|

|

市場調査レポート

商品コード

1550244

インドの半導体:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)India Semiconductor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドの半導体:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

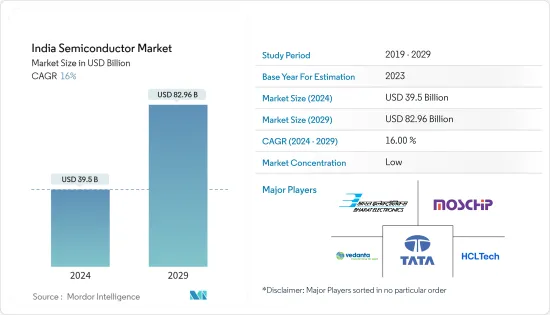

インド半導体市場規模は2024年に395億米ドルと推定、2029年には829億6,000万米ドルに達すると予測、予測期間中(2024-2029年)のCAGRは16%で成長します。

主なハイライト

- シリコンのような半導体は、トランジスタ、ダイオード、集積回路を作るのに不可欠であり、現代のエレクトロニクスの基盤を形成しています。シリコンは、電気信号を管理し、さまざまな電子技術の進歩を促進するために不可欠です。データ駆動型アプリケーションの需要が高まるにつれ、従来のハードディスク・ドライブ(HDD)の代わりにソリッド・ステート・ドライブ(SSD)を使用する傾向が顕著になっています。不揮発性メモリ・エクスプレス(NVMe)技術の採用が急速に進み、データ転送速度が向上しています。

- さらに、インドのコンシューマーエレクトロニクスでは、先進技術とデジタル化を取り入れる傾向が顕著です。これには、スマートTV、スピーカー、家電製品などのIoT対応製品のようなスマートホームデバイスへの嗜好の高まりが含まれます。スマートフォン市場も、手頃な価格でありながら機能満載のモデルへとシフトしており、スマートフォンの利用が増加しています。

- スマートフォンの利用やデジタル化への取り組みも、大容量RAMモジュールの需要を後押ししています。ゲーム業界の成長も、より高速で効率的なメモリ・ソリューションへの関心を喚起しています。その一例として、韓国のSimmtech社との有利な契約により、グジャラート州でインド初の国産メモリーチップの生産が予定されています。

- ムンバイとプネーは、技術革新、研究開発に重点を置き、半導体設計・製造の重要な拠点となりつつあります。両地域では、新興企業や共同事業が増加し、エコシステムの繁栄につながっています。AI、IoT、5Gのような最先端技術の利用が増加しており、先進的な半導体製品の必要性が高まっています。

- インドには、政府が投資政策を継続的に支援し、良好な規制・ビジネス環境を育成し、不確実性を引き起こす可能性のある施策の実施を控えれば、世界の半導体バリューチェーンへの参加を大幅に強化できる可能性があります。今後5年間で、インドは最大5つの施設を設立し、28nm以上の旧世代半導体を製造するファブを誘致することで、半導体の組立・テスト・パッケージング(ATP)分野での存在感を高める可能性があります。

- さらに、インドと米国は、両国の企業、学術機関、政府機関の間の戦略的技術パートナーシップと防衛産業協力の拡大を目的とした、重要かつ新興の技術(CET)に関する協力イニシアチブを発表しました。2023年、米国の半導体産業協会(SIA)とインド電子・半導体協会(IESA)は、産業機会を特定し、両国の半導体エコシステムの戦略的発展を促進するための「準備アセスメント」で協力することに合意しました。

- インドも現在、重要な瞬間と機会を経験しています。COVID-19パンデミックの余波、サプライチェーン調整への世界の取り組み、中国におけるコスト上昇、AIやEVのような技術の進歩、人口動態の変化、その他様々な要因によって、多国籍企業は、多様化、回復力、持続可能性、コスト効率の向上を求めて、世界なバリューチェーン構造を見直す必要に迫られています。

- これに加え、インドは現在、ファブやATMP、その他の関連技術の進歩や設計のために、国内半導体産業を支援する外国投資を積極的に求めています。その一例として、アッサム州政府はモリガオンにおける半導体製造装置の設立を急ピッチで進めており、タタ・グループとの間で170エーカー以上の土地と2,700億インドルピー(32億2,000万米ドル)の投資について60年間のリース契約を結んでいます。さらに、グジャラート州にあるタタ・グループの半導体チップ製造工場は、約5,000億インドルピー(59億7,000万米ドル)の予算で承認されました。

