|

|

市場調査レポート

商品コード

1445760

能動・受動電子部品:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Active and Passive Electronic Components - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 能動・受動電子部品:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 219 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

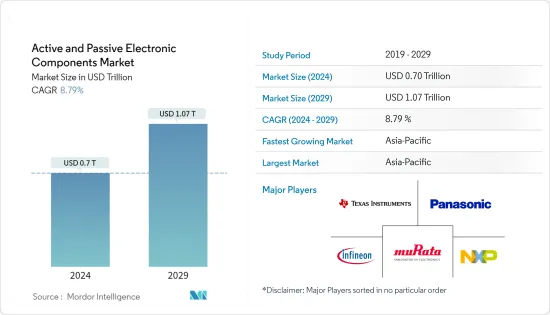

能動・受動電子部品の市場規模は、2024年に7,000億米ドルと推定され、2029年までに1兆700億米ドルに達すると予測されており、予測期間(2024年~2029年)中に8.79%のCAGRで成長する見込みです。

能動・受動電子部品は、あらゆる半導体/電子デバイスの構成要素です。これらの部品はシンプルな機能を備えているため、電子システムに電力を供給する上で重要な役割を果たします。能動部品は外部電源に依存して電気信号を変更/制御する電子回路の一部ですが、受動電子部品は機能するために外部電源を必要としません。それらは他の特性を使用して電気信号を制御します。

主なハイライト

- 能動・受動電子市場は、主にさまざまな分野のデジタル化の進展により、過去数年間で大幅な成長を遂げました。その結果、あらゆる分野でコンシューマーエレクトロニクスの採用が増加し、接続性とモビリティに対するニーズが高まりました。これらの発展に伴い、電子製品の複雑さも増大しました。これにより、特に自動車業界やコンシューマーエレクトロニクス業界で部品の必要性が加速しました。

- コンシューマーエレクトロニクス業界における現在の動向の1つは、より小さく、より軽く、より高性能なエレクトロニクスに対する需要とニーズの増大、つまりエレクトロニクスと部品の小型化です。技術の急速な進歩により、単一のプラットフォームに複数の機能を組み込んだ製品が利用できるようになりました。

- コンシューマーエレクトロニクス業界は、能動・受動電子部品の主要消費者の1つです。これらの部品は、コンピュータ、携帯電話、その他いくつかの電子機器などの機器の回路の基本的な構成要素の1つです。たとえば、トランジスタは、増幅、電圧調整、スイッチング、信号変調、発振器などのさまざまな機能を実行します。

- 最近、シリコン、鉄、ニッケル、モリブデンなどの原材料価格が大きく変動しております。パンデミックの影響により、世界の貴金属市場はサプライチェーンの問題による悪影響をさらに目の当たりにしており、それが市場価格にも影響を与えています。このパラジウム、ニッケル、ルテニウムの価格上昇は、特定の大量生産部品の全体的な生産コストに影響を与え、市場の成長に課題をもたらしています。

- COVID-19のパンデミック中、検出と治療のプロセスを高速化し、遠隔患者監視機能を強化するために、医療およびヘルスケア分野全体で能動・受動部品の需要が大幅に増加しました。ヘルスケア機関は先進的な電子機器に多額の投資を行い、その結果、トランジスタ、コンデンサ、アンプなどの部品の需要が高まりました。

- たとえば、モジュール式アーキテクチャを備えた電気化学トランジスタの需要により、複雑な体液中の特定の抗原を単一分子からナノモルレベルまで迅速に定量するためのセンシングデバイスでの使用が顕著に増加しました。さらに、COVID期間中には、SARS-CoV-2を検出するためのレーザー誘起グラフェン電界効果トランジスタ(LIG-FET)のさまざまな使用例も観察されました。これらの部品が有益であることが判明したことで、さらなる技術革新がCOVID-19後の期間に新たな成長機会を開くことが期待されています。

能動・受動電子部品の市場動向

5Gテクノロジーの採用増加が市場を牽引

- 5Gは通信業界だけでなく画期的なイノベーションであり、5Gが提供する高速かつ低遅延の接続によりこれらの業界全体でのユースケースが大幅に拡大するため、コンシューマーエレクトロニクス、自動車、産業などを含むさまざまな業界の成長に大きな影響を与えると予想されています。

