|

|

市場調査レポート

商品コード

1445459

病理デバイス:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Pathology Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 病理デバイス:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

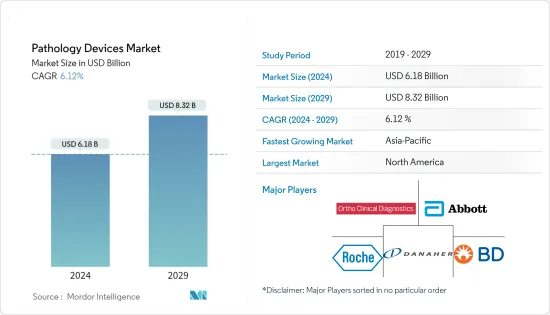

病理デバイス市場規模は2024年に61億8,000万米ドルと推定され、2029年までに83億2,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に6.12%のCAGRで成長します。

主なハイライト

- COVID-19のパンデミックは世界中のヘルスケアシステムに大きな影響を与え、多くのヘルスケア施設が日常診療や病理学的検査の提供を停止し、がんや心血管障害などの慢性疾患を持つ患者を深刻なリスクにさらしました。たとえば、2022年1月にInternational Medical Journalに掲載された記事によると、ロックダウン前とロックダウン後の病理検査数とベースライン期間の比率がそれぞれ1.02から0.53に減少したことが観察されました。

- しかし、国民の間でのコロナウイルス感染者の増加により、病理学的検査の需要が増加しています。たとえば、2022年 3月にFrontiers in Pathologyに掲載された記事によると、ロックダウン期間中に分子微生物検査の数が3倍以上増加したことがわかりました。これにより、同社は革新的な病理学的検査キットおよび装置の開発に一層注力するようになりました。したがって、調査対象の市場は今後数年間で成長し、その可能性を最大限に取り戻すことが期待されています。

- 世界中でアルツハイマー病、自己免疫疾患、がんなどの有病率と負担の増加により、効果的で高度な診断検査の必要性が高まっており、市場の成長を推進しています。たとえば、アルツハイマー病協会が発行した2022年の統計によると、2022年には65歳以上のアメリカ人は推定650万人がアルツハイマー型認知症を抱えており、この数は2050年までに1,300万人に達すると予測されています。アルツハイマー病に苦しむ人の割合が増加すると、医師が病気の原因となる認知症の症状を早期に特定するのに役立つ病理デバイスの需要が高まり、市場の成長が促進されると予想されます。

- さらに、ACSが発表した2023年の統計によると、2023年には米国で約24,810件の脳または脊髄の悪性腫瘍(男性で14,280件、女性で10,530件)が診断されると予想されています。脊髄腫瘍は、脊椎の病状を検出するための放射性核種骨シンチグラフィー(骨スキャン)の需要を刺激し、市場の成長を促進すると予想されます。さらに、技術的に高度な病理学的キットおよび装置の開発に注力している新興企業も市場の成長に貢献しています。たとえば、2022年 4月にシスメックス欧州は、新しい3部構成の差動システムであるXQ-320 XQシリーズ自動血液分析装置を発売しました。これは、信頼性の高い技術と新しい機能により、さまざまな臨床検査環境に卓越した品質をもたらす堅牢なデバイスです。使用感のレベル。

- したがって、慢性疾患や感染症の負担の高さや新製品の発売などの要因により、調査対象の市場は予測期間中に成長すると予想されます。しかし、機器の高コストと厳しい規制、熟練した専門家の不足により、予測期間中の病理学的機器の成長が妨げられる可能性があります。

病理デバイス市場動向

分子診断セグメントは予測期間中にかなりの市場シェアを保持すると予想される

- 分子診断装置は、ゲノムおよびプロテオーム内の生物学的マーカーを分析して病原体や変異を検出するために使用されます。この技術に基づいて、分子診断デバイスは、チップとマイクロアレイ、質量分析法、次世代シーケンシング(NGS)、ポリメラーゼ連鎖反応(PCR)ベースの方法、細胞遺伝学、および分子イメージングに分割できます。細菌およびウイルスの流行の大規模発生、ポイントオブケア診断の需要の増加、急速に進化する技術などの要因が、分子診断分野の成長を推進しています。

- がん、心血管疾患、脳腫瘍などによる負担の増大が、この部門の成長を推進する重要な要因となっています。たとえば、英国心臓財団が2022年 1月に発表した統計によると、2021年には英国で760万人以上が心血管疾患を抱えて暮らしていました。

