米国の航空宇宙・防衛:市場シェア分析、産業動向、成長予測(2025~2030年)

United States Aerospace And Defense - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 116 Pages

- 納期

- 2~3営業日

- 商品コード

- 1689734

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

米国の航空宇宙・防衛市場規模は2025年に5,251億6,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは5.76%で、2030年には6,948億6,000万米ドルに達すると予測されます。

米国の航空宇宙・防衛部門は、インフラと製造活動の面で最大級の規模を誇る。同市場は主に、新たな脅威に対抗するための軍の調達とアップグレード活動によって成長すると予想されます。現在、軍、空軍、海軍からいくつかの契約が進行中であり、予測期間中にも多くの新規契約が分散されると予想され、防衛機器に対する並行需要が生まれます。

米国軍は空軍や海軍の航空機を複数使用しています。南シナ海での侵略をめぐる中国との国際的な対立が激化しているため、米国は、中国が台湾や日本など米国と密接な関係にある国々に引き起こす可能性のある問題に取り組む準備を整えています。その結果、既存の艦隊をアップグレードし、効率的な技術を搭載した新しい艦隊を購入するための大規模な投資が、過去1年間に確認されています。

航空・防衛装備品の開発において、3Dプリンティング、人工知能、ビッグデータ分析などの先端技術の採用が進むことで、今後数年間はより良い機会が生まれると考えられます。しかし、サプライチェーンや進化するサイバーセキュリティリスクに関する問題は、市場の成長を妨げる可能性があります。

米国の航空宇宙・防衛市場の動向

宇宙セグメントが予測期間中に最も高い成長を遂げる見込み

宇宙機能は、米国とその同盟国に、国家意思決定、軍事作戦、国土安全保障においてかつてない優位性を与えています。最近の宇宙探査は一握りの非公開会社が主導しているが、米国では第6の軍事部門として宇宙軍を設立する議論が進行中です。

米国の衛星製造・打上げ産業は、急速に発展している産業であり、米国の宇宙開発と国家安全保障の取り組みにおいて重要な役割を果たしています。近年、この産業は、技術の進歩、衛星サービスに対する需要の増加、様々な有力参入企業の存在により、大きな変化を遂げています。新たな衛星打ち上げの需要は、宇宙からの低遅延インターネットアクセスの提供など、様々な衛星サービスの必要性によってもたらされています。2022年4月、Amazonの子会社であるKuiper Systems LLCは、2026年までに1,500基の衛星を打ち上げる承認を連邦通信委員会から得たと発表しました。同社は2029年までに3,236基の衛星を打ち上げ、世界中でブロードバンドインターネットサービスを提供する計画です。同社はこれらの衛星を打ち上げるために、Blue Origin、Arianespace、United Launch Alliance(ULA)から約83の打ち上げサービスを確保しました。

米国宇宙司令部は、おそらく米国国防総省(DoD)と米国の航空宇宙・防衛産業に利益をもたらすと考えられます。宇宙軍によって管理される人員と資産を使用して宇宙業務を監督する米国宇宙司令部は、革新的な技術と能力への投資を加速させるA& D企業を支援する可能性が高いです。このように、宇宙研究開発への支出の増大と衛星打ち上げの増加は、国全体の市場成長を促進します。

空軍は予測期間中に目覚ましい成長を見せる見込み

米国空軍は、陸海軍に航空支援を提供し、戦場とその周辺にいる部隊を支援する最新技術を備えています。空軍は、ロシアや中国との大きな勢力争いの要求に応えるため、次世代航空機の開発と調達を続けています。米国空軍は、1万3,247機の運用機、予備機、運用終了機で構成されています。日本や台湾などとの外交・軍事関係から、中国からの挑発的な軍事行動に対抗するため、航空機の増備に多額の投資を余儀なくされています。

中東での軍事紛争への米国の関与は、攻撃機や輸送機の調達を大きく後押ししました。空軍省は2023年度に1,940億米ドルの予算要求を提案したが、これは2022年度の予算要求から202億米ドル(11.7%)の増加です。例えば、2023年5月、米国空軍は、中国の軍事技術の急速な進歩に対抗して優位性を保つために、第6世代戦闘機の契約を2024年に締結する意向であることが発表されました。ロシア・ウクライナ戦争で米国からウクライナへの兵器供給が大幅に増加したことを受け、同国の国防機関は調達に余念がないです。

