|

|

市場調査レポート

商品コード

1441624

半導体業界:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Semiconductor Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 半導体業界:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 354 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

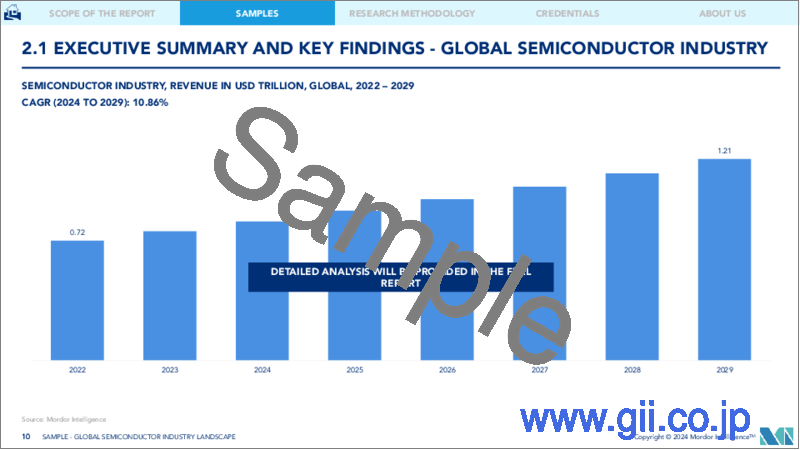

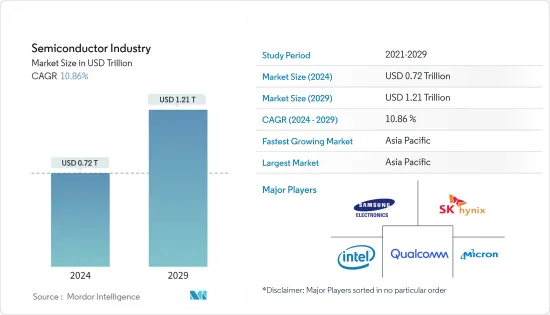

半導体業界は、2024年の7,200億米ドルから2029年までに1兆2,100億米ドルまで、予測期間(2024年から2029年)中に10.86%のCAGRで成長すると予想されています。

主なハイライト

- 半導体が現代技術の基本コンポーネントとなりつつあるため、半導体部門は急速に拡大しています。この業界の進歩と画期的な進歩は、その後のすべてのテクノロジーに直接影響を与えています。

- 半導体デバイスは、半導体材料を基盤として使用する電子部品です。この材料は、トランジスタ、ダイオード、および集積回路(IC)に見られるその他の基本的な機能ユニットを生成します。これらのデバイスは、電気をうまく伝えず、効果的な絶縁体としても機能しないという特徴があります。半導体デバイスの利点には、手頃な価格、信頼性、コンパクトなサイズが含まれます。過去数十年にわたって、さまざまなエレクトロニクスの製造におけるこれらのデバイスの利用の人気が急増しており、今後数年間でその勢いはさらに増し続けると予測されています。

- 半導体業界は、人工知能(AI)、自動運転、モノのインターネット、5Gなどの新興技術における半導体材料の需要の高まりに応えるため、予見可能な将来に大きな成長を遂げると予測されています。この成長は、主要企業間の激しい競合と研究開発(R&D)への一貫した投資によって促進されています。その結果、ベンダーは常に革新を推進し、市場での競争上の優位性を獲得する必要があります。

- 企業による電動化と自動化の普及により、半導体デバイスの市場需要は増加すると予測されています。電気自動車は、エレクトロニクスと半導体が重要なコンポーネントとして機能し、持続可能な未来に向けた動きの先頭に立っています。世界中の政府が交通部門の電化に野心的な目標を設定しており、大手自動車メーカーが電気自動車の研究開発に多額の投資を行うよう促しています。半導体はEVの中央処理装置として台頭しており、EVが最適なパフォーマンスを発揮できるようになります。その結果、電気自動車への投資の増加が半導体市場の需要を刺激すると予想されます。

