|

市場調査レポート

商品コード

1687917

欧州の航空宇宙および防衛:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Aerospace And Defense - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の航空宇宙および防衛:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

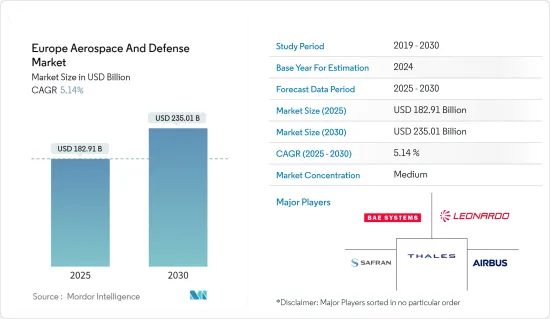

欧州の航空宇宙および防衛市場規模は2025年に1,829億1,000万米ドルと推計され、予測期間(2025-2030年)のCAGRは5.14%で、2030年には2,350億1,000万米ドルに達すると予測されます。

欧州市場は主に、新たな脅威に対抗するための軍の調達とアップグレード活動によって成長すると予想されます。欧州諸国の軍隊は、空軍機や海軍機など複数の航空機を使用しています。ロシア、ウクライナ、中東で国際紛争が増加しているため、欧州各国はこのような紛争から生じる潜在的な問題に対処するための準備を進めています。その結果、既存の航空機のアップグレードや、効率的な技術を搭載した新しい航空機の購入に多額の投資が行われています。

欧州の航空宇宙および防衛市場は、技術の急速な進歩によって革命的な変化を遂げつつあります。人工知能(AI)、先端素材、3Dプリンティング、自律型・無人システムといった最先端の技術革新が業界を再構築しています。BAE Systems PLC、Dassault Aviation SA、Fincantieri SpA、GKN Aerospace、Leonardo SpAといった企業が最前線に立ち、次世代航空機の先駆けとなる研究開発に多額の投資を行っています。AIや先端素材を取り入れることで、有人プラットフォームの性能が向上し、無人システムの需要が高まる。

航空宇宙および防衛産業は大きな成長を遂げようとしている一方で、サプライチェーンの脆弱性という手ごわい課題に直面しています。COVID-19パンデミックが生産とロジスティクスに与えた影響からも明らかなように、この業界のサプライチェーンは、しばしば世界で複雑なため、混乱の影響を受けやすいです。これらのサプライチェーンの回復力を確保することは、一貫した操業を維持し、防衛計画の要求に応えるために極めて重要です。同様に、少なくとも欧州市場での半導体船不足は2024年まで続くと思われます。しかし、欧州では、技術の変化、労働力不足、工場火災、サイバー攻撃などに対処しながら、独自の工場を建設し、台湾からの生産シフトを進めています。こうした要因は、予測期間中、欧州市場の需要を促進すると予想されます。

欧州航空宇宙および防衛市場の動向

商用・一般航空機分野が予測期間中に最も高い市場成長を遂げる見込み

COVID-19パンデミック後、欧州全域で航空旅客数が大幅に増加し、ほとんどの国でパンデミック前の航空旅客数に達し、それを上回っています。2023年1~9月の欧州連合(EU)全体の旅客輸送量は約7億4,900万人で、2022年比で21%増加しました。同期間におけるEU域外への国際輸送はEU全体の旅客数の48.5%を占め、EU域内の国際輸送と国内輸送のシェアはそれぞれ約36.2%と15.3%でした。

その後、欧州各国の航空会社は新たな民間航空機を発注しており、また一部の航空会社は、増加する旅客数に対応するため、既存の航空機をアップグレードしています。この地域全体では、2023年の民間航空機納入数は約324機で、2022年の納入数と比べて17%増加しました。2023年10月に発表されたインターナショナル・エアラインズ・グループ(IAG)の20機のワイドボディ・ジェット機発注計画には、英国でブリティッシュ・エアウェイズが運航するB777型機の一部を置き換えるものが含まれます。さらに、ルフトハンザは2023年12月、B737-8 MAX 40機とA220-300 40機を含む、高効率の短・中距離路線用航空機80機を新たに発注しました。これらは2026年から2032年にかけて納入される予定です。