- インドは幸いなことに設計エンジニアの数が多いです。しかし、チップの製造や生産に不可欠なデバイス物理学やプロセス技術に精通した半導体技術者の不足は顕著で、市場の成長を大きく妨げています。インドの半導体産業では、2027年までに研究開発、製造、設計、先進パッケージングなど様々な分野で25万人から30万人の専門家が不足すると予想されています。

インド半導体市場動向

センサーとアクチュエーター分野が著しい成長を遂げる見込み

- インド市場ではセンサーの利用が増加しており、ベンダーやユーザーはこの市場の成長に向けて多額の投資を行うようになっています。自動車産業や家電産業も、インドにおけるセンサー需要の牽引役として重要な役割を果たしています。センサー市場の拡大は、産業部門全体の成長やMEMS(Micro Electro Mechanical Systems)センサーのイントロダクションとも関連しています。

- 自動化需要の増加や、タブレット、PC、スマートフォン、スマートウォッチなどのデバイスの普及に加え、自動車販売の増加や家電技術の進歩が、インドのセンサー市場を牽引する主な要因になると予想されます。

- さらに、インドの製造業は人口拡大により著しい成長を遂げています。この分野への投資は増加しており、「Make in India」のようなイニシアチブは、インドを世界の製造拠点として位置づけることを目的としています。製造業の2023年度の年間生産成長率は4.7%です。数多くの組織や機関がこの取り組みに積極的に関与しており、2024年2月にはIITジョードプルの研究者が初の「メイク・イン・インディア」人呼気センサーを開発するなど、顕著な成果を挙げています。このセンサーは金属酸化物とナノシリコンをベースにしており、室温で作動します。

- 工場の自動化の進展とインダストリー4.0の導入は、産業用センサーの使用に大きく依存しています。モーションセンサー、環境センサー、振動センサーなど、これらのセンサーはこのプロセスで重要な役割を果たします。インドの産業部門は、経済的・人口的成長を遂げ、地元ビジネスと輸出見通しの両方を支え、大幅な発展が見込まれています。

- 産業オートメーション、プロセス制御、ロボット工学、機器の分野では、センサーが不可欠です。インドはまた、モノのインターネット(IoT)技術の進歩やスマートシティプロジェクトにも多額の投資を行っています。NASSCOMのレポートによると、インドのIoT市場は2025年までに150億米ドルに達すると予想されています。農業、ヘルスケア、製造業、スマートシティなど、さまざまな業界がIoTイノベーションによって前向きな変化を経験しています。

インド全土で成長する自動車産業とEV需要が市場を牽引

- インドの自動車産業とEV産業は、国の交通事情に大きな影響を与える可能性を秘めた変革の旅に出ようとしています。この産業は、変革を推進し、インドのより持続可能な未来を創造し、気候変動対策や都市生活の質向上に向けた世界の取り組みに貢献する能力を有しています。CIIによると、インドは2030年までに様々な自動車カテゴリーにおけるEV販売比率を高めるという野心的な目標を掲げています。

- IBEFの情報によると、インドは2030年までに主要な電気自動車(EV)市場として台頭する可能性があり、今後8~10年間で2,000億米ドルを超える大きな投資機会がもたらされると予測されています。また、飲食品、製造業、医薬品などの主要産業では、労働力の制約や遠隔監視・操作の必要性から、自動化のニーズが高まっています。その結果、このような自動化要件の増加に対応するため、さまざまなセンサーに対する需要が高まっています。

- インド政府は「Make in India」イニシアティブに基づき、自動車製造の成長に重点を置いています。オート・ミッション・プラン(AMP)2016-26では、乗用車市場が2026年までに940万台へと大幅に増加すると予測されており、その結果、この地域のセンサー需要が高まることになります。

- EVの成功は、中央・州レベルの政府の取り組み、業界の強力な注力、一般市民の電気自動車受け入れの拡大など、さまざまな要因によるものと考えられます。FAMEインド、自動車・自動車部品PLIスキーム、ACCバッテリー製造PLIスキームなどのプログラムは、現地生産を促進し、EVの採用を促進する上で重要な役割を果たしています。

