|

市場調査レポート

商品コード

1850279

航空機用アクチュエータ:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Aircraft Actuators - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空機用アクチュエータ:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月24日

発行: Mordor Intelligence

ページ情報: 英文 131 Pages

納期: 2~3営業日

|

概要

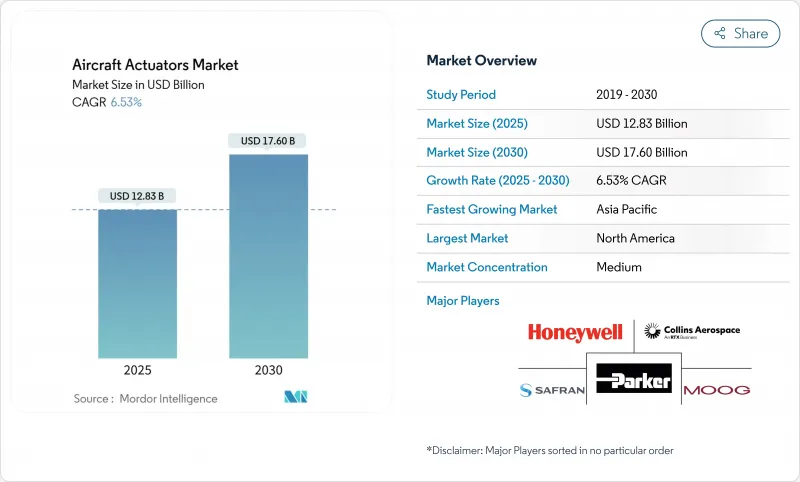

航空機用アクチュエータの市場規模は2025年に101億6,000万米ドル、2030年には137億3,000万米ドルに達すると予測され、CAGRは6.21%です。

単通路プログラム、航空機の電動化戦略、ヘルスモニター用電子機器を組み込んだ改修のための製品タイプの受注残が、すべての主要プラットフォームタイプで堅調な受注を維持しています。航空会社が燃費を重視する中、電気・電子機械ユニットのシェアが拡大する一方、油圧設計は最も安全性が重視される主制御の足場を固めつつあります。ワイドボディの急速な代替サイクル、eVTOL認証パスの加速化、レアアース供給チェーンの逼迫が、Tier1インテグレーターやTier2部品スペシャリストのキャパシティプランニングをさらに複雑にしています。

世界の航空機用アクチュエータ市場の動向と洞察

ナローボディ機生産残の急増

各機体には、航空機用アクチュエータ市場を支える複数のリニアユニットとロータリーユニットが搭載されています。エアバスは2024年に766機を引き渡し、ボーイングは348機を出荷したが、合計のバックログは2025年に14年ぶりのピークを記録しました。パーカー・ハネフィンの航空宇宙部門は、リーン・マニュファクチャリングのアップグレード後、2025年第3四半期に28.7%の営業利益率を達成しました。納入されるすべてのナローボディは、15~20年の予測可能なアフターマーケット需要を牽引し、アクチュエーターベンダーの安定した収益基盤を支えます。北米と欧州はバックログの大半を受け入れているため、これらの地域は新しいアクチュエーターテストスタンドとデジタルスレッドイニシアチブのための資本を引き付け続けています。

二次飛行システムの電化の増加

航空機メーカーは、フラップ、スラット、ランディングギアステアリング、環境制御を油圧式から電気機械式に移行しており、対応可能な航空機用アクチュエータ市場を拡大しています。コリンズ・エアロスペース社は、電気システム開発に30億米ドルを計上し、より軽量でクリーンなプラットフォームへの長期的なコミットメントを表明しました。B787に搭載されたサフランの電動ブレーキは、油圧ラインを取り除き、使用中の摩耗分析を可能にしました。クリーン・アビエーションの電動ノーズギア実証機は、静電作動によって質量を20%削減することを目指しています。電気負荷の増大は組込み型熱制御の需要を高め、電力密度の高いドライブと先進的な誘電オイルの技術革新に拍車をかけています。

プライマリ・フライト・コントロールにおける油圧に対する持続的な信頼性懸念

航空規制当局は、プライマリ・コントロール・サーフェスに業界最高の耐故障閾値を課していますが、電気機械ユニットは、三重冗長油圧回路と比較した場合、いまだに懐疑的な見方に直面しています。FAAのシステム安全規則改正では、徹底的な共通原因故障解析が義務付けられ、認証プログラムが最大7年延長されることになりました。ムーグは30年にわたり航空宇宙用EMAを提供してきたが、採用はスポイラー、スラット、トリムタブに限られ、エレベーターとエルロンは油圧式にとどまっています。航空会社は、未解決の信頼性認識をスケジュールおよび法的責任リスクとみなしており、プライマリサーフェス用途の航空機用アクチュエータ市場の当面の成長を減速させています。

セグメント分析

リニア設計は2024年の売上高の69.00%を占めました。ナローボディにはフラップ、スポイラー、ドアに複数のスクリュージャックソリューションが組み込まれているためです。回転機構の航空機用アクチュエータ市場規模は、低質量で正確な角度位置決めを重視するアダプティブ・ウィングやティルト・ローター・システムから獲得し、最も急速に拡大します。航空機用アクチュエータ市場におけるロータリー需要は、厳しいバックラッシュ制御と長いライフサイクルを必要とするeVTOLチルトシステムと将来の可変キャンバー翼からもたらされます。

