|

市場調査レポート

商品コード

1684522

海軍艦艇市場の機会、成長促進要因、産業動向分析、2025年~2034年予測Naval Vessels Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 海軍艦艇市場の機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年01月02日

発行: Global Market Insights Inc.

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

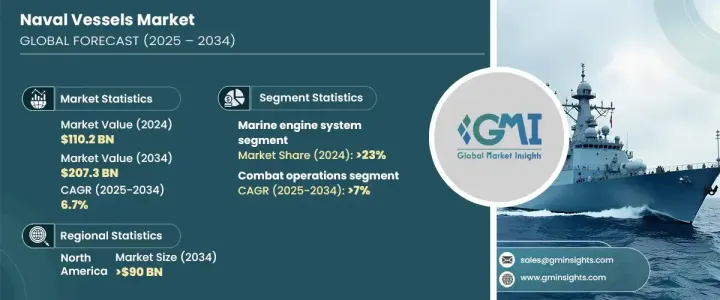

世界の海軍艦艇市場は2024年に1,102億米ドルに達し、2025年から2034年にかけてCAGR 6.7%で成長する見通しです。

この成長軌道は、世界中で安全保障上の脅威が増大していることを反映しており、高度な攻撃・防御兵器システムに対する需要がかつてないほど急増しています。世界中の政府と防衛機関は、海上安全保障を強化し、進化する脅威に対処するため、最先端の海軍技術に多額の投資を行っています。海軍艦隊の近代化は、人工知能(AI)、自律システム、先進推進技術の統合と相まって、市場の展望を再構築しています。地政学的緊張の高まりと海洋領土をめぐる紛争は、国家安全保障戦略における海軍艦艇の重要な役割をさらに強調しています。さらに、環境に優しい推進システムへの移行は、運航効率とともに持続可能性を重視し、厳しい環境規制への対応を示しています。

市場はシステム別に、舶用エンジンシステム、武器発射システム、制御システム、電気システム、通信システム、その他に区分されます。このうち、舶用エンジンシステム分野は2024年に市場シェアの23%を占め、今後数年で大きく拡大すると予測されています。海軍艦艇の推進技術は急速に進歩しており、ハイブリッドシステムやバイオ燃料駆動システムへのシフトが顕著です。これらの技術は、従来の燃料エンジンに電気モーターを統合するもので、最新の駆逐艦や潜水艦の戦術的・運用的ニーズに対応すると同時に、環境上の義務にも合致しています。エネルギー効率の高いシステムの推進は、性能を損なうことなく軍事作戦の二酸化炭素排出量を削減することに重点が置かれていることを反映しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1,102億米ドル |

| 予測金額 | 2,073億米ドル |

| CAGR | 6.7% |

用途別では、沿岸作戦、捜索救助任務、戦闘作戦、地雷対策(MCM)作戦、その他に分類されます。戦闘作戦分野は、2034年までCAGR7%を記録し、力強い成長が見込まれます。極超音速ミサイル技術、指向性エネルギー・システム、精密魚雷などの革命的進歩は、海軍戦闘部隊の能力を変革しています。これらの技術は、武器の射程距離、精度、全体的な有効性を高め、沿岸地域やそれ以外の地域に優れた防衛能力を提供します。さらに、AIと自律技術の統合は、海軍作戦を根本的に変え、迅速な脅威検知、合理化された任務遂行、複数の領域にわたる状況認識の強化を可能にしています。

北米は、特に駆逐艦と潜水艦の分野で、海軍艦艇市場の主要プレーヤーであり続けています。同地域は、米国が海軍能力の強化に注力していることから、2034年までに900億米ドルの市場規模になると予測されています。米国は、極超音速兵器と自律システムに対する多額の投資で市場をリードし続け、戦略的優位性と比類のない運用効率を確保しています。海軍艦艇市場の成長は、防衛投資の増加、推進技術の進歩、AIと自律型ソリューションの採用拡大によって促進され、世界の海上安全保障における重要な役割を確固たるものにしています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 2次データ