- インドは世界規模で自動車部品の調達先として著名になりつつあり、同産業は毎年生産量の25%以上を輸出しています。例えば、現代自動車は、インドにおける電気自動車構想をさらに発展させるため、今後10年間でタミル・ナードゥ州に24億5,000万米ドルを投資する意向を表明しました。同社はまた、電気自動車のバッテリーパックを組み立て、電気自動車用の充電ステーションを100カ所設置することも検討しています。

- さらに、NITI AayogとRocky Mountain Institute(RMI)は、インドの電気自動車(EV)ファイナンス部門は2030年までに3.7 lakh crore(500億米ドル)に達すると予測しています。大手自動車メーカーはすでに、需要の増加に対応するため、業界のさまざまな分野で大規模な投資を開始しています。例えば、2023年3月には、台湾のハイテク企業であるFoxconnが、インドで半導体とEVの開発に投資する計画を明らかにしました。

インド半導体産業の概要

インドの半導体市場は断片化されており、Tata Group、HCL Technologies、Bharat Electronics Limited、MosChip Technologies、その他以下のような様々な世界企業が存在します。 AMD, Foxconn, and NXP Semiconductors. The companies aim to continuously invest in strategic partnerships and product developments to gain substantial market share.

- 2024年5月ラムリサーチは、世界の半導体製造装置のサプライチェーンをインドに拡大することを発表。電子情報技術省(Ministry of Electronics and IT)の川下エコシステム開発への取り組みがこの決定に貢献しました。ラムリサーチは、さまざまなサプライチェーンセグメントの能力を評価しており、精密部品やその他の必要な供給品の需要を満たすため、インドに拠点を置くサプライヤーとの協力に関心を示しています。

- 2024年3月タタ・グループは、2026年までにインド初の半導体製造装置による商業生産を開始し、スマートフォンから防衛システムまで幅広い技術に不可欠なチップの自立を目指すと発表。アッサム州にあるTata Electronics Pvt.Ltdが所有するこの工場は、当初は28nmの半導体チップの生産に重点を置く。工場での生産は2025年後半から2026年前半までに開始され、自動車、電力、電子機器、消費財、医療機器などさまざまな分野に対応すると予想されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 新規参入業者の脅威

- COVID-19とマクロ経済要因が市場に与える影響の評価

- 半導体産業バリューチェーン分析

- サプライチェーン分析

- バリューチェーンの重点分野とインドが現在奨励しているプロジェクトの種類

- 世界の半導体産業分析

- インドにおける最大の半導体クラスターと予想される最大の製造拠点

- 政府の規制とインセンティブ・プログラムの分析

- インドにおける政府の取り組み/制度と制度へのアクセス方法

- 各種カテゴリー(シリコン半導体ファブ、ディスプレイファブ、化合物半導体/SiPh/センサーファブ、OSAT/組立/テスト)の適格基準と財政支援

- インドの半導体IC産業のSWOT分析(IC設計、IC製造、組立/テスト/パッケージング)

- インド半導体産業の労働力分析

- 半導体部品調達分析

- 半導体設計市場分析

- インドの半導体産業形成における主要利害関係者リストとその役割

- インドにおける半導体製造工場設立の課題

第5章 市場力学

- 市場促進要因

- 自動車産業とEV需要の成長

- スマートフォンと家電需要の成長

- 5Gと固定インターネット接続による通信インフラの成長

- 市場抑制要因

- 設計分野での存在感の薄さと国産ベンダーの不足

- 台湾、日本、中国など他国と比較した鋳造能力と投資額

第6章 市場セグメンテーション

- 半導体デバイスタイプ別

- ディスクリート半導体

- オプトエレクトロニクス

- センサーとアクチュエーター

- 集積回路

- アナログ

- マイクロ

- ロジック

- メモリー

- エンドユーザー産業別

- コンピュータ

- 通信(有線・無線含む)

- 自動車

- コンシューマー

- その他のエンドユーザー産業(産業、政府など)

第7章 競合情勢

- 企業プロファイル

- Tata Group

- Bharat Electronics Limited

- Moschip Semiconductor Technologies

- Vedanta Semiconductors Private Limited(VSPL)

- HCL Technologies

- ASM Technologies Ltd

- Applied Materials India Pvt. Ltd

- Hon Hai Technology Group(Foxconn)

- Broadcom Inc.

