|

市場調査レポート

商品コード

1444132

飼料カロテノイド:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Feed Carotenoids - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 飼料カロテノイド:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 126 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

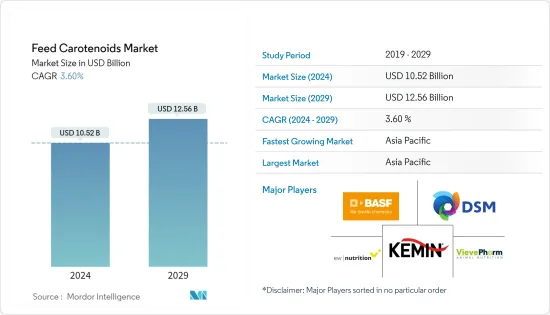

飼料カロテノイド市場規模は、2024年に105億2,000万米ドルと推定され、2029年までに125億6,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に3.60%のCAGRで成長します。

世界レベルで観察されたサプライチェーンの混乱により、市場はCOVID-19のパンデミックによって中程度の影響を受けると予想されています。さまざまな政府が国際港の部分閉鎖を命令し、飼料カロテノイドのサプライチェーンの混乱を促進しています。一部の生産施設の閉鎖に加え、病気の蔓延により世界中の家畜生産と飼料製造業が混乱しました。したがって、COVID-19のパンデミックの継続的な影響は原材料の供給にマイナスの影響を及ぼしていると推測されており、今後数年間は価格が高騰する可能性が高いです。

長期的には、水産養殖産業の成長と魚介類の消費量の増加により、カロテノイド市場の成長が促進されると予想されます。アスタキサンチンは、魚の筋肉、主にサケの色素沈着に使用される主要なカロテノイドです。さまざまな研究により、水生動物におけるカロテノイドの生物学的および栄養学的役割、ならびにカロテノイドの輸送と保持、および最終的な肉の色素沈着に対する生物的および非生物的要因の影響が文書化されています。

アジア太平洋地域は世界有数の配合飼料生産・消費地域であるため、飼料カロテノイド市場に直接的な影響を与えています。この地域における工業用家畜の生産規模の拡大は、この地域の主要経済国の飼料生産能力の増加に大きく貢献しています。アジアにおける水牛と牛、家禽、羊、ヤギの食肉総生産量は、2018年の18,748.3、49,151.2、916万7,700トンと比較して、2020年にはそれぞれ19,208.3、50,689.1、972万200トンに達しました。したがって、アジアにおける畜産物の需要の高まりは、今後数年間で市場の成長を促進すると予想されます。

飼料カロテノイド市場動向

水産養殖用飼料としての使用量の増加

カロテノイドのさまざまな生物学的特性により、水産養殖飼料の添加物としての使用が増加しています。カロテノイドは、サケ、マス、アカダイ、エビやロブスターなどの貝類の飼料に広く使用されています。カロテノイドは水産養殖種の幼生段階で必須であり、カロテノイドを含む生餌で飼育される魚の幼生は生存率を劇的に高めます。 2021年末までに、世界の魚やその他の水産養殖消費量のほぼ20%が、野生の魚ではなく養殖によるものになると推定されています。

世界の水産養殖生産の増加は飼料の需要の増加をもたらし、それによってカロテノイド市場の成長が促進されています。水産養殖飼料は2019年に4%増加したと報告されています(2020 Alltech Global Feed Survey)。アジア太平洋市場はトン当たりの成長が最も大きく、前年比でさらに150万トン増加し、3,000万トン近くに達しました。 2019年には、中国、バングラデシュ、ベトナム、インド、インドネシアがこの地域の水産飼料の主要生産国でした。中国だけでも世界の水産飼料生産に1,650万トン貢献しています。これは、水産養殖飼料カロテノイド市場の発展の機会が拡大していることを示しています。養殖場における最適な栄養の要件に対する水産養殖農家の意識の高まりは、飼料カロテノイド市場の水産養殖部門の成長をさらに促進すると予想されます。