- Ericssonによれば、世界の5G加入者数は急速に拡大し、2019年のわずか1,269万人から2027年までに43億7,273万人にまで増加すると予想されています。さらに、北東アジアは5G加入者数が最も多く、2027年までに17億560万加入者に達すると予想されています。

- 5Gが提供する低遅延と高速速度は、インテリジェントオートメーション、人工知能(AI)、モノのインターネット(IoT)のさらなる進歩に必要なものであるため、このような動向はあらゆるテクノロジー業界に新たな可能性の世界を開くことが期待されています。自動運転車、拡張現実、ブロックチェーン、およびその他のいくつかのテクノロジーはまだ検討されていません。

- Qualcommの調査によると、5Gは2035年までに自動車業界全体で2兆4,000億米ドル以上の収益を生み出すと予想されています。数百万台の車両がリアルタイムナビゲーション、緊急サービス、コネクテッドインフォテインメントなどにモバイルテクノロジーを活用しているため、5Gの出現が生まれると予想されています。Vehicle-2-Vehicle、Vehicle-2-Network(V2N)、Vehicle-2-Infrastructor(V2I)、およびVehicle-2-Pedestrian(V2P)通信などの新しい範囲のアプリケーションです。

- さらに、5Gはコンシューマーエレクトロニクス業界の成長にも同様の影響を与えると予想されています。低遅延で高速な接続ネットワークが利用できるようになったことで、IoTに接続された消費者向けデバイスの需要が増加すると考えられます。このような動向は総合的に、予測期間中の調査対象市場の成長をサポートします。

アジア太平洋は大幅な成長が見込まれる

- エレクトロニクス産業の成長により、複数の多国籍企業が独立して、またはさまざまな地域企業との合弁事業を通じてアジア諸国に製造工場を設立するよう誘致されています。これには、Tyco Electronics、FCI OEN、Molex、Vishay、EPCOSなどの大規模な世界的組織が含まれます。これにより、アジア太平洋における抵抗器の現地製造活動がさらに促進されることが予想されます。

- 中国では、調査対象市場の成長はエレクトロニクス産業の急成長によるものとも考えられます。エレクトロニクスは中国最大の産業の1つであり、中国全体の経済成長に大きく貢献しています。例えば、中華人民共和国国務院によると、2022年1月から2月までの2か月間で、大手電機メーカーの付加価値は前年比12.7%増加したのに対し、この国の産業部門全体では7.5%の成長が見られました。中国は、テレビ、スマートフォン、ラップトップ、PC、冷蔵庫、エアコンなどの電子機器の世界有数の生産国です。

- 世界最大規模の日本の電子製品産業は、同国の半導体販売需要を牽引する最も重要な要因となっています。電子情報技術産業協会(JEITA)によると、2021年の日本の電子機器生産額は前年比10.6%増の約3兆9,400億円となりました。可処分所得の増加人々のスマートホームやスマートビジネス環境に対する人々の好みは、日本のコンシューマーエレクトロニクスの成長にとって重要な原動力です。

- 韓国は世界の半導体メモリ市場で重要な地位を獲得しました。韓国のデータセンター市場は最も急速に成長している市場の一つであり、多くの外国企業からの投資が増加しています。たとえば、2022年4月には、Digital Edge(Singapore)Holdings Pte. Ltdは、SK eco plantとの提携を通じて、韓国の仁川にデータセンターを開発することを計画していました。両社は共同で仁川市富平区の国立産業団地内に120MWの超大規模データセンター開発プロジェクトを建設、推進します。

- 電子機器製造は台湾の国内総生産(GDP)に大きく貢献しています。Taiwan Semiconductor Manufacturing Company(TSMC)は、この地域で最も重要な半導体メーカーです。最近、TSMCは2022年第2四半期の決算を報告し、前年比36.6%という大幅な収益成長を示しました。同社によれば、この目覚ましい成長の最も重要な理由の1つは、ハイパフォーマンスコンピューティング(HPC)業界における顧客の急速な拡大でした。これらには、人工知能の研究者、AmazonのAmazon Web Servicesなどのクラウドプロバイダーのデータセンター、エッジコンピューティングネットワークが含まれます。HPCの収益は第2四半期に前四半期比14%増加し、現在TSMCの収益全体の43%を占めています。

