自動車エンジニアリングサービスのアウトソーシング:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)

Automotive Engineering Services Outsourcing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 90 Pages

- 納期

- 2~3営業日

- 商品コード

- 1536979

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

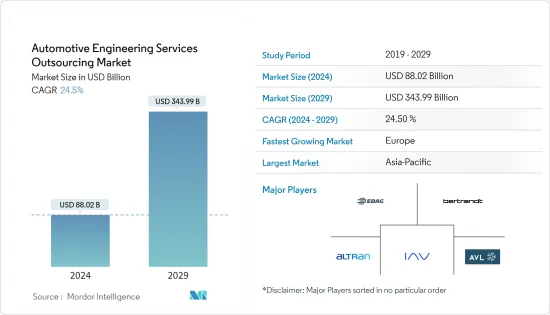

自動車エンジニアリングサービスのアウトソーシング市場規模は、2024年に880億2,000万米ドルと推定され、2029年には3,439億9,000万米ドルに達すると予測され、予測期間中(2024~2029年)のCAGRは24.5%で成長すると予測されます。

長期的に見れば、エンジニアリング企業はコスト削減、効率化、能力向上のためにアウトソーシングに急速に移行しています。企業がエンジニアリングサービスのアウトソーシングする理由は、短納期の必要性、柔軟性、社内専門家の不足、予算の制約などさまざまです。さらに、電気自動車に対する需要の増加、電気自動車の採用拡大、車両と乗客の安全性を高めるADASなどの自律走行車の革新的技術、軽量化車両などは、今後数年間の市場成長にプラスの影響を与える可能性のある主要要因です。

電気自動車販売の伸びを考慮し、サプライチェーンの複数の企業が車両部品の設計を強化するためにパートナーシップを結んでいます。各国政府は、購入者が従来の自動車よりも電気自動車に傾倒するよう奨励するため、世界中でさまざまな計画や取り組みを開始しています。

主なハイライト

- 電気自動車の購入を奨励するこうした計画のひとつに、2025年までに150万台の電気自動車を走らせるというカリフォルニアZEV計画があります。

- 2023年11月、キャップジェミニは、自律走行車、コネクテッドカー、電気自動車、シェアードカーの各領域において、ソフトウェア開発やプロダクトエンジニアリングなどの主な専門知識を駆使し、持続可能で安全、安心なコネクテッドソリューションを提供しました。キャップジェミニは、Everest Group ACES Automotive Engineering Services PEAK Matrix Assessment 2023で最高の「ビジョンと能力」評価を受け、トップリーダーに指名されました。

欧州は、OEMの存在と電気自動車に対する消費者の嗜好の変化により、対象市場で大きく成長すると予想されます。ドイツや英国などの国々の存在も、政府が実施する排出ガスに関する政策と政策、グリーン技術の利用奨励により、市場の成長にプラスの影響を与えます。北米も予測期間中にかなりの市場成長が見込まれます。

自動車エンジニアリングサービスのアウトソーシング市場の動向

乗用車がトップシェア

乗用車は、スタイリッシュなデザイン、コンパクトなサイズ、経済的価値といった特徴から、ここ数年 促進要因の間で絶大な人気を博しています。乗用車は、多くの先進国で最も一般的な交通手段となっています。ライフスタイルの改善、購買力の向上、可処分所得の増加、ブランド認知度の向上、経済性の改善により、世界的に顧客の嗜好が変化し、乗用車の販売台数が増加しています。

インド自動車工業会によると、2022~2023年の乗用車販売台数は14,67,039台から17,47,376台に増加しました。

アジア太平洋における電気自動車需要の増加も市場の成長をもたらしました。2023年第1四半期、インドの電気自動車販売台数は2022年同期比で倍増しました。

スポーツ用多目的車(SUV)の需要の高まりは、市場プレーヤーに有益な機会を創出し、世界の乗用車市場の成長の主な原動力となっています。乗用車(PV)販売全体に占めるSUVのシェアは、2016年の18%から2023年には41%に上昇しました。

各社は、自動車工学の分野でエキサイティングな能力を開発し、モビリティの将来に対するビジョンを共有することに注力しています。また、これらの能力とイノベーションを世界に拡大するための合意にも注力しています。セグメントには、電気・電子、ソフトウェア、コンサルティング・サービス、テスト、車両開発などが含まれます。

例えば、2022年10月、デジタルトランスフォーメーション、コンサルティング、ビジネス・リエンジニアリング・サービスおよびソリューションの大手プロバイダーであるテック・マヒンドラは、モビリティ業界における協業を促進するオープンEVアライアンスであるフォックスコン主導のMIH(Mobility in Harmony)コンソーシアムとの提携を発表しました。

このように、上記の要因は市場にプラスの影響を与えると予想されます。

アジア太平洋地域が自動車エンジニアリングサービスのアウトソーシング市場で大きなシェアを占める見込み

アジア太平洋地域は対象市場で大きなシェアを占めると予想されます。これは、大手自動車メーカーが存在し、低コストの労働力が利用できるため、インド、韓国、中国などの国々に生産と関連業務のアウトソーシングを行っていることに起因します。その結果、自動車用ESOプロバイダーはこの地域に事業を移転しています。