アジア太平洋が世界市場をリード

アジア太平洋は中国が独占する世界最大の水産養殖市場であり、飼料添加物としてのカロテノイドの最大の消費国です。ベトナム、インドネシア、インドは、新しい科学的養殖方法の採用と魚やその他の畜産物の消費量の増加により、将来的に大きな成長が見込まれる主要市場です。アジア諸国での輸出の可能性を高めるという目標も飼料需要を刺激し、カロテノイド市場の成長を促進しています。インドネシア政府は、水産養殖の輸出を促進するため、2022年末までに数十の村に養殖場を持つネットワークを構築する計画を立てています。

現在、主な輸出種には、アジアンタイガーシュリンプ(Penaeus monodon)やホワイトレッグシュリンプ(Litopenaeus vannamei)が含まれます。さらに、この地域の動物飼育者は、飼料に含まれる天然添加物の重要性を認識し始めています。飼料添加物では合成カロテノイドが天然カロテノイドに置き換えられ、人間や動物、さらには環境への健康への影響の問題に取り組んでいます。合成カロテノイドは250~2,000米ドル/kgで販売されますが、天然カロテノイドは350~7,500米ドル/kgで販売されます。したがって、天然カロテノイドへの投資は、予測期間中にこの地域の市場を押し上げると予想されます。

飼料カロテノイド業界の概要

調査された飼料カロテノイド市場は統合されており、世界の主要企業が重要な市場シェアを占めています。 BASF SE、Kemin Industries、DSM Animal Nutrition、EW Nutrition、VievePharm Animal Nutrition BV、Allied Biotech Corporationが、2021年の総収益に基づく世界の飼料カロテノイド市場の80%以上を占める主要企業です。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- タイプ

- ベータカロチン

- リコピン

- ルテイン

- アスタキサンチン

- カンタキサンチン

- その他のタイプ

- 動物の種類

- 反芻動物

- 家禽

- 豚

- 水産養殖

- 他の種類の動物

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- ロシア

- イタリア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東とアフリカ

- サウジアラビア

- 南アフリカ

- その他中東およびアフリカ

- 北米

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- BASF SE

- Thoroughbred Remedies Manufacturing

- DSM Animal Nutrition

- Kemin Industries

- Synthite Industries Ltd

- Nutrex NV

- VievePharm Animal Nutrition BV

- Impextraco

- Allied Biotech Corporation

- Vitafor

- EW Nutrition

- Avivagen

- Innovad

第7章 市場機会と将来の動向

第8章 COVID-19の市場への影響

The Feed Carotenoids Market size is estimated at USD 10.52 billion in 2024, and is expected to reach USD 12.56 billion by 2029, growing at a CAGR of 3.60% during the forecast period (2024-2029).

The market is anticipated to be moderately impacted by the COVID-19 pandemic owing to the supply chain disruptions observed at the global level. Various governments have ordered the partial closure of international ports, promoting disruptions in the feed carotenoids supply chain. In addition to the closure of some production facilities, the spread of the disease disrupted the livestock production and feed manufacturing industries across the world. Therefore, the ongoing impact of the COVID-19 pandemic is speculated to have a negative impact on the raw material supply, which is likely to spike the prices for the next couple of years.

Over the long term, the growth of the aquaculture industry and increased consumption of seafood are anticipated to boost the growth of the carotenoids market. Astaxanthin is the major carotenoid used for the pigmentation of fish muscle, mainly salmons. Various studies have documented the biological and nutritional role of carotenoids in aquatic animals, along with the effect of biotic and abiotic factors on carotenoid transport and retention and final flesh pigmentation.

The Asia-Pacific region is the leading compound feed producing and consuming region in the world, thereby inflicting a direct impact on the feed carotenoids market. The increased scale of industrial livestock production in the region has significantly contributed to an increase in feed production capacities in major economies across the region. The total meat production for buffalo and cattle, poultry, sheep, and goat respectively reached 19,208.3, 50,689.1, and 9,720.2 thousand metric tons in 2020 as compared to 18,748.3, 49,151.2, and 9,167.7 thousand metric tons in 2018 in Asia. Hence, the growing demand for livestock products in Asia is expected to boost the market growth in the coming years.

