|

市場調査レポート

商品コード

1689974

艦艇:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Naval Vessels - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 艦艇:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 181 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

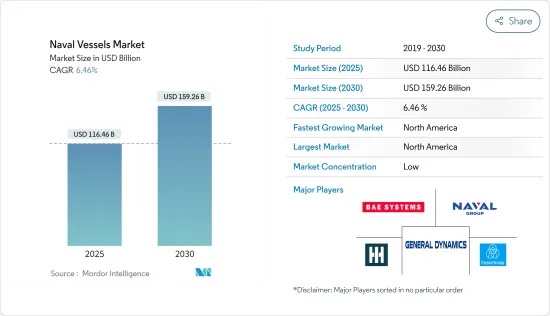

艦艇の市場規模は2025年に1,164億6,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは6.46%で、2030年には1,592億6,000万米ドルに達すると予測されます。

国家間の地政学的緊張や海洋紛争が高まるにつれ、各国は海軍力の強化に努めています。いくつかの国は、既存の海軍艦隊をアップグレードしたり、老朽化した艦隊を高度な機能を備えた新世代の船舶に置き換えたりしています。過去10年間に数カ国が国防費を増加させたことで、業界は大規模な調達・開発活動を目の当たりにしました。

技術の進歩も、各国が海上戦闘能力の更新を望んでいることから、新世代の艦艇の開発を後押ししています。現在、いくつかの国が旧式の艦艇を運用しているため、敵対国に対して質的な技術的優位を得るために、最新技術を搭載した艦艇の調達を重視しています。世界各国は、既存の海軍艦隊の開発、拡張、近代化、高度化に多額の投資を行っています。フリゲート艦、潜水艦などの新型艦艇の開発・調達は、より新しい戦闘艦艇の需要を生み出すと予想されます。一方、地政学的な不確実性や経済的な要因が市場の成長を妨げると予想されます。

艦艇市場の動向

潜水艦セグメントは予測期間中に大きな成長が見込まれる

- エンジンの無音運転や魚雷照準技術などの統合技術の進歩により、潜水艦は多用途かつ致命的なプラットフォームへと進化しています。潜水艦は弾道ミサイル型、誘導ミサイル型、核攻撃型、通常攻撃型に大別されます。

- 現在のシナリオでは、世界中の政府が先進的な潜水艦システムの調達に投資することを計画しており、ミサイル攻撃から水中での探知・監視まで、さまざまな活動を行うために配備されます。さらに、潜水艦市場の成長は、世界の地政学的紛争の増加、国際水域でのテロ活動の増加、戦略的安定を得るために敵地の包括的な水中調査を行う需要などの要因によって牽引されています。米国、英国、フランス、中国、ロシア、インドは、特定のシナリオのために設計された潜水艦の艦隊を持っているいくつかの国です。

- 現在、原子力潜水艦の取得計画がいくつか進行中です。例えば、米国、オーストラリア、英国は2023年3月、オーストラリアが原子力潜水艦を取得できる枠組みを発表しました。この契約に基づき、オーストラリアは2030年代初頭までに米国バージニア級原子力潜水艦3隻を調達し、必要に応じて2隻を追加購入することができます。このような開発は、今後数年間、このセグメントの成長を促進すると予想されます。

予測期間中に最も高い成長を遂げる北米

- 北米の艦艇市場を牽引しているのは主に米国です。米国海軍は490隻以上の艦艇を就役および予備役として保有しており、さらに90隻が計画・発注段階または建造中です。

- 米国海軍は戦力増強計画の実施を計画しており、耐用年数の延長と新造を組み合わせて2034年度までに355隻の目標達成を目指しています。

- 米国は、陸・空・水すべての支配権に対する軍事力を育成するために、その膨大な技術力をいくつかの兵器システムの独自開発に投資してきました。

- 2023年度予算案で米国海軍は、海軍1,805億米ドル、海兵隊503億米ドルを含む総額2,308億米ドルの予算要求を提案しました。米国海軍は、同国の海軍拡張プロジェクトの一環として、さまざまな軍艦や空母艦隊を海軍から除外したり、海軍に含めたりして、艦隊を近代化する計画を提案しました。USSニミッツは2025年度までに戦力から外され、ジェラルド・R・フォード級空母を順次受け入れ、機動力のある艦隊に容易に編入できるようにします。新型艦の最初の艦であるUSSジェラルド・R・フォード(CVN 78)は、2022年第3四半期近く、あるいはその時期に最初の作戦展開が予定されています。

