無人水上艇(USV)・無人潜水艇(UUV)の世界市場(2025年~2035年)

Global Unmanned Surface and Underwater Vessels Market 2025-2035- 発行日

- ページ情報

- 英文 150+ Pages

- 納期

- 3営業日

- 商品コード

- 1735755

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

- 航空宇宙/防衛関連専門 航空宇宙/防衛関連専門を専門とする市場調査会社です。

概要

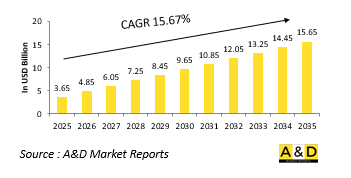

世界の無人水上艇(USV)・無人潜水艇(UUV)市場は、2025年に推定36億5,000万米ドルであり、2035年までに156億5,000万米ドルに達すると予測され、予測期間の2025年~2035年にCAGRで15.67%の成長が見込まれます。

無人水上艇(USV)・無人潜水艇(UUV)市場における技術の影響

技術革新は、防衛作戦における無人水上艇(USV)・無人潜水艇(UUV)の役割と能力を劇的に再形成しています。これらのシステムは現在、先進の航行技術、推進技術、センサー技術を活用し、高い自律性と精度で作戦を遂行しています。搭載された知能により、最適な航路図を作成し、危険を回避し、最小限の人間の入力でタスクを完了することができます。水上艇では、レーダー、光学追跡、電子戦スイートの統合により、脅威の検知と交戦が強化されます。一方、潜水艇には、ソナーイメージング、磁気異常センサー、音響通信システムが搭載され、これらが複雑な海底環境での航行や操作を可能にしています。AIは適応的行動を可能にする上で重要な役割を果たし、船舶がリアルタイムで状況を評価し、戦術を調整することを可能にします。強化されたエネルギーシステムはより長い時間の作戦をサポートし、低騒音推進は探知リスクを最小化します。安全な通信フレームワークは、紛争環境下であっても、指揮系統や他の資産との連携を確保します。これらの技術はまた、有人船、航空機、衛星ネットワークとの協調作戦における無人船の使用をサポートし、統合防衛アプローチを可能にします。ソフトウェアとハードウェアが進化を続ける中、これらのプラットフォームはよりレジリエントで効率的で多用途なものとなり、従来の海上交戦の限界を押し広げ、海上戦の有効性における新たな基準を打ち立てています。

無人水上艇(USV)・無人潜水艇(UUV)市場の主な促進要因

防衛戦略における無人水上艇(USV)・無人潜水艇(UUV)の台頭は、その戦略的価値を強く示す、相互に関連する複数の要因によって推進されています。その最たるものは、人的リスクを最小化しながら作戦範囲を拡大する必要性です。これらのプラットフォームは、脅威の高い地帯に展開され、反復的または危険なタスクを遂行し、疲労することなく長時間の作戦を遂行することができます。領海や水中資源をめぐる戦略的競争も、各国を海軍のインテリジェンスや監視能力の強化へと駆り立てています。無人船は、持続的なモニタリングに費用対効果の高いソリューションを提供し、単独でも、より広大なシステムの一部としても運用できます。また、水中機雷やステルス潜水艦の脅威が高まっていることから、有人船を危険にさらすことなく探知・掃海が可能なプラットフォームに再び注目が集まっています。自律性、耐久性、センサー統合の改良により信頼性と作戦成功率が向上したことから、技術的実現可能性がこうしたシステムをより魅力的なものにしています。海上作戦の分散化に向けた政策のシフトは、戦力を増強させるものとしての無人システムの展開をさらに後押ししています。無人システムは、抑止から迅速な危機対応まで、さまざまなシナリオへの柔軟な対応を可能にします。つまり、戦略的必要性、技術的即応性、運用効率の融合が、こうした先進の海軍資産の展開の背景にある世界的な機運を高めています。