- また、全米脳腫瘍協会が発表した2022年の統計によれば、2022年に米国では約88,970人が原発性脳腫瘍と診断されました。したがって、人口における心臓病と脳腫瘍の高い有病率が、脳腫瘍の増加を促進すると予想されます。分子診断に対する需要が高まっており、これにより診断精度が向上し、予後予測が可能になり、標的の特定が可能になります。これにより、予測期間中のセグメントの成長が促進されると予想されます。

- さらに、分子診断における技術的に高度な製品の開発と新製品の発売の増加に対する企業の注力の増加が市場の成長に貢献しています。たとえば、Mylab Discovery Solutionsは2022年 3月に、免疫学、生化学、血液学向けのあらゆる種類の日常診断キットとデバイスを、従来型およびポイントオブケア形式で発売しました。この製品ラインの拡張により、研究室は同社のデバイスと試薬キットを使用して、肝臓パネル、心臓プロファイル、尿パネル、ホルモンパネル、発熱パネル、腎機能検査、がんマーカー、その他の検査などのあらゆる日常的な検査を行うことができるようになります。

- したがって、心臓病や脳腫瘍の負担の高さ、高精度医療に対する需要の増大、製品発売の増加などの要因により、調査対象のセグメントは予測期間中に成長すると予想されます。

北米は予測期間中にかなりの市場シェアを持つと予想される

- 北米は、感染症や慢性疾患の蔓延、ヘルスケアインフラの改善、病理デバイスの技術進歩により、病理デバイス市場で大きなシェアを握ると予想されています。

- この地域での慢性疾患や感染症の増加により、病状の早期発見と診断の需要が増加し、それが病理検査の需要を刺激し、それによって市場の成長を促進すると予想されます。たとえば、ACSが発表した2023年の統計によると、2023年には米国で約1,958,310人の新規がん患者が診断されると予測されています。

- さらに、同じ情報源から、2023年には米国で新たに結腸直腸がん16万3,020例、肺および気管支23万8,340例、乳がん29万7,790例、前立腺がん28万8,300例が新たに診断されると予想されています。 CDCが発表した2022年のデータによると、2030年には米国の約1,210万人が心房細動を患うと予想されています。したがって、人口における乳がんと心臓病の負担の増加により、診断検査の需要が増加すると予想されます。がんの早期発見に貢献し、市場の成長を推進します。

- さらに、この地域での新製品発売の数の増加により、製品や検査キットの入手可能性が増加し、これも予測期間中の市場の成長を促進すると予想されます。たとえば、2021年 6月にThermo Fisher Scientific Inc.は、活動性SARS-CoV-2感染を検出するための新しいCE-IVDマーク付き高速PCRコンボキット 2.0であるTaqPathを発売しました。

- また、2021年 3月にMatMaCorpは、ポリメラーゼ連鎖反応(PCR)増幅とリアルタイム蛍光検出を実行できる新しいハンドヘルドデバイス MYリアルタイムアナライザー(MYRTA)を発売しました。したがって、人口におけるがんや心臓病の高い負担、企業活動の増加、地域内の病理学研究所の数の増加などの前述の要因により、調査対象の市場は予測期間中に成長すると予想されます。

病理デバイス業界の概要

病理デバイス市場は、多数の世界企業とローカル企業が市場に存在するため、細分化されています。両社は、市場での地位を維持するために、製品の発売、契約、コラボレーションなどのさまざまなビジネス戦略の採用に注力しています。市場の主要企業としては、Abbott Laboratories、Becton, Dickinson and Company、Ortho-Clinical Diagnostics、F. Hoffmann-La Roche AG、Danaher Corporation、Bio-Rad Laboratoriesなどが挙げられます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 慢性疾患および感染症の罹患率の増加

- 病理デバイスにおける技術の進歩

- 新興諸国のヘルスケアインフラへの投資が増加

- 市場抑制要因

- デバイスのコストが高い

- 厳しい規制と熟練した専門家の不足

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 技術別

- 臨床化学

- 免疫測定技術

- 微生物学

- 分子診断学

- その他の技術

- 用途別

- 創薬と開発

- 病気の診断

- 法医学診断

- その他の用途

- エンドユーザー別

- 製薬会社

- 病院および診断研究所

- その他のエンドユーザー

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東およびアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Abbott Laboratories

- Becton, Dickinson and Company

- Bio-Rad Laboratories

- Beckman Coulter Inc.

