|

市場調査レポート

商品コード

1431034

世界のスマートインプラント:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Global Smart Implants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 世界のスマートインプラント:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 112 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

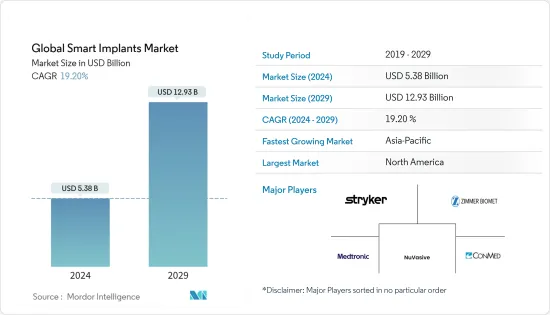

世界のスマートインプラントの市場規模は、2024年に53億8,000万米ドルと推定され、2029年までには129億3,000万米ドルに達すると予測され、予測期間(2024年~2029年)のCAGRは19.20%で成長する見込みです。

COVID-19パンデミックは、スマートインプラント市場、特に歯科サービスに大きな影響を与えました。COVID-19の蔓延を遅らせることを意図した厳格な封鎖と政府規制により、すべてのセグメントで製品需要が減少しました。COVID-19の流行を受け、米国歯科医師会(ADA)15や米国歯科衛生士会(ADHA)16などのさまざまな組織が、すべての選択的歯科処置の延期と重要でない歯科治療の提供を推奨しています。メディケア・メディケイド・サービスセンターは、重要でない検査や処置はすべて、追って通知があるまで延期するよう勧告しています。2022年3月にSpringer Natureに掲載された「歯内治療中の高速ハンドピースと超音波ユニットから発生するエアロゾルがCOVID-19のパンデミックを示唆している」という論文によると、歯科診療において、エアロゾルを発生させる器具と血液や唾液からCOVID-19が感染する危険性があります。

さらに、The Pandemic Practice, Anxiety, Coping, and Support Survey for Vascular Surgeons 2021が提供したデータによれば、回答者の大多数(91.7%)が選択手術のキャンセルを指摘しています。このように、COVID-19の流行は、ほとんどのインプラント手術において市場の成長に悪影響を与えました。しかし、世界的にスマートインプラントデバイスの使用が大幅に増加しているため、市場は牽引力を増すと予想されます。

さらに、さまざまな慢性疾患を抱える高齢者人口の増加、事故やスポーツ傷害の発生率の上昇、スマートインプラント分野における技術進歩などが、調査対象市場の成長を促進する主な要因となっています。現在、スマートインプラントは、部位での感染を減少させる可能性があり、迅速な回復と再入院の減少が将来の成長を支える可能性があります。このような要因は、スマートインプラントの採用を後押しし、それによって調査した市場の成長に貢献する可能性が高いです。

また、同市場の主要企業による新製品の発売や戦略的活動は、調査対象市場の成長にプラスの影響を与えています。例えば、2020年8月、Zimmer Biomet Holdingsは、米国食品医薬品局(FDA)がPersona IQの脛骨延長部の販売許可を与えたと発表しました。さらに、2021年8月には、Johnson & Johnsonが、患者ケアのアプローチで設計されたINHANCE Shoulder Systemを発表しています。このように、製品の発売により、市場は予測期間中に大きく成長することが期待されます。

したがって、前述の要因によって、調査した市場は分析期間中に成長を示すと予想されます。しかし、インプラントの高コストと厳しい規制枠組みが市場成長を阻害する可能性が高いです。

スマートインプラント市場動向

整形外科用スマートインプラント分野は予測期間中に高成長が見込まれる

整形外科用スマートインプラントは、膝関節置換術や人工股関節置換術、脊椎固定術、骨折などの治療や診断に利用できます。スマート股関節インプラントは、人工股関節置換術の最も一般的な合併症の1つである圧力や温度の測定、人工関節のゆるみを検出することができます。さらに、国立医学図書館に2022年3月に掲載された「脊椎インプラント用'SMART'移植可能デバイス」と題された論文によると、これらのインテリジェント・インプラントは、インプラントに損傷を与える危険性のある一般的な活動の把握、癒合の進行状況のモニタリング、ペディクル・スクリューのゆるみや体間ケージの沈下などの潜在的合併症の早期発見のための使用が示唆されています。したがって、整形外科用スマートインプラントが提供する利点により、これらの製品の採用は対象人口の間で増加し、最終的に市場成長を促進すると思われます。

さらに、市場の大手企業による継続的なコラボレーションが、このセグメントの成長にプラスの影響を与えています。例えば、2020年11月、Medtronic plcは、人工知能(AI)、予測モデリング、患者専用インプラントによる脊椎外科手術の変革のパイオニアであるフランスのMedicrea Internationalに対する友好的公開買付けを完了したと発表しました。したがって、整形外科用スマートインプラント分野は、上記の要因により、予測期間中に大きな成長を示すことが期待されています。