無人水上艇(USV)・無人潜水艇(UUV)市場の地域動向

防衛向け無人水上艇(USV)・無人潜水艇(UUV)に対する地域のアプローチは、多様な安全保障上の優先事項と技術投資を反映しています。インド太平洋では、海上紛争と戦略的水路の保護が、水上・潜水無人資産の積極的な開発と展開を促進しています。沿岸監視、侵入防止作戦、海域認識は、この地域の複数の国にとっての重点部門です。北米軍は、長距離作戦と海中における優位性を維持しようと、大規模な海軍演習や艦隊近代化プログラムにこれらのシステムを組み込むことを重視しています。

当レポートでは、世界の無人水上艇(USV)・無人潜水艇(UUV)市場について調査分析し、成長促進要因、今後10年間の見通し、各地域の動向などの情報を提供しています。

目次

無人水上艇(USV)・無人潜水艇(UUV)市場レポートの定義

無人水上艇(USV)・無人潜水艇(UUV)市場のセグメンテーション

地域別

用途別

動作方式別

今後10年間の無人水上艇(USV)・無人潜水艇(UUV)市場の分析

無人水上艇(USV)・無人潜水艇(UUV)市場の技術

世界の無人水上艇(USV)・無人潜水艇(UUV)市場の予測

地域の無人水上艇(USV)・無人潜水艇(UUV)市場の動向と予測

北米

促進要因、抑制要因、課題

PEST

市場予測とシナリオ分析

主要企業

サプライヤーのTierの情勢

企業ベンチマーク

欧州

中東

アジア太平洋

南米

無人水上艇(USV)・無人潜水艇(UUV)市場の分析:国別

米国

最新ニュース

特許

この市場における現在の技術成熟度

市場予測とシナリオ分析

カナダ

イタリア

フランス

ドイツ

オランダ

ベルギー

スペイン

スウェーデン

ギリシャ

オーストラリア

南アフリカ

インド

中国

ロシア

韓国

日本

マレーシア

シンガポール

ブラジル

無人水上艇(USV)・無人潜水艇(UUV)市場の機会マトリクス

無人水上艇(USV)・無人潜水艇(UUV)市場レポートに関する専門家の意見

結論

Aviation and Defense Market Reportsについて

図表

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Control, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Application, 2025-2035

- Table 20: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Control, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Application, 2025-2035

List of Figures

- Figure 1: Global Unmanned Surface and Underwater Vessels Market Forecast, 2025-2035

- Figure 2: Global Unmanned Surface and Underwater Vessels Market Forecast, By Region, 2025-2035

- Figure 3: Global Unmanned Surface and Underwater Vessels Market Forecast, By Control, 2025-2035

- Figure 4: Global Unmanned Surface and Underwater Vessels Market Forecast, By Application, 2025-2035

- Figure 5: North America, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 6: Europe, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 7: Middle East, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 8: APAC, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 9: South America, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 10: United States, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 11: United States, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 12: Canada, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 13: Canada, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 14: Italy, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 15: Italy, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 16: France, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 17: France, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 18: Germany, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 19: Germany, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 20: Netherlands, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 21: Netherlands, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 22: Belgium, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 23: Belgium, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 24: Spain, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 25: Spain, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 26: Sweden, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 27: Sweden, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 28: Brazil, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 29: Brazil, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 30: Australia, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 31: Australia, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 32: India, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 33: India, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 34: China, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 35: China, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 36: Saudi Arabia, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 37: Saudi Arabia, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 38: South Korea, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 39: South Korea, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 40: Japan, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 41: Japan, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 42: Malaysia, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 43: Malaysia, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 44: Singapore, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 45: Singapore, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 46: United Kingdom, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 47: United Kingdom, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 48: Opportunity Analysis, Unmanned Surface and Underwater Vessels Market, By Region (Cumulative Market), 2025-2035

- Figure 49: Opportunity Analysis, Unmanned Surface and Underwater Vessels Market, By Region (CAGR), 2025-2035

- Figure 50: Opportunity Analysis, Unmanned Surface and Underwater Vessels Market, By Control (Cumulative Market), 2025-2035

- Figure 51: Opportunity Analysis, Unmanned Surface and Underwater Vessels Market, By Control (CAGR), 2025-2035

- Figure 52: Opportunity Analysis, Unmanned Surface and Underwater Vessels Market, By Application (Cumulative Market), 2025-2035