空軍はロシアの脅威に対処するため、いくつかの調達計画を成功させています。米国空軍の将来準備計画とともに、重要な調達イニシアチブのおかげで、空軍の需要は予測期間中に大幅な成長率を記録すると予想されます。

米国の航空宇宙・防衛産業概要

米国の航空宇宙・防衛市場は、その性質上、統合されています。同市場の有力企業には、General Dynamics Corporation、AirbusSE、Lockheed Martin Corporation、The Boeing Company、RTX Corporationなどがあります。規制の変化に伴い、企業はエンドユーザーの進化する要求に製品ポートフォリオを合わせなければならないです。市場はまた、現在の現役航空資産の能力を強化するためのアップグレード契約の分散によっても大きな影響を受けています。世界の政治戦線における米国の積極的な役割により、先進的な航空機、UAV、衛星の需要が伸びています。

長期契約を獲得し市場シェアを高めるため、参入企業は洗練された製品の研究開発に多額の投資を行っています。さらに、継続的な研究開発により、米国の航空宇宙・防衛市場のプラットフォームや関連製品ソリューションの技術的進歩が促進されています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場セグメンテーション

- 民間航空と一般航空

- 市場概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 市場動向

- セグメンテーション民間航空機

- 航空交通

- 訓練・フライトシミュレータ

- 空港サービス(地上支援設備とロジスティクス)

- 構造物

- 機体

- 材料(複合材、金属と金属合金、その他)

- 接着剤とコーティング

- エンジンとエンジンシステム

- 客室内装

- 着陸装置

- アビオニクスと制御システム

- 通信システム

- ナビゲーションシステム

- 飛行制御システム

- ヘルスモニタリングシステム

- 電気システム

- 環境制御システム

- 燃料と燃料システム

- MRO

- 研究開発

- サプライチェーン分析(設計、原料、製造、組立、検査、認証)

- 競合分析

- セグメンテーション一般航空

- 航空交通

- 訓練とフライトシミュレータ

- 空港サービス(地上支援設備とロジスティクス)

- 構造物

- 機体

- 材料(複合材、金属と金属合金、その他)

- 接着剤とコーティング

- エンジンとエンジンシステム

- 客室内装

- 着陸装置

- アビオニクスと制御システム

- 通信システム

- ナビゲーションシステム

- 飛行制御システム

- ヘルスモニタリングシステム

- 電気システム

- 環境制御システム

- 燃料と燃料システム

- MRO

- 研究開発

- サプライチェーン分析

- 競合分析

- 軍用機とシステム

- 市場概要

- 国防支出と予算配分の詳細

- 陸軍

- 海軍と海兵隊

- 空軍

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 市場動向

- MRO

- 研究開発

- 訓練とフライトシミュレータ

- 競合分析

- サプライチェーン分析

- 顧客/代理店情報

- セグメンテーション戦闘機

- 構造

- 機体

- 材料(複合材、金属と金属合金、その他)

- 接着剤とコーティング

- エンジンとエンジンシステム

- 着陸装置

- アビオニクスと制御システム

- 一般アビオニクス

- ミッション専用アビオニクス

- ミサイルと兵器

- セグメンテーション非戦闘機

- 構造

- 機体

- 材料(複合材、金属と金属合金、その他)

- 接着剤とコーティング

- エンジンとエンジンシステム

- 着陸装置

- アビオニクスと制御システム

- 一般アビオニクス

- ミッション専用アビオニクス

- ミサイルと兵器

- 無人航空機システム

- 市場概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 市場動向

- 研究開発

- 競合分析

- 規制状況と今後の施策変化

- セグメンテーション

- 商用

- 軍事用

- 宇宙システム機器

- 市場概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 市場動向

- 研究開発

- 競合分析

- 規制状況と今後の施策変更

- 顧客情報

- セグメンテーション宇宙ロケット、宇宙船、地上システム

- セグメンテーション衛星

- サブシステム別

- コマンド&コントロールシステム

- テレメトリ、トラッキング、コマンドリング、モニタリング(TTCM)

- アンテナシステム

- トランスポンダー

- 電力システム

- 用途別

- 軍事用

- 商用

第5章 競合情勢

- 企業プロファイル

- Airbus SE

- BAE Systems plc

- Fincantieri S.p.A

- GKN Aerospace

- Leonardo S.p.A

- Naval Group

- QinetiQ Group PLC

- Rheinmetall AG

- Rolls-Royce plc

- Safran SA

- THALES

- Lockheed Martin Corporation

- The Boeing Company

- RTX Corporation

- Northrop Grumman Corporation

- General Dynamics Corporation

- L3Harris Technologies Inc.

