|

市場調査レポート

商品コード

1431711

橋梁建設:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Bridge Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 橋梁建設:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

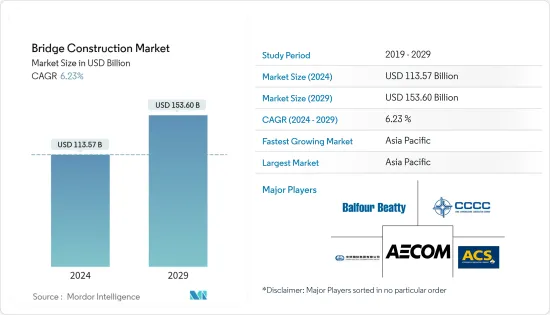

橋梁建設市場規模は2024年に1,135億7,000万米ドルと推定され、2029年には1,536億米ドルに達すると予測され、予測期間中(2024年~2029年)のCAGRは6.23%で成長する見込みです。

市場拡大の主な要因は、道路交通量の増加と自動車台数の拡大です。また、鉄道網の拡大や、交通インフラ整備のための官民連携が重視されるようになった結果、鉄道橋のニーズが高まっています。

橋梁建設市場は、組織、個人事業主、パートナーシップによる売上で構成されます。橋梁建設とは、水域、渓谷、高速道路などの物理的な障壁を越えるための構造物を建設することを指します。橋が構造的にどのような挙動を示すかにもよるが、橋の建設に使われる一般的な材料には、構造用鋼、鉄筋コンクリート、プレストレストコンクリート、ポストテンションコンクリートなどがあります。

梁橋、トラス橋、アーチ橋、吊り橋、斜張橋などが、一般的な橋梁の形式です。梁橋という用語は、両端の支柱の上に載り、交通を支える梁の役割を果たす水平構造物を指します。梁橋建設は、事業体(組織、パートナーシップ、個人事業主)によって販売されています。

梁は、そこにかかる静的および動的な応力を支えるのに十分な強度があります。橋の建設には、鋼鉄、コンクリート、複合材料などの材料が使われます。道路、高速道路、鉄道は、橋が建設されるインフラのひとつです。

このインフラは、ビル、道路、電力源、橋などの構造物を含むことで、家庭や企業の長期的な存続を支えています。拡大する交通量に対応する物理的なシステムからなるハードインフラには、橋も含まれます。

例えば、2021年2月に産業・貿易省(DPIIT)が発表した調査によると、2020年のインフラ開発・建設への直接投資は172億2,000万米ドルでした。2023年末には1兆4,000億米ドルに達すると予測されています。その結果、橋梁建設における今後の拡大は、インフラ開発への投資増加によって支えられることになります。

橋梁建設市場は、新技術の導入よって変化しています。橋梁建設市場の主要企業は、より良く、より速く、より長寿命の橋を建設するため、革新的な技術の統合に注力しています。道路-鉄道斜張橋のような新技術は、新しい橋、特に河川にかかる橋を建設する際に利用されています。

橋梁建設市場の動向

鉄道部門は、予想される期間中に大幅に拡大すると予想されます。

橋梁建設市場の分類には、タイプ、材料、用途、地域が用いられます。国際市場は、梁式、トラス式、アーチ式、吊り橋式、斜張橋式、その他などのタイプに分類されます。市場は、鋼鉄、コンクリート、複合材料のセグメントに分けられます。橋梁建設市場は、用途によって道路・高速道路と鉄道の2つのセグメントに分けられます。橋梁市場は地域別に調査され、北米、アジア太平洋、欧州が含まれます。都市化の進展とインフラ投資の増加により、アジア太平洋地域は調査期間を通じて世界の橋梁建設市場で大きなシェアを占めると予想されています。

カリフォルニア州(米国)の高速鉄道は、2022年10月現在、世界中で計画段階または実行段階にある最も価値のあるインフラプロジェクトの一つです。開発中の主要インフラプロジェクトのほとんどは、ノルウェーやスウェーデン、英国、米国、アジア・東南アジア、日本などの鉄道路線でした。2,500万米ドル以上の大型インフラプロジェクトが最も多かった国はインドでした。

