アジア太平洋のコンテンツサービスプラットフォーム- 市場シェア分析、産業動向、成長予測(2025年~2030年)

Asia Pacific Content Services Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 134 Pages

- 納期

- 2~3営業日

- 商品コード

- 1644484

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

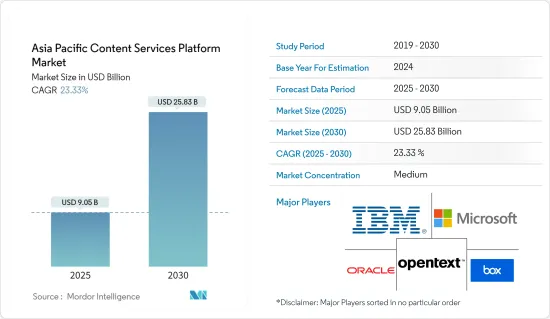

アジア太平洋のコンテンツサービスプラットフォーム市場規模は、2025年に90億5,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは23.33%で、2030年には258億3,000万米ドルに達すると予測されます。

アジア太平洋では、中国やインドなどの経済発展途上国におけるデータトラフィックの増加や、整理する必要のあるデータや情報の継続的な増加により、市場の急激な成長が見込まれています。

主要ハイライト

- インターネット接続ユーザーの増加、中小企業やクラウドサービスベンダーの増加により、アジア太平洋には大きな成長機会がもたらされています。同地域では、相互接続の帯域幅も急激に拡大しています。例えば、エクイニクスによると、アジア太平洋は、都市化の進展により、年率51%で拡大し、世界の相互接続帯域幅の27%以上を占めると予想されています。

- 加えて、より良い顧客体験を提供したいという需要の高まりや、人口のスマート技術利用の増加、コンテキスト化されたユーザー体験を提供したいというニーズの高まり、複数の企業におけるデジタルコンテンツの増加なども、市場を強化する重要な要因の1つとなっています。さらに、予測期間中、エンドツーエンドのクロスプラットフォームソリューションの採用が増加し、RPAとCSPソリューションの統合が進み、サービスの技術開発と近代化が進むことで、アジア太平洋のコンテンツサービスプラットフォーム市場に新たな成長の可能性と機会がもたらされます。

- さらに、モバイル、ソーシャルメディア、分析、クラウド技術の採用が増加し、さまざまな企業でデジタルコンテンツが普及していることが、同地域のコンテンツサービスプラットフォーム産業を強化しています。アジア太平洋におけるクラウドの導入は非常に速いペースで成長しており、予測期間中に調査した市場の成長にプラスの影響を与えると予想されます。また、シンガポールはアジア太平洋で最もクラウド対応が進んでいる地域の1つです。アジアクラウドコンピューティング協会(ACCA)のクラウド対応指数(CRI)の最新版では、香港を抜いてトップに立った。また、シンガポール政府は、市民サービスをより安価で迅速な方法で提供するための継続的な取り組みの一環として、予測期間中にITシステムの大部分を商用クラウドサービスに移行するとみられ、市場の成長にプラスの影響を与えます。

- 一方、データプライバシーやセキュリティに関する懸念の高まりは、市場の成長を阻害する大きな要因となっています。また、CSP戦略と組織の戦略的イニシアチブの整合性が継続的に高まっていることも、予測期間を通じてコンテンツサービスプラットフォーム市場へのさらなる課題となる可能性があります。

- COVID-19の流行は、クラウドベースの技術に移行し、従業員へのコンテンツフローの維持と実装の必要性が高まるにつれてプロセス全体が強化されたため、市場の調査にプラスの影響を与えました。また、政府機関も業務の電子化とデジタル化を余儀なくされました。例えばインドでは、Aarogya Setuをはじめ、National e-Health Authorityや新しい遠隔医療ガイドラインなどの関連イニシアチブが、2022年までの完成を目指すNational Health Stackに向けてまとまりつつあります。

アジア太平洋のコンテンツサービスプラットフォーム市場動向

ソリューションソフトウェアセグメントが最大市場シェアを占める見込み

- クラウドコンピューティングは、一般的なデータストレージに革命をもたらし、文書管理システムにも多大な影響を与えました。アジア太平洋では、紙への依存を最小限に抑えるため、文書のデジタル管理が急速に普及しています。また、中国のような数カ国では、人件費の削減や作業効率の向上など、企業経営の重要な動機となっています。

