環として行った調査によると、サービス・プロバイダー、テクノロジー・ベンダー、企業の3分の1以上(33%)が、2023年末までにWi-Fi 7の導入をすでに計画しています。さらに、44%が今後12~18ヵ月以内にWi-Fi 6Eの導入を計画しています。このようなWi-Fi採用の成長見通しは、ワイヤレスコネクティビティ市場に大きな成長をもたらすと予想されます。

ワイヤレスコネクティビティ市場の動向

自動車産業が市場成長を牽引する見込み

- Bluetoothワイヤレスコネクティビティは、ハンズフリー通話、オーディオストリーミング、車載インフォテインメントシステムなど、ワイヤレス通信や接続を可能にするために、さまざまな自動車システム機器への採用が進んでいます。wi-fiやBluetoothのようなワイヤレスコネクティビティを使用することで、ユーザーはスマートフォンやその他のスマートデバイスをインフォテインメントシステムに接続することができます。そのため、自動車販売台数の伸びは、ワイヤレスコネクティビティソリューションの需要を促進すると思われます。

- 現代の自動車はますますモバイルIoT(モノのインターネット)デバイスに似てきており、ドライバーの安全性と快適性を高めるために、内部および外部の情報を収集し、それに対応することで、さまざまなセンサーを使用するようになってきています。ワイヤレス通信が自動車技術の進歩に不可欠な役割を果たす中、ADAS(先進運転支援システム)や車載インフォテインメントなどのアプリケーションによって生成されるデータ量の増加が、BluetoothやWi-Fi、セルラーなどのワイヤレス技術の革新を促し、市場に成長をもたらしています。

- 自律走行車とコネクテッドカーは消費者の間で人気が高まっており、今後も成長が続くと予想されます。展示されている先進運転支援システム(ADAS)は、現在の自動車と将来の自動車のギャップを埋めることを目的としています。また、自動車業界の技術革新が進むにつれて、最終消費者は運転体験を向上させ、ドライバーと同乗者の安全性を高める最新技術により多くの資金を投じようとしています。これにより、自律走行車向けのワイヤレスコネクティビティソリューションの需要が高まると思われます。

- さらに、中東GMはグーグル内蔵の新しい車載技術を発表し、コネクティビティのリーダーシップを強化し、顧客体験を向上させました。中東ゼネラルモーターズは、車両インテリジェンス技術目標の一環として、グーグルを組み込んだインフォテインメント・システムの導入を発表しました。これらの新機能は、全体的な顧客体験を強化し、顧客が将来のコネクテッドカーにデジタルライフを持ち込むことを容易にします。

- グーグル内蔵サービスは、LT以上のトリムに標準装備され、オンスター・モジュール・システムを搭載するGMの全車種ブランドに広く展開されます。このため、クウェートとアラブ首長国連邦の顧客はWi-Fiプランを通じてGoogleビルトイン・サービスを利用でき、一方、クウェートとバーレーンの顧客は個人のモバイルWi-Fiホットスポットを通じて接続できます。

アジア太平洋地域は高い成長率を記録する見込み

- 同地域の市場拡大は、主に消費者の支出増とスマートホームの導入拡大によってもたらされます。ソフトウェア会社のUtimacoが2023年4月に実施したデジタル調査によると、シンガポールではスマートホームデバイスの利用が大幅に増加しており、回答者の61%がスマートテレビ、43%が家電製品、33%が省エネデバイス、バーチャルアシスタント、掃除機ロボットを利用していると回答しています。これが、この地域でワイヤレスコネクティビティソリューションの採用が増加している主な成長要因となっています。

- スマートシティに向けた動向の高まりは、同地域のスマートシティ開発を容易にする新製品やソリューションの開発を企業や機関に促しています。例えば、2023年10月、リビングラボIIITハイデラバード・スマートシティは、セキュアでインテリジェントな無線技術のリーダーであるシリコン・ラボと共同で、モノのインターネット(IoT)とスマートシティのための研究とソリューションをサポートするキャンパス全体のWi-SUNネットワークの導入を発表しました。このような開発により、地域全体でワイヤレスコネクティビティに対する需要が加速しています。