例えば、インド初の垂直昇降式鉄道橋「Rail Sea Bridge」は、鉄道によって積極的に建設が進められています。インド本土とラーメスワラム島を結ぶインド初の垂直昇降式鉄道橋は、別名パンバン橋とも呼ばれ、インド鉄道省が工事の最新情報とともに投稿した写真で紹介されたばかりです。最新のデータによると、橋の工事の81%は終了しています。工事終了後、この橋はルートの交通量と交通ペースの増加に伴い、列車が追加重量を運ぶのを助けることになります。船舶やストリーマは、障害物に遭遇することなくこの橋を通過することができます。

鉄道省によると、インド本土とラーメスワラム島を結ぶインド初の垂直昇降式鉄道海上橋パンバン橋は、工事の81%を終えました。333本の杭がすべて建設され、101本の杭キャップと下部構造が完成し、99本の桁のうち76本が打ち上げられました。

アジア太平洋地域が市場を独占

アジア太平洋地域では、大規模なインフラ整備がかつてないほど重要になっています。都市化、人口増加、経済発展のすべてが、インフラの新設・更新の緊急需要に寄与しています。長期的なインフラ計画は、地域間のインフラ整備の格差によってさらに複雑になっています。先進経済諸国と新興経済諸国では、インフラの有無や充実度、インフラ・プロジェクトを計画し資金を調達する能力や能力が大きく異なるが、共通しているのは、予算が逼迫しているという問題です。インフラ整備に必要な資金を独占的に調達できる政府もあります。

アジア開発銀行(ADB)は、アジア地域が経済成長を維持し、貧困と闘い、気候変動リスクを軽減するためには、2030年までアジア全体で年間約1兆7,000億米ドルをインフラに投資する必要があると試算しました。これは2009年にADBが推奨した投資額の2倍以上です。予測されるインフラ需要と、実現されるインフラとの差は拡大しています。

中国では、2022年5月時点で2,500万米ドル以上のインフラプロジェクトが開発・実行されており、その規模は5兆米ドルを超えています。米国とインドがこれに続き、約2兆米ドル相当のインフラプロジェクトがあります。一方、大型インフラプロジェクトが最も多い国はインドでした。

2026年までに、世界の再生可能エネルギーによる発電容量は2020年比で60%以上増加し、現在の化石燃料と原子力を合わせた世界の総発電容量に匹敵すると予測されています。現在、世界人口の約40%が海岸から100km以内に住んでおり、沿岸生態系への圧力が高まっています。

橋梁建設業界の概要

ロボット、バーチャルリアリティ、拡張現実(AR)技術は、より速く、より低い運用コストで橋を建設するために利用されている最先端技術のひとつです。例えば、橋の構造性能を高めるために、バングラデシュで現在建設中の新しいアーチ式鋼橋では、橋の維持管理に最先端技術が使われています。ACS Group、AECOM、Balfour Beatty、China Communications Construction Company Limitedなどが主要な企業です。市場リーチを拡大し、市場で競争するために、大手企業は製品開発、事業拡大、契約、パートナーシップ、買収などの主な戦略を採用しました。これらの戦略は現在、より低い運用コストで橋を建設し、プロジェクトのリードタイムを短縮するために利用されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場分析

- 現在の経済と橋梁建設市場のシナリオ

- サプライチェーン/バリューチェーン分析への洞察

- 政府の規制と取り組みが業界に与える影響

- 政府のインフラ開発計画に関するレビューと解説

- COVID-19が市場に与える影響

第5章 市場力学

- 促進要因

- リサイクル材料を使った持続可能性の重視と環境への影響の最小化

- 強化ポリマーやステンレス鋼のような耐腐食性材料の採用

- 抑制要因

- 橋の建設には設計とエンジニアリングが不可欠

- 機会

- 技術革新

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者/買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第6章 市場セグメンテーション

- タイプ別

- 梁橋

- トラス橋

- アーチ橋

- 吊橋

- 斜張橋

- その他

- 材料別

- 鋼

- コンクリート

- 複合材料

- 用途別

- 道路・高速道路

- 鉄道

- 地域別

- 北米

- 米国

- カナダ

- その他北米

- ラテンアメリカ

- メキシコ

- ブラジル

- その他ラテンアメリカ

- 欧州

- 英国

- フランス

- その他欧州

- アジア太平洋

- 中国

- インド

- その他アジア太平洋

- 北米

第7章 競合情勢

- 市場集中度の概要

- 企業プロファイル

- ACS Group

- AECOM

- Balfour Beatty

- China Communications Construction Company Limited

- China Railway Group Ltd

- VINCI

- Bechtel

- Hochtief

- Skanska

- Bouygues Construction*

第8章 市場機会と今後の動向

第9章 主要インフラ開発プロジェクト

- 既存のインフラ

- 進行中のプロジェクト

- 今後のプロジェクト

第10章 付録

第11章 免責事項

The Bridge Construction Market size is estimated at USD 113.57 billion in 2024, and is expected to reach USD 153.60 billion by 2029, growing at a CAGR of 6.23% during the forecast period (2024-2029).