- 最近では、中国の税関総署(GAC)がペーパーレス通関試行改革を開始し、コンピュータやその他のさまざまな電子媒体を通じて通関申告情報を転送・保存し、自動的に確認できるようにしました。GACはまた、中国の国家通関統合改革を支援し、通関の全体的な効率を向上させるため、価格審査のための通関書類のペーパーレス化を推進していました。さらに、中国では、輸送・貿易部門における違法伐採を抑制するために文書管理ソリューションを導入する必要性も高まっており、DMSの需要全体が高まると予想されています。

- さらに、インドではデジタルトランスフォーメーションやインテリジェントデバイスの普及に伴い、環境に対する関心が高まっており、インドではペーパーレス化が進み、文書管理ソリューションの迅速な導入が進んでいます。インド政府の主要部門は、全面的または部分的にオフライン・オンライン文書管理システムに移行しています。最近では、Lok Sabhaが樹木の節約とコスト削減のために下院のペーパーレス化を宣言し、国会議員がデジタル文書を活用して質問を書くようになりました。インドの教育機関も、安全のために文書管理ソリューションを導入しています。例えば、インドの教育機関であるManipal Academy of Higher Education(MAHE)は、記録や情報を管理・整理し、より効率的にデータを蓄積するため、ペーパーレス文書管理システムに移行しました。

- また、日本のような国々では、生産性への関心の高まりや、人口減少と高齢化に伴う労働力不足が、あらゆるセグメントでのデジタル化に拍車をかけています。さらに、日本政府は、政府全体の成長を制限してきた記録管理の問題を防ぐことを目的として、2026年の国立公文書館の新館開館までに、ほとんどの公文書のデジタル管理への移行を計画しています。さらに、オーストラリアは他のアジア太平洋諸国よりも早くペーパーレス化への支持を得ました。例えば、オーストラリア税務局(ATO)は2002年にデジタル申告の支持を表明しました。電子記録保存のガイドラインとなる一連の税務規則を制定しました。

- さらに、オーストラリア政府評議会(COAG)の医療評議会を通じてすべての準州と州が承認した国家デジタルヘルス戦略は、医療産業における紙ベースのメッセージングを根絶することを優先しています。同局は、ソフトウェア産業や医療プロバイダーと協力し、医療情報の安全な交換を改善する標準の開発に取り組んできました。このシステムは、5つの異なる人に繰り返し病状を説明するフラストレーションを回避し、医療専門家が安全かつ迅速に情報を共有できるようにするため、個人と顧客に利益をもたらします。

IT、電気通信、小売、eコマース部門が急成長へ

- 通信産業は、コンテンツ、顧客チャネル、通信サービスがデジタル化され、新たなバリュー・エコシステムが形成されるなど、大きな構造変化を遂げつつあります。現代のデジタル時代において、様々なプロバイダーが顧客のニーズを満たすために高性能なネットワークを構築しています。このような構造的変化は、このセグメント全体のワークフロー管理サービスに新たな機会をもたらしています。ネットワーク技術とデバイスの強化が進むことで、市場におけるさまざまなIoTコンテンツサービスプラットフォームの範囲も広がっています。GSMAによると、IoTと統合された電力広域ネットワークの早期導入により、2026年までに総額1兆8,000億米ドルが創出されると予想されています。

- デジタルトランスフォーメーションの実施と所有に伴い、デジタルトランスフォーメーションの大部分はIT部門によって広く推進されています。データ接続の増加に伴い、ベンダーはクラウドやIoTベースのコンテンツサービスプラットフォームをビジネスに広く採用し、ウェブコンテンツの管理や作成を支援しています。CMSはまた、訪問者のアクティビティや検索など、ウェブトラフィックの追跡と管理も可能にします。

- さらに、Archive Oneは、重要な文書を自動的に検索、保護、分類、保存し、監査ツールとして機能する文書管理ソフトウェアです。一般的に数,000人の従業員を抱えるIT-BPMセグメントでは非常に有用で、追跡すべきデータが大量にあります。また、Paperless Trail Inc.は、技術の進歩によって組織が直面する課題に対応するため、ビジネスの新常識を受け入れ、文書管理とコンプライアンスをデジタル空間に効果的に移行することの重要性を強調しています。

- 同市場では、クラウド、オンプレミス、ハイブリッドの各モデルに対応する、アジア太平洋を中心とした販売契約が進んでいます。例えば、2021年7月、テックデータとシニティはアジア太平洋で新たな販売提携を結びました。この提携により、アジア太平洋の企業は、クラウド、オンプレミス、ハイブリッドモデルなど、さまざまな方法でSyniti Data Replicationを導入できるようになります。