- このように、海軍プログラムへの支出の増加と海軍能力の強化への関心の高まりが、この地域における市場の成長を促進しています。

海軍戦闘艦艇産業の概要

海軍戦闘艦艇の市場は半固体化しており、欧州とアジア太平洋の多くの地元企業が海軍の戦闘艦艇の要求に応えています。同市場の著名なプレーヤーには、ゼネラル・ダイナミクス・コーポレーション、ハンティントン・インガルス・インダストリーズ社、BAEシステムズPLC、ナバル・グループSA、ティッセンクルップAGなどがあります。

- 業界の競争が激化する中、プレーヤーが際立つためには技術革新が不可欠です。多くの国が、高度な能力を持つ次世代軍艦を調達しようとしています。例えば、英国海軍は2023年2月、BAEシステムズPLCと契約を結び、カンブリア州の造船所でドレッドノート級潜水艦3番艦「ウォースパイト」の建造を開始しました。この潜水艦は、先進技術と核抑止力を搭載します。

- OEM各社は、世界中の海軍による艦隊の拡大と近代化への取り組みにより、健全な収益成長を享受することが期待されます。また、新興国市場各社は、軍隊の需要に応えるため、先進的な艦艇を開発するために協力しています。このようなパートナーシップは、予測期間中にプレーヤーがビジネスを拡大するのに役立つと思われます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 艦艇タイプ別

- 駆逐艦

- フリゲート

- 潜水艦

- コルベット

- 航空母艦

- その他の船舶

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- シンガポール

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- General Dynamics Corporation

- ThyssenKrupp AG

- BAE Systems PLC

- Naval Group SA

- EDGE Group PJSC

- Damen Shipyards Group

- HD Korea Shipbuilding & Offshore Engineering Co. Ltd

- Huntington Ingalls Industries Inc.

- Lockheed Martin Corporation

- Austal Limited

- FINCANTIERI SpA

- Hanwha Ocean(Hanwha Group)

- LARSEN & TOUBRO LIMITED

- その他の企業

- PT PAL Indonesia

- Navantia SA SME

- Kalashnikov Group

- Fr. Lurssen Werft Gmbh & Co. KG

- China State Shipbuilding Corporation Limited

第7章 市場機会と今後の動向

The Naval Vessels Market size is estimated at USD 116.46 billion in 2025, and is expected to reach USD 159.26 billion by 2030, at a CAGR of 6.46% during the forecast period (2025-2030).

As geopolitical tensions and marine disputes between countries increase, they strive to enhance their naval capabilities. Several countries are upgrading their existing naval fleets or replacing their aging fleets with newer-generation vessels with advanced features. With several countries increasing their defense spending over the past decade, the industry witnessed large-scale procurement and development activities.

Technological advancements also support the development of newer-generation naval vessels, as each country wants to update its maritime combat capabilities. As several countries currently operate older naval fleets, they emphasize procuring ships with the latest technologies to gain a qualitative technological edge over their adversaries. Counties worldwide heavily invest in their existing naval fleets' development, expansion, modernization, and gradation. Developing and procuring new naval vessels, such as frigates, submarines, etc., are expected to generate demand for newer combat vessels. On the other hand, geopolitical uncertainties and economic factors are anticipated to hinder the market's growth.

Naval Vessels Market Trends

Submarines Segment is Expected to Witness Significant Growth During the Forecast Period

- Due to advancements in integrated technologies, such as silent engine operations and torpedo targeting technologies, submarines have evolved into versatile and lethal platforms. A submarine can be broadly classified as a ballistic missile, guided missile, nuclear attack, or conventional attack submarine.

- In the present scenario, governments worldwide plan to invest in procuring advanced submarine systems, which can then be deployed to carry out various activities, from missile attacks to underwater detection and surveillance. Moreover, the growth of the submarine market is driven by factors such as the increase in global geopolitical conflicts, increasing terrorism activities in international waters, and the demand to have a comprehensive underwater study of enemy territories to gain strategic stability. The United States, the United Kingdom, France, China, Russia, and India are some nations with an armada of submarines designed for specific scenarios.

