|

|

市場調査レポート

商品コード

1437608

日本の航空宇宙・防衛市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Japan Aerospace And Defense - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 日本の航空宇宙・防衛市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

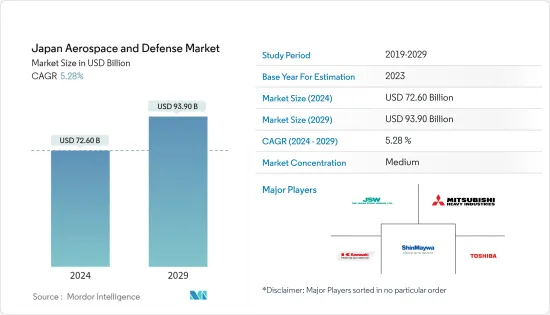

日本の航空宇宙・防衛の市場規模は、2024年に726億米ドルと推定され、2029年には939億米ドルに達し、予測期間中(2024年~2029年)にCAGR5.28%で成長すると予測されています。

日本の航空宇宙分野は世界最大規模の一つであり、特に研究開発(R&D)の分野で国際的に高い評価を得ています。日本企業は、ヘリコプターや軽攻撃機などの軍民両用航空宇宙防衛技術の研究開発において大きな可能性を秘めています。 2022年には、日本の航空会社による国際線の乗客数は約680万人となり、前年の140万人から増加しました。

防衛費の増加、次世代兵器の調達の増加、軍事通信における先進技術の導入が日本全体の市場の成長を推進しています。ストックホルム国際平和調査(SIPRI)が2022年に発表した報告書によると、日本の防衛費は460億米ドルで、世界で10番目に大きい国防支出国となりました。同国は2023会計年度に514億米ドルの国防支出を承認しました。

いくつかの国際的な課題や不安定要因が深刻化しており、日本の安全保障環境はますますストレスが高まっています。このため、安全保障環境の変化の増大に適応するため、日本は防衛力の強化を急ピッチで進めています。防衛予算案は9年連続で日本の国防予算の新記録を樹立しました。 2023年度について、日本政府は前年度比26.3%増の6兆8,200億円(514億米ドル)を承認しました。国防予算の増加と進行中の軍事近代化が市場成長の主な促進要因となると予想されます。

日本の航空宇宙・防衛市場動向

2023年には製造セグメントが大きなシェアを占める

製造サービス型セグメントが突出しており、最大のシェアを占めています。三菱重工業株式会社や川崎重工業株式会社などの有名企業が、この分野の形成において重要な役割を果たしています。これらの業界大手は、精密工学と最先端技術の専門知識を活用して、戦闘機やヘリコプターから高度なミサイルシステムに至るまで、幅広い航空宇宙製品や防衛製品を製造しています。製造サービス型の重要性は、これらの企業と日本政府との複雑な連携によって強調され、国家安全保障のための戦略的パートナーシップを促進します。さらに、スバル株式会社のような新興企業は、航空宇宙部品を含めてポートフォリオを多様化することで、この分野の成長に貢献しています。イノベーション、品質、信頼性を重視することで、日本の製造サービス部門は、技術力と戦略的先見性の相乗効果を反映して、日本の航空宇宙・防衛能力の要として位置づけられています。さらに、日本政府からの国産製品の受注増加も製造業の成長に貢献しています。たとえば、三菱重工業は2023年11月、防衛関連の売上高が2026年までに倍増して1兆円(67億米ドル)に達し、地政学的な緊張が三菱重工の事業を押し上げる中、引き続き堅調に推移すると予測しました。日本政府の最新の5か年戦略は、日本の防衛力の強化に向けて、2027年までに防衛費を前期比56%増額することを示唆しています。三菱重工の主な焦点は、1,000キロメートル以上の距離を達成できる長距離ミサイルを国内で生産する能力を開発することです。政府はまた、現地の技術革新と製造を奨励するために製造業者に最大10%の利益率を提供しており、高いインフレ率を支援するために最大5%のコスト増加を相殺する用意があります。このような分野での発展は、日本の新たな多次元統合防衛力の一部となることが期待されています。したがって、このような進行中の開発は、予測期間中に日本の防衛市場を牽引すると予想されます。

