|

市場調査レポート

商品コード

1445690

シャンパン: 市場シェア分析、業界動向と統計、成長予測(2024:2029)Champagne - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| シャンパン: 市場シェア分析、業界動向と統計、成長予測(2024:2029) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 156 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

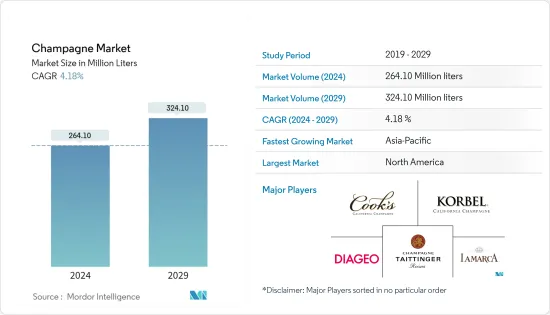

シャンパン市場規模は2024年に2億6,410万リットルと推定され、2029年までに3億2,410万リットルに達すると予測されており、予測期間(2024年から2029年)中に4.18%のCAGRで成長します。

シャンパンはさまざまなブドウから作られ、柑橘類、リンゴ、アーモンドなどの風味があります。外食レストランやバーの増加により、欧州や北米などの地域でシャンパンの需要が高まっています。かつて人々は、業績や結婚式などの特別な機会にシャンパンを飲んでいました。しかし最近では、この地域では誕生日、会社のパーティー、食事会などでカジュアルに飲むことが増えています。さらに、ヴィンテージワインやシャンパンは、本物の味や味わいに対する消費者の意識の高まりにより、世界中で人気を集めています。中期的に見て、業界のプレミアム化は依然としてアルコール飲料市場、特に蒸留酒とワインを推進する主要な要因の1つです。

可処分所得の増加により、消費者は特別な日のために高価な高級シャンパンをすぐに購入します。オーガニック/ナチュラルおよびビーガン原料の使用に関するメーカーの製品革新や、シャンパンの場合の環境に優しいパッケージングにより、世界中の新しい市場への浸透と拡大が可能になっています。たとえば、2021年 4月、Ruinart Champagneは、自社のシャンパンに環境に優しい新しいセカンドスキン包装を発売しました。新しい100%紙製ケースは完全にリサイクル可能で、劣化するまで数時間アイスバケツの冷たさに耐えることができます。この革新的なデザインは、ケースが地球を意識しながらも、入ってくる光を遮断することでワインの完全性を維持するために作られました。

シャンパン市場の動向

市場の成長を促進するオンラインプラットフォーム

シャンパンを含むアルコールのオンライン小売は急速に成長しています。 Drizlyやliquor.comなどのオンデマンド配達アプリがこの分野の原動力となっています。最近では、消費者からの需要の高まりに応えるために、著名なeコマース小売業者も市場に参入しています。伝統的に、シャンパンブランドはワインの販売を流通業者や小売業者にのみ依存してきました。それでも、ホスピタリティ業界の苦戦が続く中、生産者にとって失われた収益を取り戻すための消費者直販(DTC)チャネルは魅力的なものとなっています。中国、インド、日本などの国々での多くの空港拡張もシャンパン市場の成長の理由です。シャンパンは貿易外で購入するのに便利な選択肢であるため、バーやレストランの数によりオンライン販売が増加しました。さらに、各国の輸出入の可能性も市場を牽引すると予想されます。

欧州が大きなシェアを保持

この地域の原産であるシャンパンは、他のアルコール飲料の中でも高い浸透率を誇ります。その結果、世界的には欧州地域がシャンパン消費量で大きなシェアを占めており、フランス、英国、ドイツなどで生産されるシャンパンのほとんどが世界150カ国以上に輸出されています。さらに、業界でのプレミアム化の普及により、製品のバリューセールが増加しています。健康に優しい飲料への注目の高まりにより、無味無添加、グルテンフリー、低炭水化物、ビーガン対応、オーガニック、パレオフレンドリーなどの記述子を使用したシャンパンのバリエーションが欧州の消費者の間で注目を集めています。さらに、外国人観光客がエキゾチックな高級シャンパンに惹かれているため、地域観光の成長も市場を牽引しています。 2021年のUNWTOデータによると、2021年に欧州を訪れる国際観光客は3億310万人です。

シャンパン業界の概要

シャンパン市場は細分化されており、さまざまな製品を提供する複数の世界的および地域的プレーヤーの存在により、競争が激しくなっています。市場の主要企業には、 Diageo plc、La Marca USA、F. Korbel & Bros.、Cook's Champagne Cellars、Champagne Taittinger CCVCなどが含まれます。これらの企業は、より大きな市場シェアを獲得するために、生産・流通ネットワークを拡大し、ソーシャルメディアでの存在感を強化することに加えて、合併・買収、製品革新、パートナーシップにも着手しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- タイプ

- ブリュット・シャンパン

- ロゼ・シャンパン

- ブラン・ド・ブラン

- ブラン・ド・ノワール

- デミセック

- プレステージキュヴェ

- 流通チャネル

- オントレード

- オフトレード

- オンライン小売店

- オフラインの小売店

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米

- 欧州

- 英国

- ドイツ

- スペイン

- フランス

- イタリア

- ロシア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東とアフリカ

- 南アフリカ

- サウジアラビア

- その他中東およびアフリカ

- 北米

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- Diageo plc

- La Marca USA

- F. Korbel &Bros.