- Several acquisition programs for nuclear-powered submarines are currently underway. For instance, in March 2023, the United States, Australia, and the United Kingdom announced a framework enabling Australia to acquire nuclear-powered submarines, thereby making Australia the seventh country in the world to possess this technology. Under the contract, Australia will procure three US Virginia-class nuclear-powered submarines by the early 2030s and can buy two additional vessels if required. Such developments are expected to drive the growth of the segment in the coming years.

North America to Witness Highest Growth During the Forecast Period

- The United States mainly drives the North American naval vessels market. The US Navy has over 490 ships in service and the reserve fleet, with 90 more in the planning and ordering stage or under construction.

- The US Navy plans to implement force structure expansion plans and aims to reach its 355-ship goal by FY 2034 through a mix of service life extensions and new construction.

- The United States has invested its vast technological prowess toward the indigenous development of several weapon systems to foster its military prowess over all dominion - land, air, and water.

- In the FY2023 budget proposal, the US Navy proposed a total budget request of USD 230.8 billion, including USD 180.5 billion for the US Navy and USD 50.3 billion for the US Marine Corps. As part of the country's naval expansion projects, the US Navy proposed plans to modernize its fleet by excluding and including various warships and carrier fleets in the Navy. The USS Nimitz is to be removed from the battle force by the FY2025, gradually accepting the Gerald R Ford-class carriers to be inducted readily into the fleet of agile force. The first of the new ships, USS Gerald R Ford (CVN 78), is scheduled for its first operational deployment near or in the third quarter of 2022.

- Thus, the increasing spending on naval programs and a growing focus on enhancing naval capabilities are driving the market's growth in the region.

Naval Combat Vessels Industry Overview

The market for naval vessels is semi-consolidated, with many local players in Europe and Asia-Pacific catering to the requirements of maritime vessels to the navies. Some prominent players in the market are General Dynamics Corporation, Huntington Ingalls Industries Inc., BAE Systems PLC, Naval Group SA, and ThyssenKrupp AG.

- With the industry's growing competition, innovation is critical for players to stand out. Many countries are trying to procure next-generation warships that possess advanced capabilities. For instance, in February 2023, the UK Royal Navy awarded a contract to BAE Systems PLC to initiate construction of the third Dreadnought Class submarine, Warspite, at its shipyard in Cumbria. The submarine will have advanced technology and a carrying capacity for nuclear deterrence.

- OEMs are expected to enjoy healthy revenue growth owing to fleet expansion and modernization efforts from navies worldwide. The market players also collaborate to develop advanced naval vessels to meet the armed forces' demands. Such partnerships will help the players expand their business during the forecast period.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Vessel Type

- 5.1.1 Destroyers

- 5.1.2 Frigates

- 5.1.3 Submarines

- 5.1.4 Corvettes

- 5.1.5 Aircraft Carriers

- 5.1.6 Other Vessel Types

- 5.2 By Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Russia

- 5.2.2.5 Spain

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Australia

- 5.2.3.6 Singapore

- 5.2.3.7 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Mexico

- 5.2.4.3 Rest of Latin America

- 5.2.5 Middle East and Africa

- 5.2.5.1 United Arab Emirates

- 5.2.5.2 Saudi Arabia

- 5.2.5.3 South Africa

- 5.2.5.4 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 General Dynamics Corporation

- 6.2.2 ThyssenKrupp AG

- 6.2.3 BAE Systems PLC

- 6.2.4 Naval Group SA

- 6.2.5 EDGE Group PJSC

- 6.2.6 Damen Shipyards Group

- 6.2.7 HD Korea Shipbuilding & Offshore Engineering Co. Ltd

- 6.2.8 Huntington Ingalls Industries Inc.

- 6.2.9 Lockheed Martin Corporation

- 6.2.10 Austal Limited

- 6.2.11 FINCANTIERI SpA

- 6.2.12 Hanwha Ocean (Hanwha Group)

- 6.2.13 LARSEN & TOUBRO LIMITED

- 6.3 Other Players

- 6.3.1 PT PAL Indonesia

- 6.3.2 Navantia SA SME

- 6.3.3 Kalashnikov Group

- 6.3.4 Fr. Lurssen Werft Gmbh & Co. KG

- 6.3.5 China State Shipbuilding Corporation Limited