- さらに、同地域における5Gネットワークの拡大は、直接的・間接的に市場の成長を促進する主な要因の1つになると予想されます。GSMAの最新レポートによると、5Gは2030年までに東アジア・太平洋地域の新興経済諸国に約9,600億米ドルの貢献が見込まれています。5Gは、同地域における自動化スマート工場展開の大きな原動力になると予想されます。

- 中国では、モノのインターネット(IoT)プラットフォームの普及が急速に進んでいます。半導体の生産と製造において中国が主導的な役割を担っていることから、産業用モノのインターネット(lIoT)の進歩と応用への参加と開発が、エンドユーザー産業全体にワイヤレスコネクティビティの需要を生み出すと予想されます。

ワイヤレスコネクティビティ産業の概要

ワイヤレスコネクティビティ市場の競合情勢は細分化されており、Qualcomm Incorporated、Intel Corporation、Texas Instruments Inc、NXP Semiconductors NV、Microchip Technology Inc.など、多数のプレーヤーが市場で競争しています。同市場では、競争優位を獲得するために、製品投入、合併、買収などの戦略的開拓が行われています。

- 2024年2月、世界のIoTソリューションプロバイダーであるQuectel Wireless Solutionsは、2つの新しいWi-Fiモジュール、FCU741RとFCS950R、およびブルートゥースモジュール、HCM010SとHCM111Zを発表しました。このブルートゥースとWi-Fiモジュールの発売により、同社は設計者や開発者に複数の選択肢を提供し、サイズ、コスト、電力効率の面で多様なニーズに対応することを目指しています。

- 2024年1月、スマートエッジデバイスの確実かつ効率的なデータ接続、センス、推論を可能にするシリコンおよびソフトウェアIPのライセンサーであるCeva Inc.と、マルチメディアおよび車載アプリケーション向けチッププロバイダであるSunplus Technologyは、Cevaの最新世代RivieraWaves Bluetoothオーディオソリューションを、ワイヤレススピーカー、サウンドバー、その他のプレミアムワイヤレスオーディオデバイスをターゲットとするSunplus airlyra HDオーディオプロセッサ・ファミリーに統合することで協業を拡大しました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- 堅牢なワイヤレスコネクティビティソリューションに向けたIoTとコネクテッドデバイスの普及

- スマートインフラ構築のための無線センサーネットワーク需要の増加

- 市場の課題

- データプライバシーとセキュリティへの懸念

- インフラ不足、膨大な導入コスト、技術ノウハウの欠如

第6章 市場セグメンテーション

- 技術別

- Wi-Fi

- Bluetooth

- Zigbee

- その他の技術

- エンドユーザー産業別

- 自動車

- 産業

- ヘルスケア

- エネルギー

- インフラ

- その他のエンドユーザー産業

- 地域別

- 北米

- 欧州

- アジア

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Qualcomm Incorporated

- Intel Corporation

- Texas Instruments Inc.

- NXP Semiconductors NV

- Microchip Technology Inc.

- MediaTek Inc.

- Rensas Electronics Corporation

- Broadcom Inc.

- STMicroelectronics

- Nordic Semiconductor

第8章 投資分析

第9章 市場の将来

The Wireless Connectivity Market size is estimated at USD 101.84 billion in 2025, and is expected to reach USD 185.89 billion by 2030, at a CAGR of 12.79% during the forecast period (2025-2030).

Key Highlights

- The wireless connectivity market is experiencing significant growth, driven by the increasing demand for seamless internet access and interconnected devices encompassing various technologies, including Wi-Fi, Bluetooth, and Zigbee, enabling data transmission without requiring cables.