インドは、低コスト国の中で利用可能な労働力の約30%を占めています。欧州、中南米、北米諸国と比較して15~26%のコスト優位性があります。インドは、世界のさまざまなセグメントのニーズに応える世界OEMにとって、競争力の高い市場を提供しています。起亜自動車とMGは、インド市場における2つの新しいOEMです。

インドには低コストで教育を受けた半熟練労働者がいるため、アウトソーシングを求める国際的なOEMにとって魅力的な選択肢となっています。持続可能なモビリティソリューションを開発し、モビリティ業界の消費者に価値を提供できる次世代の電気自動車、自律走行ソリューション、モビリティサービスアプリケーションを構築するために、複数の企業がパートナーシップに注力しています。例えば

- 2022年8月、インドに本社を置くL&Tテクノロジーサービスは、BMWグループから5年間のインフォテインメント契約を獲得し、同社のインフォテインメントスイートにハイエンドのエンジニアリング・サービスを提供しました。BMWグループのキャンパスに近いことから、LTTSのエンジニアはさまざまなソリューションに取り組み、リアルタイムでサービスを提供できるようになります。

このように、上記の要因は市場の成長にプラスの影響を与えると予想されます。

自動車エンジニアリングサービスのアウトソーシング業界の概要

自動車エンジニアリングサービスのアウトソーシング市場は、世界的および地域的に確立された企業によって統合され、主導されています。これらの企業は、市場での地位を維持するために、新製品の発売、提携、合併などの戦略を採用しています。例えば

- 2023年9月、HCLTechはドイツの自動車エンジニアリング・サービス・プロバイダーであるASAP Groupの株式100%を2億7,600万米ドルで取得しました。この取引は2023年9月までに完了する予定でした。ASAPは、自律走行、eモビリティ、コネクティビティといった分野における未来志向の自動車技術に注力しています。

市場を独占している主要企業には、AVL List GmbH、Bertrandt AG、EDAG Engineering GmbH、IAV GmbH、Altranなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 自動車産業の急激な成長

- 市場抑制要因

- 自動車分野における研究開発業務のデジタル化

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- サービスタイプ別

- デザイン

- プロトタイピング

- システム統合

- テスト

- ロケーションタイプ別

- オンショア

- オフショア

- 車両タイプ

- 乗用車

- 商用車

- 推進タイプ

- ICエンジン

- 電気エンジン

- 地域

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 世界のその他の地域

- 南米

- 中東・アフリカ

- 北米

第6章 競合情勢

- 企業プロファイル

- AVL List GmbH

- Bertrandt AG

- EDAG Engineering GmbH

- IAV GmbH

- HORIBA Ltd

- Altran(Capgemini Engineering)

- FEV Group GmbH

- MBtech Group GmbH(A subsidiary of AKKA Technologies)

- Alten GmbH

- P3 Automotive GmbH

- Altair Engineering Inc.

- ITK Engineering GmbH(Robert Bosch GmbH)

- ESG Elektroniksystem-und Logistik-GmbH

- RLE International Group

- ASAP Holding GmbH

- Kistler Holding AG

第7章 市場機会と今後の動向

目次

The Automotive Engineering Services Outsourcing Market size is estimated at USD 88.02 billion in 2024, and is expected to reach USD 343.99 billion by 2029, growing at a CAGR of 24.5% during the forecast period (2024-2029).

Over the long term, engineering firms are rapidly shifting to outsourcing to save costs, boost efficiency, or increase competence. Companies outsource engineering services for various reasons, including the need for fast delivery, flexibility, a lack of in-house specialists, and a constrained budget. Additionally, increasing demand for electric vehicles, as well as increasing adoption of electric vehicles, autonomous vehicle innovative technologies such as ADAS for vehicle and passenger safety, and lightweight vehicles, are key factors that may positively impact market growth in the coming years.

Considering the growth in electric vehicle sales, several companies from the supply chain are entering into partnerships to enhance the design of vehicle components. Governments have launched various plans and efforts worldwide to encourage buyers to lean toward electric vehicles over conventional automobiles.

Key Highlights

- One such plan that encourages the purchase of electric vehicles is the California ZEV program, which intends to have 1.5 million electric vehicles on the road by 2025.

- In November 2023, Capgemini offered sustainable, safe, secure, and connected solutions with key expertise such as software development and product engineering in the Autonomous, Connected, Electric, and Shared vehicles domains. It received the highest "Vision and Capability" rating and was designated the top Leader by the Everest Group ACES Automotive Engineering Services PEAK Matrix Assessment 2023.

Europe is expected to grow significantly in the target market, owing to the presence of OEMs and changing consumer preference toward electric vehicles. The presence of countries such as Germany and the United Kingdom also positively impacts the market's growth due to the policies and regulations implemented by their governments related to emissions and encouraging the usage of green technology. North America is also expected to witness considerable market growth during the forecast period.