- Figure 53: Opportunity Analysis, Unmanned Surface and Underwater Vessels Market, By Application (CAGR), 2025-2035

- Figure 54: Scenario Analysis, Unmanned Surface and Underwater Vessels Market, Cumulative Market, 2025-2035

- Figure 55: Scenario Analysis, Unmanned Surface and Underwater Vessels Market, Global Market, 2025-2035

- Figure 56: Scenario 1, Unmanned Surface and Underwater Vessels Market, Total Market, 2025-2035

- Figure 57: Scenario 1, Unmanned Surface and Underwater Vessels Market, By Region, 2025-2035

- Figure 58: Scenario 1, Unmanned Surface and Underwater Vessels Market, By Control, 2025-2035

- Figure 59: Scenario 1, Unmanned Surface and Underwater Vessels Market, By Application, 2025-2035

- Figure 60: Scenario 2, Unmanned Surface and Underwater Vessels Market, Total Market, 2025-2035

- Figure 61: Scenario 2, Unmanned Surface and Underwater Vessels Market, By Region, 2025-2035

- Figure 62: Scenario 2, Unmanned Surface and Underwater Vessels Market, By Control, 2025-2035

- Figure 63: Scenario 2, Unmanned Surface and Underwater Vessels Market, By Application, 2025-2035

- Figure 64: Company Benchmark, Unmanned Surface and Underwater Vessels Market, 2025-2035

目次

The Global Unmanned Surface and Underwater Vessels market is estimated at USD 3.65 billion in 2025, projected to grow to USD 15.65 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 15.67% over the forecast period 2025-2035.

Introduction to Unmanned Surface and Underwater Vessels Market:

Defense unmanned surface and underwater vessels have become central to the modernization of naval forces worldwide. These platforms offer strategic capabilities that enhance situational awareness, extend operational reach, and reduce the exposure of personnel in dangerous maritime environments. By operating autonomously or under remote control, these vessels support a wide range of missions such as anti-submarine warfare, mine countermeasures, intelligence collection, and maritime patrols. Surface units navigate above water to perform visible deterrence and surveillance, while underwater systems execute stealth missions that involve detection, reconnaissance, or precision strikes. The demand for these technologies is accelerating as maritime challenges evolve, requiring persistent presence and rapid adaptability. With increased activity in littoral zones, contested waterways, and strategic choke points, navies are seeking reliable solutions that can perform effectively across various ocean conditions. The modular nature of these systems allows for mission-specific configurations, making them suitable for both routine security and high-threat operations. Defense organizations are integrating unmanned maritime vessels into their existing fleets to complement traditional assets and support distributed operational models. As maritime threats become more unpredictable and technologically sophisticated, unmanned surface and underwater systems are proving indispensable in maintaining maritime dominance and executing complex naval strategies with greater precision and flexibility.

Technology Impact in Unmanned Surface and Underwater Vessels Market:

Technological innovation is dramatically reshaping the roles and capabilities of unmanned surface and underwater vessels in defense operations. These systems now leverage advanced navigation, propulsion, and sensor technologies to execute missions with high levels of autonomy and accuracy. Onboard intelligence enables them to chart optimal routes, avoid hazards, and complete tasks with minimal human input. In surface vessels, integration of radar, optical tracking, and electronic warfare suites enhances threat detection and engagement. Meanwhile, underwater vehicles benefit from sonar imaging, magnetic anomaly sensors, and acoustic communication systems that allow them to navigate and operate in complex sub-sea environments. Artificial intelligence plays a crucial role in enabling adaptive behavior, allowing vessels to assess conditions and adjust tactics in real time. Enhanced energy systems support longer missions, while low-noise propulsion minimizes detection risk. Secure communication frameworks ensure coordination with command structures and other assets, even in contested environments. These technologies also support the use of unmanned vessels in coordinated operations with manned ships, aircraft, and satellite networks, enabling a unified defense approach. As software and hardware continue to evolve, these platforms are becoming more resilient, efficient, and versatile, pushing the boundaries of traditional naval engagement and setting new standards in maritime warfare effectiveness.