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 破壊

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 促進要因

- 地政学的緊張の高まりと軍事近代化

- 防衛予算の増加

- 潜水艦をベースとした戦略防衛への需要の高まり

- 海洋安全保障への注目の高まり

- 海軍艦隊の多様化への注目の高まり

- 業界の潜在的リスク&課題

- 高い開発コストとメンテナンスコスト

- 地政学的不安定性と規制上の制約

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:船舶タイプ別、2021年~2034年

- 主要動向

- 駆逐艦

- フリゲート

- 潜水艦

- コルベット

- 航空母艦

- その他

第6章 市場推計・予測:システム別、2021年~2034年

- 主要動向

- 舶用エンジンシステム

- 兵器発射システム

- 制御システム

- 電気システム

- 通信システム

- その他

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 捜索救助

- 戦闘作戦

- 地雷対策(MCM)活動

- 沿岸作業

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Austal

- BAE Systems

- Damen Shipyards

- Fincantieri

- General Dynamics

- Hanwha Ocean

- HD Korea Shipbuilding

- Huntington Ingalls

- Larsen &Toubro

- Lockheed Martin

- Naval Group

- ThyssenKrupp

The Global Naval Vessels Market reached USD 110.2 billion in 2024 and is poised to grow at a CAGR of 6.7% between 2025 and 2034. This growth trajectory reflects the rising prevalence of security threats across the globe, which has led to an unprecedented surge in demand for advanced offensive and defensive weapon systems. Governments and defense organizations worldwide are investing heavily in cutting-edge naval technologies to strengthen their maritime security and address evolving threats. The modernization of naval fleets, combined with the integration of artificial intelligence (AI), autonomous systems, and advanced propulsion technologies, is reshaping the market landscape. Increasing geopolitical tensions and disputes over maritime territories further underscore the critical role of naval vessels in national security strategies. Additionally, the transition toward eco-friendly propulsion systems demonstrates the sector's response to stringent environmental regulations, emphasizing sustainability alongside operational efficiency.

The market is segmented by system into marine engine systems, weapon launch systems, control systems, electrical systems, communication systems, and others. Among these, the marine engine systems segment accounted for 23% of the market share in 2024 and is anticipated to expand significantly in the coming years. Propulsion technologies for naval vessels are advancing rapidly, with a notable shift toward hybrid and biofuel-driven systems. These technologies integrate electric motors with conventional fuel engines, aligning with environmental mandates while addressing the tactical and operational needs of modern destroyers and submarines. The push for energy-efficient systems reflects a growing emphasis on reducing the carbon footprint of military operations without compromising performance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $110.2 billion |

| Forecast Value | $207.3 billion |

| CAGR | 6.7% |

By application, the market is categorized into coastal operations, search and rescue missions, combat operations, Mine Countermeasures (MCM) operations, and others. The combat operations segment is expected to witness robust growth, registering a CAGR of 7% through 2034. Revolutionary advancements such as hypersonic missile technology, directed energy systems, and precision torpedoes are transforming the capabilities of naval combat forces. These technologies enhance weapon range, accuracy, and overall effectiveness, providing superior defense capabilities for coastal regions and beyond. Furthermore, the integration of AI and autonomous technologies has fundamentally changed naval operations, enabling rapid threat detection, streamlined mission execution, and enhanced situational awareness across multiple domains.

North America remains a key player in the naval vessels market, particularly in the destroyers and submarines segments. The region is projected to generate USD 90 billion in value by 2034, driven by the United States' focus on advancing naval capabilities. The U.S. continues to lead the market with substantial investments in hypersonic weapons and autonomous systems, ensuring strategic dominance and unmatched operational efficiency. The naval vessels market growth is fueled by rising defense investments, advancements in propulsion technologies, and the growing incorporation of AI and autonomous solutions, solidifying its critical role in global maritime security.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Growing geopolitical tensions and military modernization

- 3.6.1.2 Increasing defense budgets

- 3.6.1.3 Growing demand for submarine-based strategic defense

- 3.6.1.4 Rising focus on maritime security

- 3.6.1.5 Increased focus on naval fleet diversification

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High development and maintenance costs

- 3.6.2.2 Geopolitical instability and regulatory constraints

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vessel Type, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Destroyers

- 5.3 Frigates

- 5.4 Submarines

- 5.5 Corvettes

- 5.6 Aircraft carriers

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By System, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Marine engine system

- 6.3 Weapon launch system

- 6.4 Control system

- 6.5 Electrical system

- 6.6 Communication system

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Search and rescue

- 7.3 Combat operations

- 7.4 Mine countermeasures (MCM) operations

- 7.5 Coastal Operations

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Austal

- 9.2 BAE Systems

- 9.3 Damen Shipyards

- 9.4 Fincantieri

- 9.5 General Dynamics

- 9.6 Hanwha Ocean

- 9.7 HD Korea Shipbuilding

- 9.8 Huntington Ingalls

- 9.9 Larsen & Toubro

- 9.10 Lockheed Martin

- 9.11 Naval Group

- 9.12 ThyssenKrupp