航空宇宙産業は予測期間中に大幅な成長を遂げる

航空宇宙分野は、予測期間中に目覚ましい成長を示す準備ができています。日本は輸入航空機、航空機部品、エンジンにとって有利な市場を提供し続けています。現在、日本は、B777、B777X、B787を含むいくつかの航空機ファミリーの開発において中心的な役割を果たしています。 2023年3月、日本のナショナルフラッグキャリアである日本航空(JAL)は、ボーイングB737 MAX型機21機の発注を発表しました。同社は、2026年から先進的で燃料効率の高い航空機を自社機材に導入することを目指しています。契約額は約25億米ドルでした。羽田国際空港(HND)、成田国際空港(NRT)、関西国際空港(KIX)、福岡国際空港(FUK)は日本の4つの主要空港であり、合わせて年間2億人以上の乗客が利用しています。

さらに、日本企業は、V2500、Trent1000、GEnx、GE9X、PW1100G-JMなどの航空機エンジンの開発やMROに向けたエンジニアリングサービスの提供にも積極的に取り組んでいます。同様に、2022年1月には米国国防総省(国防省)は、航空自衛隊(JASDF)のF-15イーグルスーパーインターセプター部隊向けの新しいシステムの開発に関して、ボーイング社と4億7,100万米ドル相当の契約を締結したと発表しました。日本企業はまた、ひまわり8号、9号などの気象衛星をはじめ、各種工学試験衛星、海洋・地上観測衛星、通信、放送、全地球測位衛星などの開発にも貢献してきました。2021年、日本政府は宇宙活動に41億4,000万米ドルを支出しました。日本の宇宙企業は、MV、H-IIA/B、イプシロンロケットなどの打ち上げロケットを開発しました。日本の衛星メーカーも高い技術力、高品質、競争力のあるコストを武器に海外市場の開拓に取り組んでいます。したがって、研究開発への支出の増加と航空インフラの強化への支出の増加が、国全体の市場の成長を推進しています。

日本の航空宇宙・防衛産業の概要

日本の航空宇宙・防衛市場は半統合されており、三菱重工業株式会社、株式会社東芝、川崎重工業株式会社、新明和工業株式会社、日本製鋼所株式会社などのいくつかの主要企業がより高い市場シェアを獲得するための製品・サービスレベルで競合しています。日本は武器輸出に関する新たな原則とガイドラインを採用しており、国際協力と安全保障上の利益に貢献する目的にかなう場合に限り、ある国への武器輸出を許可しています。 2022年の国防白書によると、戦闘機の製造には約1,100社、駆逐艦の建造には約8,300社、戦車の製造には約1,300社が携わっています。したがって、地元の航空宇宙・防衛メーカーへの支持の拡大と研究開発への投資の増加により、予測期間中の市場の成長が促進されます。例えば、日本の防衛省(MoD)は、弾薬関連支出として2022年比330%増の62億3,000万米ドルを確保しました。この中には、米国製長距離巡航ミサイル「トマホーク」500発の調達に15億9,000万米ドルが含まれています。日本の防衛省は反撃能力の開発を目指し、2026~27年度にトマホークを配備する予定です。東京都は、海上自衛隊のイージス艦に搭載するための先進型トマホークブロックVを取得します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 分野

- 航空宇宙

- 防衛

- サービスタイプ

- 製造

- MRO

- プラットフォーム

- 陸上

- 航空

- 海上

第6章 競合情勢

- 企業プロファイル

- BAE Systems plc

- Kawasaki Heavy Industries, Ltd.