- 半導体業界はより熟練した労働者を必要としています。 2030年までに、業界の需要を満たすために100万人を超える追加の熟練労働者が必要となる可能性があります。さらに、半導体業界は長いリードタイムと多額の設備投資を特徴としています。製造能力の制約と需要の変化により、サプライチェーンでの不足が生じています。これらの要因は、市場の成長に課題をもたらすと予想されます。

- この分野は新型コロナウイルス感染症(COVID-19)の影響で大きな変化を遂げ、顧客の行動、事業収益、企業運営に影響を与えています。さらに、パンデミックにより、これまで気付かなかった供給側のリスクが明らかになり、重要な部品やコンポーネントの不足が生じる可能性があります。その結果、半導体企業はレジリエンスを強化するためにサプライチェーンの再構築を積極的に進めており、こうした調整はパンデミック後の時代にも続く可能性があります。

半導体市場動向

ディスクリート半導体が半導体デバイス分野で大きな市場シェアを握る

- 高エネルギーで電力効率の高いデバイスに対する需要の高まり、ワイヤレスおよびポータブル電子製品の普及の増加、さらには電動化への移行による自動車業界でのこれらのデバイスの使用増加が、成長を推進する主な要因の一部です。セグメントの。

- ディスクリート半導体における重要な動向の1つは、効率的な電力管理です。新しいシステムアーキテクチャにより、AC-DC電源アダプタの効率が向上すると同時に、サイズとコンポーネント数が削減されます。 Power-over-Ethernet(PoE)の新しい規格により、より高い電力伝送が可能になり、コネクテッド照明などの新しいクラスのデバイスの開発が可能になります。

- スイッチング電源はパワーMOSFETの最も一般的なアプリケーションであり、MOSFETはMOS RFパワーアンプにも一般的に使用されており、モバイルネットワークがアナログからデジタルに移行できるようにするため、MOSFETは通信分野で常に重要な役割を果たしてきました。エリクソンによると、5G契約数は2022年第1四半期に7000万件増加し、約6億2000万件に達したといいます。 2022年末までにその数は10億人に達すると予測されています。このような理由により、パワー半導体の需要が刺激され、MOSFETの需要が増加し、通信分野におけるいくつかのブレークスルーにつながるでしょう。

- さらに、さまざまなディスクリート半導体の中でもIGBTの需要が高まっており、低電力コンバータに広く使用されています。自動車、その他のモータードライブ、および再生可能エネルギーシステムにおける電力変換用の最も一般的な半導体スイッチは、ディスクリート IGBTです。また、主な原動力は、自動車、家庭用電化製品、産業、ITおよび通信、ヘルスケア、航空宇宙および防衛などを含むさまざまな分野で絶縁ゲートバイポーラトランジスタ(IGBT)デバイスの使用が増加していることです。

- ディスクリート IGBTアプリケーションの大部分には、インバータ、エアコンや洗濯機などのさまざまな消費財、パーソナルコンピュータで使用されるコンポーネントであるスイッチングモード電源(SMPS)、溶接装置、電子レンジ、電気調理器、IHなどの誘導加熱装置が含まれます。ストーブなどのソフトスイッチングやストロボフラッシュ制御に。低電流アプリケーション向けにディスクリート IGBTタイプを使用するUPS、パワーコンディショナ、エアコンなどの民生用電子機器に対する需要の増加が、ディスクリート IGBT市場の成長を促進していると考えられています。ディスクリート IGBTは消費財の中で電力損失が最も低いことがわかっており、これがこのセグメントの市場成長に影響を与える重要な要素になると予想されています。