- NXP Semiconductors

- ROHM Semiconductor

- Infineon Technologies

- Renesas Electronics

- STMicroelectronics

- Powerchip Semiconductor Manufacturing Corp(PSMC)

- AMD Group

- Intel Corporation

- Samsung Electronics Co. Ltd

- Qualcomm Incorporated

- Micron Technology Inc.

- Texas Instruments Incorporated

- Mediatek Inc.

第8章 投資分析

第9章 市場の将来

The India Semiconductor Market size is estimated at USD 39.5 billion in 2024, and is expected to reach USD 82.96 billion by 2029, growing at a CAGR of 16% during the forecast period (2024-2029).

Key Highlights

- Semiconductors like silicon are essential for creating transistors, diodes, and integrated circuits, forming the foundation of modern electronics. They are crucial for managing electrical signals and facilitating the advancement of various electronic technologies. As the demand for data-driven applications grows, there is a noticeable trend toward using solid-state drives (SSDs) instead of traditional hard disk drives (HDDs). The adoption of non-volatile memory express (NVMe) technology is rapidly increasing, improving data transfer speeds.

- Furthermore, there is a noticeable trend in consumer electronics in India toward embracing advanced technologies and digitalization. This includes a growing preference for smart home devices such as IoT-enabled products like smart TVs, speakers, and appliances. The smartphone market is also seeing a shift toward affordable yet feature-packed models, leading to an increase in smartphone usage.

- The use of smartphones and digitalization efforts are also driving the demand for high-capacity RAM modules. The gaming industry's growth is also sparking interest in faster and more efficient memory solutions. An example of this is the upcoming production of India's first domestically made memory chip in Gujarat due to a lucrative deal with South Korea's Simmtech.

- Mumbai and Pune are becoming important hubs for semiconductor design and manufacturing, with a strong emphasis on innovation, research, and development. The regions are experiencing growth in startups and collaborations, leading to a thriving ecosystem. The increasing use of cutting-edge technologies like AI, IoT, and 5G is fueling the need for advanced semiconductor products.

- India has the potential to greatly enhance its participation in global semiconductor value chains if the government continues to support investment policies, fosters a favorable regulatory and business environment, and refrains from implementing measures that may cause uncertainty. Over the next five years, India could potentially increase its presence in the semiconductor assembly, test, and packaging (ATP) sector by establishing up to five facilities and attracting fabs that manufacture older-generation semiconductors at 28 nm or higher.

- In addition, India and the United States announced a collaborative initiative on Critical and Emerging Technology (CET) aimed at expanding strategic technology partnerships and defense industrial cooperation between businesses, academic institutions, and government agencies of both nations. In 2023, the Semiconductor Industry Association (SIA) in the United States and the India Electronics and Semiconductor Association (IESA) agreed to work together on a "readiness assessment" to identify industry opportunities and promote the strategic development of their semiconductor ecosystem.

- India is also currently experiencing a significant moment and opportunity. The aftermath of the COVID-19 pandemic, along with global efforts to adjust supply chains, rising costs in China, advancements in technologies like AI and EVs, demographic changes, and various other factors have prompted multinational companies to reevaluate their global value chain structures in search of improved diversification, resilience, sustainability, and cost efficiency.

- In addition to this, India is currently actively seeking foreign investments to support its domestic semiconductor industry for the advancement and design of fabs, ATMP, and other related technologies. One example of this is the Government of Assam's efforts to fast-track the establishment of a semiconductor unit in Morigaon, achieved through a 60-year lease agreement with the Tata Group for more than 170 acres of land and an investment of INR 270 billion (USD 3.22 billion). Furthermore, approval has been granted for Tata's semiconductor chip fabrication unit in Gujarat with a budget of nearly INR 500 billion (USD 5.97 billion)

- India is fortunate to have a significant number of design engineers. However, there is a noticeable shortage of semiconductor engineers with expertise in device physics and process technology, which is crucial for chip fabrication and manufacturing and is significantly hindering market growth. It is anticipated that the semiconductor industry in India will encounter a deficit of 250,000 to 300,000 professionals in various sectors, such as research and development, manufacturing, design, and advanced packaging, by 2027.

India Semiconductor Market Trends

The Sensors and Actuators Segment is Expected to Witness Significant Growth

- The increasing use of sensors in the Indian market has prompted vendors and users to make significant investments in the growth of this market. The automotive and consumer electronics industries are also playing a key role in driving demand for sensors in India. The expansion of the sensor market can also be linked to the overall growth of the industrial sector, as well as the introduction of micro electro mechanical systems (MEMS) sensors.