Feed Carotenoids Market Trends

Increasing Usage in Aquaculture Feed

The various biological properties of carotenoids have led to their increased usage as an additive in aquaculture feed. Carotenoids are extensively used in the feed for salmon, trout and red porgy, and shellfish, like shrimp and lobster. Carotenoids are essential at the larval stage of aquaculture species, and fish larvae dramatically increase their survival rate when reared on live feeds containing carotenoids. It has been estimated that by the end of 2021, almost 20% of the global fish and other aquaculture consumption will be from cultured aquaculture, as opposed to the wild collection.

The growth in global aquaculture production has led to the increased demand for feed, thereby promoting the growth of the carotenoids market. Aquaculture feed reportedly grew by 4% in 2019(2020 Alltech Global Feed Survey). The Asia-Pacific market grew the most per metric ton, producing an additional 1.5 million metric ton over the previous year, and reached nearly 30 million metric ton. In 2019, China, Bangladesh, Vietnam, India, and Indonesia were the major producers of aquafeed in the region. China alone contributed 16.5 million metric ton to the global aquafeed production. This presents a growing opportunity for the development of the aquaculture feed carotenoids market. The increasing awareness of aquaculture farmers about the requirement for optimum nutrition in their farms is expected to further provide a fillip to the growth of the aquaculture segment of the feed carotenoids market.

Asia-Pacific Leads the Global Market

Asia-Pacific is the largest consumer of carotenoids as feed additives, as it is the largest market for aquaculture across the world, dominated by China. Vietnam, Indonesia, and India are the key markets expected to witness significant growth in the future due to the adoption of new scientific methods for farming and the increasing consumption of fish and other livestock products. The aim to increase the export potential in the Asian countries is also fuelling the feed demand, hence boosting the growth of the carotenoids market. In Indonesia, the government plans to have a network of dozens of villages with aquaculture farms by the end of 2022 to boost its aquaculture exports.

At present, some of its top export species include Asian tiger shrimp (Penaeus monodon) and whiteleg shrimp (Litopenaeus vannamei). Additionally, the animal rearers in the region are becoming aware of the importance of natural additives in the feed. Synthetic carotenoids are being replaced with natural ones in feed additives, addressing the issue of health impact on humans and animals, as well as the environment. Synthetic carotenoids sell for USD 250-2,000/kg, whereas natural carotenoids sell for between USD 350-7,500/kg. Hence, the investment in natural carotenoids is expected to boost the market in the region during the forecast period.

Feed Carotenoids Industry Overview

The feed carotenoid market studied is consolidated, with leading global players occupying significant market shares. BASF SE, Kemin Industries, DSM Animal Nutrition, EW Nutrition, VievePharm Animal Nutrition BV, and Allied Biotech Corporation are the major players accounting for over 80% of the global feed carotenoids market based on overall revenue in 2021.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Beta-Carotene

- 5.1.2 Lycopene

- 5.1.3 Lutein

- 5.1.4 Astaxanthin

- 5.1.5 Canthaxanthin

- 5.1.6 Other Types

- 5.2 Animal Type

- 5.2.1 Ruminant

- 5.2.2 Poultry

- 5.2.3 Swine

- 5.2.4 Aquaculture

- 5.2.5 Other Animal Types

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Spain

- 5.3.2.5 Russia

- 5.3.2.6 Italy

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 BASF SE

- 6.3.2 Thoroughbred Remedies Manufacturing

- 6.3.3 DSM Animal Nutrition

- 6.3.4 Kemin Industries

- 6.3.5 Synthite Industries Ltd

- 6.3.6 Nutrex NV

- 6.3.7 VievePharm Animal Nutrition BV

- 6.3.8 Impextraco

- 6.3.9 Allied Biotech Corporation

- 6.3.10 Vitafor

- 6.3.11 EW Nutrition

- 6.3.12 Avivagen

- 6.3.13 Innovad