半導体材料分野で大きな市場シェアを握る製造業

- 半導体製造材料は、家庭用電化製品、ハイエンドデータセンター、自動車アプリケーション、医療機器、IoTデバイス、パワーエレクトロニクスなどに見られる高度なマイクロエレクトロニクスの重要な構成要素を形成します。このセグメントは、プロセスケミカル、フォトマスク、電子ガス、フォトレジスト付属品、スパッタリングターゲット、シリコン、その他の材料などの材料をカバーしています。

- 半導体製造材料の需要を押し上げる主な要因の1つは、電気、電子、自動車、通信業界におけるデジタル集積ICの使用の増加です。さらに、エネルギー部門への投資の増加も、ソーラーパネル、ドライブ、風力タービンや水力タービンのポンプ、エネルギー変換における保護回路などに半導体が広く応用されているため、この部門の成長にプラスに寄与すると予想されています。効率を確保し、電力損失を最小限に抑えます。たとえば、IEAによると、世界のエネルギー投資は2022年に8%増加し、2兆4,000億米ドルに達すると予想されています。さらにIRENAによると、再生可能エネルギーへの支出は着実に増加すると予想されており、市場を押し上げています。

- 幅広い材料が半導体特性を示すことができますが、一部の材料は、その特有の特性により電子デバイスの製造でより一般的に使用されます。最も一般的な半導体材料の2つは、シリコンとガリウムヒ素です。シリコンは、主にその豊富さ、低コスト、および高温での比較的安定した特性により、最も広く使用されている半導体材料です。シリコンの電気伝導率は約1000 S/mです。さらに、シリコンには十分に確立された製造インフラがあり、メーカーにとって魅力的な選択肢となっています。ただし、シリコンには他の材料に比べて電子移動度が低いなど、高速デバイスの性能が制限される可能性があるいくつかの欠点があります。

- ガリウムヒ素も人気のある半導体材料であり、その高い電子移動度とダイレクトバンドギャップが評価されています。これらの特性により、レーザーや太陽電池などのオプトエレクトロニクス用途に適しています。ただし、ガリウムヒ素はシリコンよりも高価であり、量が少ないため、その広範な採用が制限される可能性があります。ガリウムヒ素のもう1つの欠点は、ガリウムヒ素が本来、導電率0.000001 S/mの半導体ではなく半絶縁体として存在することです。

- シリコンとガリウムヒ素の他に、研究者は有望な半導体特性を備えた新しい材料を継続的に探索しています。これらの材料には、窒化アルミニウム、カーボンナノチューブ、および業界に革命を起こす可能性のあるその他の多くの材料が含まれます。これらの新興材料に対する理解が深まるにつれ、将来の半導体製造においてますます重要な役割を果たすようになるでしょう。

- さらに、プロセスケミカル市場は、低コストの手法や半導体分野での内部効率化への応用により、堅調な成長が見込まれています。半導体プロセス用化学薬品の消費は、設置された製造能力の増加と新技術によって消費される高価な化学薬品、および処理されたシリコンウエハー表面積によって促進されています。

半導体業界の概要

半導体業界には、Intel Corporation、Samsung Electronics、Qualcomm Incorporated、Micron Technology Inc.、SK Hynix Inc.などの大手企業があり、その半連結化に貢献しています。市場参入企業は、自社の製品ポートフォリオを強化し、永続的な競争上の優位性を確保するために、パートナーシップや買収などの戦略を積極的に活用しています。

2023年 10月、Micronは16Gb DDR5メモリを導入することにより、1ワットプロセスノードテクノロジーを大幅に拡張しました。この新製品は、最大7,200 MT/sの速度でシステム内機能について厳密にテストおよび検証され、現在マイクロンのデータセンターおよびPC顧客に出荷されています。 Micronの1βベース DDR5メモリに高度なHigh-k CMOSデバイステクノロジ、4フェーズクロッキングシステム、およびクロック同期1を組み込むことにより、最大50%の大幅なパフォーマンス向上と33%のパフォーマンス向上が実現します。前世代と比較してワットあたり。

