|

市場調査レポート

商品コード

1687224

合成ガス:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Syngas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 合成ガス:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

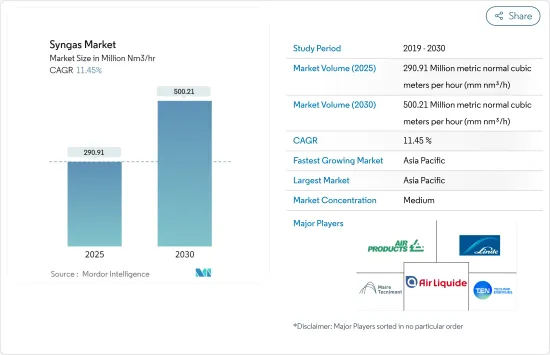

合成ガス市場規模は、2025年に2億9,091万メートル毎時と推定・予測され、2030年には5億21万メートル毎時に達すると予測され、予測期間中(2025~2030年)のCAGRは11.45%です。

COVID-19は2020年の市場にマイナスの影響を与えました。しかし、2021年には主要用途での運転が再開されるため、予測期間中に市場は大幅に回復するとみられます。

主要ハイライト

- 電力・化学産業からの合成ガス需要の増加、環境意識の高まりと再生可能燃料利用に関する政府規制、肥料用水素需要の増加が市場の成長を牽引すると予想されます。

- 逆に、合成ガス製造プラントのセットアップには高額な設備投資と資金が必要となります。この要因は市場の成長を妨げると予想されます。

- 地下石炭ガス化技術の開発は、将来的には機会になると考えられます。

- アジア太平洋は世界全体で市場を独占し、最大の消費量を誇り、市場で大きなシェアを占めています。

合成ガス市場の動向

市場を独占するアンモニアセグメント

- アンモニアは、メタンを主原料とする合成ガスから製造されます。蒸気とメタンを触媒に通し、第一段階で二酸化炭素と水素を生成します。第2段階では空気が加えられ、二酸化炭素、水素、窒素、蒸気が生成されます。

- 次の段階では、二酸化炭素が除去され、混合物が乾燥され、先に圧縮・冷却された窒素と水素が触媒の存在下で結合され、アンモニアが生成されます。最後のプロセスで生成された残りの合成ガスは、再び反応器に送られます。

- アンモニアは、世界の窒素産業の基本コンポーネントです。窒素肥料用アンモニアの消費は、世界のアンモニア市場の80%以上を占めています。

- アンモニアは、爆薬を製造するための硝酸アンモニウムの製造にも使用されます。また、アクリル繊維やプラスチック用のアクリロニトリル、ナイロン66用のヘキサメチレンジアミン、ナイロン6用のカプロラクタム、ポリウレタンやヒドラジン用のイソシアネート、各種アミンやニトリルの製造にも使用されます。

- 米国地質調査所(United States Geological 2022)によると、2021年の世界のアンモニア生産量は1億5,000万トンと推定されています。

- 中国がアンモニアの主要生産国で、ロシア、米国、インドがこれに続きます。2021年の中国のアンモニア生産量は3,900万トン。

- 米国のアンモニア生産量は1,400万トンと推定されます。16社が2021年に米国内16州の35工場で生産しています。米国全体のアンモニア生産能力の約60%は、天然ガスの埋蔵量が多いルイジアナ州、オクラホマ州、テキサス州にありました。

- 米国地質調査所によると、今後4年間に世界のアンモニア生産能力は4%増加すると推定されています。生産能力の増加は、アフリカ、東欧、南アジアで見込まれています。

- したがって、アンモニア産業の急成長に伴い、合成ガスの需要も予測期間中に増加すると予想されます。

アジア太平洋が市場需要を牽引

- アジア太平洋は、世界で最も経済成長著しい中国やインドなどの国々からの需要が増加しており、世界市場シェアを独占しています。さらに、各国は再生可能エネルギーへの移行を進めており、これが市場成長の引き金となっています。

- 中国では、エアープロダクツは、中国のフフホトにある九泰新材料の高価値モノエチレングリコールプロジェクト向けに合成ガスを供給する長期オンサイト契約を獲得しました。プロジェクトは2023年に開始される予定です。この施設/プラントは毎時50万Nm3以上の合成ガスを生産するよう設計されており、5基のガス化炉、合成ガスの精製・処理を行う毎時約10万Nm3の空気分離装置(ASU)2基、関連インフラと公益事業で構成されます。

