|

市場調査レポート

商品コード

1851349

モジュラー建設:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Modular Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| モジュラー建設:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月28日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

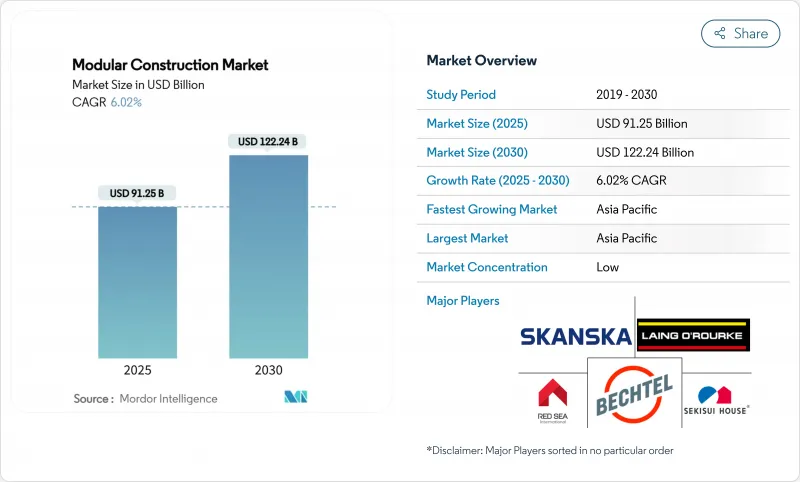

モジュラー建設市場規模は2025年に912億5,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは6.02%で、2030年には1,222億4,000万米ドルに達すると予測されます。

労働力不足の深刻化、支援的な規制、工場建設住宅プロジェクトの目に見える成功によって、モジュール工法はニッチなソリューションから多くの地域で主要な建設オプションへと位置づけを変えつつあります。アジア太平洋地域は、急速な都市化、長期にわたる手頃な価格の住宅供給義務、国内および輸出プロジェクトにモジュールを供給する厚みのある製造基盤を背景に、47%の売上シェアを占めています。恒久的なソリューションがモジュラー建設市場の67%を占めているが、これは工場で組み立てられた建物が、現場で建てられた構造と同等の耐久性と美観の期待に応えられることが広く受け入れられていることを反映しています。鉄骨フレームワークは、構造強度、寸法安定性、および確立されたサプライ・チェーンが支持され、依然として84%のシェアを占め、生産の基幹となっています。施設所有者、特に教育機関やヘルスケア事業者は、オフサイトでの製作により混乱を最小限に抑え、入居を早め、プロジェクト全体のスケジュールを短縮できるため、需要をリードしています。

世界のモジュラー建設市場の動向と洞察

先進国経済のモジュール式ソリューションの採用

北米と西欧では、高い世帯需要と建設労働力の減少が衝突しています。スウェーデンでは、戸建住宅の84%が工場ラインから供給されており、政策立案者が研究すべき成熟した基準点を確立しています。日本の建設業者も高水準の採用率を維持しています。一方、米国は住宅生産量の4%未満にとどまっているもの、ヘルスケア、教育、集合住宅プロジェクトで力強い勢いを記録しています。スカンジナビアと日本の成功事例の知名度は、投資家にとって、モジュラー建設の市場リスクは管理可能であるという安心感を与えています。オーストラリアやカナダの建設業者は、ソーシャルハウジングのパイプラインに同様のモデルを導入し、専門知識を広め、先行者の不確実性を低減するグローバルな学習ループを強化しています。

政府の取り組みが市場成長を促進

公共機関は、住宅やインフラ計画にモジュール式の要件を盛り込むようになってきています。クイーンズランド州の2024~25年度予算では、28億豪ドル(18億5,000万米ドル)を計上し、従来型の長期的な建設スケジュールに対し、3ヵ月で現地に設置できるモジュール式住宅600戸を供給することにしました。米国住宅都市開発省は、2024年に90の製造住宅基準を新規または改訂し、30年間ほとんど固定されていた基準を近代化しました。このような措置は、認可を合理化し、金融機関を安心させ、仕様決定者にモジュール方式を最初に評価するよう促し、モジュラー建設市場を拡大します。

高額な初期投資による市場参入障壁

専用工場、自動化ライン、認証された品質管理システムを立ち上げるには、収益が上がるまでに多額の資本支出が必要となります。Katerra社を含め、資金力のある新興企業のいくつかは、製品市場適合性が明確であったにもかかわらず、資本が消費されるよりも事業の立ち上げが遅かったために失敗しました。エネルギーコストの上昇とインフレは、キャッシュフローへのストレスを増大させる。既存の請負業者は、リスクを共有するジョイントベンチャーを通じて対応することが多いが、基本的なハードルは依然として残っています。新規参入企業は、固定資産を償却するためにほぼ即座に規模を拡大する必要があり、実行可能な新規競合企業のプールを制限し、モジュラー建設市場の全体的な成長を遅らせています。