- Definiens

- Hamamatsu Photonics

- Mikroscan Technologies

- Ortho-Clinical Diagnostics

- F. Hoffmann-La Roche AG

- Thermo Fisher Scientific

- Danaher Corporation

- Siemens Healthineers

第7章 市場機会と将来の動向

The Pathology Devices Market size is estimated at USD 6.18 billion in 2024, and is expected to reach USD 8.32 billion by 2029, growing at a CAGR of 6.12% during the forecast period (2024-2029).

Key Highlights

- The COVID-19 pandemic had a huge impact on healthcare systems around the world and caused many healthcare facilities to stop providing routine care and pathological testing, putting patients with chronic conditions, including cancer and cardiovascular disorders, at severe risk. For instance, according to an article published in International Medical Journal in January 2022, it was observed that the ratio of the number of pathology tests pre-lockdown and post-lockdown versus baseline period decreased from 1.02 to 0.53, respectively.

- However, the increased coronavirus cases among the population have increased the demand for pathological tests. For instance, as per an article published in Frontiers in Pathology in March 2022, it was found that the number of molecular microbiology tests was more than three times higher during the lockdown period. This has increased the company's focus on developing innovative pathological test kits and devices. Thus, the studied market is expected to grow and regain its full potential in the coming years.

- The increasing prevalence and burden of Alzheimer's disease, autoimmune diseases, cancer, and others around the world are driving the need for effective and advanced diagnostic tests, hence propelling the market growth. For instance, according to the 2022 statistics published by Alzheimer's Association, an estimated 6.5 million Americans age 65 and older were living with Alzheimer's dementia in 2022, and this number is projected to reach 13 million by 2050. Thus, the expected increase in the number of people suffering from Alzheimer's disease is anticipated to fuel the demand for pathology devices that helps physicians in early identifying the disease-causing dementia symptoms, thereby propelling the market growth.

- Additionally, as per the 2023 statistics published by ACS, about 24,810 malignant tumors of the brain or spinal cord (14,280 in males and 10,530 in females) are expected to be diagnosed in the United States in 2023. Thus, the high burden of brain or spinal cord tumors is anticipated to fuel the demand for radionuclide bone scintigraphy (bone scan) for detecting spinal pathologies, hence bolstering the market growth. Moreover, the rising company focus on developing technologically advanced pathological kits and devices is also contributing to the market growth. For instance, in April 2022, Sysmex Europe launched a new three-part differential system, XQ-320 XQ-Series Automated Hematology Analyzer, a robust device that brings excellence in quality to a diverse range of clinical laboratory environments with reliable technology and a new level of usability.

- Therefore, owing to the factors such as the high burden of chronic and infectious diseases and new product launches, the studied market is expected to grow over the forecast period. However, the high cost of devices and stringent regulations, as well as the lack of skilled professionals, are likely to impede the growth of pathological devices over the forecast period.

Pathology Devices Market Trends

Molecular Diagnostics Segment is Expected to Hold Significant Market Share Over the Forecast Period

- Molecular diagnostic devices are used to analyze biological markers in the genome and proteome to detect pathogens or mutations. Based on the technology, molecular diagnostic devices can be segmented into chips and microarrays, mass spectroscopy, next-generation sequencing (NGS), polymerase chain reaction (PCR)-based methods, cytogenetics, and molecular imaging. Factors such as large outbreaks of bacterial and viral epidemics, increasing demand for point-of-care diagnostics, and rapidly evolving technology are driving the growth of the molecular diagnostics segment.

- The growing burden of cancer, cardiovascular diseases, brain tumors, and others is the key factor driving the segment's growth. For instance, according to the statistics published by the British Heart Foundation, in January 2022, more than 7.6 million people were living with cardiovascular diseases in the United Kingdom in 2021.

- Also, as per 2022 statistics published by the National Brain Tumor Society, approximately 88,970 people were diagnosed with a primary brain tumor in the United States in 2022. Thus, the high prevalence of heart diseases and brain tumors among the population is anticipated to propel the demand for molecular diagnosis, which improves diagnosis accuracy, allows for predictive prognosis, and enables target identification. This is expected to fuel the segment growth over the forecast period.