2023年のビジネス航空の回復は、2020年と2021年に比べてより持続的でした。HNWIの急増は、リージョナル市場におけるビジネスジェット・セグメントを後押しすると予想され、2024年から2030年にかけて約1,120機が納入される見込みです。2023年、欧州のUHNWI数は2022年比で1.8%増加しました。これは、ユーロ圏の公益事業、ハイテク株、高級品業界が好調に推移し、堅調な伸びを記録したためです。納入実績では、2017年から2023年にかけて、大型ジェット機セグメントが52%のシェアで欧州市場を席巻し、次いで小型ジェット機が35%、中型ジェット機が13%のシェアを占めました。

その一環として、複数のヘリコプターがさまざまな地域で就航しています。よりクリーンなエネルギーへの移行が進むなか、風力エネルギーはエネルギー危機を打開する有力な選択肢となっています。このように欧州各国でヘリコプター・サービスの需要が高まっているため、民間ヘリコプターの需要が高まっています。エアバス・ヘリコプターズは2022年3月にH160の増産を発表しており、ロシアのヘリコプター・サービス会社が需要リストのトップになると予想されています。しかし、ロシア・ウクライナ戦争により、ロシアは世界のその他の地域から大きな経済制裁を受けており、ロシアはエアバスの生産停止を余儀なくされる可能性が高いと予想されます。このような調達・開発要因は、予測期間中の市場の需要を促進すると予想されます。

予測期間中、市場の成長が期待されるドイツ

商業部門では、ドイツの航空宇宙および防衛市場の需要は、主に航空交通量の増加によって煽られ、それに比例して新しい航空機の納入需要が創出されます。例えば、2023年にドイツの全空港で処理された旅客数は1億5,200万人で、1億2,700万人であった2022年と比較して19%の成長でした。このデータは、航空旅客数の増加を浮き彫りにしています。この増加傾向に対応するため、多くの航空会社が航空旅客輸送量の増加に対応するために新しい航空機を発注しています。例えば、ルフトハンザドイツ航空は2023年12月、エアバスとボーイングに対し、2026年から2032年の間に80機の新造航空機を納入する契約を結びました。この契約では、ボーイングはB737 MAX 8を40機、エアバスはA220-300を40機納入します。この契約には、B737 MAX 8 60機、A220 20機、エアバスA320 40機のオプションも含まれています。

ジェネラル・アビエーション・セグメントでは、超富裕層(UHNWI)の増加が市場の需要に大きな影響を及ぼしています。これらの富裕層は、プライベートの旅行ニーズのためにビジネス・ジェットを好み、しばしば購入します。彼らの富と旅行ニーズが高まるにつれて、ビジネスジェットやその他のプライベート航空サービスへの需要は増加の一途をたどっています。例えば、2023年には、成長率1.1%で、UHNWI人口は29,021人に達し、前年の28,711人を上回る。

さらに、2019年から2023年の間に、82機のビジネスジェットが納入されました。航空救急サービス、捜索救助任務、政府目的で使用されるヘリコプターのドイツ市場におけるエアバスの優位性は、業界をリードするプロバイダーとしての地位を確固たるものにしています。2023年12月現在、エアバスの市場シェアは61%に達し、こうした重要産業の多様なニーズに対応する能力を示しています。エアバスに次いで、ユーロコプターが37%の第2位の市場シェアを占めています。同期間中、同国のヘリコプター保有数は255機で、そのうち121機が航空救急サービス用、109機が政府用、22機が捜索救助活動用、1機が消防用として配備されていました。

軍事部門では、ドイツの軍事力を強化し、テロリズムなどの地政学的脅威に対応することを目的とした国防費の増加が、この市場の拡大を後押ししています。2023年の国防予算は668億米ドルで、同国はこの地域で第3位、世界でも第7位の国防支出国です。ロシアとウクライナの戦争により、ドイツ政府は軍事力のための特別基金の一部として1,070億米ドルを割り当て、国防費を国内総生産(GDP)の2%以上に引き上げる計画を発表しました。

ドイツは、安全保障上の脅威が増大していることを考慮し、国防能力への投資を大幅に拡大しました。この資源配分の増加は、国の安全保障体制を強化するために、国の行政部隊をアップグレードし、強化することを目的としています。例えば、2024年4月、ドイツはラインメタル・ディフェンス・オーストラリアに、ドイツ陸軍向けにボクサー重戦車123両を27億米ドルで発注し、2025年から納入を開始しました。同様に2024年6月、ラインメタルはドイツから榴弾砲弾20万発(9億5,700万米ドル)の供給契約を獲得しました。ドイツはウクライナのロシア軍への対抗を支援するため、新たに獲得したこれらの砲弾はドイツ軍の備蓄を補充することになります。