2023年 9月、Intel Foundry Services(IFS)と、アナログ半導体ソリューションの著名なプロバイダーであるTower Semiconductorが提携を発表しました。インテルは、タワー社が世界中の顧客に対応できるよう、ファウンドリ・サービスと300mm製造能力を拡張します。タワー社は契約の一環として、ニューメキシコ州にあるインテルの高度な製造施設を活用して運営上のニーズを満たすことになります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 技術動向

- 業界のバリューチェーン/サプライチェーン分析

- COVID-19の影響、マクロ経済動向、地政学的シナリオ

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場力学

- 市場促進要因

- 家庭用電子機器のニーズの高まりにより製造の見通しが高まる

- AI、IoT、コネクテッドデバイスが業界全体で急増

- 自動車における半導体の応用の増加

- 5G導入の増加と5Gスマートフォンの需要の高まり

- 市場の課題/抑制要因

- サプライチェーンの混乱による半導体チップの不足

- テクノロジーの動的な性質により、製造装置にいくつかの変更が必要

- 垂直統合はOSATプレーヤーの重大な関心事の1つです

第6章 市場セグメンテーション

- 半導体デバイス別

- ディスクリート半導体

- オプトエレクトロニクス

- センサー

- 集積回路

- 半導体装置別

- フロントエンド機器

- バックエンド機器

- 半導体材料別

- 製作

- 包装

- 半導体ファウンドリ市場別

- 外部委託半導体組立テストサービス(OSAT)市場別

第7章 競合情勢

- 企業プロファイル

- Intel Corporation

- Samsung Electronics Co. Ltd

- Qualcomm Incorporated

- Micron Technology Inc.

- SK Hynix Inc.

- Texas Instruments Incorporated

- Broadcom Inc.

- Mediatek Inc.

- Applied Materials Inc.

- ASML Holding NV

- Tokyo Electron Limited

- Lam Research Corporation

- KLA Corporation

- Advantest Corporation

- Screen Holdings Co. Ltd

- Teradyne Inc.

- BASF SE

- LG Chem Ltd

- Indium Corporation

- Resonac Holding Corporation

- Kyocera Corporation

- Henkel AG &Co. KGaA

- Sumitomo Chemical Co. Ltd

- Dow Chemical Co.(Dow Inc.)

- Taiwan Semiconductor Manufacturing Company(TSMC)Limited

- Samsung Foundry(Samsung Electronics Co. Ltd)

- United Microelectronics Corporation(UMC)

- GlobalFoundries Inc.

- Semiconductor Manufacturing International Corporation(SMIC)

- Hua Hong Semiconductor Limited

- Powerchip Technology Corporation

- ASE Technology Holding Co.Ltd

- Amkor Technology Inc.

- Jiangsu Changjiang Electronics Technology Co. Ltd

- Powertech Technology Inc.

- Tongfu Microelectronics Co. Ltd

- Tianshui Huatian Technology Co. Ltd

- King Yuan Electronics Co. Ltd

- ベンダーの市場シェア

- ベンダー市場シェア-半導体デバイス市場

- ベンダー市場シェア-半導体装置市場

- ベンダー市場シェア-半導体ファウンドリ市場

- ベンダー市場シェア-OSAT市場

第8章 投資分析

第9章 市場の将来展望

The Semiconductor Industry is expected to grow from USD 0.72 trillion in 2024 to USD 1.21 trillion by 2029, at a CAGR of 10.86% during the forecast period (2024-2029).

Key Highlights

- The semiconductor sector is experiencing a swift expansion as semiconductors are becoming the fundamental components of contemporary technology. The progress and breakthroughs in this industry are directly influencing all subsequent technologies.

- Semiconductor devices are electronic components that use semiconducting material as their foundation. This material produces transistors, diodes, and other fundamental functional units found in integrated circuits (ICs). These devices are characterized by their ability to neither conduct electricity well nor act as effective insulators. The benefits of semiconductor devices encompass their affordability, dependability, and compact size. Over the past few decades, the utilization of these devices in the production of diverse electronics has surged in popularity, and it is projected to continue gaining momentum in the forthcoming years.