- Komatsu Ltd.

- Lockheed Martin Corporation

- Mitsubishi Heavy Industries, Ltd.

- Northrop Grumman Corporation

- RTX Corporation

- ShinMaywa Industries Ltd.

- THALES

- The Boeing Company

- Japan Steel Works, Ltd.

- Toshiba Corporation

- Toray Industries, Inc.

第7章 市場機会と将来の動向

The Japan Aerospace And Defense Market size is estimated at USD 72.60 billion in 2024, and is expected to reach USD 93.90 billion by 2029, growing at a CAGR of 5.28% during the forecast period (2024-2029).

The Japanese aerospace sector is one of the largest in the world, with a strong international reputation, particularly in the field of research and development (R&D). Japanese companies have great potential in the research and development of dual-use aerospace defense technology, such as helicopters and light attack aircraft. In 2022, around 6.8 million passengers were carried on international flights via Japanese airlines, up from 1.4 million passengers in the previous year.

An increase in defense expenditure, rising procurement of next-generation weapons, and adoption of advanced technologies in military communication drive the growth of the market across Japan. According to the report published by Stockholm International Peace Research Institute (SIPRI) in 2022, Japan was the tenth largest defense spender in the world, with a defense budget of USD 46 billion. The country approved USD 51.4 billion in defense spending in FY2023.

The security environment in Japan has become increasingly stressed, with several international challenges and destabilizing factors becoming more acute. Hence, to adapt to the growing changes in the security environment, Japan has been strengthening its defense capabilities at a rapid pace. For the ninth consecutive year, the defense budget draft set a new record for Japan's national defense budget. For FY2023, the Japanese government approved 6.82 trillion yen (USD 51.4 billion), which showed an increase of 26.3% from the previous year. The growth in the defense budget and the ongoing military modernization are expected to be the major drivers for the growth of the market.

Japan Aerospace And Defense Market Trends

The Manufacturing Segment Accounted for a Major Share in 2023

The manufacturing service type segment stands out as the dominant force, holding the largest market share. Renowned companies such as Mitsubishi Heavy Industries, Ltd. and Kawasaki Heavy Industries, Ltd. play pivotal roles in shaping this sector. These industry giants leverage their expertise in precision engineering and cutting-edge technology to manufacture a wide array of aerospace and defense products, ranging from fighter jets and helicopters to sophisticated missile systems. The significance of the manufacturing service type is underscored by the intricate collaboration between these companies and the Japanese government, fostering a strategic partnership for national security. Additionally, emerging players like Subaru Corporation contribute to the sector's growth by diversifying their portfolios to include aerospace components. The emphasis on innovation, quality, and reliability positions Japan's manufacturing service type segment as a linchpin in the nation's aerospace and defense capabilities, reflecting a synergy between technological prowess and strategic foresight. Moreover, increasing orders from Japan government for indigenous manufactured products is also contributing to the growth of manufacturing sector. For instance, in November 2023, Mitsubishi Heavy Industries forecast its defense sales to double to 1 trillion yen (USD 6.7 billion) by 2026 and stay strong as geopolitical tensions boost business for MHI. The Japanese government's latest five-year strategy suggests a 56% increase in defense spending, through 2027, from the previous term as it strives to build up the Japan's defense capabilities. Major key focus of MHI is to develop a domestic capability to produce long-range missiles that can achieve distances of over 1,000 kilometers. The government is also offering manufacturers profit margins of up to 10% to encourage indigenous innovation and manufacturing and is prepared to offset up to 5% in cost increases to help with high inflation rates. Developments in such domains are expected to be a part of Japan's new multidimensional integrated defense force. Thus, such ongoing developments are expected to drive the Japanese defense market during the forecast period.