- Cook's Champagne Cellars

- Champagne Taittinger CCVC

- Societe Jacques Bollinger SA

- Andre Champagne Cellars

- Laurent-Perrier Group

- Champagne AYALA

- LVMH Moet Hennessy

第7章 市場機会と将来の動向

The Champagne Market size is estimated at 264.10 Million liters in 2024, and is expected to reach 324.10 Million liters by 2029, growing at a CAGR of 4.18% during the forecast period (2024-2029).

Champagne is made from various grapes and flavors like citrus, apple, and almond. Demand for champagne is increasing in the regions like Europe and North America because of the increase in food service restaurants and bars. People used to have champagne for special occasions like achievements or weddings. But these days, casual drinking on birthdays, office parties, and dinners is increased in the region. Furthermore, vintage wines and champagnes are gaining popularity worldwide because of consumer awareness regarding authentic flavors and tastes. Over the medium term, industry premiumization remains one of the major factors driving the alcoholic beverage market, particularly spirits and wine.

Due to the increased disposable income, consumers quickly buy expensive luxury champagnes for their special occasions. Product innovations by manufacturers regarding the usage of organic/natural and vegan ingredients, as well as eco-friendly packaging in the case of champagne, are allowing deeper penetration and expansion to new markets across the globe. For instance, in April 2021, Ruinart Champagne launched the new Eco-Friendly Second Skin Packaging for its champagne. The new 100% paper case is fully recyclable and can withstand an ice bucket chill for several hours before deteriorating. The innovative design was created to maintain the wine's integrity by blocking incoming light while keeping the case conscious of the planet.

Champagne Market Trends

Online Platform to Increase the Market Growth

Online retailing of alcohol, including champagne, is growing faster. The on-demand delivery apps, such as Drizly and liquor.com, are the driving forces of this segment. Recently, prominent e-commerce retailers also entered the market to cater to the increasing demand from consumers. Traditionally, champagne brands have relied exclusively on distributors and retailers to sell their wines. Still, as the hospitality sector continues to struggle, direct-to-consumer (DTC) channels have become attractive for producers to recuperate lost revenue. Many airport expansions in the countries like China, India, and Japan are also the reasons for the champagne market growth. The number of bars and restaurants increased the online sales of champagne as it is a convenient option for off-trade purchases. Furthermore, the import-export potential of the countries is also expected to drive the market.

Europe Held a Significant Share

Being native to the region, Champagne witnesses high penetration among other alcoholic beverages. As a result, globally, the European area holds a significant share in champagne consumption, whereby most of the champagne produced in countries like France, the United Kingdom, and Germany, among others, is exported to more than 150 countries across the globe. Additionally, the growing prevalence of premiumization in the industry is boosting the value sales of the product. Champagne variants that use descriptors like no taste additives, gluten-free, low carb, vegan-friendly, organic, and paleo-friendly have been gaining prominence among European consumers due to the increasing focus on health-friendly beverages. Furthermore, growing regional tourism is also driving the market as international visitors are attracted to exotic luxury champagnes. According to UNWTO data from 2021, international tourists visiting Europe in 2021 are 303.1 million.

Champagne Industry Overview

The champagne market is fragmented and highly competitive owing to the presence of multiple global and regional players offering various products. Key players in the market include Diageo plc, La Marca USA, F. Korbel & Bros., Cook's Champagne Cellars, and Champagne Taittinger CCVC, among others. These players have been embarking on mergers & acquisitions, product innovations, and partnerships, apart from expanding their production & distribution networks and strengthening their social media presence to garner a larger market share.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Brut Champagne

- 5.1.2 Rose Champagne

- 5.1.3 Blanc De Blancs

- 5.1.4 Blanc De Noirs

- 5.1.5 Demi-Sec

- 5.1.6 Prestige Cuvee

- 5.2 Distribution Channel

- 5.2.1 On-Trade

- 5.2.2 Off-Trade

- 5.2.2.1 Online Retail Stores

- 5.2.2.2 Offline Retail Stores

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 Spain

- 5.3.2.4 France

- 5.3.2.5 Italy

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Diageo plc

- 6.3.2 La Marca USA

- 6.3.3 F. Korbel & Bros.

- 6.3.4 Cook's Champagne Cellars

- 6.3.5 Champagne Taittinger CCVC

- 6.3.6 Societe Jacques Bollinger SA

- 6.3.7 Andre Champagne Cellars

- 6.3.8 Laurent-Perrier Group

- 6.3.9 Champagne AYALA

- 6.3.10 LVMH Moet Hennessy