- The semiconductor industry is projected to experience strong growth in the foreseeable future as it caters to the rising need for semiconductor materials in emerging technologies like artificial intelligence (AI), autonomous driving, the Internet of Things, and 5G. This growth is fueled by intense competition among key players and consistent investment in research and development (R&D). As a result, vendors are constantly driven to innovate and gain a competitive advantage in the market.

- The market demand for semiconductor devices is projected to rise due to businesses' widespread adoption of electrification and autonomy. Electric vehicles are spearheading the movement toward a sustainable future, with electronics and semiconductors serving as crucial components. Governments across the globe are setting ambitious goals for the electrification of their transportation sectors, prompting leading automakers to make substantial investments in electric vehicle research and development. Semiconductors are emerging as the central processing units of EVs, empowering them to deliver optimal performance. Consequently, the growing investments in electric vehicles are anticipated to fuel the demand for the semiconductor market.

- The semiconductor industry needs more skilled workers. By the year 2030, more than one million additional skilled workers are likely to be needed to meet the industry's demand. Further, the semiconductor industry is characterized by long lead times and high capital investments. Manufacturing capacity constraints and changes in demand have led to shortages in the supply chain. These factors are expected to challenge the market's growth.

- The sector has undergone substantial changes due to COVID-19, impacting customer behavior, business revenues, and corporate operations. Additionally, the pandemic has revealed previously unnoticed risks on the supply side, potentially resulting in shortages of essential parts and components. Consequently, semiconductor companies are proactively restructuring their supply chains to enhance resilience, and these adjustments may persist in the post-pandemic era.

Semiconductor Market Trends

Discrete Semiconductors to Hold Significant Market Share in the Semiconductor Devices Segment

- The rising demand for high-energy and power-efficient devices, the increasing prevalence of wireless and portable electronic products, coupled with the increased use of these devices in the automotive industry due to the shift towards electrification are some of the key factors driving the growth of the segment.

- One of the significant trends in discrete semiconductors is efficient power management. New system architectures are improving the efficiency of AC-DC power adapters while simultaneously reducing the size and component count. New standards for Power-over-Ethernet (PoE) allow higher power transfer, which enables the development of new classes of devices, like connected lighting.

- MOSFET has always played an important part in the telecom sector, as switching power supply is the most prevalent application for power MOSFETs, which are also commonly utilized for MOS RF power amplifiers, allowing mobile networks to move from analog to digital. According to Ericsson, the number of 5G subscriptions increased by 70 million during the first quarter of 2022, reaching about 620 million. By the end of 2022, the number is predicted to reach 1 billion. Such reasons will spur the demand for power semiconductors, which will increase the demand for MOSFETs and lead to several breakthroughs in the telecom sector.

- Further, the demand for IGBT among various discrete semiconductors has been gaining traction and is widely used in low-power converters. The most popular semiconductor switches for power conversion in automotive, other motor drives, and renewable energy systems are discrete IGBTs. The main driving force is also the growing use of Insulated Gate Bipolar Transistor (IGBT) devices across a variety of sectors, including automotive, consumer electronics, industrial, IT and communications, healthcare, aerospace and defense, and others.

- The majority of discrete IGBT applications include inverters, various consumer goods like air conditioners and washing machines, switching-mode power supplies (SMPS), which are components used in personal computers, welding equipment, and induction heating devices like microwaves, electric cookers, induction stoves, etc. for soft switching and strobe flash control. The increasing demand for consumer electronic appliances like UPSs, power conditioners, air conditioners, etc., which use discrete IGBT types for lower-current applications, is credited with driving the growth of the discrete IGBT market. Discrete IGBTs have been found to have the lowest power losses in consumer goods, which is anticipated to be a key factor influencing the segment's growth in the market.