Automotive Engineering Services Outsourcing Market Trends

Passenger Cars Hold the Highest Share

Passenger cars have gained immense popularity among drivers over the past few years due to features such as stylish design, compact size, and economic value. Passenger cars are the most common mode of transportation in numerous advanced countries. The improving lifestyles, increasing purchasing power, rising disposable incomes, growing brand awareness, and improving economy are leading to a shift in customer preferences worldwide globe, resulting in high sales of passenger cars.

According to the Society of Indian Automobile Manufacturers, sales of passenger cars increased from 14,67,039 to 17,47,376 units during 2022-2023.

The increased demand for electric vehicles in Asia-Pacific also resulted in market growth. In the first quarter of 2023, electric car sales in India doubled compared to the same period in 2022.

The rising demand for sport utility vehicles (SUVs) creates profitable opportunities for market players and acts as a major driving factor for the global passenger car market's growth. The share of SUVs in overall passenger vehicle (PV) sales rose from 18% in 2016 to 41% in 2023.

Companies are focusing on developing some exciting capabilities in automotive engineering and sharing their vision for the future of mobility. They are also focusing on agreements to scale these capabilities and innovations globally. The segments include electric/electronics, software, consulting and service, testing, and vehicle development.

For instance, in October 2022, Tech Mahindra, a leading provider of digital transformation, consulting, and business re-engineering services and solutions, announced a partnership with Foxconn-initiated MIH (Mobility in Harmony) Consortium, an open EV alliance that promotes collaboration in the mobility industry.

Thus, the abovementioned factors are expected to have a positive impact on the market.

Asia-Pacific is Expected to Hold a Major Share in the Automotive Engineering Service Outsourcing Market

Asia-Pacific is likely to have a large share of the target market, attributed to the presence of significant automobile OEMs and the outsourcing of production and associated operations to countries such as India, South Korea, and China due to the availability of low-cost labor. As a result, automotive ESO providers are transferring their operations to this region.

India accounts for roughly 30% of all available manpower among low-cost countries. The country has a 15-26% cost advantage over European, Latin American, and North American countries. India has provided a highly competitive market for global OEMs catering to the needs of various segments worldwide. Kia and MG are two new OEMs in the Indian market.

The availability of low-cost, educated, and semi-skilled labor in India makes it an attractive option for international OEMs seeking to outsource their operations. Several firms focus on partnerships to develop sustainable mobility solutions and build the next generation of electric vehicles, autonomous driving solutions, and mobility service applications that can deliver value for consumers in the mobility industry. For instance,

- In August 2022, L&T Technology Services, headquartered in India, bagged a 5-year infotainment deal from BMW Group to provide high-end engineering services for the company's suite of infotainment. The proximity to BMW Group's campus will enable LTTS' engineers to work on a variety of solutions and offer services in real-time.

Thus, the abovementioned factors are expected to positively impact the market's growth.

Automotive Engineering Services Outsourcing Industry Overview

The automotive engineering services outsourcing market is consolidated and led by globally and regionally established players. These companies adopt strategies such as new product launches, collaborations, and mergers to sustain their market positions. For instance,

- In September 2023, HCLTech acquired a 100% stake in the German automotive engineering services provider ASAP Group for USD 276 million. The transaction was expected to close by September 2023. ASAP is focused on future-oriented automotive technologies in areas such as autonomous driving, e-mobility, and connectivity.

Some major players dominating the market include AVL List GmbH, Bertrandt AG, EDAG Engineering GmbH, IAV GmbH, and Altran.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Exponential Increase in Automotive Sector

- 4.2 Market Restraints

- 4.2.1 Digitization of R&D Operations in Automotive Sector

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Service Type

- 5.1.1 Designing

- 5.1.2 Prototyping

- 5.1.3 System Integration

- 5.1.4 Testing

- 5.2 By Location Type

- 5.2.1 Onshore

- 5.2.2 Offshore

- 5.3 Vehicle Type

- 5.3.1 Passenger Vehicles

- 5.3.2 Commercial Vehicles

- 5.4 Propulsion Type

- 5.4.1 IC Engine

- 5.4.2 Electric Engine

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Rest of the World

- 5.5.4.1 South America

- 5.5.4.2 Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE*

- 6.1 Company Profiles

- 6.1.1 AVL List GmbH

- 6.1.2 Bertrandt AG

- 6.1.3 EDAG Engineering GmbH

- 6.1.4 IAV GmbH

- 6.1.5 HORIBA Ltd

- 6.1.6 Altran (Capgemini Engineering)

- 6.1.7 FEV Group GmbH

- 6.1.8 MBtech Group GmbH (A subsidiary of AKKA Technologies)

- 6.1.9 Alten GmbH

- 6.1.10 P3 Automotive GmbH

- 6.1.11 Altair Engineering Inc.

- 6.1.12 ITK Engineering GmbH (Robert Bosch GmbH)

- 6.1.13 ESG Elektroniksystem- und Logistik-GmbH

- 6.1.14 RLE International Group

- 6.1.15 ASAP Holding GmbH

- 6.1.16 Kistler Holding AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 90 Pages

- 納期

- 2~3営業日