能動・受動電子部品業界の概要

能動・受動電子部品市場は、製品に多大な投資を行ってきた長年確立されたプレーヤーで構成されています。市場に新規参入する企業には多額の投資が必要です。企業は強力な競争戦略を通じて自らを維持することができます。製品イノベーションは、新興企業やあまり開拓されていないアプリケーション分野をターゲットにして市場での存在感をさらに拡大できるため、新規プレーヤーに有利に働く可能性もあります。市場における競合の度合いは高く、予測期間中も同様の状況が続くと予想されます。

2022年12月、非常に高いスイッチング周波数で動作できるDCリンクアプリケーション向けに設計されたモジュラーコンデンサであるModCap HFがTDK Corporationから提供されました。B25647A*シリーズの6つの新しく作成されたパワーコンデンサの定格は900ボルトから1600ボルトで、静電容量範囲は640マイクロファラッドから1850マイクロファラッドです。ホットスポットの最高許容温度は90°C、定格電流は種類に応じて160Aから210Aです。

2022年10月、受動部品の世界トップサプライヤーであるYAGEO Groupは、車載グレードの薄膜チップ抵抗器-RPシリーズをリリースしました。RPシリーズの独自のパッシベーション設計により、防水インターフェースが実現されます。このカバーは抵抗層をシールドし、外部からの湿気の侵入を防ぎます。この防御機能により、RPシリーズは困難な条件下でも高い抵抗安定性を維持できるため、電力システム、産業/医療機器、通信、産業/自動車エレクトロニクス、産業/産業用機器に最適です。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界のバリューチェーン分析

- 業界の魅力 - ポーターのファイブフォース

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係の激しさ

- 代替品の脅威

- COVID-19の業界への影響

第5章 市場力学

- 市場促進要因

- 小型化設計への関心の高まり

- コンピューティング、通信、コンシューマーエレクトロニクスの数の増加

- 5Gテクノロジーの導入拡大

- 市場抑制要因

- 金属価格の上昇が部品の生産コストに影響

第6章 市場セグメンテーション

- 部品別

- 能動部品

- トランジスタ

- ダイオード

- 集積回路(IC)

- アンプ

- 真空管

- 受動部品

- コンデンサ

- インダクタ

- 抵抗器

- 能動部品

- エンドユーザー業界別

- 自動車

- コンシューマーエレクトロニクスとコンピューティング

- 医療

- 産業用

- コミュニケーション

- その他のエンドユーザー業界

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Infineon Technologies AG

- NXP Semiconductors NV

- Texas Instruments, Inc.

- Panasonic Corporation

- Murata Manufacturing Co. Ltd

- Eaton Corporation

- TE Connectivity Ltd.

- Honeywell International Inc.

- Toshiba Corp.

- Vishay Intertechnology Inc.

- YAGEO Corporation

- TDK Corporation

- KEMET Corporation(Yageo Corporation)

- AVX Corporation(Kyocera Corp)

- Lelon Electronics Corporation

- Taiyo Yuden Co. Ltd

第8章 投資分析

第9章 市場の将来

The Active and Passive Electronic Components Market size is estimated at USD 0.7 trillion in 2024, and is expected to reach USD 1.07 trillion by 2029, growing at a CAGR of 8.79% during the forecast period (2024-2029).

Active and passive electronic components are any semiconductor/electronic device's building blocks. With their simple functionalities, these components play a crucial role in powering an electronic system. While active components are part of an electronic circuit that relies on an external power source to modify/control electrical signals, passive electronic components do not need an external power source to function. They use other properties to control the electrical signal.

Key Highlights

- The active and passive electronics market witnessed significant growth over the past few years, primarily due to the increasing digitalization of various sectors. This resulted in the growing adoption of consumer electronics across sectors and the rising need for connectivity and mobility. With these developments, the complexity of electronic products also increased. This accelerated the need for components, especially in the automotive and consumer electronics industries.

- One of the current trends in the consumer electronics industry is the growing demand and need for smaller, lighter, and higher-performing electronics, i.e., the miniaturization of electronics and components. Rapid technological advances have led to the availability of products that incorporate multiple features on a single platform.

