|

市場調査レポート

商品コード

1440361

微小残存疾患:世界市場シェア分析、業界動向と統計、成長予測(2024~2029年)Global Minimal Residual Disease - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 微小残存疾患:世界市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

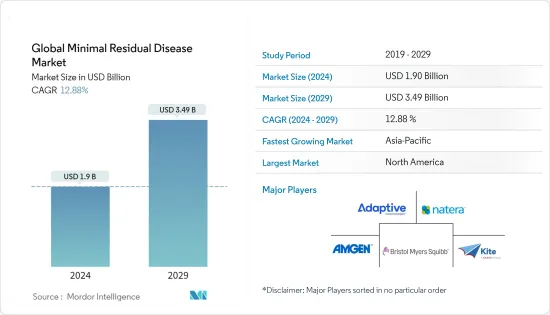

世界の微小残存疾患市場規模は、2024年に19億米ドルと推定され、2029年までに34億9,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に12.88%のCAGRで成長します。

COVID-19感染症のパンデミックは世界中のヘルスケアシステムに影響を及ぼし、多くのヘルスケア施設で通常の診療が中断され、脆弱ながん患者が重大なリスクにさらされています。新型コロナウイルス感染症(COVID-19)のパンデミックが始まって以来、新型コロナウイルス感染症患者の入院を増やし、入院する非新型コロナウイルス感染症患者の数を減らすための措置が講じられ、治療の延期につながっています。 2020年9月の「がん治療に対するCOVID-19感染症パンデミックの影響:世界規模の共同研究」と題した研究では、2020年4月21日から5月8日までに6大陸54カ国の合計356のセンターが参加したと報告しました。これらのセンターは71万6,979人にサービスを提供しています。毎年新たにがん患者が発生します。そのほとんど(88.2%)が、パンデミック中にケアを提供する際に課題に直面していると報告しました。 55.34%が先制戦略の一環としてサービスを削減しましたが、その他の一般的な理由としては、システムの過負荷(19.94%)、個人用保護具の不足(19.10%)、スタッフ不足(17.98%)、医薬品へのアクセスの制限(9.83%)などが挙げられます。「がん患者に対するCOVID-19の臨床的影響は何か」というタイトルの記事によると、 2020年6月、がん患者のCOVID-19症、特にこの感染症の深刻な影響に対する脆弱性が高まったため、一部の患者は潜在的な感染者との接触を減らすために抗がん剤治療を遅らせたり一時停止したりするようになりました。パンデミックの初期段階では市場に悪影響を及ぼしました。このような研究は、がん治療が深刻な影響を受け、その後市場の成長に影響を与えたことを示しています。したがって、COVID-19感染症のパンデミックは市場の成長に全体的に悪影響を及ぼしています。

微小残存疾患市場の成長を推進する要因は、世界中でさまざまな種類のがんの有病率が上昇していることと、発がん物質の存在を確認するという人々の意識の高まりです。継続的ながん治療を受けている患者は、微小残存疾患市場を前進させる最も重要な要素になると期待されています。さらに、治療のための個別化医薬品の採用の増加と研究開発活動の増加が市場の成長に貢献しています。

さまざまながんに苦しむ人の数の増加が、微小残存疾患市場の成長の重要な促進要因です。たとえば、米国臨床腫瘍学会の2021年 2月の報告書によると、米国では推定235,760人の成人(男性119,100人、女性116,6600人)が肺がんと診断されると予想されています。たとえば、Globocan誌(2020年)では、インドでは18.3%の新規がん症例があり、子宮頸がんが全がんの9.4%を占めていることがわかりました。たとえば、米国がん協会(ACS)が発表した2022年 1月の最新統計によると、2021年には米国で約26,560人の新たな胃がん症例が検出されると予測されており、その内訳は男性16,160人、女性10,400人です。国立乳がん財団が発表した統計によると、2021年7月時点で乳がん患者の約63%が局所期乳がん、27%が局所期乳がん、6%が遠隔(転移)乳がんと診断されています。

さらに、世界中で血液がんの有病率が上昇しているため、より優れた治療選択肢と残存がん細胞の除去精度に対する需要が高まっており、残存疾患を最小限に抑える市場への需要が高まる可能性があります。米国がん協会が発表した統計によると、2022年1月に米国で新たに34,920人の多発性骨髄腫と診断されたと推定されています。

ただし、研究開発活動のコストが高いため、予測期間中の市場の成長が妨げられる可能性があります。

微小残存疾患市場動向

次世代シーケンス(NGS)セグメントは、予測期間中に最高のCAGRで推移すると予想されます

次世代シーケンスは、疾患に関連する遺伝的変異を研究するためにDNAまたはRNAの配列を決定するために使用される技術です。特定の時点で多くのDNAの配列を決定できるため、超並列配列決定とも呼ばれます。