ドイツはまた、衛星製造への民間投資を誘致するための新法も起草しています。ドイツはその技術的優位性で世界的に有名です。従って、整備された法的枠組みは、地元市場のプレーヤーが運用能力を強化し、新興の宇宙経済に対応することを可能にするかもしれないです。例えば、2019年から2023年の間に、23基の衛星が製造され、国内の様々な事業者によって打ち上げられました。最も多くの衛星を打ち上げたロケットはSoyuz-2.1bで、7機近くの衛星を搭載し、次いでFalcon 9が5機の衛星を打ち上げました。これらの開発により、予測期間を通じてこれらの分野の市場需要がプラスに働くと予想されます。

欧州の航空宇宙および防衛産業の概要

同市場は、エアバスSE、BAEシステムズPLC、レオナルドSpA、サフランSA、THALESなどの世界的企業が大きなシェアを占めており、半固体化しています。この地域のいくつかの国で地政学的不安が高まっていることが、安全保障環境の新興化に寄与しており、先進的な航空機、UAV、衛星に対する需要が高まっています。長期契約を確保し市場シェアを向上させるため、プレーヤーは洗練された製品の研究開発に多額の投資を行っています。継続的な研究開発により、欧州の航空宇宙および防衛市場におけるプラットフォームや関連製品・ソリューションの技術的進歩が促進されています。例えば、2023年9月、エールフランスはエアバスとA350を50機、さらに40機のオプション付きで契約しました。この発注は、50機のA350-900およびA350-1000と、40機の追加購入権をカバーするもので、最初の納入は2026年から2030年に完了する予定です。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヵ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場セグメンテーション

- 民間航空と一般航空

- 市場概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 市場動向

- 商用航空機

- 航空交通

- 訓練とフライト・シミュレーター

- 空港サービス(地上支援設備とロジスティクス)

- 構造物

- 機体

- 材料(複合材料、金属および金属合金、その他の材料)

- 接着剤とコーティング

- エンジンおよびエンジンシステム

- 客室内装

- 着陸装置

- アビオニクスと制御システム

- 通信システム

- ナビゲーションシステム

- 飛行制御システム

- ヘルスモニタリングシステム

- 電気システム

- 環境制御システム

- 燃料および燃料システム

- MRO

- 研究開発

- サプライチェーン分析(設計、原材料、製造、組立、試験、認証)

- 競合分析

- 一般航空

- 航空交通

- 訓練とフライトシミュレーター

- 空港サービス(地上支援設備とロジスティクス)

- 構造物

- 機体

- 材料(複合材料、金属および金属合金、その他の材料)

- 接着剤とコーティング

- エンジンおよびエンジンシステム

- 客室内装

- 着陸装置

- アビオニクスと制御システム

- 通信システム

- ナビゲーションシステム

- 飛行制御システム

- ヘルスモニタリングシステム

- 電気システム

- 環境制御システム

- 燃料および燃料システム

- MRO

- 研究開発

- サプライチェーン分析

- 競合分析

- 軍用機とシステム

- 市場概要

- 国防支出と予算配分の詳細

- 陸軍

- 海軍と海兵隊

- 空軍

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 市場動向

- MRO

- 研究開発

- 訓練とフライトシミュレーター

- 競合分析

- サプライチェーン分析

- 顧客/代理店情報

- 戦闘機

- 構造

- 機体

- 材料(複合材、金属および金属合金、その他の材料)

- 接着剤とコーティング

- エンジンおよびエンジンシステム

- 着陸装置

- アビオニクスと制御システム

- 一般アビオニクス

- ミッション専用アビオニクス

- ミサイルおよび兵器

- 非戦闘機

- 構造

- 機体

- 材料(複合材料、金属および金属合金、その他の材料)