- さらに、Syniti Data Replicationは、ビジネスクリティカルなシステムの応答性を阻害することなく、データウェアハウス、分析、その他のアプリケーションに対応するデータの一貫したコピーを提供する、ロータッチで柔軟なソリューションです。その多様なチェンジ・データキャプチャー(CDC)は、ビジネスデータを確実に更新し、リアルタイムのパフォーマンス・レポートや分析システムを支援します。これは、データと分析能力を強化し、大規模な市場参入イニシアチブを可能にするという点で、企業を支援します。

アジア太平洋のコンテンツサービスプラットフォーム産業概要

アジア太平洋のコンテンツサービスプラットフォーム市場全体は適度にセグメント化されており、Microsoft Corporation、IBM Corporation、Oracle Corporation、OpenText Corporationなど少数の参入企業が大きな市場シェアを占めています。これらの企業は、収益性を拡大し市場シェアを最大化するために、さまざまな戦略的イノベーションと共同イニシアティブを活用しています。企業全体でデジタルコンテンツが広く採用されていることが、調査対象の市場を大きく拡大すると予想されます。

- 2022年3月-Adobeは、医療企業がカスタマイズ型安全なデジタル体験とシームレスなカスタマージャーニーを提供できるようにするソリューション、Adobe Experience Cloud for Healthcareの一般提供を宣言。

- 2021年9月-IntalioはOn-OneTech(Pty)Ltdとの提携を宣言し、アフリカへの地理的リーチを拡大。この提携により、Intalioは、アフリカの医療産業への販売とサポート、アフリカ全域の医療組織の変革が可能になり、主要市場を超えた幅広い地理的リーチを記載しています。

- 2021年7月-EYとIBMは、主に組織がデジタルトランスフォーメーションを後押しし、クライアントの成果を向上させることを支援することを目的とした、強化された世界の複数年の提携を発表しました。この提携には、Red Hat OpenShiftのさまざまなハイブリッドクラウド機能、IBM Watson、IBM Blockchain、IBMの5Gとエッジ技術の活用が含まれます。両社の専門家は共に、顧客のビジネスの近代化と変革の支援に注力することができます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

第5章 市場力学

- 市場促進要因

- SMAC技術の採用増加

- 企業全体におけるデジタルコンテンツの増加

- コンテキスト化されたユーザー体験の提供に対する需要

- 市場抑制要因

- データプライバシーとセキュリティへの懸念

第6章 市場セグメンテーション

- コンポーネント別

- ソリューション/ソフトウェア

- 文書・記録管理

- データキャプチャ

- ワークフロー管理

- 情報セキュリティとガバナンス

- ケース管理

- その他のソリューション

- サービス別

- ソリューション/ソフトウェア

- 導入タイプ別

- オンプレミス

- クラウド

- 組織規模別

- 中小企業

- 大企業

- エンドユーザー産業別

- BFSI

- 政府・公共機関

- 医療ライフサイエンス

- IT、通信、小売、eコマース

- 運輸・物流

- その他

- 国別

- インド

- 中国

- 日本

- 韓国

- その他のアジア太平洋

第7章 競合情勢

- 企業プロファイル

- IBM Corporation

- Microsoft Corporation

- OpenText corporation

- Box Inc.

- Oracle Corporation

- Hyland Software Inc.

- Laserfiche Inc.

- Hewlett Packard enterprise(Micro Focus)

- Adobe Systems Inc.

- M-Files Inc.

第8章 投資分析

第9章 市場の将来

目次

The Asia Pacific Content Services Platform Market size is estimated at USD 9.05 billion in 2025, and is expected to reach USD 25.83 billion by 2030, at a CAGR of 23.33% during the forecast period (2025-2030).

In the Asia Pacific region, the market is expected to witness exponential growth, owing to increasing data traffic and continously growing data and information that requires to be organized in economically developing countries, such as China and India.

Key Highlights

- The rising growth of Internet-connected users, with a growing number of SMEs and cloud service vendors, provides significant growth opportunities in the Asia Pacific region. The interconnection bandwidth is also accelerating drastically in the region. For instance, according to Equinix, the Asia Pacific region is expected to expand by 51% per annum, accounting for over 27% of interconnection bandwidth globally, owing to a rise in urbanization.

- In addition, the rising demand to provide better customer experience, as well as rising usage of smart technologies among the population, growing need for delivering contextualized user experience, and rise in the of digital content across several enterprises, are among the vital factors enhancing the market. Moreover, during the projection period, rising adoption of end-to-end, cross-platform solutions, rise in the integration of RPA with CSP solutions, and growing technological developments and modernization in the services will offer new growth possibilities and apportunities for the market for Asia Pacific content services platform.