- The consumer electronics industry is among the major consumer of active and passive electronic components. These components are among the fundamental building blocks of the circuitry in devices such as computers, cell phones, and several other electronic devices. For instance, a transistor performs various functions such as amplification, voltage regulation, switching, signal modulation, and oscillators.

- The raw materials prices, such as silicon, iron, nickel, and molybdenum, have recently seen significant changes. With the pandemic's influence, the global precious metal market is further witnessing adverse effects of supply chain issues, which also impact the market prices. This increase in the price of palladium, nickel, and ruthenium impacts the overall cost of production for specific large-volume components, challenging the market's growth.

- During the COVID-19 pandemic, the demand for active and passive components increased significantly across the medical and healthcare sector to speed up the detection and treatment process as well as to enhance remote patient monitoring capabilities; healthcare institutions significantly invested in advanced electronic devices, which in turn drove the demand for components such as transistors, capacitors, amplifiers, etc.

- For instance, the demand for electrochemical transistors with a modular architecture witnessed a notable increase in use in sensing devices for the rapid quantification of single-molecule-to-nanomolar levels of specific antigens in complex bodily fluids. Furthermore, various use cases of laser-induced graphene field-effect transistors (LIG-FET) for detecting SARS-CoV-2 were also observed during the COVID period. With these components proving beneficial, further technological innovations are expected to open new growth opportunities in the post-COVID-19 period.

Active & Passive Electronic Components Market Trends

Increasing Adoption of 5G Technology is Driving the Market

- 5G has been a groundbreaking innovation not just for the communication industry but is expected to significantly impact the growth of various industries, including consumer electronics, automotive, industrial, etc., as the fast and low latency connectivity offered by 5G will significantly expand use cases across these industries.

- According to Ericsson, the global number 5G subscriptions are expected to expand rapidly, growing up from a mere 12.69 million in 2019 to 4,372.73 million by 2027. Furthermore, Northeast Asia is expected to hold the largest number of 5G subscribers, reaching 1,705.6 million subscribers by 2027.

- Such trends are expected to open up a new world of possibilities for every tech industry as the low-latency and fast speed offered by 5G is what is needed for further advances in intelligent automation, Artificial Intelligence (AI), the Internet of Things (IoT), autonomous cars, extended reality, blockchain, and several other technologies yet to be explored.

- According to a study by Qualcomm, 5G will generate more than USD 2.4 trillion across the automotive industry by 2035. As millions of vehicles leverage mobile technology for real-time navigation, emergency services, connected infotainment, etc., the advent of 5G will spawn a new range of applications such as Vehicle-2-Vehicle, Vehicle-2-Network (V2N), Vehicle-2-Infrastructure (V2I), and Vehicle-2-Pedestrian (V2P) communications.

- Furthermore, 5G is also expected to have a similar impact on the growth of the consumer electronics industry. The demand for IoT-connected consumer devices will grow due to the availability of low latency and fast connectivity networks. Such trends combinedly will support the growth of the studied market during the forecast period.

Asia Pacific is Expected to Witness Significant Growth

- The growing electronics industry is attracting several MNCs to set up manufacturing plants in Asian countries either independently or through a joint venture with different regional companies. This includes large global organizations such as Tyco Electronics, FCI OEN, Molex, Vishay, and EPCOS. This is further anticipated to boost the local manufacturing activity of resistors in the Asia Pacific region.

- In China, the growth of the studied market can also be attributed to the booming electronics industry. Electronics is one of the largest industries in China and is a significant contributor to the country's overall economic growth. For instance, as per the State Council of the People's Republic of China, during the two months from January to February 2022, the added value of major electronics manufacturers rose 12.7% year-on-year, compared with the 7.5% growth seen in the overall industrial sector in the country. China is the world's leading producer of electronic devices such as TVs, smartphones, laptops and PCs, refrigerators, and air conditioners.

- Japan's electronic products industry, which is one of the largest in the world, is the most significant factor driving demand for sales of semiconductors in the country. As per the Japan Electronics and Information Technology Industries Association (JEITA), in 2021, the production value of electronic devices in Japan grew by 10.6% compared to the previous year, reaching a value of about JPY 3.94 trillion in 2021. The rising disposable income of the people and their preferences for smart homes and smart business environments are important drivers for the growth of consumer electronics in Japan.

