|

市場調査レポート

商品コード

1910692

モバイルウォレット:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Mobile Wallet - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| モバイルウォレット:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

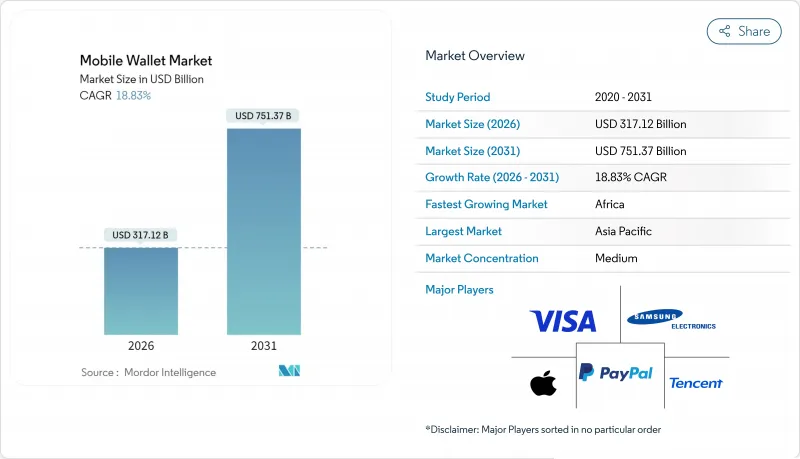

2026年のモバイルウォレット市場規模は3,171億2,000万米ドルと推定されており、2025年の2,668億5,000万米ドルから成長を続けています。

2031年までの予測では7,513億7,000万米ドルに達し、2026年から2031年にかけてCAGR18.83%で拡大が見込まれます。

この成長は、スマートフォン所有率の急増、リアルタイム決済インフラに関する政府の義務付け、および銀行の非接触型モデルへの戦略的転換によって推進されています。2024年にはブラジルのPixが640億件の取引を処理し、前年比53%増加しました。一方、インドのUPIは1,200億件以上の取引を処理し、口座間決済システムがモバイルウォレット市場の主要な推進力であることを裏付けています。スーパーアプリエコシステムは、特にアジア太平洋地域において、電子商取引、配車サービス、マイクロ融資といった分野にモバイルウォレットが組み込まれることで、ユーザーエンゲージメントの深化を続けております。一方、QRコード決済システムは新興経済国において加盟店の導入コストを低減し、小規模小売業者が高額なPOS端末を回避することを可能にしております。特にEUにおけるインターチェンジ手数料への規制圧力により、プロバイダーはロイヤルティプログラム、融資、保険といった付加価値サービスへの多角化を進めており、収益化戦略の再構築が進んでおります。

世界のモバイルウォレット市場の動向と洞察

政府主導のリアルタイム決済基盤が市場変革を推進

中央銀行主導の取り組みが、カードネットワークに代わる即時・低コストの代替手段を提供することで競争構造を再定義しています。ブラジルのPixは2024年に26兆5,000億米レアル(4兆7,000億米ドル)を処理し、5年以内に国内電子商取引取引の58%を占める見込みです。インドでも同様の動きが顕著で、UPIの成長により同プラットフォームは相互運用性のある決済における官民のベンチマークとなっています。国境を越えた実験も進行中です。ブラジルが計画するラテンアメリカ諸国とのPix回廊や、2025年度に予定される日本・ASEAN QRコード連携などが挙げられます。各国政府はこれらのインフラを、金融主権の確立と金融政策の伝達効率化を促進する触媒と位置付けています。

スーパーアプリ・エコシステムが消費者の決済行動を変革

多機能アプリ内に決済機能を組み込むことで、ユーザーエンゲージメントが向上し、獲得コストが削減されます。テンセントはWeChat Payが月間14億ユーザーを収益化した結果、2025年第1四半期に13%の収益成長を報告しました。東南アジアでは、ベトナムのデジタルウォレットユーザー数が2024年末までに前年比40%増の5,000万人に達すると予測されています。PayPalなどの欧米企業は、ショッピング・ポイント還元・クレジット機能を融合させることで準スーパーアプリ化を進めておりますが、データプライバシー規制が完全な統合を遅らせています。競争優位性はデータ駆動型パーソナライゼーションに由来し、単純な決済を超えた個別対応型の融資・保険商品提供を可能にしております。

EUのインターチェンジ手数料規制が収益モデルに圧力をかける

EUが2029年までインターチェンジ上限を延長したことで、カードベースのウォレットの利益率が制限されています。VisaとMastercardは、小売手数料の圧縮を補うため、モバイル仮想カードの導入やB2Bウォレットの拡大で対応しました。Weroウォレットなどの欧州の取り組みはカード決済基盤を完全に回避しており、口座間決済アーキテクチャへの戦略的転換を示しています。規模に欠ける小規模プロバイダーは、収益化が融資、データ、保険へ移行する中で、統合圧力に直面しています。

セグメント分析

リモート決済は2031年までにCAGR22.94%で拡大し、近接決済の成長率を上回ります。Eコマースプラットフォームは決済時の摩擦を最小化し即時返金を可能とするため、ウォレットをますます重視しています。デジタルウォレットは2024年に世界のオンライン支出の53%を占めました。国境を越えた機能性は重要な優位性であり、従来型コルレス銀行ネットワークを介さず消費者が支払いを可能にします。しかしながら近接決済は、交通システムや小売業における日常的な活動の基盤であり続けています。2024年に25億枚のカードに搭載されたNFCトークンは、店舗内での高頻度取引において依然として有用です。