- Furthermore, the increasing company focus on developing technologically advanced products in molecular diagnostics and rising new product launches contributes to market growth. For instance, in March 2022, Mylab Discovery Solutions launched an entire range of routine diagnostic kits and devices, for immunology, biochemistry, and hematology, in conventional and point-of-care formats. This product line expansion assists the labs in using the company's devices and reagent kits to do all routine tests such as liver panels, cardiac profiles, urine panels, hormone panels, fever panels, kidney function tests, cancer markers, and other tests.

- Therefore, owing to the factors such as the high burden of heart diseases and brain tumors, growing demand for precision medicine as well as rising product launches, the studied segment is expected to grow over the forecast period.

North America is Expected to Have the Significant Market Share Over the Forecast Period

- North America is expected to hold a significant market share in the pathology devices market, owing to the rising prevalence of infectious and chronic diseases, better healthcare infrastructure, and the technological advancements of pathological devices.

- The increasing number of chronic and infectious diseases in the region increases the demand for early detection and diagnosis of the condition, which in turn is anticipated to fuel the demand for pathological testing, thereby boosting the market growth. For instance, according to 2023 statistics published by ACS, about 1,958,310 new cancer cases are projected to be diagnosed in the United States in 2023.

- In addition, from the same source, 1,63,020 new cases of colorectal cancer, followed by 2,38,340 cases of lung and bronchus, 297,790 breast cancer, and 288,300 prostate cancer, are expected to be diagnosed in the United States in 2023. Also, as per 2022 data published by CDC, about 12.1 million people in the United States are expected to have atrial fibrillation in 2030. Thus, the rising burden of breast cancer and heart disease cases among the population is anticipated to increase the demand for diagnostic tests for the early detection of cancer, thereby propelling market growth.

- Furthermore, the increasing number of new product launches in the region increases the availability of products and test kits, which is also expected to boost market growth over the forecast period. For instance, in June 2021, Thermo Fisher Scientific Inc. launched TaqPath, a new CE-IVD-marked fast PCR combo kit 2.0, to detect active SARS-CoV-2 infection.

- Also, in March 2021, MatMaCorp launched a new handheld device, MY Real-Time Analyzer (MYRTA), which can carry out polymerase chain reaction (PCR) amplification and real-time fluorescent detection. Therefore, due to the aforementioned factors, such as the high burden of cancer and heart disease among the population, increasing company activities, and the growing number of pathological labs in the region, the studied market is expected to grow over the forecast period.

Pathology Devices Industry Overview

The pathology devices market is fragmented as numerous global and local companies are present in the market. The companies are focusing on adopting various business strategies, such as product launches, agreements, and collaborations, to withhold their market position. Some of the key players in the market are Abbott Laboratories, Becton, Dickinson and Company, Ortho-Clinical Diagnostics, F. Hoffmann-La Roche AG, Danaher Corporation, and Bio-Rad Laboratories, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Chronic and Infectious Diseases

- 4.2.2 Technological Advancements in Pathology Devices

- 4.2.3 Increasing Investment in Healthcare Infrastructure in Developing Countries

- 4.3 Market Restraints

- 4.3.1 High Cost of Devices

- 4.3.2 Stringent Regulations and Lack of Skilled Professionals

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Technology

- 5.1.1 Clinical Chemistry

- 5.1.2 Immunoassays Technology

- 5.1.3 Microbiology

- 5.1.4 Molecular Diagnostics

- 5.1.5 Other Technologies

- 5.2 By Application

- 5.2.1 Drug Discovery and Development

- 5.2.2 Disease Diagnostics

- 5.2.3 Forensic Diagnostics

- 5.2.4 Other Applications

- 5.3 By End-User

- 5.3.1 Pharmaceutical Companies

- 5.3.2 Hospitals and Diagnostic Laboratories

- 5.3.3 Other End-Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abbott Laboratories

- 6.1.2 Becton, Dickinson and Company

- 6.1.3 Bio-Rad Laboratories

- 6.1.4 Beckman Coulter Inc.

- 6.1.5 Definiens

- 6.1.6 Hamamatsu Photonics

- 6.1.7 Mikroscan Technologies

- 6.1.8 Ortho-Clinical Diagnostics

- 6.1.9 F. Hoffmann-La Roche AG

- 6.1.10 Thermo Fisher Scientific

- 6.1.11 Danaher Corporation

- 6.1.12 Siemens Healthineers