Aerospace Sector to Witness Significant Growth During the Forecast Period

The aerospace sector is poised to showcase remarkable growth during the forecast period. Japan continues to offer a lucrative market for imported aircraft, aircraft parts, and engines. Currently, Japan is playing a pivotal role in the development of several aircraft families, including the B777, B777X, and B787. In March 2023, Japan Airlines (JAL), Japan's national flag carrier, announced an order of 21 Boeing B737 MAX aircraft. The airline aims to bring advanced and fuel-efficient aircraft into its fleet starting in 2026. The value of the contract was approximately USD 2.5 billion. Haneda International Airport (HND), Narita International Airport (NRT), Kansai International Airport (KIX), and Fukoma International Airport (FUK) are the four major airports in Japan that together handle over 200 million passengers annually.

Furthermore, Japanese companies are also actively engaged in providing engineering services towards the development and MRO of aircraft engines, such as the V2500, Trent1000, GEnx, GE9X, PW1100G-JM, etc. Similarly, in January 2022, the US Department of Defense (DoD) announced a contract worth USD 471 million to the Boeing Company for the development of new systems for Japan Air Self-Defense Force's (JASDF) F-15 Eagle Super Interceptors fleet. The Japanese firms have also contributed to the development of various engineering test satellites, marine and terrestrial observation satellites, communications, broadcasting, global navigation satellites, etc., including weather satellites such as the HIMAWARI 8 and 9. In 2021, the Japanese government spent USD 4.14 billion on space activities. The Japanese space firms developed Launch vehicles such as the M-V, H-IIA/B, and Epsilon rockets. The Japanese satellite manufacturers are also using their advanced technical capabilities, high quality, and competitive costs to open the overseas market. Thus, growing expenditure on research and development and rising spending on enhancing aviation infrastructure drive market growth across the country.

Japan Aerospace And Defense Industry Overview

The Japan aerospace and defense market is semi-consolidated and several key players such as Mitsubishi Heavy Industries, Ltd., Toshiba Corporation, Kawasaki Heavy Industries, Ltd., ShinMaywa Industries, Ltd., and Japan Steel Works, Ltd. compete on product and services level to gain higher market share. Japan has adopted new principles and guidelines on arms exports and would permit arms exports to a country only if they serve the purpose of contributing to international cooperation and its security interests. According to the 2022 defense white paper, nearly 1,100 companies are involved in the manufacture of fighter aircraft, about 8,300 in building destroyers, and around 1,300 in the production of tanks. Thus, growing support for local aerospace and defense manufacturers and rising investment in research and development boost the market growth during the forecast period. For instance, The Japanese Ministry of Defense (MoD) secured USD 6.23 billion for ammunition-related spending, which is 330% higher than in 2022. It included USD 1.59 billion for the procurement of 500 US-made long-range Tomahawk cruise missiles. The Japanese MoD will deploy the Tomahawks in fiscal year 2026-27 as it aims to develop counterstrike capabilities. Tokyo will acquire the advanced model Tomahawk Block V to be equipped with Japan Maritime Self-Defense Force (JMSDF) Aegis-equipped destroyers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Sector

- 5.1.1 Aerospace

- 5.1.2 Defense

- 5.2 Service Type

- 5.2.1 Manufacturing

- 5.2.2 MRO

- 5.3 Platform

- 5.3.1 Terrestrial

- 5.3.2 Aerial

- 5.3.3 Naval

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 BAE Systems plc

- 6.1.2 Kawasaki Heavy Industries, Ltd.

- 6.1.3 Komatsu Ltd.

- 6.1.4 Lockheed Martin Corporation

- 6.1.5 Mitsubishi Heavy Industries, Ltd.

- 6.1.6 Northrop Grumman Corporation

- 6.1.7 RTX Corporation

- 6.1.8 ShinMaywa Industries Ltd.

- 6.1.9 THALES

- 6.1.10 The Boeing Company

- 6.1.11 Japan Steel Works, Ltd.

- 6.1.12 Toshiba Corporation

- 6.1.13 Toray Industries, Inc.