- Embraer SA

- Textron Inc.

目次

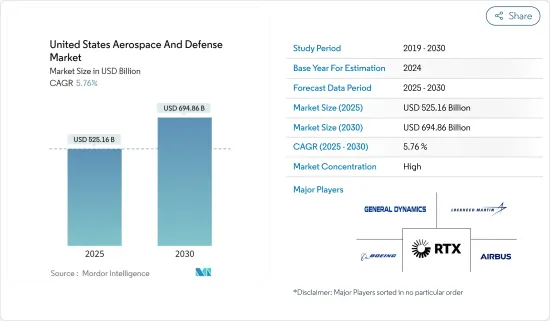

The United States Aerospace And Defense Market size is estimated at USD 525.16 billion in 2025, and is expected to reach USD 694.86 billion by 2030, at a CAGR of 5.76% during the forecast period (2025-2030).

The US aerospace and defense sector is one of the largest in terms of infrastructure and manufacturing activities. The market is expected to grow primarily due to the armed forces' procurement and upgrade activities to counter emerging threats. Several contracts from the military, air force, and naval force are currently underway, and many new contracts are anticipated to be dispersed during the forecast period, creating a parallel demand for defense equipment.

The US military uses multiple aircraft across the air force and naval aircraft. Owing to the increasing international conflict with China over its aggression in the South China Sea, the US is gearing up to tackle any potential issues China might create for countries with close ties with the US, like Taiwan and Japan. As a result, significant investments in upgrading the existing fleet and purchasing a new fleet equipped with efficient technologies have been witnessed over the past year.

The growing adoption of advanced technologies such as 3D printing, artificial intelligence, and big data analytics in developing aviation and defense equipment will create better opportunities in the coming years. However, issues related to the supply chain and evolving cybersecurity risks may hinder market growth.

United States Aerospace And Defense Market Trends

The Space Sector is Expected to Witness the Highest Growth During the Forecast Period

Space capabilities give the US and its allies unprecedented advantages in national decision-making, military operations, and homeland security. While a handful of private companies have driven the most recent space exploration efforts, there are ongoing discussions for establishing the Space Force as the sixth US military branch.

The US satellite manufacturing and launch industry is a rapidly evolving industry that plays a critical role in the country's space exploration and national security efforts. In recent years, this industry has undergone significant changes due to technological advancements, increasing demand for satellite services, and the presence of various prominent players. The demand for new satellite launches is driven by the need for various satellite services, such as providing low-latency internet access from space. In April 2022, Kuiper Systems LLC, a subsidiary of Amazon, announced that it had received approval from the Federal Communications Commission to launch 1,500 satellites by 2026. The company plans to reach 3,236 satellites by 2029, offering broadband internet services worldwide. The company secured around 83 launch services from Blue Origin, Arianespace, and United Launch Alliance (ULA) to launch these satellites.

The US Space Command will likely benefit the US Department of Defense (DoD) and the US aerospace and defense industry. The US Space Command, which oversees space operations using personnel and assets managed by the Space Force, will likely support A&D companies in accelerating investments in innovative technologies and capabilities. Thus, growing spending on space research and development and an increasing number of satellite launches drive market growth across the country.

The Air Force is Expected to Showcase Remarkable Growth During the Forecast Period

The US Air Force is equipped with the most modern technology that provides air support for land and naval forces and aids the troops on and around a battlefield. The Air Force continues developing and procuring next-generation aircraft to meet the demands of significant power conflicts with Russia and China. The US Air Force comprises 13,247 operational, reserve, and out-of-service aircraft. The country's diplomatic and military relations with nations such as Japan and Taiwan have compelled it to drive significant investments into increasing the fleet of aircraft to counter any provocative military action from China successfully.

The US involvement in the military conflict in the Middle East majorly drove its procurement of attack aircraft and transport aircraft. The Department of Air Force proposed a budget request of USD 194 billion for FY 2023, an increase of USD 20.2 billion or 11.7% from the FY 2022 budget request. For instance, in May 2023, it was announced that the US Air Force intends to award a contract in 2024 for its sixth-generation fighter jet as it races to retain its edge against rapid advances in Chinese military technology. The country's defense agencies have been on a spree of procurements given the Russia-Ukraine War that drove significant US weapon supply to Ukraine.