The key factors propelling market expansion are the rising volume of traffic on the roads and the expanding number of automobiles. In addition, the need for railway bridges is increasing as a result of the growth of rail networks and the increasing emphasis on public-private partnerships for the development of transportation infrastructure.

The bridge construction market comprises sales made by organizations, sole proprietors, and partnerships. Bridge construction refers to building a structure across a physical barrier, such as water bodies, valleys, or highways, to provide a crossing over that barrier. Depending on how the bridge will structurally behave, common materials used in bridge building include structural steel, reinforced concrete, pre-stressed concrete, and post-tensioned concrete.

Beam, truss, arch, suspension, and cable-stayed bridges are among the common forms of bridge construction. The term "beam bridge" refers to a horizontal structure that rests on two ends supports and acts as a beam to carry traffic. Beam bridge construction is sold by entities (organizations, partnerships, and sole proprietors).

The beam is strong enough to support the static and dynamic stresses placed on it. In the construction of bridges, materials like steel, concrete, and composites are used. Roads, highways, and railroads are among the infrastructure types for which bridges are built.

This infrastructure supports the long-term viability of homes and companies by including structures like buildings, roads, electricity sources, and bridges. Hard infrastructure, which consists of the physical systems that serve to handle expanding traffic, includes bridges.

For instance, according to a study released by the Department for Promotion of Industry and Internal Trade (DPIIT) in February 2021, FDI investments in infrastructure development and construction were USD 17.22 billion in 2020. They were projected to reach USD 1.4 trillion by the end of 2023. As a result, future expansion in bridge construction will be supported by increased investments in infrastructure development.

The bridge construction market is changing due to the introduction of new technology. Major corporations in the bridge construction market are concentrating on integrating innovative technologies to build better, faster, and longer lifespan bridges. New technologies like road-rail cable-stayed are utilized when building new bridges, particularly those over rivers.

Bridge Construction Market Trends

The railway sector is anticipated to expand significantly over the anticipated period.

Type, material, application, and geography are used to categorize the bridge construction market. The international market is divided into several types, including beam, truss, arch, suspension, cable-stayed, and others. The market is divided into steel, concrete, and composite material segments. The bridge building market is divided into two segments based on application: road & highway and railway. The bridge-building market is examined by region, including LAMEA, North America, Europe, and Asia-Pacific. Due to rising urbanization and increased investments in infrastructure, the Asia-Pacific region is anticipated to hold a disproportionately large share of the worldwide bridge-building market throughout the study period.

The High-Speed Rail Line in California (United States) was, as of October 2022, one of the most valuable infrastructure projects either in their planning or execution phase worldwide. Most of the major infrastructure projects in development were railway lines, such as the ones in Norway and Sweden, the UK, the US, Asia and South-East Asia, and Japan. The country with the highest number of great infrastructure projects valued at over USD 25 million was India.

For Instance, the first vertical lift Rail Sea Bridge in India is actively being constructed by Railways. The first vertical lift railway bridge in India, also known as the Pamban Bridge, which connects the Indian mainland with Rameswaram Island, just featured in photos posted by the Ministry of Indian Railways along with construction updates. According to the most recent data, 81% of the bridge's construction is finished. After construction is finished, the bridge will assist the trains in carrying additional weight due to the increasing volume and pace of traffic on the route. The ships and streamers can move through this bridge without encountering any obstructions.

The first vertical lift railway sea bridge in India, the Pamban Bridge, which connects the Indian mainland with Rameswaram Island, finished 81% of its construction work, according to the Ministry of Railways. All 333 piles are built, 101 pile caps and substructures are finished, and 76 of 99 girders are launched.