- The proliferation of connected devices across various sectors like healthcare and smart homes drives demand for low-power, short-range connectivity solutions, such as Bluetooth and Zigbee. For instance, Amazon's growing portfolio of Echo smart speakers leverages Wi-Fi and Bluetooth technology for connectivity. In addition, the growing consumer interest in smart home devices, such as smart thermostats, lighting, and security systems, is boosting the demand for wireless connectivity.

- The increasing demand for consumer electronic devices drives the market's growth. Adopting advanced technologies like AI, IoT, AR, and VR is also accelerating demand for wireless connectivity across various industry verticals. The global development of smart infrastructure is also a significant factor in the increasing demand for wireless connectivity.

- Moreover, the increasing investment by governments globally in smart city projects that use wireless connectivity for various applications is propelling the market's growth. For instance, in October 2023, the Department of Information Technology, Electronics & Communication (DITE&C) announced a plan to set up and operationalize more than 100 Wi-Fi hotspots across the state to provide free and seamless internet services. The hotspots will be at selected government offices, bus stands, public parks, citizen service centers, and other locations with high footfalls.

- However, security concerns are restraining the wireless connectivity market's growth as wireless networks are vulnerable to cyberattacks. As wireless communication continues to grow across industries and applications, strong security measures are essential to prevent data breaches and malware attacks. Poor encryption protocols, weak authentication mechanisms, and vulnerable network configurations can reveal sensitive information and compromise the security of wireless systems.

- For instance, according to a survey by the Wireless Broadband Alliance (WBA) as part of the WBA Annual Industry Report 2023, more than a third (33%) of service providers, technology vendors, and enterprises already plan to deploy Wi-Fi 7 by the end of 2023. Further, 44% are planning to adopt Wi-Fi 6E in the next 12-18 months. Such growth prospects in adopting Wi-Fi are anticipated to add significant growth to the wireless connectivity market.

Wireless Connectivity Market Trends

The Automotive Industry is Expected to Drive the Market's Growth

- Bluetooth wireless connectivity is increasingly used in various automotive system equipment to enable wireless communication and connectivity, including hands-free calling, audio streaming, and in-car infotainment systems. By using wireless connectivity like wi-fi and bluetooth, users are able to connect their smartphones and other smart devices to their infotainment systems. Thus, the growth in the sales of automotive vehicles would drive demand for wireless connectivity solutions.

- Modern automobiles increasingly resemble mobile internet of things (IoT) devices and increasingly use a wide range of sensors to enhance driver safety and comfort by collecting and responding to internal and external information. As wireless communications play an essential role in advancing automotive technology, the increasing amount of data produced by applications like advanced driver assistance systems (ADAS) and in-vehicle infotainment is driving innovations in wireless technologies like bluetooth and wi-fi, as well as cellular and adding growth to the market.

- Autonomous vehicles and connected cars are becoming more popular among consumers and are expected to continue to grow over the coming years. The advanced driving assistance systems (ADAS) on display aim to bridge the gap between the cars of today and the cars of tomorrow. In addition, with more technological innovation in the auto industry, end consumers are willing to spend more money on the newest technology that enhances the driving experience and enhances the safety of drivers and passengers. This would drive demand for wireless connectivity solutions for autonomous vehicles.

- Moreover, GM Middle East launched new in-vehicle technology with Google built-in, strengthening connectivity leadership and enhancing the customer experience. General Motors Middle East announced the introduction of infotainment systems with Google built in as part of its vehicle intelligence technology goals. These new features would augment the overall customer experience and make it easier for customers to bring their digital lives into future connected vehicles.

- The Google built-in services would be standard on LT and higher trims, with widespread deployment across all GM vehicle brands equipped with the OnStar module system. Thus, customers in Kuwait and the UAE can utilize Google built-in via their wi-fi plans, while those in KSA and Bahrain can connect through their personal mobile wi-fi hotspots.