- 接着剤とコーティング

- エンジンおよびエンジンシステム

- 着陸装置

- アビオニクスと制御システム

- 一般アビオニクス

- ミッション専用アビオニクス

- ミサイルおよび兵器

- 無人航空機システム

- 市場概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 市場動向

- 研究開発

- 競合分析

- 規制状況と今後の政策変化

- セグメンテーション

- 商業

- 軍事

- 宇宙システム・機器

- 市場概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 市場動向

- 研究開発

- 競合分析

- 規制状況と今後の政策変更

- 顧客情報

- セグメンテーション宇宙ロケット、宇宙船、地上システム

- セグメンテーション衛星

- サブシステム別

- コマンド&コントロールシステム

- テレメトリ、トラッキング、コマンドリング、モニタリング(TTCM)

- アンテナシステム

- トランスポンダー

- 電力システム

- 用途別

- 軍事

- 商用

- 地域別

- 英国

- フランス

- ドイツ

- イタリア

- スペイン

- その他欧州

第5章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Airbus SE

- BAE Systems PLC

- Dassault Aviation SA

- Fincantieri SpA

- GKN Aerospace

- Leonardo SpA

- Naval Group

- QinetiQ Group PLC

- Rheinmetall AG

- Rolls-Royce PLC

- Rostec

- Safran SA

- THALES

- Lockheed Martin Corporation

第6章 市場機会と今後の動向

The Europe Aerospace And Defense Market size is estimated at USD 182.91 billion in 2025, and is expected to reach USD 235.01 billion by 2030, at a CAGR of 5.14% during the forecast period (2025-2030).

The European market is expected to grow primarily due to the armed forces' procurement and upgradation activities to counter emerging threats. Military forces in European countries use multiple aircraft across their Air Force and naval aircraft. Owing to the increasing international conflicts in Russia, Ukraine, and the Middle East, countries in Europe are gearing up to tackle any potential issues arising from such conflicts. As a result, significant investments in upgrading the existing fleet and purchasing a new fleet equipped with efficient technologies have been witnessed over the past year.

The European aerospace and defense market is undergoing a revolutionary shift driven by rapid advancements in technologies. Cutting-edge innovations in artificial intelligence (AI), advanced materials, 3D printing, and autonomous and unmanned systems are reshaping the industry. Companies like BAE Systems PLC, Dassault Aviation SA, Fincantieri SpA, GKN Aerospace, and Leonardo SpA are at the forefront, investing substantially in research and development to usher in the next generation of aircraft. Incorporating AI and advanced materials enhances the performance of manned platforms and promotes high demand for unmanned systems.

While the aerospace and defense industry stands on the cusp of significant growth, it faces formidable challenges in supply chain vulnerabilities. The industry's supply chains, often global and intricate, are susceptible to disruptions, as evidenced by the impact of the COVID-19 pandemic on production and logistics. Ensuring the resilience of these supply chains is crucial for maintaining consistent operations and meeting the demands of defense programs. Similarly, at least semiconductor ship shortages in the European market will continue till 2024. However, Europe is building its own factories and shifting production away from Taiwan while dealing with changing technology, labor shortages, factory fires, and cyber attacks. Such factors are expected to drive demand in the European market during the forecast period.

Europe Aerospace and Defense Market Trends

The Commercial and General Aviation Aircraft Segment is Expected to Witness the Highest Market Growth During the Forecast Period

There has been a tremendous increase in air passenger traffic across Europe after the COVID-19 pandemic, and most countries have reached and exceeded their pre-pandemic air passenger numbers. In the first nine months of 2023, passenger traffic across the European Union was around 749 million, a 21% growth compared to 2022. International extra-EU transport accounted for 48.5% of all passengers across the European Union in the same period, while international intra-EU and national transport shares were around 36.2% and 15.3%, respectively.

Subsequently, airlines across European countries are ordering new commercial aircraft, and some are upgrading their existing fleet to serve the increasing number of passengers. Across the region, the number of commercial aircraft deliveries in 2023 was around 324, a 17% increase compared to the deliveries in 2022. Some ongoing and future commercial aircraft orders include the plans of International Airlines Group (IAG), announced in October 2023, to order 20 widebody jets to replace some of the B777s operated by British Airways in the United Kingdom. Additionally, in December 2023, Lufthansa ordered 80 new highly efficient short-and medium-haul aircraft, including 40 B737-8 MAX and 40 A220-300s, with an option of 120 aircraft. These will be delivered from 2026 to 2032.