次世代シーケンシング技術の成長を推進する要因としては、世界的にがんの発生率が増加していること、創薬、臨床処置、精密医療における次世代シーケンシングのサービスとアプリケーションに対する需要の高まり、次世代シーケンシング用に確立された最新技術の採用などが挙げられます。

最近、患者の微小残存疾患をより正確にモニタリングするために、次世代シーケンスを含む新しいアッセイが開発されました。次世代シーケンシングは、従来使用されていた形態学的検査および細胞遺伝学的検査よりも高い感度を提供します。 2020年1月にJournal of Molecular Diagnosticsに掲載された「急性骨髄性白血病患者におけるDNAレベルでの突然変異と染色体再配列の同時解析のための新しい次世代シーケンス戦略」と題された論文によると、次のことが判明しました。世代シーケンスは、1回の実行ですべてのゲノム病変を検出できることを約束します。さらに、患者には複数の分子異常が頻繁に存在するため、次世代シーケンスは、新たに診断されたすべての急性骨髄性白血病に適用されます。

さまざまなエラー修正された次世代方法論のイントロダクション、微小な残存疾患の検出が容易になりました。最近、分子バーコーディングは、次世代シーケンシングライブラリの作成に使用される個々のDNA分子のバーコーディングに基づく、いくつかのエラー修正された次世代シーケンシングアプローチの開発に使用されています。国立バイオテクノロジー情報センターが2021年6月に発表した「次世代シーケンスによる微小残存疾患モニタリング」というタイトルの論文によると、次世代シーケンスには未診断の微小残存疾患の有病率を減らす可能性があることが判明しました。これにより、急性リンパ性白血病(ALL)患者の生存にとって重要な早期管理が可能になります。

さらに、企業の研究開発活動への投資、先進技術の導入、最小限の残存病変を評価するアッセイの開発への注力の強化により、予測期間中に次世代シーケンシングの成長が高まる可能性があります。たとえば、2020年 1月、Adaptive BiotechnologiesはGlaxoSmithKlineと協力し、clonoSEQアッセイを使用してGSKの血液学製品ポートフォリオの微小残存疾患(MRD)を評価しました。

北米は予測期間中にかなりの市場シェアを持つと予想される

がんの発生率の増加、最小限の残存疾患を検出するための次世代およびポリメラーゼ連鎖反応技術に対する需要の高まり、最新技術の採用、プロテオミクス、ゲノミクス、腫瘍学の確立された調査インフラストラクチャが、がんの市場の成長を推進する要因です。北米地域。

米国における血液がんの発生率と有病率の増加により、がん細胞が残存するリスクが増加しており、残存疾患を最小限に抑える市場への需要が高まる可能性があります。米国がん協会が発表した2022年の統計によると、2022年の米国における多発性骨髄腫の新規症例数は34,470人です。さらに、同じ情報源によると、2022年の急性リンパ性白血病(ALL)の新規症例数は約6,660人です。白血病・リンパ腫協会が発表した統計によると、2021年には米国の患者で新たに90,390人のリンパ腫症例が診断されると予想されており、このうち8,830人がホジキンリンパ腫、81,560人が非ホジキンリンパ腫となります。

さらに、微小な残存病変を検出するための治療法や検査の開発に企業がますます注力していることも、市場の成長に貢献しています。たとえば、Invitaeは2022年 2月に、さまざまな腫瘍タイプにわたるパーソナライズされた微小残存疾患検査に関する実際のデータを生成する研究を開始しました。同様に、2020年 4月にイニバタは、以前にがんと診断された患者の血漿サンプルにおける残存疾患と再発を検出および監視するためのアッセイ、RaDaRを開始しました。 RaDaRアッセイは、Inivataの実証済みのInVisionリキッドバイオプシープラットフォームテクノロジーに基づいて構築されており、高感度で特異的な変異検出のための組み込み制御とエラー修正を組み込んだ次世代シーケンシングプラットフォームです。

微小残存疾患業界の概要

微小残存疾患市場は競争が激しく、複数の主要企業で構成されています。両社は、より良い治療法と検出法を患者に提供するための研究開発活動に投資しており、市場での地位を留保するために提携や買収などのさまざまなビジネス戦略を採用しています。主要なプレーヤーには、Adaptive Biotechnologies、Bristol-Myers Squibb Company、Natera、Kite Pharma、Amgen Incなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- がんの罹患率の増加

- 研究開発への投資の増加

- 市場抑制要因

- 高額な研究開発費

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 検査手法別

- ポリメラーゼ連鎖反応

- 蛍光In situハイブリダイゼーション(FISH)

- 次世代シーケンシング(NGS)

- 検出対象別

- 白血病

- リンパ腫

- 固形腫瘍

- その他

- エンドユーザー別

- 病院

- 検査センター

- 専門クリニック

- 地域別

- 北米

- 欧州

- アジア太平洋

- 中東とアフリカ

- 南米

第6章 競合情勢

- 企業プロファイル

- Adaptive Biotechnologies

- Bristol-Myers Squibb Company

- Amgen Inc.

- Kite Pharma

- Natera

- SYNIMMUNE GmbH

- Navidea Biopharmaceuticals

- Novartis

- AstraZeneca

- iRepertoire

第7章 市場機会と将来の動向

The Global Minimal Residual Disease Market size is estimated at USD 1.9 billion in 2024, and is expected to reach USD 3.49 billion by 2029, growing at a CAGR of 12.88% during the forecast period (2024-2029).

The COVID-19 pandemic affected healthcare systems globally and resulted in the interruption of usual care in many healthcare facilities, exposing vulnerable patients with cancer to significant risks. Since the beginning of the COVID-19 pandemic, measures have been taken to increase the admissions of covid patients and reduce the number of non-covid patients in the hospitals, leading to postponing the treatment. A study titled 'Impact of the COVID-19 Pandemic on Cancer Care: A Global Collaborative Study' in September 2020 reported that a total of 356 centers from 54 countries across six continents participated between April 21 and May 8, 2020. These centers serve 716,979 new patients with cancer a year. Most of them (88.2%) reported facing challenges in delivering care during the pandemic. Although 55.34% reduced services as part of a preemptive strategy, other common reasons included an overwhelmed system (19.94%), lack of personal protective equipment (19.10%), and staff shortage (17.98%), and restricted access to medications (9.83%). According to an article titled 'What is the Clinical Impact of COVID-19 on Cancer Patients?' in June 2020, the increased vulnerability of cancer patients to COVID-19, particularly to the severe effects of this infectious disease, has led some patients to delay or pause their anti-cancer treatments to reduce their exposure to potentially infected people, and this condition during initial pandemic phase affected the market adversely. Such studies indicate that cancer care was severely impacted, subsequently impacting the market growth. Hence, there is an overall negative impact of the COVID-19 pandemic on the market's growth.

The factors propelling the growth of the minimal residual disease market are the rising prevalence of various types of cancer worldwide and the increasing awareness among people to confirm the presence of carcinogens. The patients undergoing continued cancer treatment are expected to be the most important element driving the minimal residual disease market forward. In addition, the rising adoption of personalized medicines for the treatment and rising research and development activities contribute to the market's growth.

The increasing number of people suffering from various cancers is the key driving factor for the minimal residual disease market growth. For instance, as per the American Society of Clinical Oncology February 2021 report, an estimated 235,760 adults (119,100 men and 116,6600 women) in the United States were expected to be diagnosed with lung cancer. For instance, Globocan, 2020, it found that there are 18.3% new cases of cancers in India, and cervical cancer accounted for 9.4% of all cancers. For instance, according to statistics published by the American Cancer Society (ACS) updates from January 2022, approximately 26,560 new cases of stomach cancer are projected to be detected in the United States in 2021, with 16,160 males and 10,400 women. According to the statistics published by the National Breast Cancer Foundation, in July 2021, approximately 63% of breast cancer patients have been diagnosed with local-stage breast cancer, 27% with regional stage, and 6% with a distant (metastatic) disease.

In addition, the rising prevalence of blood cancer worldwide increases the demand for better treatment options and accuracy in removing the residual cancerous cells, which is likely to increase the demand for a minimal residual disease market. According to the statistics published by the American Cancer Society, in January 2022, 34,920 new cases of multiple myeloma were estimated to be diagnosed in the United States.

However, the high cost of research and development activities will likely hinder the market's growth over the forecast period.

Minimal Residual Disease Market Trends

Next Generation Sequencing (NGS) Segment Expects to Register a Highest CAGR in the Forecast Period

Next-generation sequencing is a technology used to determine the sequence of DNA or RNA to study the genetic variations associated with the disease. It is also called as massively-parallel sequencing as it enables the sequencing to determine the sequencing of many DNA at a particular time.

The factors propelling the growth of next-generation sequencing technology are increasing incidences of cancer globally, rising demand for next-generation sequencing services and applications in drug development, clinical procedures, precision medicines, and adoption of the latest technology established for next-generation sequencing.

Recently, new assays, including next-generation sequencing, were developed to monitor minimal residual disease more precisely in the patients. Next-Generation Sequencing offers greater sensitivity than conventionally employed morphologic and cytogenetic tests. According to an article published by the Journal of Molecular Diagnostics in January 2020, titled 'A New Next-Generation Sequencing Strategy for the Simultaneous Analysis of Mutations and Chromosomal Rearrangements at DNA Level in Acute Myeloid Leukemia Patients' it has been found that the next-generation sequencing offers the promise of detecting all genomic lesions in a single run. In addition, next-generation sequencing applies to every newly diagnosed acute myeloid leukemia because of the frequent prevalence of multiple molecular aberrations among patients.

The introduction of various error-corrected next-generation methodologies has made the detection of minimal residual diseases easy. Molecular barcoding has recently been used to develop several error-corrected next-generation sequencing approaches based on barcoding the individual DNA molecules used for next-generation sequencing library creation. According to an article published by the National Center for Biotechnology Information in June 2021, titled "Minimal Residual Disease Monitoring with Next-Generation Sequencing," it has been found that next-generation sequencing has the potential to reduce the prevalence of undiagnosed minimal residual diseases, allowing for early management, which is critical for Acute lymphocytic leukemia (ALL) patient survival.

Moreover, the companies' investment in research and development activities, adoption of advanced technology, and increasing their focus on developing assays to assess minimal residual disease are likely to increase the growth of next-generation sequencing over the forecast period. For instance, in January 2020, Adaptive Biotechnologies collaborated with GlaxoSmithKline to use its clonoSEQ Assay to assess minimal residual disease (MRD) in GSK's portfolio of hematology products.

North America is Expected to Have the Significant Market Share during the Forecast Period

The increasing incidences of cancer, rising demand for next-generation and polymerase chain reaction techniques for detecting minimal residual diseases, adoption of the latest technology, and established research infrastructure for proteomics, genomics, and oncology are the factors propelling the growth of the market in the North American region.

The increasing incidences and prevalence of hematological cancers in the United States have increased the risk of people having residual cancerous cells, which is likely to increase the demand for minimal residual disease market. According to the statistics published by the American Cancer Society 2022, 34,470 new cases of multiple myeloma in the United States in 2022. In addition, as per the same source, about 6,660 new cases of acute lymphocytic leukemia (ALL) in 2022. As per the statistics published by the Leukemia and Lymphoma Society, in 2021, 90,390 new lymphoma cases were expected to be diagnosed in patients in the United States, of which 8,830 cases would be of Hodgkin lymphoma and 81,560 cases of non-Hodgkin lymphoma.

Moreover, the increasing focus of the companies on developing treatments and tests for detecting minimal residual disease is also contributing to the market's growth. For instance, in February 2022, Invitae launched a study to generate real-world data on personalized minimal residual disease tests across various tumor types. Similarly, in April 2020, Inivata launched an assay, RaDaR, to detect and monitor residual disease and recurrence in the plasma samples of patients previously diagnosed with cancer. The RaDaR assay is built on Inivata's proven InVision liquid biopsy platform technology, a next-generation sequencing platform that incorporates built-in controls and error correction for highly sensitive and specific variant detection.

Minimal Residual Disease Industry Overview

The minimal residual disease market is highly competitive and consists of several major players. The companies are investing in research and development activities to provide patients with better treatment and detection methods and adopt various business strategies such as collaboration and acquisitions to withhold their positions in the market. Some key players are Adaptive Biotechnologies, Bristol-Myers Squibb Company, Natera, Kite Pharma, and Amgen Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Cancer

- 4.2.2 Increasing Investment in Research and Development

- 4.3 Market Restraints

- 4.3.1 High Cost of Research and Development Activities

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Test Technique

- 5.1.1 Polymerase Chain Reaction

- 5.1.2 Fluorescence In Situ Hybridization (FISH)

- 5.1.3 Next Generation Sequencing (NGS)

- 5.2 By Detection Target

- 5.2.1 Leukemia

- 5.2.2 Lymphoma

- 5.2.3 Solid Tumors

- 5.2.4 Others

- 5.3 By End-user

- 5.3.1 Hospitals

- 5.3.2 Laboratory centers

- 5.3.3 Specialty Clinics

- 5.4 Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia-Pacific

- 5.4.4 Middle-East and Africa

- 5.4.5 South America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Adaptive Biotechnologies

- 6.1.2 Bristol-Myers Squibb Company

- 6.1.3 Amgen Inc.

- 6.1.4 Kite Pharma

- 6.1.5 Natera

- 6.1.6 SYNIMMUNE GmbH

- 6.1.7 Navidea Biopharmaceuticals

- 6.1.8 Novartis

- 6.1.9 AstraZeneca

- 6.1.10 iRepertoire