- The increasing demand for automation and the widespread use of devices such as tablets, PCs, smartphones, and smartwatches, along with the growing automotive sales and advancements in consumer electronics technology, are expected to be the main factors driving the Indian sensors market.

- Furthermore, the manufacturing industry in India has been experiencing significant growth due to the country's expanding population. Investments in the sector are increasing, and initiatives like 'Make in India' are aimed at positioning India as a global manufacturing hub. The manufacturing industry saw a 4.7% annual production growth rate in the fiscal year 2023. Numerous organizations and institutions are actively involved in this initiative, with notable achievements such as the development of the first "Make in India" human breath sensor by researchers at IIT Jodhpur in February 2024. This sensor is based on metal oxides and nano silicon and operates at room temperature.

- The advancement of factory automation and the adoption of Industry 4.0 are greatly dependent on the use of industrial sensors. These sensors, such as motion, environmental, and vibration sensors, play a crucial role in the process. India's industrial sectors are set for economic and demographic growth, supporting both local businesses and export prospects, which are expected to see substantial development.

- In the field of industrial automation, process control, robotics, and equipment, sensors are essential. India has also been making significant investments in the advancement of the Internet of Things (IoT) technology and smart city projects. According to a NASSCOM report, the Indian IoT market is expected to reach a value of USD 15 billion by 2025. Various industries, including agriculture, healthcare, manufacturing, and smart cities, are experiencing positive changes driven by IoT innovations.

Growing Automotive Industry and EV Demand Across India to Propel the Market

- India's automotive and EV industry is poised for a transformative journey that has the potential to greatly impact the nation's transportation landscape. This industry has the ability to drive change, create a more sustainable future for India, and contribute to global initiatives to combat climate change and improve the quality of urban living. According to CII, India has set ambitious goals to increase the percentage of EV sales in various vehicle categories by 2030.

- According to information provided by IBEF, it is projected that India has the potential to emerge as the leading electric vehicle (EV) market by 2030, presenting a significant investment opportunity of over USD 200 billion within the next 8-10 years. There is also a growing need for automation in key industries like food and beverage, manufacturing, and pharmaceuticals, driven by workforce constraints and the necessity for remote monitoring and operations. Consequently, there is a rising demand for a variety of sensors to cater to this increase in automation requirements.

- In line with the 'Make in India' initiative, the Indian government is placing emphasis on the growth of automobile manufacturing. The Auto Mission Plan (AMP) 2016-26 forecasts a significant increase in the passenger car market to 9.4 million units by 2026, resulting in a higher demand for sensors in the region.

- The success of EVs can be attributed to a variety of factors, such as government initiatives at both the central and state levels, a strong focus from the industry, and the increasing acceptance of electric vehicles by the public. Programs like FAME India, the PLI scheme for the Auto and Auto Component, and the PLI scheme for manufacturing ACC batteries have played a crucial role in promoting local production and encouraging the adoption of EVs.

- India is becoming a prominent destination for sourcing auto components on a global scale, with the industry exporting more than 25% of its production each year. For instance, Hyundai Motor expressed its intention to invest USD 2.45 billion in Tamil Nadu over the next 10 years to further develop its electric vehicle initiatives in India. The company is also looking to assemble EV battery packs and establish 100 charging stations for electric vehicles.

- Furthermore, the NITI Aayog and Rocky Mountain Institute (RMI) have forecasted that India's electric vehicle (EV) finance sector is projected to reach INR 3.7 lakh crore (USD 50 billion) by 2030. Leading automakers have already started making significant investments across different segments of the industry to cater to the increasing demand. For example, in March 2023, Foxconn, a tech company based in Taiwan, revealed its plans to invest in the development of semiconductors and EVs in India.

India Semiconductor Industry Overview

The Indian semiconductor market is fragmented with the presence of several players like Tata Group, HCL Technologies, Bharat Electronics Limited, MosChip Technologies, and various other global players such as AMD, Foxconn, and NXP Semiconductors. The companies aim to continuously invest in strategic partnerships and product developments to gain substantial market share.