The recovery of business aviation in 2023 was more sustained compared to 2020 and 2021. The surge in HNWI individuals is expected to aid the business jet segment in the regional market, and around 1,120 aircraft are expected to be delivered between 2024 and 2030. In 2023, the number of UHNWIs in Europe increased by 1.8% compared to 2022. This was because the Eurozone utilities, tech stocks, and luxury goods industries performed well, registering solid gains. In terms of deliveries, during 2017-2023, the large jet segment dominated the European market with a 52% share, followed by light and mid-size jets accounting for shares of 35% and 13%, respectively.

As part of this, several helicopters have been introduced into service in different geographical places. With the increasing transition toward cleaner energy, wind energy has become a viable alternative to the energy crisis, owing to which several countries have been investing in developing offshore wind farms to harvest electricity from winds. This increasing demand for helicopter services across European countries prompts the requirement for civil helicopters. Some of the procurements include Airbus Helicopters, which, in March 2022, announced the ramp-up of H160 production, with Russian helicopter service companies expected to top the demand list. However, the Russia-Ukraine war has led to significant economic sanctions on Russia from the rest of the world, and it is expected that Russia would likely force Airbus to halt production. Such procurement and development factors are expected to drive the demand in the market during the forecast period.

Germany Expected to Witness Market Growth During the Forecast Period

In the commercial segment, the demand in the aerospace and defense market in Germany is primarily fueled by increasing air traffic, which proportionally creates demand for new aircraft deliveries. For instance, in 2023, the passengers processed across all German airports accounted for 152 million, with a growth of 19% compared to 2022, which was recorded at 127 million. The data highlights a rise in air passenger traffic. In response to this growing trend, numerous airlines are placing orders for new aircraft to accommodate the increasing air passenger traffic. For instance, in December 2023, Lufthansa awarded contracts to Airbus and Boeing for 80 new aircraft deliveries between 2026 and 2032. Under the contract, Boeing will deliver 40 B737 MAX 8s, and Airbus will deliver 40 A220-300s. The agreement also covers options for 60 B737 MAX 8, 20 A220, and 40 Airbus A320s.

In the general aviation segment, the market demand is significantly influenced by the increasing number of ultra high net worth individuals (UHNWIs). These individuals prefer and often acquire business jets for their private travel needs. As their wealth and travel requirements grow, the demand for business jets and other private aviation services continues to rise. For instance, in 2023, with a growth rate of 1.1%, the UHNWI population reached 29,021 individuals, surpassing the previous year's count of 28,711.

Moreover, during 2019-2023, 82 business jets were delivered. The dominance of Airbus in the German market for helicopters used in air ambulance services, search and rescue missions, and government purposes has solidified its position as the leading provider in the industry. As of December 2023, Airbus commanded an impressive 61% market share, showcasing its ability to meet the diverse needs of these critical industries. Followed by Airbus, Eurocopter held the second-largest market share, amounting to 37%. During the same period, the country's helicopter fleet consisted of 255 helicopters, of which 121 were deployed for air ambulance services, 109 were used by the government, 22 were designated for search and rescue operations, and one for fire service.

In the military segment, the expansion of this market is being propelled by the rising defense expenditures aimed at enhancing Germany's military capabilities and adapting to emerging geopolitical threats such as terrorism. The country was the third-largest defense spender in the region and the seventh-largest globally, with a defense budget of USD 66.8 billion in 2023. Due to the Russia-Ukraine war, the German government announced plans to allocate USD 107 billion as part of a special fund for its military forces and raise its defense spending to over 2% of its gross domestic product (GDP).

Germany has substantially ramped up its defense capability investments, considering growing security threats. This increased allocation of resources is geared toward upgrading and fortifying the nation's administrative forces to bolster the country's security framework. For instance, in April 2024, Germany awarded Rheinmetall Defence Australia a contract to deliver 123 Boxer Heavy Weapon Carrier vehicles for the German Army for USD 2.7 billion, with deliveries starting in 2025. Similarly, in June 2024, Rheinmetall was granted a contract by Germany to supply 200,000 howitzer shells valued at USD 957 million. These newly acquired shells will replenish the German army's stockpiles as Germany supports Ukraine in countering the Russian military forces.