Key Drivers in Unmanned Surface and Underwater Vessels market:

The rise of unmanned surface and underwater vessels in defense strategy is propelled by multiple interrelated factors that underscore their strategic value. Foremost is the need to extend operational reach while minimizing the risk to personnel. These platforms can be deployed in high-threat zones, perform repetitive or hazardous tasks, and conduct long-endurance missions without fatigue. Strategic competition over maritime territories and underwater resources is also prompting nations to enhance their naval intelligence and surveillance capabilities. Unmanned vessels offer cost-effective solutions for persistent monitoring and can operate independently or as part of a broader system. The increasing threat of underwater mines and stealthy submarines has also led to a renewed focus on platforms capable of conducting detection and clearance without endangering manned vessels. Technological feasibility has made these systems more attractive, as improvements in autonomy, durability, and sensor integration have increased their reliability and mission success rates. Policy shifts toward distributed maritime operations further support the deployment of unmanned systems as force multipliers. They enable flexible response to a variety of scenarios, from deterrence to rapid crisis response. Ultimately, the convergence of strategic necessity, technological readiness, and operational efficiency is driving the global momentum behind the deployment of these advanced naval assets.

Regional Trends in Unmanned Surface and Underwater Vessels Market:

Regional approaches to defense unmanned surface and underwater vessels reflect diverse security priorities and technological investments. In the Indo-Pacific, maritime disputes and the protection of strategic waterways have driven aggressive development and deployment of both surface and sub-sea unmanned assets. Coastal surveillance, anti-intrusion missions, and maritime domain awareness are key focus areas for several nations in this region. North American forces are emphasizing the integration of these systems into large-scale naval exercises and fleet modernization programs, seeking to maintain an edge in long-range operations and undersea dominance. European nations are balancing innovation with collaborative frameworks, often pooling resources to develop interoperable platforms suitable for both national and allied missions. This cooperative model enables broader surveillance coverage and cost efficiency. Middle Eastern countries are increasingly turning to unmanned surface vehicles to monitor critical maritime infrastructure and shipping lanes, especially in areas with a history of sabotage and asymmetric threats. African and Latin American defense entities, while at earlier stages of adoption, are beginning to invest in these technologies for coastal security, anti-smuggling efforts, and environmental monitoring. Across all regions, the trend is clear: unmanned surface and underwater vessels are transitioning from experimental tools to vital components of modern naval defense, driven by specific regional imperatives and evolving maritime threats.

Key Defense Unmanned Surface and Underwater Vessels Program:

HII announced that its Mission Technologies division has been awarded a contract to produce nine small unmanned undersea vehicles (SUUVs) for the U.S. Navy's Lionfish System program. The agreement includes the potential for expansion to up to 200 vehicles over the next five years, with a total contract value exceeding $347 million. The Lionfish System is derived from HII's REMUS 300-a compact, two-person-deployable SUUV featuring an open architecture and flexible payload configurations. In early 2022, the REMUS 300 was designated as the Navy's official program of record for its next-generation SUUV platform. Managed by Naval Sea Systems Command, the contract covers the production and support of these advanced SUUVs, along with associated afloat and auxiliary support equipment and engineering services. The vehicles, equipped with cutting-edge autonomous and unmanned technologies, are intended to perform vital undersea missions for the Navy.

Table of Contents

Unmanned Surface and Underwater Vessels Market Report Definition

Unmanned Surface and Underwater Vessels Market Segmentation

By Region

By Application

By Mode of Operation

Unmanned Surface and Underwater Vessels Market Analysis for next 10 Years

The 10-year unmanned surface and underwater vessels market analysis would give a detailed overview of unmanned surface and underwater vessels market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Unmanned Surface and Underwater Vessels Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Unmanned Surface and Underwater Vessels Market Forecast

The 10-year unmanned surface and underwater vessels market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Unmanned Surface and Underwater Vessels Market Trends & Forecast

The regional unmanned surface and underwater vessels market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Unmanned Surface and Underwater Vessels Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Unmanned Surface and Underwater Vessels Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Unmanned Surface and Underwater Vessels Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

- 発行日

- 発行

- Aviation & Defense Market Reports (A&D)

- ページ情報

- 英文 150+ Pages

- 納期

- 3営業日