- May 2024: Lam Research announced its expansion of the global semiconductor fabrication equipment supply chain to India. The Ministry of Electronics and IT's efforts to develop a downstream ecosystem have been instrumental in this decision. Lam Research is evaluating capabilities in different supply chain segments and has expressed its interest in collaborating with India-based suppliers to meet the demand for precision components and other necessary supplies.

- March 2024: Tata Group announced that it was aiming to commence commercial production from India's first semiconductor fabrication unit by 2026, with the goal of achieving self-reliance in chips that are essential for powering a wide range of technologies, from smartphones to defense systems. The plant, owned by Tata Electronics Pvt. Ltd, located in Assam, will initially focus on producing semiconductor chips starting at 28 nm. It is anticipated that production at the plant will begin by late 2025 or early 2026, catering to various sectors, such as automotive, power, electronics, consumer goods, and medical devices.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers/Consumers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of Substitute Products

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of New Entrants

- 4.3 Assessment of the Impact of COVID-19 and Macroeconomic Factors on the Market

- 4.4 Semiconductor Industry Value Chain Analysis

- 4.4.1 Supply Chain Analysis

- 4.4.2 Focus Areas in the Value Chain and Type of Projects Currently Encouraged by India

- 4.5 Global Semiconductor Industry Analysis

- 4.6 Largest Semiconductor Clusters in India and Expected Largest Manufacturing Hubs

- 4.7 Analysis of Government Regulations and Incentive Programs

- 4.7.1 Government Initiatives/Schemes in India and Ways to Access the Schemes

- 4.8 Eligibility Criteria and Fiscal Support for Various Categories (Silicon Semiconductor Fab, Display Fab, Compound Semiconductor/SiPh/Sensors Fab and OSAT/Assembly/Testing)

- 4.9 SWOT Analysis of Semiconductor IC Industry in India (IC Design, IC Fabrication, and Assembly/Test/Packaging)

- 4.10 Workforce Analysis for the Indian Semiconductor Industry

- 4.11 Semiconductor Component Sourcing Analysis

- 4.12 Semiconductor Design Market Analysis

- 4.13 List of Key Stakeholders and Their Role in Shaping the Semiconductor Industry in India

- 4.14 Challenges in Setting up a Semiconductor Manufacturing Plant in India

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Automotive Industry and EV Demand

- 5.1.2 Smartphone and Consumer Electronics Demand Growth

- 5.1.3 Growing Telecom Infrastructure Augmented by 5G and Fixed Internet Connections

- 5.2 Market Restraints

- 5.2.1 Limited Presence in the Design Space and Lack of Homegrown Vendors

- 5.2.2 Foundry Capacity and Investment Compared to Other Countries such as Taiwan, Japan, and China

6 MARKET SEGMENTATION

- 6.1 By Semiconductor Device Type

- 6.1.1 Discrete Semiconductor

- 6.1.2 Optoelectronics

- 6.1.3 Sensors and Actuators

- 6.1.4 Integrated Circuits

- 6.1.4.1 Analog

- 6.1.4.2 Micro

- 6.1.4.3 Logic

- 6.1.4.4 Memory

- 6.2 By End-user Industry

- 6.2.1 Computer

- 6.2.2 Communication (Includes Wireline and Wireless)

- 6.2.3 Automotive

- 6.2.4 Consumer

- 6.2.5 Other End-user Industries (Industrial, Government, etc.)

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Tata Group

- 7.1.2 Bharat Electronics Limited

- 7.1.3 Moschip Semiconductor Technologies

- 7.1.4 Vedanta Semiconductors Private Limited (VSPL)

- 7.1.5 HCL Technologies

- 7.1.6 ASM Technologies Ltd

- 7.1.7 Applied Materials India Pvt. Ltd

- 7.1.8 Hon Hai Technology Group (Foxconn)

- 7.1.9 Broadcom Inc.

- 7.1.10 NXP Semiconductors

- 7.1.11 ROHM Semiconductor

- 7.1.12 Infineon Technologies

- 7.1.13 Renesas Electronics

- 7.1.14 STMicroelectronics

- 7.1.15 Powerchip Semiconductor Manufacturing Corp (PSMC)

- 7.1.16 AMD Group

- 7.1.17 Intel Corporation

- 7.1.18 Samsung Electronics Co. Ltd

- 7.1.19 Qualcomm Incorporated

- 7.1.20 Micron Technology Inc.

- 7.1.21 Texas Instruments Incorporated

- 7.1.22 Mediatek Inc.