Germany is also drafting new laws to attract private investments in satellite manufacturing. The country is renowned globally for its technical superiority. Thus, a well-formulated legal framework may enable localized market players to enhance their operational capabilities and cater to an emerging space economy. For instance, during 2019-2023, 23 satellites were manufactured and launched by various operators across the country. The launch vehicle that launched the most satellites was Soyuz-2.1b, which carried nearly seven satellites, followed by Falcon 9, which launched five satellites. These developments are anticipated to positively drive market demand in these segments throughout the forecast period.

Europe Aerospace and Defense Industry Overview

The market is semi-consolidated, with several global players, including Airbus SE, BAE Systems PLC, Leonardo SpA, Safran SA, and THALES, occupying a significant market share. The growing geopolitical unrest across several countries in the region contributes to an emerging security environment, with increasing demand for advanced aircraft, UAVs, and satellites. To secure long-term contracts and improve their market share, players are investing significantly in the R&D of sophisticated product offerings. Continuous R&D has fostered technological advancements in platforms and associated products and solutions in the European aerospace and defense market. For instance, in September 2023, Air France sealed a deal with Airbus for 50 A350s, with an option for 40 more. This order will cover 50 A350-900 and A350-1000 aircraft, along with purchase rights for 40 additional aircraft, with the first deliveries expected to be completed in 2026 through 2030.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET SEGMENTATION

- 4.1 Commercial and General Aviation

- 4.1.1 Market Overview

- 4.1.2 Market Dynamics

- 4.1.2.1 Drivers

- 4.1.2.2 Restraints

- 4.1.2.3 Opportunities

- 4.1.3 Market Trends

- 4.1.4 Commercial Aircraft

- 4.1.4.1 Air Traffic

- 4.1.4.2 Training and Flight Simulators

- 4.1.4.3 Airport Services (Ground Support Equipment and Logistics)

- 4.1.4.4 Structures

- 4.1.4.4.1 Airframe

- 4.1.4.4.1.1 Materials (Composite, Metal and Metal Alloys, Other Materials)

- 4.1.4.4.1.2 Adhesives and Coatings

- 4.1.4.4.2 Engine and Engine Systems

- 4.1.4.4.3 Cabin Interiors

- 4.1.4.4.4 Landing Gear

- 4.1.4.4.5 Avionics and Control Systems

- 4.1.4.4.5.1 Communication System

- 4.1.4.4.5.2 Navigation System

- 4.1.4.4.5.3 Flight Control System

- 4.1.4.4.5.4 Health Monitoring System

- 4.1.4.4.6 Electrical Systems

- 4.1.4.4.7 Environmental Control Systems

- 4.1.4.4.8 Fuel and Fuel Systems

- 4.1.4.4.9 MRO

- 4.1.4.4.10 Research and Development

- 4.1.4.4.11 Supply Chain Analysis (Design, Raw Materials, Manufacturing, Assembly, Testing, and Certification)

- 4.1.4.4.12 Competitor Analysis

- 4.1.5 General Aviation (Includes Business Jets, Helicopter, and Personal Aircraft)

- 4.1.5.1 Air Traffic

- 4.1.5.2 Training and Flight Simulators

- 4.1.5.3 Airport Services (Ground Support Equipment and Logistics)

- 4.1.5.4 Structures

- 4.1.5.4.1 Airframe

- 4.1.5.4.1.1 Materials (Composite, Metal and Metal Alloys, Other Materials)