Fabrication to Hold Significant Market Share in Semiconductor Materials Segment

- Semiconductor fabrication materials form a crucial building block for the advanced microelectronics found in consumer electronics, high-end data centers, automotive applications, medical devices, IoT devices, power electronics, and more. The segment covers materials like process chemicals, photomasks, electronic gases, photoresist ancillaries, sputtering targets, silicon, and other materials.

- One of the primary factors driving the demand for semiconductor fabrication materials is the increasing use of digitally integrated ICs in the electrical, electronics, automotive, and telecommunication industries. Additionally, the rising investments in the energy sector are also expected to contribute positively to the growth of this segment, owing to the widespread application of semiconductors in solar panels, drives, and pumps in wind and water turbines, and protection circuits in energy conversion to ensure efficiency and minimal power loss. For instance, as per IEA, global energy investment will increase by 8% in 2022 to reach USD 2.4 trillion. Furthermore, according to IRENA, the spending on renewable energy is expected to grow steadily, boosting the market.

- While a wide range of materials can exhibit semiconductor properties, some materials are more commonly used in the fabrication of electronic devices due to their specific characteristics. Two of the most prevalent semiconductor materials are silicon and gallium arsenide. Silicon is the most widely used semiconductor material, primarily due to its abundance, low cost, and relatively stable properties at high temperatures. The electric conductivity of silicon is around 1000 S/m. Additionally, silicon has a well-established fabrication infrastructure, making it an attractive choice for manufacturers. However, silicon does have some drawbacks, such as lower electron mobility compared to other materials, which can limit the performance of high-speed devices.

- Gallium arsenide is another popular semiconductor material, valued for its higher electron mobility and direct bandgap. These properties make it well-suited for optoelectronic applications, such as lasers and solar cells. However, gallium arsenide is more expensive and less abundant than silicon, which can limit its widespread adoption. Another drawback of gallium arsenide is that it exists intrinsically as a semi-insulator rather than a semiconductor with an electrical conductivity of 0.000001 S/m.

- Aside from silicon and gallium arsenide, researchers are continually exploring new materials with promising semiconductor properties. These materials include aluminum nitride, carbon nanotubes, and many other materials that have the potential to revolutionize the industry. As the understanding of these emerging materials grows, they will likely play an increasingly important role in the future of semiconductor fabrication.

- Moreover, the market for process chemicals is expected to grow steadily due to the low-cost method and the applications for internal efficiency in the semiconductor sector. The consumption of semiconductor process chemicals is fueled by growth in installed fabrication capacity and expensive chemicals consumed by new technology, as well as processed silicon wafer surface area.

Semiconductor Industry Overview

The semiconductor industry features major players like Intel Corporation, Samsung Electronics Co. Ltd, Qualcomm Incorporated, Micron Technology Inc., and SK Hynix Inc., contributing to its semi-consolidated nature. Market participants are actively leveraging strategies such as partnerships and acquisitions to bolster their product portfolios and secure enduring competitive advantages.

In October 2023, Micron significantly expanded its 1β process node technology by introducing the 16Gb DDR5 memory. Rigorously tested and validated for in-system functionality at speeds of up to 7,200 MT/s, this new product is now being shipped to Micron's data center and PC clientele. The incorporation of advanced high-k CMOS device technology, a 4-phase clocking system, and clock-sync 1 in Micron's 1β-based DDR5 memory yield a substantial performance enhancement of up to 50%, accompanied by a 33% improvement in performance per watt compared to the prior generation.