- 中国江蘇省のXuwei National Petrochemical Parkにある石炭から合成ガスへの処理施設における画期的な進歩は、Debang Xinghua Technology(Jiangsu Debang Chemical Industrial Group(「Debang Group」)の子会社)とのエアプロダクツ80%/20%の合弁事業で明らかになりました。

- インドは高灰分のインド産石炭をメタノールに転換する技術を開発し、ハイデラバードに最初のパイロットプラントを設立しました。石炭をメタノールに変換するプロセスは、石炭を合成(シンガス)ガスに変換し、さらに処理することで構成される可能性があります。

- インドのコングロマリット、Reliance Industries Limitedも、グリーン水素の価格が下がるまで、ジャムナガルコンプレックスで合成ガスをブルー水素に転換する計画を発表しました。このような要因は、調査された市場にプラスの影響を与える可能性があります。

- アンモニアは主に肥料生産に使用されます。インド政府は、2021~22年度の肥料予算として107億5,000万米ドルを計上しています。このことが、予測期間中のアンモニア生産用合成ガス市場を牽引すると予想されます。

- したがって、上記の要因は今後の市場に大きな影響を与えると予想されます。

合成ガス産業概要

合成ガス市場は、その性質上、部分的にセグメント化されています。市場の主要企業(順不同)には、Air Liquide SA、Linde PLC、Air Products and Chemicals Inc.、Maire Tecnimont SpA、Technip Energies NVなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 電力と化学産業における需要の高まり

- 環境意識の高まりと再生可能燃料利用に関する政府規制

- 肥料用水素需要の増加

- 抑制要因

- 高い設備投資と資金調達

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 原料

- ペットコークス

- 石炭

- 天然ガス

- その他の原料タイプ

- 技術

- 水蒸気改質

- ガス化

- ガス化炉タイプ

- 固定床

- エントレインフロー

- 流動床

- 用途

- メタノール

- アンモニア

- 水素

- 液体燃料

- 直接還元鉄

- 合成天然ガス

- 電気

- その他

- 地域

- アジア太平洋

- 中国

- インド

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- トリニダード・トバゴ

- 欧州

- ロシア

- その他の欧州

- 南米

- ベネズエラ

- ブラジル

- その他の南米

- 中東・アフリカ

- サウジアラビア

- カタール

- 南アフリカ

- イラン

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- A.H.T Syngas Technology NV

- Air Liquide

- Air Products and Chemicals Inc.

- Airpower Technologies Limited

- John Wood Group PLC

- KBR Inc.

- Linde PLC

- Maire Tecnimont Spa

- Sasol

- Shell PLC

- Technip Energies NV

- Topsoe AS

第7章 市場機会と今後の動向

- 地下石炭ガス化技術の開発

The Syngas Market size is estimated at 290.91 million metric normal cubic meters per hour (mm nm3/h) in 2025, and is expected to reach 500.21 million metric normal cubic meters per hour (mm nm3/h) by 2030, at a CAGR of 11.45% during the forecast period (2025-2030).

COVID-19 negatively impacted the market in 2020. However, with the resumption of operations in major applications in 2021, the market is expected to recover significantly during the forecast period.

Key Highlights

- The growing demand for syngas from the electricity and chemical industry, increasing environmental awareness and government regulations on renewable fuel use, and increasing hydrogen demand for fertilizers are expected to drive the growth of the market.

- Conversely, syngas production plant setup requires high capital investment and funding. This factor is expected to hinder the market's growth.

- The development of underground coal gasification technology is likely to act as an opportunity in the future.

- Asia-Pacific dominated the market across the world, with the largest consumption, holding a major share in the market.

Syngas Market Trends

Ammonia Segment to Dominate the Market

- Ammonia is produced from syngas with methane as the main feedstock. Steam and methane are passed through a catalyst to produce carbon dioxide and hydrogen in the first phase. In the second phase, air is added, forming carbon dioxide, hydrogen, nitrogen, and steam.

- In the next step, carbon dioxide is removed, the mixture is dried, and nitrogen and hydrogen, which were previously compressed and cooled, are combined in the presence of a catalyst to form ammonia. The remaining syngas formed in the penultimate step is sent back to the reactor.

- Ammonia is the basic building block of the global nitrogen industry. Consumption of ammonia for nitrogen fertilizers accounts for over 80% of the global ammonia market.

- Ammonia is used to produce ammonium nitrates to make explosives. It is also used in producing acrylonitrile for acrylic fibers and plastics, hexamethylenediamine for nylon 66, caprolactam for nylon 6, isocyanates for polyurethanes and hydrazine, and various amines and nitriles.

- According to the United States Geological 2022, global ammonia production is estimated to be 150 million metric tons in 2021.