- Korea acquired a prominent position in the global semiconductor memory market. The data center market in Korea is one of the fastest growing and is attracting increasing investments from many foreign players. For instance, in April 2022, Digital Edge (Singapore) Holdings Pte. Ltd planned to develop a data center in Incheon, South Korea, through a partnership with the SK eco plant. The companies will jointly build and promote a 120MW hyper-scale data center development project in the National Industrial Complex in Bupyeong-gu, Incheon.

- Electronics manufacturing is a significant contributor to Taiwan's total Gross domestic product (GDP). Taiwan Semiconductor Manufacturing Company (TSMC) is the most important semiconductor manufacturer in the region. Recently TSMC reported its Q2 2022 earnings results, presenting a strong revenue growth of 36.6% year over year. As per the company, one of the most important reasons for this remarkable growth was the rapid expansion of its customers in the high-performance computing (HPC) industry. These include artificial intelligence researchers, data centers for cloud providers like Amazon's Amazon Web Services, and edge computing networks. HPC revenue grew 14% quarter over quarter in Q2 and now makes up 43% of TSMC's overall revenue.

Active & Passive Electronic Components Industry Overview

The active and passive electronic components market comprises long-standing established players who have made significant investments in the product. The new players entering the market require high investments. The companies can sustain themselves through powerful competitive strategies. Product innovations can also work in favor of new players as they can target emerging and less explored application areas to expand their market presence further. The degree of competition is high in the market and is expected to remain the same for the forecasted period.

In December 2022, ModCap HF, a modular capacitor designed for DC link applications that can operate at extremely high switching frequencies, was offered by TDK Corporation. The six newly created power capacitors in the B25647A* series are rated for between 900 to 1600 volts and have capacitance ranges between 640 to 1850 microfarads. The highest allowable hot spot temperature is 90 °C, and the rated currents range from 160 A to 210 A depending on the kind.

In October 2022, YAGEO Group, the world's top supplier of passive components, released the automotive grade thin film chip resistor - RP Series. The RP series' unique passivation design creates a waterproofing interface. This cover shields the resistive layer, preventing moisture from entering from the outside. With this defense, the RP Series can maintain high resistance stability in challenging conditions, making it ideal for power systems, industrial/medical equipment, telecommunications, industrial/automotive electronics, and industrial/industrial equipment.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter Five Forces

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitutes

- 4.4 Impact of COVID-19 on the industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Preference For Miniaturized Designs

- 5.1.2 Growing Number of Computing, Communications, and Consumer Electronics

- 5.1.3 Increasing Adoption of 5G Technology

- 5.2 Market Restraints

- 5.2.1 Rising Metal Prices Impacting Component Production Costs

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Active Components

- 6.1.1.1 Transistors

- 6.1.1.2 Diode

- 6.1.1.3 Integrated Circuits (ICs)

- 6.1.1.4 Amplifiers

- 6.1.1.5 Vacuum Tubes

- 6.1.2 Passive Components

- 6.1.2.1 Capacitors

- 6.1.2.2 Inductors

- 6.1.2.3 Resistors

- 6.1.1 Active Components

- 6.2 By End-user Industry

- 6.2.1 Automotive

- 6.2.2 Consumer Electronics and Computing

- 6.2.3 Medical

- 6.2.4 Industrial

- 6.2.5 Communications

- 6.2.6 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Infineon Technologies AG

- 7.1.2 NXP Semiconductors NV

- 7.1.3 Texas Instruments, Inc.

- 7.1.4 Panasonic Corporation

- 7.1.5 Murata Manufacturing Co. Ltd

- 7.1.6 Eaton Corporation

- 7.1.7 TE Connectivity Ltd.

- 7.1.8 Honeywell International Inc.

- 7.1.9 Toshiba Corp.

- 7.1.10 Vishay Intertechnology Inc.

- 7.1.11 YAGEO Corporation

- 7.1.12 TDK Corporation

- 7.1.13 KEMET Corporation (Yageo Corporation)

- 7.1.14 AVX Corporation (Kyocera Corp)

- 7.1.15 Lelon Electronics Corporation

- 7.1.16 Taiyo Yuden Co. Ltd