Asia-Pacific Region dominates the market

Significant infrastructure development is now more crucial than ever in the Asia Pacific. Urbanization, population increase, and economic development all contribute to the urgent demand for new and upgraded infrastructure. Long-term infrastructure planning is further complicated by the disparity in infrastructure development between territories. Although the availability and caliber of infrastructure, as well as the capacity and ability to plan and finance infrastructure projects, vary significantly between developed and developing economies, they all include one issue in common: tight budgets. Some governments can finance their infrastructure exclusively.

If the region is to sustain economic growth, combat poverty, and reduce climate risk, the Asian Development Bank (ADB) estimated that roughly USD 1.7 trillion will need to be invested annually in infrastructure across Asia through 2030. It is more than twice the amount of investment that the ADB recommended in 2009. The difference between projected infrastructure requirements and delivered infrastructure is widening.

In China, the infrastructure projects in development or execution of over USD 25 million as of May 2022 were worth over USD 5 trillion. The United States and India were the following countries on the list, with around USD 2 trillion worth of infrastructure projects. In contrast, the country with the highest number of big infrastructure projects was India.

By 2026, renewable electricity capacity worldwide is forecasted to rise more than 60% from 2020 levels, equivalent to the current total global power capacity of fossil fuels and nuclear combined. About 40% of the world's population currently lives within 100 km of the coast, adding increased pressure to coastal ecosystems.

Bridge Construction Industry Overview

Robots, virtual reality, and augmented reality technologies are among the cutting-edge technologies being utilized to build bridges faster and with lower operational costs. For instance, to enhance the structural performance of the bridges, the new arch steel bridge that is currently being built in Bangladesh is using cutting-edge technologies in bridge maintenance and management. ACS Group, AECOM, Balfour Beatty, China Communications Construction Company Limited, and many more are some of the major players. To increase their market reach and compete in the markets, the major players adopted key strategies like product development, business expansion, agreements, partnerships, and acquisitions. These strategies are now being used to build bridges at lower operational costs and shorten project lead times.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Economic and Bridge Construction Market Scenario

- 4.2 Insights into Supply Chain/Value Chain Analysis

- 4.3 Impact of Government Regulations and Initiatives on the Industry

- 4.4 Review and Commentary on the Extent of Government Infrastructure Development Schemes

- 4.5 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Drivers

- 5.1.1 Focus on sustainability using recycled materials and minimizing environmental impact.

- 5.1.2 Adoption of corrosion-resistant materials like reinforced polymers and stainless steel.

- 5.2 Restraints

- 5.2.1 The design and engineering of the bridge are critical to its construction.

- 5.3 Opportunities

- 5.3.1 Technological Innovations

- 5.4 Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Consumers/Buyers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Beam Bridge

- 6.1.2 Truss Bridge

- 6.1.3 Arch Bridge

- 6.1.4 Suspension Bridge

- 6.1.5 Cable-stayed Bridge

- 6.1.6 Others

- 6.2 By Material

- 6.2.1 Steel

- 6.2.2 Concrete

- 6.2.3 Composite Materials

- 6.3 By Application

- 6.3.1 Road and Highway

- 6.3.2 Railway

- 6.4 By Region

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.1.3 Rest of North America

- 6.4.2 Latin America

- 6.4.2.1 Mexico

- 6.4.2.2 Brazil

- 6.4.2.3 Rest of Latin America

- 6.4.3 Europe

- 6.4.3.1 United Kingdom

- 6.4.3.2 France

- 6.4.3.3 Rest of Europe

- 6.4.4 Asia- Pacific

- 6.4.4.1 China

- 6.4.4.2 India

- 6.4.4.3 Rest of Asia- Pacific

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 ACS Group

- 7.2.2 AECOM

- 7.2.3 Balfour Beatty

- 7.2.4 China Communications Construction Company Limited

- 7.2.5 China Railway Group Ltd

- 7.2.6 VINCI

- 7.2.7 Bechtel

- 7.2.8 Hochtief

- 7.2.9 Skanska

- 7.2.10 Bouygues Construction*

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 MAJOR INFRASTRUCTURE DEVELOPMENT PROJECTS (PROJECT DESCRIPTION, VALUE, LOCATION, SECTOR, CONTRACTORS)

- 9.1 Existing Infrastructure

- 9.2 Ongoing Projects

- 9.3 Upcoming Projects