- China is the major producer of ammonia, followed by Russia, the United States, and India. In 2021, China's ammonia production was 39 million metric tons.

- Ammonia production in the United States was estimated to be 14 million metric tons. Sixteen companies produced it at 35 plants in 16 States in the United States in 2021. About 60% of the total US ammonia production capacity was in Louisiana, Oklahoma, and Texas because of their large natural gas reserves.

- According to the US Geological Survey, it is estimated that global ammonia capacity is expected to increase by 4% during the next four years. Capacity additions are expected in Africa, Eastern Europe, and South Asia.

- Therefore, with the rapid growth of the ammonia industry, the demand for syngas is expected to increase during the forecast period.

Asia-Pacific Region to Drive the Market Demand

- Asia-Pacific dominated the global market share, with rising demand from the countries such as China and India, which are among the fastest-growing economies across the world. Moreover, countries are moving toward renewable energy sources, which triggers market growth.

- In China, Air Products was awarded a long-term onsite contract to supply syngas to Jiutai New Material Co. Ltd for its high-value mono-ethylene glycol project in Hohhot, China. The project is expected to start in 2023. The facility/plant is designed to produce over 500,000 Nm3/hr of syngas, comprised of five gasifiers, two approximately 100,000 Nm3/hr air separation units (ASU) with syngas purification and processing, and associated infrastructure and utilities.

- A breakthrough in the coal-to-syngas processing facility in Xuwei National Petrochemical Park, Lianyungang City, Jiangsu Province, China, is evident in the 80% Air Products/20% joint venture with Debang Xinghua Technology Co. Ltd (a subsidiary of Jiangsu Debang Chemical Industrial Group Co. Ltd ('Debang Group')).

- India developed a technology to convert high ash Indian coal to methanol and established its first pilot plant in Hyderabad. The process of converting coal into methanol may consist of converting coal to synthesis (syngas) gas, and further process, thus adding to the syn gas market in the country.

- Indian conglomerate Reliance Industries Limited also announced its plans to turn syngas into blue hydrogen in its Jamnagar complex until the pricing of green hydrogen comes down. Such factors may positively affect the market studied.

- Ammonia is majorly used in fertilizer production. The Indian government has also provided a budget allocation for fertilizers in FY 2021-22 of USD 10.75 billion. This is expected to drive the syn gas market for ammonia production during the forecast period.

- Therefore, the abovementioned factors are expected to impact the market in the future significantly.

Syngas Industry Overview

The syngas market is partly fragmented in nature. Some of the key players in the market (not in particular order) include Air Liquide SA, Linde PLC, Air Products and Chemicals Inc., Maire Tecnimont SpA, and Technip Energies NV, among other companies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Report

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand in the Electricity and Chemical Industry

- 4.1.2 Increasing Environmental Awareness and Government Regulations on the Use of Renewable Fuel

- 4.1.3 Increasing Hydrogen Demand for Fertilizers

- 4.2 Restraints

- 4.2.1 High Capital Investment and Funding

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Feedstock

- 5.1.1 Pet Coke

- 5.1.2 Coal

- 5.1.3 Natural Gas

- 5.1.4 Other Feedstock Types

- 5.2 Technology

- 5.2.1 Steam Reforming

- 5.2.2 Gasification

- 5.3 Gasifier Type

- 5.3.1 Fixed Bed

- 5.3.2 Entrained Flow

- 5.3.3 Fluidized Bed

- 5.4 Application

- 5.4.1 Methanol

- 5.4.2 Ammonia

- 5.4.3 Hydrogen

- 5.4.4 Liquid Fuels

- 5.4.5 Direct Reduced Iron

- 5.4.6 Synthetic Natural Gas

- 5.4.7 Electricity

- 5.4.8 Other Applications

- 5.5 Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Trinidad and Tobago

- 5.5.3 Europe

- 5.5.3.1 Russia

- 5.5.3.2 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Venezuela

- 5.5.4.2 Brazil

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 Qatar

- 5.5.5.3 South Africa

- 5.5.5.4 Iran

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 A.H.T Syngas Technology NV

- 6.4.2 Air Liquide

- 6.4.3 Air Products and Chemicals Inc.

- 6.4.4 Airpower Technologies Limited

- 6.4.5 John Wood Group PLC

- 6.4.6 KBR Inc.

- 6.4.7 Linde PLC

- 6.4.8 Maire Tecnimont Spa

- 6.4.9 Sasol

- 6.4.10 Shell PLC

- 6.4.11 Technip Energies NV

- 6.4.12 Topsoe AS

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Underground Coal Gasification Technology