September 2023 witnessed Intel Foundry Services (IFS) and Tower Semiconductor, a notable provider of analog semiconductor solutions, announcing a collaboration. Intel will extend its foundry services and 300mm manufacturing capacity to assist Tower in catering to its global clientele. Tower, as part of the agreement, will leverage Intel's advanced manufacturing facility in New Mexico to fulfill its operational needs.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Technological Trends

- 4.3 Industry Value Chain/Supply Chain Analysis

- 4.4 Impact of COVID-19, Macro Economic Trends, and Geopolitical Scenarios

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Needs of Consumer Electronic Devices Boosting the Manufacturing Prospects

- 5.1.2 Proliferation of AI, IoT, and Connected Devices Across Industry Verticals

- 5.1.3 Increased Applications of Semiconductors in Automotive

- 5.1.4 Increased Deployment of 5G and Rising Demand for 5G Smartphones

- 5.2 Market Challenges/Restraints

- 5.2.1 Supply Chain Disruptions Resulting in Semiconductor Chip Shortage

- 5.2.2 Dynamic Nature of Technologies Requires Several Changes in Manufacturing Equipment

- 5.2.3 Vertical Integration is One of the Significant Concerns of OSAT Players

6 MARKET SEGMENTATION

- 6.1 By Semiconductor Devices

- 6.1.1 Discrete Semiconductors

- 6.1.2 Optoelectronics

- 6.1.3 Sensors

- 6.1.4 Integrated Circuits

- 6.2 By Semiconductor Equipment

- 6.2.1 Front-end Equipment

- 6.2.2 Back-end Equipment

- 6.3 By Semiconductors Materials

- 6.3.1 Fabrication

- 6.3.2 Pacakging

- 6.4 By Semiconductor Foundry Market

- 6.5 By Outsourced Semiconductor Assembly Test Services (OSAT) Market

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 Intel Corporation

- 7.1.2 Samsung Electronics Co. Ltd

- 7.1.3 Qualcomm Incorporated

- 7.1.4 Micron Technology Inc.

- 7.1.5 SK Hynix Inc.

- 7.1.6 Texas Instruments Incorporated

- 7.1.7 Broadcom Inc.

- 7.1.8 Mediatek Inc.

- 7.1.9 Applied Materials Inc.

- 7.1.10 ASML Holding NV

- 7.1.11 Tokyo Electron Limited

- 7.1.12 Lam Research Corporation

- 7.1.13 KLA Corporation

- 7.1.14 Advantest Corporation

- 7.1.15 Screen Holdings Co. Ltd

- 7.1.16 Teradyne Inc.

- 7.1.17 BASF SE

- 7.1.18 LG Chem Ltd

- 7.1.19 Indium Corporation

- 7.1.20 Resonac Holding Corporation

- 7.1.21 Kyocera Corporation

- 7.1.22 Henkel AG & Co. KGaA

- 7.1.23 Sumitomo Chemical Co. Ltd

- 7.1.24 Dow Chemical Co. (Dow Inc.)

- 7.1.25 Taiwan Semiconductor Manufacturing Company (TSMC) Limited

- 7.1.26 Samsung Foundry (Samsung Electronics Co. Ltd)

- 7.1.27 United Microelectronics Corporation (UMC)

- 7.1.28 GlobalFoundries Inc.

- 7.1.29 Semiconductor Manufacturing International Corporation (SMIC)

- 7.1.30 Hua Hong Semiconductor Limited

- 7.1.31 Powerchip Technology Corporation

- 7.1.32 ASE Technology Holding Co.Ltd

- 7.1.33 Amkor Technology Inc.

- 7.1.34 Jiangsu Changjiang Electronics Technology Co. Ltd

- 7.1.35 Powertech Technology Inc.

- 7.1.36 Tongfu Microelectronics Co. Ltd

- 7.1.37 Tianshui Huatian Technology Co. Ltd

- 7.1.38 King Yuan Electronics Co. Ltd

- 7.2 Vendor Market Share

- 7.2.1 Vendor Market Share - Semiconductor Devices Market

- 7.2.2 Vendor Market Share - Semiconductor Equipment Market

- 7.2.3 Vendor Market Share - Semiconductor Foundry Market

- 7.2.4 Vendor Market Share - OSAT Market

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET