|

市場調査レポート

商品コード

1644297

コンテンツサービスプラットフォーム:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Content Services Platforms - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| コンテンツサービスプラットフォーム:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

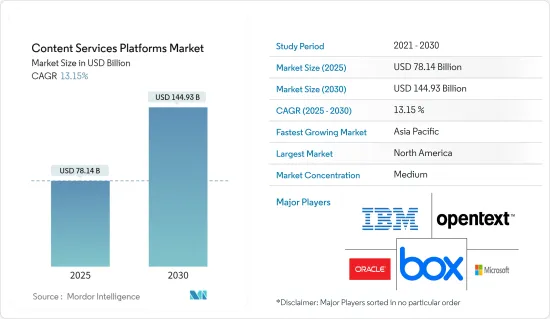

コンテンツサービスプラットフォームの市場規模は、2025年に781億4,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは13.15%で、2030年には1,449億3,000万米ドルに達すると予測されます。

コンテンツサービスプラットフォーム市場を牽引する主な要因としては、ソーシャル、モバイル、アナリティクス、クラウド(SMAC)技術の採用拡大、企業全体でのデジタルコンテンツの普及などが挙げられます。

主なハイライト

- コンテンツサービスプラットフォーム(CSP)は、複数の企業レベルのコンテンツ利用をサポートするために、標準的なアプリケーション・プログラミング・インターフェース(API)とリポジトリを共有する、コンテンツ関連のソリューションとツールの統合セットです。従来のエンタープライズ・コンテンツ管理(ECM)システムの次の進化段階です。

- 多くの組織がペーパーレス化を進めているか、リモートで働く従業員を抱えているか、あるいはその両方であるため、オフィス内の物理的な書類棚や箱に文書や書類を保管するのは非現実的です。クラウドベースの文書管理システムには、コスト削減のメリットがあります。インフラへの初期投資を大幅に削減でき、共有や拡張、サードパーティとの統合も容易です。このため、中小企業はコストとオペレーションの合理化のために、クラウドベースのソリューションを採用するケースが増えています。

- さらに、顧客管理システムとも呼ばれるケース管理システムは、組織が患者のニーズを満たし、プログラムやサービスを提供するために必要なデータをすべて追跡するのに役立ちます。ヘルスケア企業は、さまざまなケース管理のために整流ソリューションを導入しており、ケース管理ソリューションの世界市場の成長にプラスの影響を与えています。

- ヘルスケア業界では、組織が医療保険の相互運用性と説明責任に関する法律(HIPAA)を遵守する必要がある場合、業務提携契約(BAA)を締結するベンダーのケース管理システムを選択することをお勧めします。BAAは、保護されるべき医療情報のプライバシー、セキュリティ、トランスミッション、保管、および使用に関して、組織とベンダーとの間の契約上の合意を確立するものです。

- 組織の共有ドライブにファイルを保管するだけでは、業界のコンプライアンス基準を満たすには不十分です。法的な義務にとどまらず、記録管理戦略は組織の情報ライフサイクルに不可欠です。組織レベルの戦略は、情報の作成、保存、共有、追跡、保護の方法を管理します。

コンテンツサービスプラットフォームの市場動向

オンプレミス型が優位な地位を占める

- オンプレミス型は、予測期間中の市場成長に大きく貢献すると予測されます。CSPソリューションのオンプレミス展開では、企業による初期投資が高額になるが、クラウド展開のように所有期間を通じてコストを増加させる必要はないです。

- 昨今、企業データはモバイル・デバイスから簡単にアクセスできるようになった。このため、ビジネス関係者間のデータ転送量が増加し、サイバー攻撃やデータ損失のリスクが高まっています。そのため、顧客の個人データに関連するセキュリティ上の懸念が、クラウドではなくオンプレミスの導入を選択する重要な理由となっています。この種の導入は、大企業全体に広がっています。

- 例えば、シスコシステムズによると、2022年には世界の消費者のIPトラフィック・データ量は、CAGR27%で月間333エクサバイトに達すると予想されています。

- さらに、ロシアのモバイルインターネット経由のデータ転送量は継続的に増加しています。2021年には、モバイル・データ・トラフィック量は前年比で131%増加しました。

- オンプレミスを導入することで、ユーザーはソリューションを社内で維持し、組織にとって理にかなった形で成長させることができます。オンプレミス・ソリューションは、自社のインフラ、IT部門、またはその他のリソース上に存在し、自社のソリューションを維持・進化させます。オンプレミスの導入は、社内でECMソリューションのエキスパートになれることを意味し、ソリューションの変更や機能強化はユーザーの手元で行うことができます。

- さらに、インドのような国々では、組織情報の完全性、機密性、入手可能性に対する脅威が急激に高まっています。そのため、顧客の情報セキュリティ全体を確立、実装、運用、監視、レビュー、維持、改善するために、ビジネス・リスク・アプローチに基づく標準化された情報セキュリティ・モデルの提供に注力することが必須となっています。

アジア太平洋地域が大きな市場シェアを獲得する見込み

- アジア太平洋地域では、インドや中国などの経済発展途上国でデータトラフィックが増加し、整理する必要のあるデータや情報が急速に増加していることから、市場の急成長が見込まれています。

- また、日本のような国々では、高齢化や人口減少に伴う生産性や労働力不足への懸念が高まっており、あらゆる分野でデジタル化が進んでいます。加えて、日本政府は2026年の国立公文書館の新館開館までに、ほとんどの公文書をデジタル管理に移行する計画であり、政府の成長を妨げてきた記録管理問題の防止を目指しています。

- 同地域ではクラウドの導入が急ピッチで進んでおり、予測期間中の市場成長にプラスの影響を与えると予想されます。さらに、シンガポールはアジア太平洋(APAC)で最もクラウド対応が進んでいる地域の1つです。アジアクラウドコンピューティング協会(ACCA)のクラウド対応指数(CRI)の最新版では、香港を抜いてトップに立った。さらに、シンガポール政府は、市民サービスをより迅速かつ安価に提供するための継続的な取り組みとして、予測期間中にITシステムの大部分を商用クラウドサービスに移行すると予想されています。これは市場の成長にプラスの影響を与えると予想されます。

- 公開会社がデジタルイニシアチブを改善しようとしているため、公開クラウド設備はこの地域で大きな勢いを見せています。コンテンツサービスプラットフォームは、企業の俊敏性を高め、顧客に対応するために、企業が機能するための本質となっています。組織はまた、実装効率を最適化し、優れた顧客体験を確保するために協力しています。

- デジタルトランスフォーメーションは、急速に複数の国で最優先事項となっており、その取り組みをサポートする正式な戦略を実施する企業が増えていることから、急速に進んでいます。

コンテンツサービスプラットフォーム業界の概要

コンテンツサービスプラットフォーム市場の競争は中程度で、複数の大手企業で構成されています。現在、市場シェアで市場を独占している大手企業はほとんどないです。コンテンツサービスプラットフォーム市場の主要企業には、Hyland、OpenText、Box、Laserfiche、Adobe、IBM、Nuxeo、Objectiveなどがあります。市場で顕著なシェアを持つこれらの有力企業は、海外における顧客基盤の拡大に注力しています。これらの企業は、戦略的な協業アクションを活用して市場シェアを向上させ、収益性を高めています。

2022年8月、オープンテキストはセールスフォースAppExchangeに新たに3つのソリューションを追加すると発表しました。これにより、AppExchangeで提供されるソリューションは合計6種類となり、あらゆる規模の顧客がオープンテキストのコンテンツサービスプラットフォームのガバナンス、生産性、効率性のメリットを享受できるようになりました。OpenText Core Contentは、Salesforceのようなプログラムと連携するSaaSプラットフォームを使用し、企業の情報管理を支援する最新の作業を容易にします。

2022年6月、Box Inc.はSalesforce AppExchangeにおけるBox for Salesforce統合の強化を発表し、Salesforceにおける署名ベースのプロセスやワークフローのコンテンツ管理ソリューションとしてBoxを利用できるようになりました。顧客は、Box Signの機能を利用することで、Salesforceから署名用のBoxファイルを直接送信することができます。このエディションには、共同利用者がどこからでも簡単に契約を締結・実行できるようにする新機能と開発者ツールも含まれています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- 市場促進要因

- SMAC技術の採用増加

- 企業全体におけるデジタルコンテンツの増加

- コンテキスト化されたユーザー体験の提供に対する需要

- 市場抑制要因

- データプライバシーとセキュリティへの懸念

- COVID-19が業界に与える影響の評価

第5章 市場セグメンテーション

- コンポーネント別

- ソリューション/ソフトウェア

- 文書・記録管理

- データキャプチャー

- ワークフロー管理

- 情報セキュリティとガバナンス

- ケース管理

- その他のソリューション

- サービス

- 統合と展開

- コンサルティング

- サポートとメンテナンス

- ソリューション/ソフトウェア

- 展開タイプ別

- オンプレミス

- クラウド

- 組織規模別

- 中小企業

- 大企業

- エンドユーザー業界別

- BFSI

- 政府・公共機関

- ヘルスケア・ライフサイエンス

- IT・通信

- 運輸・物流

- その他のエンドユーザー業界別

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第6章 競合情勢

- 企業プロファイル

- IBM Corporation

- Microsoft Corporation

- OpenText Corporation

- Box Inc.

- Oracle Corporation

- Hyland Software Inc.

- Laserfiche Inc.

- Hewlett Packard Enterprise(Micro Focus)

- Adobe Systems Inc.

- M-Files Inc.

- Newgen Software Technologies Limited

- Fabasoft AG

- Everteam SAS

- DocuWare Corporation

- Alfresco Software Inc.

第7章 投資分析

第8章 市場の将来

The Content Services Platforms Market size is estimated at USD 78.14 billion in 2025, and is expected to reach USD 144.93 billion by 2030, at a CAGR of 13.15% during the forecast period (2025-2030).

The major factors driving the content services platform market include the growing adoption of social, mobile, analytics, and cloud (SMAC) technologies and the proliferation of digital content across enterprises.

Key Highlights

- Content service platforms (CSP) are an integrated set of content-related solutions and tools that share standard application programming interfaces (APIs) and repositories to support multiple enterprise-level content usage. They are the next evolutionary phase of traditional enterprise content management (ECM) systems.

- Many organizations are going paperless, having remote employees, or both, making it unrealistic to keep documents and paperwork in physical filing cabinets or boxes in an office. A cloud-based document management system offers cost-saving benefits. It reduces substantial initial capital investment in infrastructure and provides easy sharing, scalability, and integration with third parties. Due to this, SMEs are increasingly adopting cloud-based solutions to streamline their costs and operations.

- Further, case management systems, also called client management systems, help an organization track all the necessary data to meet constituent needs and provide them with programs and services. Healthcare enterprises are deploying rectification solutions for a variety of case management, positively impacting the growth of the global case management solution market.

- In the healthcare industry, if an organization needs to comply with the Health Insurance Portability and Accountability Act (HIPAA), it may want to choose a case management system from a vendor that will sign a Business Associates Agreement (BAA). A BAA establishes a contractual agreement between an organization and the vendor regarding the privacy, security, transmission, storage, and use of protected health information.

- Storing files on an organization's shared drive is insufficient to meet industry compliance standards. Beyond legal mandates, records management strategy is vital to an organization's information life cycle. The strategy at an organizational level will govern how information is created, stored, shared, tracked, and protected.

Content Services Platforms Market Trends

The On-premises Deployment Mode Holds a Dominant Position

- The on-premises deployment type is anticipated to contribute to the market growth during the forecast period significantly. On-premise deployment of CSP solutions requires initial high investment by organizations, though it does not require incremental costs throughout the ownership, as in the cloud deployment type.

- Nowadays, corporate data can be accessed effortlessly from mobile devices; this has raised the amount of data transfer between business parties and has increased the risks of cyber-attacks and data losses. Therefore, security concerns associated with customers' private data are an important reason for the selection of on-premises deployment over the cloud. These kinds of implementations are widespread across large-sized enterprises.

- For instance, according to Cisco Systems, in 2022, worldwide consumer IP traffic data volume was expected to reach 333 exabytes per month at a 27% compound annual growth rate.

- Moreover, Russia's volume of data transferred via mobile internet continuously increased. In 2021, the mobile data traffic volume increased by 131% compared to the previous year.

- Deploying on-premises allows users to keep the solution in-house and grow the solution as it makes sense for the organization. An on-premises solution lives on one's infrastructure, IT department, or other resources and maintains and evolves one's solution. An on-premises deployment means one can become the in-house expert on ECM solutions, and changes and enhancements to one's solution are at the user's fingertips.

- Moreover, the threats to the integrity, confidentiality, and obtainability of organization information are increasing exponentially in countries such as India. Thus, it has become mandatory to focus on providing a standardized information security model based on a business risk approach to establish, implement, operate, monitor, review, maintain, and improve overall information security for customers.

Asia-Pacific is Expected to Gain Significant market Share

- In the Asia-Pacific region, the market is anticipated to witness rapid growth, owing to the increasing data traffic and rapidly growing data and information that needs to be organized in economically developing countries, such as India and China.

- Also, the increasing concern about productivity and shortage of labor with a greying and shrinking population in countries like Japan is driving such nations toward digitalization in every sector. In addition, the Japanese government plans to shift toward digital management of most public records by the time the new National Archives of Japan building opens in 2026, aiming to prevent the record management problems that have hindered the growth of the government.