The Air Force has successfully implemented several procurement plans to tackle any Russian threat. Owing to significant procurement initiatives, together with the future-ready plans of the USAF, the demand in the Air Force is expected to register a substantial growth rate during the forecast period.

US Aerospace & Defense Industry Overview

The US aerospace and defense market is consolidated in nature. Some prominent players in the market are General Dynamics Corporation, Airbus SE, Lockheed Martin Corporation, The Boeing Company, and RTX Corporation. With the changing regulations, companies must align their product portfolio to the evolving requirements of end users. The market is also significantly influenced by the dispersion of upgrade contracts to enhance the capabilities of the current fleet of active aerial assets. The active role of the US in the global political front has resulted in the growth of the demand for advanced aircraft, UAVs, and satellites.

In order to gain long-term contracts and enhance market share, players are investing significantly in the R&D of sophisticated product offerings. Furthermore, continuous R&D has fostered technological advancements in platforms and associated products and solutions of the US aerospace and defense market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET SEGMENTATION

- 4.1 Commercial and General Aviation

- 4.1.1 Market Overview

- 4.1.2 Market Dynamics

- 4.1.2.1 Drivers

- 4.1.2.2 Restraints

- 4.1.2.3 Opportunities

- 4.1.3 Market Trends

- 4.1.4 Segmentation: Commercial Aircraft

- 4.1.4.1 Air Traffic

- 4.1.4.2 Training and Flight Simulators

- 4.1.4.3 Airport Services (Ground Support Equipment and Logistics)

- 4.1.4.4 Structures

- 4.1.4.4.1 Airframe

- 4.1.4.4.1.1 Materials (Composite, Metal and Metal Alloys, Others)

- 4.1.4.4.1.2 Adhesives and Coatings

- 4.1.4.4.2 Engine and Engine Systems

- 4.1.4.4.3 Cabin Interiors

- 4.1.4.4.4 Landing Gear

- 4.1.4.4.5 Avionics and Control Systems

- 4.1.4.4.5.1 Communication System

- 4.1.4.4.5.2 Navigation System

- 4.1.4.4.5.3 Flight Control System

- 4.1.4.4.5.4 Health Monitoring System

- 4.1.4.4.6 Electrical Systems

- 4.1.4.4.7 Environmental Control Systems

- 4.1.4.4.8 Fuel and Fuel Systems

- 4.1.4.4.9 MRO

- 4.1.4.4.10 Research and Development

- 4.1.4.4.11 Supply Chain Analysis (Design, Raw Materials, Manufacturing, Assembly, Testing, and Certification)

- 4.1.4.4.12 Competitor Analysis

- 4.1.5 Segmentation: General Aviation (includes Business Jets, Helicopter, and Personal Aircraft)

- 4.1.5.1 Air Traffic

- 4.1.5.2 Training and Flight Simulators

- 4.1.5.3 Airport Services (Ground Support Equipment and Logistics)

- 4.1.5.4 Structures

- 4.1.5.4.1 Airframe

- 4.1.5.4.1.1 Materials (Composite, Metal and Metal Alloys, Others)