- Further, the rise in the adoption of mobile, social media, analytics, cloud technologies and the proliferation of digital content across various companies are enhancing the content services platform industry in the region. Cloud adoption in the Asia Pacific region is growing at a very rapid pace, which is anticipated to impact the growth of the market studied positively over the forecast period. In addition, Singapore is one of the most cloud-ready regions within the Asia-Pacific region. It overtook the position of Hong Kong in the latest iteration of the Asia Cloud Computing Association's (ACCA) Cloud Readiness Index (CRI). Additionally, Singapore's government is expected to move the bulk of its IT systems to commercial cloud services over the projection period as part of ongoing efforts to provide citizen services in a cheaper and faster and way, thereby positively influencing the growth of the market.

- In contrast, rising data privacy and security related concerns are significant factors, among others impeding the market growth. Also, the continously increasing aligning of CSP strategy with the strategic initiatives of organizations may further challenge the content services platforms market throughout the forecasted time period.

- The COVID-19 pandemic impacted the market studied positively, as people move to the cloud- based technologies and the whole process was enhanced with the rising need to maintain and implement content flow to employees. Also, government bodies were forced to adopt electronic means of operations and digitalization. For instance, in India, Aarogya Setu and other allied initiatives, like the National e-Health Authority and new tele-medicine guidelines, are coalescing toward a National Health Stack, which is aimed to be completed by 2022.

APAC Content Services Platform Market Trends

The Solution and Software Segment is Expected to Accounted for the Largest Market Share

- Cloud computing has well revolutionized data storage in general and has a profound impact on document management systems, thus, ensuring that documents are well available at any time, anywhere, allowing for scalability, making it a solution for both large and small businesses. The Asia Pacific region is experiencing rapid adoption of digital management of documents to minimize its dependence on paper. Also, in a several few countries, such as China, it has resulted in cutting labor costs and fueled work efficiency, which are the significant motives to run businesses.

- In the recent times, China's General Administrative of Customs (GAC) launched the Paperless Customs Clearance Pilot Reform, enabling customs declaration information to be transferred and stored through computers and various other electronic media that can be reviewed automatically. GAC also had promoted paperless customs documents for price reviews to assist China's national customs clearance integration reform and improvise customs clearance's overall efficiency. Moreover, China has also been seeing an increased need to adopt document management solutions to curtail the illegal logging in the transport and trade sectors, which is anticipated to enhance the overall demand for DMS.

- Further, there have been rising environmental concerns in line with digital transformation and growing adoption of intelligent devices in India, which is enhancing the paperless trend in India and resulting in the quick adoption of document management solutions. Some of the key sectors of the Indian Government have either entirely or partially moved to Offline and Online Document Management Systems. In the recent times, Lok Sabha declared that the lower house has become paperless to save trees and cut costs, with Members of Parliaments utilising digital documents to write questions. Educational institutions in India have also been executing document management solutions for safety purposes. For example, Manipal Academy of Higher Education (MAHE), an educational institution in India, moved to a paperless document management system to manage and organize their records and information and to build up data more effectively.

- Also, the rising concern about productivity and the lack of labor with a shrinking and greying population in countries like Japan are fueling such nations toward digitalization in every sector. Additionally, the Japanese Government plans to shift toward digital management of most public records by the time the new National Archives of Japan building opens in 2026, aiming to prevent the record management problems that have restricted the overall growth of the Government. Moreover, Australia gained the support for a paperless way back than other Asia-Pacific countries. For instance, the Australian Taxation Office (ATO) affirmed its support of digital filing in 2002. It executed a series of Tax Rulings that would act as a guideline for electronic record keeping.

- Moreover, the National Digital Health Strategy, approved by all the territories and states through the Council of Australian Governments (COAG) Health Council, prioritizes eradicating paper-based messaging in the healthcare industry. The Agency has been operating with the software industry and healthcare providers in developing standards that will improvise the secure exchange of healthcare information. This system will benefit the individuals and the customers as it will avoid the frustration of repeatedly explaining their condition to 5 different people and allow healthcare professionals to share information securely and quickly.

IT, Telecom, Retail, and E-commerce Segment to Witness Fastest Growth

- The telecommunications industry is undergoing a significant structural change, with content, customer channels, and communication services becoming digital, thereby resulting in creating a new value ecosystem. In the modern digital era, various providers are executing high-performance networks to fulfill the needs of their customers. Such structural changes are building new opportunities for workflow management services in the entire sector. The increasing enhancement of networking technologies and devices also widens the scope for various IoT content service platforms in the market. As per GSMA, early adoption of power-wide area networks integrated with IoT is anticipated to create a total sum of USD 1.8 trillion by the year 2026.