2025年現在、近接決済はモバイルウォレット市場シェアの63.62%を占めており、物理環境における消費者の定着した習慣を示しています。加盟店は決済の迅速化とロイヤルティプログラム統合のため、タップ&ゴー対応端末への投資を進めています。単一ウォレットアプリ内でのNFCとQRコードの融合により、従来のモード区別が曖昧になり、オムニチャネル対応が長期的な差別化要因として位置づけられています。

オープンウォレットは相互運用性に関する規制要求を背景に、24.60%のCAGRで拡大が見込まれます。Appleが欧州でiOSのNFCをサードパーティに開放した決定は、プラットフォーム中立性への広範な移行を示唆しています。優れたユーザー体験とハードウェアとの緊密な連携により、クローズドエコシステムは2025年においても収益の45.12%を占めました。しかしながら、独占禁止法の監視強化や加盟店側によるプラットフォーム手数料への反発が、今後の成長ペースを抑制する要因となっています。

トークン化は安全な相互運用性の基盤となります。Visaは2014年以降100億トークンを発行し、6億5,000万米ドルの不正利用を防止しました。オープンウォレットが基盤技術ではなくサービス層で競争する中、差別化されたオンボーディング、組み込み型クレジット、状況に応じたオファーが普及の軌道を形作るでしょう。

モバイルウォレット市場レポートは、決済方式(近距離決済、遠隔決済)、用途(モバイルコマース、送金など)、ウォレットタイプ(クローズド、セミクローズド、オープン)、エンドユーザー(個人、法人)、地域別に分類されています。市場予測は金額(米ドル)で提供されます。

地域別分析

アジア太平洋地域は2025年の取引額の48.60%を占め、中国のWeChat PayとAlipayが牽引しています。両社で国内モバイル決済の90%以上を処理しています。インドのUPIは2024年に約1,200億件の送金を処理し、オープン決済インフラにおける同国の主導的立場を確固たるものにしました。東南アジアの成長は引き続き堅調です:ベトナムは2024年末までに5,000万のアクティブウォレットを目標としており、インドネシアのQRIS取引は1年間で217%増加しました。日本がASEANと提携し、2025年までに共同QR決済サービスを開始する計画は、地域間の相互運用性を深化させるでしょう。

アフリカでは2031年までにCAGRが26.05%見込まれており、成人の60%が銀行口座を持たない状況に対応するモバイルマネーソリューションが基盤となっています。ナイジェリアの急成長するフィンテック業界とケニアの成熟したM-Pesaエコシステムは、さらなる成長の可能性を示しています。中央銀行は金融包摂と決済効率のさらなる向上に向け、デジタル通貨の導入を検討中です。

ラテンアメリカでは飛躍的な進展が見られます。ブラジルのPixは2024年に26.5兆レアルを処理し、国内モバイル取引の85%を既に占めています。コロンビアでは2021年から2023年にかけてウォレット利用者が倍増し、アルゼンチンの「買ったら後払い」サービスの普及はウォレット機能の多様化を示しています。規制の地域的な差異は、規模拡大を目指す事業者にとって機会であると同時に複雑さも伴います。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3か月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 東南アジア全域におけるQRコードウォレットの急速な普及

- 決済機能を統合したスーパーアプリ・エコシステムの成長(中国、インド)

- 政府主導のリアルタイム決済基盤(例:インドUPI、ブラジルPix)が電子ウォレット普及を促進

- 交通機関が非接触型運賃収受へ移行する動きが市場を牽引しております

- カードネットワークのトークン化APIがウォレット取引の不正利用を低減

- 市場抑制要因

- EUにおけるインターチェンジ手数料上限がウォレット収益モデルを圧迫

- ラテンアメリカにおける中級Android端末のNFC搭載率の不均一性

- 中東・北アフリカ地域における断片化された本人確認(KYC)規則が新規顧客の受け入れを遅延させております

- ソーシャルエンジニアリングによる口座間詐欺の増加が信頼を損なう

- バリューチェーン分析

- 規制の見通し

- テクノロジーの見通し

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 価格分析

- 業界利害関係者分析

- 投資分析

- 市場におけるマクロ経済動向の評価

第5章 市場規模と成長予測

- 決済方法別

- 近接性

- リモート

- ウォレットタイプ別

- クローズド

- セミクローズド

- オープン

- 用途別

- 小売および店頭決済

- モバイルコマース

- 送金・送金サービス

- 請求書のお支払いとチャージ

- 公共交通機関と有料道路

- 食品・ホスピタリティ

- エンドユーザー別

- 個人

- ビジネス

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東

- アラブ首長国連邦

- サウジアラビア

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Apple Inc.

- Alphabet Inc.

- Samsung Electronics Co. Ltd.

- PayPal Holdings Inc.

- Tencent Holdings Ltd.

- Ant Group

- Visa Inc.

- MasterCard Inc.

- American Express Co.

- JPMorgan Chase & Co.

- Adyen NV

- Square Inc.

- Revolut Ltd.

- Grab Holdings Ltd.

- Paytm Payments Bank Ltd.

- One97 Communications

- PhonePe Pvt. Ltd.

- MobiKwik Systems Ltd.

- Mercado Libre Inc.(Mercado Pago)

- MTN Group(MoMo)

- Orange S.A.