- 4.1.5.4.1.2 Adhesives and Coatings

- 4.1.5.4.2 Engine and Engine Systems

- 4.1.5.4.3 Cabin Interiors

- 4.1.5.4.4 Landing Gear

- 4.1.5.4.5 Avionics and Control Systems

- 4.1.5.4.5.1 Communication System

- 4.1.5.4.5.2 Navigation System

- 4.1.5.4.5.3 Flight Control System

- 4.1.5.4.5.4 Health Monitoring System

- 4.1.5.4.6 Electrical Systems

- 4.1.5.4.7 Environmental Control Systems

- 4.1.5.4.8 Fuel and Fuel Systems

- 4.1.5.4.9 MRO

- 4.1.5.4.10 Research and Development

- 4.1.5.4.11 Supply Chain Analysis

- 4.1.5.4.12 Competitor Analysis

- 4.2 Military Aircraft and Systems

- 4.2.1 Market Overview

- 4.2.2 Defense Spending and Budget Allocation Details

- 4.2.2.1 Army

- 4.2.2.2 Navy and Marine Corps

- 4.2.2.3 Air Force

- 4.2.3 Market Dynamics

- 4.2.3.1 Drivers

- 4.2.3.2 Restraints

- 4.2.3.3 Opportunities

- 4.2.4 Market Trends

- 4.2.5 MRO

- 4.2.6 Research and Development

- 4.2.7 Training and Flight Simulators

- 4.2.8 Competitor Analysis

- 4.2.9 Supply Chain Analysis

- 4.2.10 Customer/Distributor Information

- 4.2.11 Segmentation: Combat Aircraft

- 4.2.11.1 Structures

- 4.2.11.1.1 Airframe

- 4.2.11.1.1.1 Materials (Composite, Metal and Metal Alloys, Others)

- 4.2.11.1.1.2 Adhesives and Coatings

- 4.2.11.1.2 Engine and Engine Systems

- 4.2.11.1.3 Landing Gear

- 4.2.11.2 Avionics and Control Systems

- 4.2.11.2.1 General Avionics

- 4.2.11.2.2 Mission Specific Avionics

- 4.2.11.3 Missiles and Weapons

- 4.2.12 Segmentation: Non-Combat Aircraft

- 4.2.12.1 Structures

- 4.2.12.1.1 Airframe

- 4.2.12.1.1.1 Materials (Composite, Metal and Metal Alloys, Others)

- 4.2.12.1.1.2 Adhesives and Coatings

- 4.2.12.1.2 Engine and Engine Systems

- 4.2.12.1.3 Landing Gear

- 4.2.12.2 Avionics and Control Systems

- 4.2.12.2.1 General Avionics

- 4.2.12.2.2 Mission Specific Avionics

- 4.2.12.3 Missiles and Weapons

- 4.3 Unmanned Aerial Systems

- 4.3.1 Market Overview

- 4.3.2 Market Dynamics

- 4.3.2.1 Drivers

- 4.3.2.2 Restraints

- 4.3.2.3 Opportunities

- 4.3.3 Market Trends

- 4.3.4 Research and Development

- 4.3.5 Competitor Analysis

- 4.3.6 Regulatory Landscape and Future Policy Changes

- 4.3.7 Segmentation

- 4.3.7.1 Commercial

- 4.3.7.2 Military

- 4.4 Space Systems and Equipment

- 4.4.1 Market Overview

- 4.4.2 Market Dynamics

- 4.4.2.1 Drivers

- 4.4.2.2 Restraints

- 4.4.2.3 Opportunities

- 4.4.3 Market Trends

- 4.4.4 Research and Development

- 4.4.5 Competitor Analysis

- 4.4.6 Regulatory Landscape and Future Policy Changes

- 4.4.7 Customer Information

- 4.4.8 Segmentation: Space Launch Vehicle, Spacecraft, and Ground Systems (Market Size and Forecast)

- 4.4.9 Segmentation: Satellites

- 4.4.9.1 By Subsystem

- 4.4.9.1.1 Command and Control System

- 4.4.9.1.2 Telemetry, Tracking, Commanding and Monitoring (TTCM)

- 4.4.9.1.3 Antenna System

- 4.4.9.1.4 Transponders

- 4.4.9.1.5 Power System

- 4.4.9.2 By Application

- 4.4.9.2.1 Military

- 4.4.9.2.2 Commercial

5 COMPETITIVE LANDSCAPE

- 5.1 Company Profiles

- 5.1.1 Airbus SE

- 5.1.2 BAE Systems plc

- 5.1.3 Fincantieri S.p.A

- 5.1.4 GKN Aerospace

- 5.1.5 Leonardo S.p.A

- 5.1.6 Naval Group

- 5.1.7 QinetiQ Group PLC

- 5.1.8 Rheinmetall AG

- 5.1.9 Rolls-Royce plc

- 5.1.10 Safran SA

- 5.1.11 THALES

- 5.1.12 Lockheed Martin Corporation

- 5.1.13 The Boeing Company

- 5.1.14 RTX Corporation

- 5.1.15 Northrop Grumman Corporation

- 5.1.16 General Dynamics Corporation

- 5.1.17 L3Harris Technologies Inc.

- 5.1.18 Embraer SA

- 5.1.19 Textron Inc.

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 116 Pages

- 納期

- 2~3営業日