Asia-Pacific is Expected to Register High Growth Rate

- The market expansion in the region is primarily driven by consumers' increased spending and the growing adoption of smart homes. According to a digital survey conducted by Utimaco, a software company, in April 2023, the use of smart home devices has significantly increased in Singapore, with 61% of respondents stating that they are using smart TVs, 43% using home appliances, and 33% using energy saving devices, virtual assistants, and vacuum cleaner robots. This becomes a primary growth factor for the region's increasing adoption of wireless connectivity solutions.

- The rise in the trend towards smart cities is pushing firms or institutions to develop new products or solutions to ease the development of smart cities in the region. For instance, in October 2023, the Living Lab IIIT Hyderabad Smart City, in collaboration with Silicon Labs, a leader in secure, intelligent wireless technology, announced the introduction of a campus-wide Wi-SUN network to support research and solutions for the internet of things (IoT) and smart cities. Such developments are accelerating the demand for wireless connectivity across the region.

- Additionally, the expansion of 5G networks in the region is expected to be one of the major factors driving the growth of market, both directly and indirectly. According to the GSMA's latest report, 5G is expected to contribute about USD 960 billion to the developed economies of East Asia and the Pacific by 2030. 5G is expected to be a significant driving force in automated smart factory deployments in the region.

- The widespread use of the internet of things (IoT) platform in China is increasing rapidly. Given China's leading role in the production of semiconductors and manufacturing, its participation in the advancement and application of the industrial internet of things (lIoT) and the development are expected to create demand for wireless connectivity across end-user industries.

Wireless Connectivity Industry Overview

The competitive landscape for the wireless connectivity market is fragmented, with a large number of players competing in the market, including Qualcomm Incorporated, Intel Corporation, Texas Instruments Inc., NXP Semiconductors NV, and Microchip Technology Inc. The market is witnessing strategic developments, such as product launches, mergers, and acquisitions, to gain a competitive edge.

- In February 2024, Quectel Wireless Solutions, a global IoT solutions provider, launched two new wi-fi modules, the FCU741R and the FCS950R, and bluetooth modules, the HCM010S and the HCM111Z. Through this launch of bluetooth and wi-fi modules, the company aims to empower designers and developers with multiple options, catering to diverse needs in terms of size, cost, and power efficiency.

- In January 2024, Ceva Inc., the licensor of silicon and software IP that enables Smart Edge devices to connect, sense, and infer data reliably and efficiently, and Sunplus Technology Co. Ltd, a chip provider for multimedia and automotive applications have expanded their collaboration to integrate Ceva's latest generation RivieraWaves Bluetooth audio solution into the Sunplus airlyra family of HD audio processors targeting wireless speakers, soundbars and other premium wireless audio devices.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Proliferation of IoT and Connected Devices for Robust Wireless Connectivity Solutions

- 5.1.2 Increased Demand for Wireless Sensor Networks to Create Smart Infrastructure

- 5.2 Market Challenges

- 5.2.1 Data Privacy and Security Concerns

- 5.2.2 Lack of Infrastructure, Huge Implementation Cost, and Absence of Technology Know-how

6 MARKET SEGMENTATION

- 6.1 By Technology

- 6.1.1 Wi-Fi

- 6.1.2 Bluetooth

- 6.1.3 Zigbee

- 6.1.4 Other Technologies

- 6.2 By End-user Industry

- 6.2.1 Automotive

- 6.2.2 Industrial

- 6.2.3 Healthcare

- 6.2.4 Energy

- 6.2.5 Infrastructure

- 6.2.6 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Qualcomm Incorporated

- 7.1.2 Intel Corporation

- 7.1.3 Texas Instruments Inc.

- 7.1.4 NXP Semiconductors NV

- 7.1.5 Microchip Technology Inc.

- 7.1.6 MediaTek Inc.

- 7.1.7 Rensas Electronics Corporation

- 7.1.8 Broadcom Inc.

- 7.1.9 STMicroelectronics

- 7.1.10 Nordic Semiconductor