- 4.1.5.4.1.2 Adhesives and Coatings

- 4.1.5.4.2 Engine and Engine Systems

- 4.1.5.4.3 Cabin Interiors

- 4.1.5.4.4 Landing Gear

- 4.1.5.4.5 Avionics and Control Systems

- 4.1.5.4.5.1 Communication System

- 4.1.5.4.5.2 Navigation System

- 4.1.5.4.5.3 Flight Control System

- 4.1.5.4.5.4 Health Monitoring System

- 4.1.5.4.6 Electrical Systems

- 4.1.5.4.7 Environmental Control Systems

- 4.1.5.4.8 Fuel and Fuel Systems

- 4.1.5.4.9 MRO

- 4.1.5.4.10 Research and Development

- 4.1.5.4.11 Supply Chain Analysis

- 4.1.5.4.12 Competitor Analysis

- 4.2 Military Aircraft and Systems

- 4.2.1 Market Overview

- 4.2.2 Defense Spending and Budget Allocation Details

- 4.2.2.1 Army

- 4.2.2.2 Navy and Marine Corps

- 4.2.2.3 Air Force

- 4.2.3 Market Dynamics

- 4.2.3.1 Drivers

- 4.2.3.2 Restraints

- 4.2.3.3 Opportunities

- 4.2.4 Market Trends

- 4.2.5 MRO

- 4.2.6 Research and Development

- 4.2.7 Training and Flight Simulators

- 4.2.8 Competitor Analysis

- 4.2.9 Supply Chain Analysis

- 4.2.10 Customer/Distributor Information

- 4.2.11 Combat Aircraft

- 4.2.11.1 Structures

- 4.2.11.1.1 Airframe

- 4.2.11.1.1.1 Materials (Composite, Metal and Metal Alloys, Other Materials)

- 4.2.11.1.1.2 Adhesives and Coatings

- 4.2.11.1.2 Engine and Engine Systems

- 4.2.11.1.3 Landing Gear

- 4.2.11.2 Avionics and Control Systems

- 4.2.11.2.1 General Avionics

- 4.2.11.2.2 Mission Specific Avionics

- 4.2.11.3 Missiles and Weapons

- 4.2.12 Non-combat Aircraft

- 4.2.12.1 Structures

- 4.2.12.1.1 Airframe

- 4.2.12.1.1.1 Materials (Composite, Metal and Metal Alloys, Other Materials)

- 4.2.12.1.1.2 Adhesives and Coatings

- 4.2.12.1.2 Engine and Engine Systems

- 4.2.12.1.3 Landing Gear

- 4.2.12.2 Avionics and Control Systems

- 4.2.12.2.1 General Avionics

- 4.2.12.2.2 Mission-specific Avionics

- 4.2.12.3 Missiles and Weapons

- 4.3 Unmanned Aerial Systems

- 4.3.1 Market Overview

- 4.3.2 Market Dynamics

- 4.3.2.1 Drivers

- 4.3.2.2 Restraints

- 4.3.2.3 Opportunities

- 4.3.3 Market Trends

- 4.3.4 Research and Development

- 4.3.5 Competitor Analysis

- 4.3.6 Regulatory Landscape and Future Policy Changes

- 4.3.7 Segmentation

- 4.3.7.1 Commercial

- 4.3.7.2 Military

- 4.4 Space Systems and Equipment

- 4.4.1 Market Overview

- 4.4.2 Market Dynamics

- 4.4.2.1 Drivers

- 4.4.2.2 Restraints

- 4.4.2.3 Opportunities

- 4.4.3 Market Trends

- 4.4.4 Research and Development

- 4.4.5 Competitor Analysis

- 4.4.6 Regulatory Landscape and Future Policy Changes

- 4.4.7 Customer Information

- 4.4.8 Segmentation: Space Launch Vehicle, Spacecraft, and Ground Systems

- 4.4.9 Segmentation: Satellites

- 4.4.9.1 By Subsystem

- 4.4.9.1.1 Command and Control System

- 4.4.9.1.2 Telemetry, Tracking, Commanding, and Monitoring (TTCM)

- 4.4.9.1.3 Antenna System

- 4.4.9.1.4 Transponders

- 4.4.9.1.5 Power System

- 4.4.9.2 By Application

- 4.4.9.2.1 Military

- 4.4.9.2.2 Commercial

- 4.5 Geography

- 4.5.1 United Kingdom

- 4.5.2 France

- 4.5.3 Germany

- 4.5.4 Italy

- 4.5.5 Spain

- 4.5.6 Rest of Europe

5 COMPETITIVE LANDSCAPE

- 5.1 Vendor Market Share

- 5.2 Company Profiles

- 5.2.1 Airbus SE

- 5.2.2 BAE Systems PLC

- 5.2.3 Dassault Aviation SA

- 5.2.4 Fincantieri SpA

- 5.2.5 GKN Aerospace

- 5.2.6 Leonardo SpA

- 5.2.7 Naval Group

- 5.2.8 QinetiQ Group PLC

- 5.2.9 Rheinmetall AG

- 5.2.10 Rolls-Royce PLC

- 5.2.11 Rostec

- 5.2.12 Safran SA

- 5.2.13 THALES

- 5.2.14 Lockheed Martin Corporation