セグメント分析

2024年の売上高の67%を占めるのは、恒久的モジュール形式です。その中で、ブルックリンの147 St.Felixのような高層住宅プロジェクトは、「箱型」という長引くイメージを払拭する建築的柔軟性を示しています。常設ソリューションのモジュラー建設市場規模は、機械、電気、配管システムを反復可能な筐体に編み込み、組み立て時の再作業を減らすデジタル設計ツールとともに拡大すると予測されます。

施設の顧客は、オフサイト製作がもたらす混乱の減少を高く評価しています。カリフォルニア・ポリテクニック州立大学のような大学では、15階建ての学生寮が通常の半分の期間で建設され、学生収入をより早く確保するのに役立っています。市場開拓者はまた、構造的完全性と耐火性に関して規格を満たすか上回る、工場で管理された品質も評価しており、モジュラー建設市場でのプレミアム評価を支えています。

スチールは、その高い強度対重量比と世界的な入手可能性により、2024年の材料量の84%を占めています。スチールベースのモジュールのモジュラー建設市場規模は、予測可能なねじれ剛性により、材料を変更することなく背の高い構成を可能にするという利点があります。保険会社は、不燃フレームに対する保険料を減額することが多く、生涯コストはスチールに有利に傾いています。

典型的な10,000ft2のプロジェクトと比較した20年間のライフサイクル研究では、総支出額はスチールモジュールが35万米ドルであるのに対し、従来の建築物は110万米ドルに達するという結果が出ており、経済的な弾力性が強調されています。クロスラミネート・ティンバーのような新しいエンジニアリング・ウッド技術は、ニッチな中層プロジェクトに浸透しつつあるが、成熟したサプライチェーンとリサイクル価値を持つスチールは、モジュラー建設市場における優位性を維持しています。

地域分析

2024年のモジュラー建設市場シェアは、アジア太平洋が47%を占めました。中国の広大な製造拠点が低コストのモジュール生産を可能にする一方、積水ハウスなど日本のパイオニア企業は高精度の工場住宅で高い評価を維持しています。オーストラリアは5年間で3億3,000万米ドルのプレハブ部材を輸入しており、堅調な国境を越えた貿易を浮き彫りにしています。政府補助金に支えられた都市化の圧力は、地域主導の継続を保証します。

北米は、2025年から2030年にかけて大きく成長する可能性を秘めています。米国は、700万戸の住宅供給ギャップの中で熟練した建設労働者の不足に直面しており、労働集約度を立地条件から切り離す工場プロセスが強くアピールしています。HUDの2024年規約大改正と保留中の連邦法は、より広範な採用を促しています。カナダの国家住宅戦略は、プレハブ式ソリューションに明確に言及しており、上級閣僚は、手頃な価格を改善するためのモジュール式供給を提唱しています。

欧州では、地域によって成熟度が異なります。スウェーデンは住宅の45%を工場で建設しており、近隣市場に実績のある技術的・商業的テンプレートを提供しています。英国は、2030年までにモジュール式住宅の普及率25%を目標としており、普及を加速させるためにリスク評価に資金を提供しています。南欧は、断片的なサプライチェーンと複雑な許認可のために遅れをとっているが、二酸化炭素削減目標の高まりと労働力不足は、モジュラー建設市場に有利に収束する可能性が高いです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 先進国からのモジュラー建設需要の増加

- 政府のモジュラー建設支援策

- 仮設/ポータブル構造物に対する需要の高まり

- プロジェクト期間の大幅短縮

- 熟練労働者不足の解決策

- 市場抑制要因

- 高い初期投資

- デザインの限界

- 地域間の規制と規範の違い

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- 建設タイプ別セグメント

- パーマネント・モジュラー

- リロケータブル・モジュラー

- 材料別セグメント

- スチール

- コンクリート

- 木材

- プラスチック

- エンドユーザー分野別セグメンテーション

- 住宅

- 商業

- 産業/施設

- サービス段階別セグメント

- 新設

- アフターメンテナンスと改装(リノベーション)

- 地域別セグメンテーション

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- 北欧諸国

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- チリ

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- 南アフリカ

- ナイジェリア

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/ランキング分析

- 企業プロファイル

- ACS Group

- Algeco UK Limited(Modulaire Group)

- Alta-Fab Structures Ltd.

- ATCO Ltd

- Balfour Beatty

- Bechtel Corporation

- Bouygues Construction

- CIMC Modular Building

- Daiwa House Industry Co. Ltd

- Fluor Corporation

- Guerdon, LLC.

- Laing O'Rourke

- Larsen & Toubro Limited

- Lendlease Corporation

- Red Sea International

- Sekisui House Ltd

- Skanska

- Stack Modular

- Wernick Group

- WillScot Holdings Corporation

- Zekelman Industries