電気機械式ロータリーパッケージは、次世代シングル通路の高揚力システムにおいて、油圧式に取って代わりつつあります。一方、メイン・ランディング・ギア・アップロックではリニア油圧が優位を保っており、力技と伝統的な基準が流体動力を支持しています。したがって、ティアワン・サプライヤーは、サイクルをヘッジするためにデュアル・プラットフォーム・ポートフォリオを追求しています。この戦略は、ハネウェルのデジタル・モーター・コントローラと組み合わせたリーガル・レックスノードのコンパクトなeVTOL対応ギアボックスに代表されます。

2024年の支出額の43.50%は油圧で、主にプライマリー・フライト・コントロールに使われます。二次表面の改造が電気ドライブの着実なシェア拡大を下支えし、特にバッテリー電気とハイブリッド推進プロジェクトが全システムに共通電圧バスを要求しています。静電ハイブリッドは、力密度や認証文化が依然として流体を好む場合の橋渡しソリューションを提供し、航空機用アクチュエータ市場が電動に傾いても収益を守る。

ワイドバンドギャップパワーエレクトロニクスにおける熱管理のブレークスルーは、ディレートを引き起こすことなく電動ジャッキスクリューの高デューティサイクルを可能にします。油圧インテグレーターは、流体交換間隔を延長するデジタル圧力センサーとエッジ分析を組み込むことで対応し、設置ベースを守りつつ、最終的な移行に備えます。

地域分析

北米は、ボーイングのナローボディの回復、ロッキード・マーチンの戦闘機生産、ハネウェルの強力なアフターマーケット牽引により、2024年売上高の35.25%を維持。ハイブリッド電気実証機に対する連邦政府の優遇措置により、コリンズ、ムーグ、サフランの工場に研究開発助成金が振り向けられ、この地域の技術基盤が強化される一方で、サプライチェーンがレアアースショックにさらされることになります。

アジア太平洋地域の2030年までのCAGRは7.09%になります。中国のC919の立ち上げとCOMACのCR929の設計研究は、現地調達率の目標を引き上げ、成都、上海、西安に合弁会社を設立するようティアオンに促します。インドのTejas Mk1A戦闘機と近々発表されるAMCA戦闘機には、65%の国産ハードウェア枠が設定され、国内のアクチュエーター加工会社と電子機器会社に門戸が開かれます。日本の再軍備予算は10年間でミサイルと戦闘機の数量を倍増させる。

欧州は、エアバスの運賃引き上げと、100%SAFと水素互換システムを支持するクリーン航空プログラムによって前進します。サフラン、リープヘル、ウッドワードがEUの持続可能性クレジットを活用し、全電動ブレーキ、ノーズギア、トリムタブの実証実験に資金を提供。中東と南米では、エミレーツ航空、カタール航空、エンブラエルのE2ラインでの航空機の更新に関連した緩やかな導入が見られ、ドバイとサン・ジョゼ・ドス・カンポスでのMROハブの拡大によって補完されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- ナローボディの生産残が急増

- 二次飛行システムの電動化の促進

- 健康モニタリングスマートアクチュエータの改造需要の高まり

- より多くの電気とハイブリッド電気航空機プログラム(A321XLR、Eviation Alice)

- UAVおよびeVTOLにおける軽量電気油圧アクチュエータ(EHA)の採用

- SAFと水素駆動による作動負荷の再設計に対する政府の支援

- 市場抑制要因

- 主要な飛行制御における油圧に対する継続的な信頼性の懸念

- 超音速プラットフォームにおける高出力EMAの熱管理限界

- 希土類磁石サプライチェーンの集中

- 長寿命改修プログラムにおけるAOG主導のコスト圧力

- バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- ライバル関係の激しさ

第5章 市場規模と成長予測

- タイプ別

- リニア

- ロータリー

- システム別

- 油圧アクチュエータ

- 電気/電気機械アクチュエータ

- 空気圧アクチュエータ

- 機械アクチュエータ

- 用途別

- 飛行制御面

- 着陸装置とブレーキ

- 燃料と推力の管理

- キャビンとシートシステム

- 環境・ユーティリティシステム

- エンドユーザー別

- 民間航空機

- 軍用機

- 一般航空

- フィット

- OEM

- アフターマーケット

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 南米

- ブラジル

- その他南米

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Honeywell International Inc.

- Collins Aerospace(RTX Corporation)

- Parker-Hannifin Corporation

- Moog Inc.

- Eaton Corporation plc

- Safran SA

- Woodward, Inc.

- Triumph Group, Inc.

- Liebherr-International Deutschland GmbH

- Nabtesco Corporation

- Crane Company

- Curtiss-Wright Corporation

- Electromech Technologies(TransDigm Group)

- BAE Systems plc

- Servotecnica SpA

- SAM GmbH

- ITT Inc.

- Heroux-Devtek