- With the implementation and ownership of digital transformation, the majority of the digital transformation is widely driven by the IT sector. With the increased data connectivity, vendors are widely adopting cloud and IoT-based content service platforms into the business to assist in managing and creating web content. CMS also allows tracking and management of web traffic, including visitor activities and searches.

- Moreover, Archive One, a document management software that acts as an auditing tool by automatically retrieving, securing, classifying, and storing critical documents. It is highly useful in the IT-BPM sector, where companies typically employ thousands of people, giving them a great amount of data to track. Also, Paperless Trail Inc. emphasizes the importance of embracing the new normal in business and effectively moving document management and compliance to the digital space in response to the challenges organizations face owing to technological advancements.

- The market is seeing an APAC-focused distribution agreement catering to the cloud, on-premises, and hybrid models. For example, in July 2021, Tech Data and Syniti have formed a new distribution alliance in the Asia-Pacific region. The collaboration allows enterprises in the Asia-Pacific to deploy Syniti Data Replication in various ways, including cloud, on-premises, and hybrid models.

- Moreover, Syniti Data Replication, a low-touch, flexible solution that offers a consistent copy of data ready for data warehousing, analytics, and other applications while not interfering with the responsiveness of business-critical systems. Its diversified Change Data Capture (CDC) ensures that business data is kept updated to assist real-time performance reporting and analytics systems. This will help the businesses in terms of strengthening their data and analytics capabilities and enabling large-scale go-to-market initiatives.

APAC Content Services Platform Industry Overview

The entire Asia Pacific content services platform market is moderately fragmented, with few participants like Microsoft Corporation, IBM Corporation, Oracle Corporation, OpenText Corporation, etc., holding a significant market share. These firms are leveraging various strategic innovations and collaborative initiatives to expand their profitability and maximise their market share. The wide adoption of digital content across enterprises is anticipated to be a significant amplifier of the market studied.

- March 2022 - Adobe declared the general availability of Adobe Experience Cloud for Healthcare, a solution that empowers healthcare enterprises to offer secure digital experiences and seamless customer journeys with customised and secured digital experiences.

- September 2021 - Intalio declares its partnership with On-OneTech (Pty) Ltd to expand its geographic reach to Africa. This partnership will provide Intalio with a wider geographic reach to go beyond its key markets, with the ability to sell to and support the African healthcare industry and transform healthcare organizations across Africa.

- July 2021 - EY and IBM stated an enhanced, global, multi-year alliance primarily designed to help organizations boost their digital transformation and improve client outcomes, which include leveraging the various hybrid cloud capabilities of Red Hat OpenShift, as well as IBM Watson, IBM Blockchain, and IBM's 5G and edge technologies. Together, both the company's professionals may focus on helping the clients in modernizing and transforming their businesses.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of SMAC Technologies

- 5.1.2 Increase of Digital Content Across the Enterprises

- 5.1.3 Demand for Delivering Contextualized User Experience

- 5.2 Market Restraints

- 5.2.1 Data Privacy and Security Concerns

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Solution/Software

- 6.1.1.1 Document and Records Management

- 6.1.1.2 Data Capture

- 6.1.1.3 Workflow Management

- 6.1.1.4 Information Security and Governance

- 6.1.1.5 Case Management

- 6.1.1.6 Other Solutions

- 6.1.2 Services

- 6.1.1 Solution/Software

- 6.2 By Deployment Type

- 6.2.1 On-premise

- 6.2.2 Cloud

- 6.3 By Organization Size

- 6.3.1 Small and Medium-sized Enterprises

- 6.3.2 Large Enterprises

- 6.4 By End-user Industry

- 6.4.1 BFSI

- 6.4.2 Government and Public Sector

- 6.4.3 Healthcare and Life Sciences

- 6.4.4 IT, Telecom, Retail, & E-commerce

- 6.4.5 Transportation and Logistics

- 6.4.6 Other End-user Industries

- 6.5 By Country

- 6.5.1 India

- 6.5.2 China

- 6.5.3 Japan

- 6.5.4 South Korea

- 6.5.5 Rest of Asia Pacific

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Microsoft Corporation

- 7.1.3 OpenText corporation

- 7.1.4 Box Inc.

- 7.1.5 Oracle Corporation

- 7.1.6 Hyland Software Inc.

- 7.1.7 Laserfiche Inc.

- 7.1.8 Hewlett Packard enterprise (Micro Focus)

- 7.1.9 Adobe Systems Inc.

- 7.1.10 M-Files Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 134 Pages

- 納期

- 2~3営業日