- Cloud adoption in the region is increasing at a rapid pace, which is expected to impact the market growth over the forecast period positively. Moreover, Singapore is one of the most cloud-ready regions in Asia-Pacific (APAC). It overtook the position of Hong Kong in the latest iteration of the Asia Cloud Computing Association's (ACCA) Cloud Readiness Index (CRI). Additionally, Singapore's government is anticipated to move the bulk of its IT systems to commercial cloud services over the forecast period in ongoing efforts to deliver citizen services faster and cheaper. This is anticipated to impact the market growth positively.

- Public cloud facilities have achieved enormous momentum in the region as companies are trying to improve their digital initiatives. Content service platforms have become the essence of how companies function nowadays to attain higher company agility and meet their clients. Organizations are also collaborating to optimize implementation efficiency and ensure excellent client experience.

- Digital transformation is rapidly becoming a top priority in multiple countries and moving rapidly as a greater number of companies are implementing formal strategies to support their efforts.

Content Services Platforms Industry Overview

The Content Services Platforms Market is moderately competitive and consists of several major players. Few of these major players currently dominate the market in terms of market share. Some major companies in the Content Services Platforms Market include Hyland, OpenText, Box, Laserfiche, Adobe, IBM, Nuxeo, and Objective, among others. These influential players with a noticeable share in the market are concentrating on expanding their customer base across foreign countries. These businesses leverage strategic collaborative actions to improve their market percentage and enhance profitability.

In August 2022, OpenText announced the addition of three new solutions to the Salesforce AppExchange. This brought the total number of AppExchange offerings to six and enabled customers of any size to benefit from the governance, productivity, and efficiency of the OpenText content services platform. OpenText Core Content uses a SaaS platform that interfaces with programs like Salesforce to facilitate modern work to assist enterprises in managing information.

In June 2022, Box Inc. announced the enhancement of the Box for Salesforce integration on the Salesforce AppExchange, enabling customers to use Box as the content management solution for signature-based processes and workflows in Salesforce. Customers can send Box files for signature directly from Salesforce by utilizing the capability of Box Sign. New features and developer tools that make it simple for joint customers to establish and execute agreements from any location are also a part of this edition.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

- 4.3 Market Drivers

- 4.3.1 Increasing Adoption of SMAC Technologies

- 4.3.2 Increase of Digital Content across the Enterprises

- 4.3.3 Demand for Delivering Contextualized User Experience

- 4.4 Market Restraints

- 4.4.1 Data Privacy and Security Concerns

- 4.5 Assessment of the Impact of COVID-19 on the Industry

5 MARKET SEGMENTATION

- 5.1 By Component

- 5.1.1 Solutions/Software**

- 5.1.1.1 Document and Records Management

- 5.1.1.2 Data Capture

- 5.1.1.3 Workflow Management

- 5.1.1.4 Information Security and Governance

- 5.1.1.5 Case Management

- 5.1.1.6 Other Solutions

- 5.1.2 Services**

- 5.1.2.1 Integration and Deployment

- 5.1.2.2 Consulting

- 5.1.2.3 Support and Maintenance

- 5.1.1 Solutions/Software**

- 5.2 By Deployment Type

- 5.2.1 On-Premises

- 5.2.2 Cloud

- 5.3 By Organization Size

- 5.3.1 Small and Medium-Sized Enterprises

- 5.3.2 Large Enterprises

- 5.4 By End-user Industry Vertical

- 5.4.1 BFSI

- 5.4.2 Government and Public Sector

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 IT and Telecom

- 5.4.5 Transportation and Logistics

- 5.4.6 Other End-user Industry Verticals

- 5.5 Geography

- 5.5.1 North America

- 5.5.2 Europe

- 5.5.3 Asia-Pacific

- 5.5.4 Latin America

- 5.5.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 IBM Corporation

- 6.1.2 Microsoft Corporation

- 6.1.3 OpenText Corporation

- 6.1.4 Box Inc.

- 6.1.5 Oracle Corporation

- 6.1.6 Hyland Software Inc.

- 6.1.7 Laserfiche Inc.

- 6.1.8 Hewlett Packard Enterprise (Micro Focus)

- 6.1.9 Adobe Systems Inc.

- 6.1.10 M-Files Inc.

- 6.1.11 Newgen Software Technologies Limited

- 6.1.12 Fabasoft AG

- 6.1.13 Everteam SAS

- 6.1.14 DocuWare Corporation

- 6.1.15 Alfresco Software Inc.