北米がスマートインプラント市場を独占する見込み

北米は、技術的に先進的な製品が容易に入手可能であること、消費者の意識が高いこと、ヘルスケアインフラが改善されていること、製薬会社やバイオテクノロジー会社がこの地域で拡大していることなどの要因により、市場を独占すると予想されています。例えば、Stanford Children's Health organizationのSports Injury statisticsによると、2021年には米国では3,000万人の子供と10代の若者が何らかの形で組織化されたスポーツに参加し、毎年350万人以上が怪我をしています。米国では、迅速かつ効果的な結果を得るためにスマートインプラントの使用が増加していることが、北米の調査市場の成長に寄与する主な要因の1つです。

主要製品の発売、市場プレイヤーの高集中度、米国におけるメーカーのプレゼンスは、同国におけるスマートインプラント市場の成長を促進する要因の一部です。例えば、2021年6月、MedtronicはVantaデバイスのFDA(米国食品医薬品局)承認を取得しました。Vantaデバイスは充電不要の埋め込み型神経刺激装置(INS)で、デバイス寿命は最長11年です。例えば、2020年5月、NuVasive, Inc.は、モジュラスXLIFデュアルサイドプレートの商業的発売により、アドバンスド・マテリアル・サイエンス・インプラント・ポートフォリオの拡大を発表しました。同地域におけるこうした継続的な製品投入は、同国市場の成長を促進すると予想されます。

従って、上記の要因から、北米地域における市場の成長が期待されます。

スマートインプラント産業の概要

スマートインプラント市場は、世界的および地域的に事業を展開する少数の企業が存在するため、その性質上、統合されています。主要な市場プレーヤーは、最大市場シェアを獲得するために技術的進歩に注力しています。主要企業は、Stryker、Zimmer Biomet、DePuy Synthes、Medtronic、IQ Implants USA、Canary Medical Inc.Smart Implant Solutions、REJOINT SRLなどが挙げられます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 様々な慢性疾患を抱える高齢者人口の増加

- 事故やスポーツ傷害の増加

- スマートインプラント分野における技術進歩

- 市場抑制要因

- 厳しい規制枠組み

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 製品タイプ別

- 整形外科用スマートインプラント

- 膝関節形成術

- 人工股関節置換術

- 脊椎固定術

- 骨折固定

- その他

- 心血管スマートインプラント

- ペーシングデバイス

- ステント

- 心臓構造インプラント

- 眼科用スマートインプラント

- 眼内レンズ

- 緑内障インプラント

- 歯科用スマートインプラント

- 美容スマートインプラント

- その他

- 整形外科用スマートインプラント

- エンドユーザー別

- 病院

- 外来手術センター

- 整形外科クリニック

- 眼科クリニック

- 歯科ラボ

- その他

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Stryker

- Zimmer Biomet

- Johnson & Johnson(DePuy Synthes)

- IQ Implants USA

- Canary Medical Inc.

- Medtronic

- NuVasive Inc.

- Smart Implant Solutions

- Rejoint srl

- CONMED

第7章 市場機会と今後の動向

The Global Smart Implants Market size is estimated at USD 5.38 billion in 2024, and is expected to reach USD 12.93 billion by 2029, growing at a CAGR of 19.20% during the forecast period (2024-2029).

COVID-19 pandemic had a substantial impact on the smart implants market, specifically for dental services. The strict lockdowns and government regulations intended to slow down the spread of COVID-19 resulted in a decrease in demand for products across all segments. In wake of COVID-19 outbreak, various organizations, such as, American Dental Association (ADA)15 and the American Dental Hygienists' Association (ADHA)16 have recommended postponing all elective dental procedures and provision of noncritical dental care. The Centers for Medicare and Medicaid Services recommend that all nonessential examinations and procedures must be postponed until further notice. As per the articles published in March 2022 titled 'Aerosols generated by high-speed handpiece and ultrasonic unit during endodontic coronal access alluding to the COVID-19 pandemic' in Springer Nature, there is a risk of transmission of Covid-19, in dental practice from blood or saliva, combined with instruments that generate aerosols.

Furthermore, as per the data provided by The Pandemic Practice, Anxiety, Coping, and Support Survey for Vascular Surgeons 2021, the majority of respondents (91.7%) noted elective surgery cancellation. Thus, the COVID-19 outbreak affected the market's growth adversely for most of the implant surgeries; however, the market is expected to gain traction due to the significant increase in the use of smart implant devices globally.

Further, an increase in the geriatric population with various chronic disorders, rising incidence of accidents or sports injuries, and technological advancements in the field of smart implants are among the major factors driving the growth of the studied market. Currently, smart implants have the potential to reduce the infection at the site, speedy recovery and reduced readmission may support the growth in the future. Such factors are likely to boost the adoption of smart implants, thereby contributing to the studied market growth.

In addition, new product launches and strategic activities by major players in the market are positively affecting the growth of the studied market. For instance, in August 2020 Zimmer Biomet Holdings announced U.S. Food and Drug Administration (FDA) has granted authorization to market the tibial extension for Persona IQ. Additionally, in August 2021, The Johnson & Johnson introduces the INHANCE Shoulder System designed with patient care approach. Thus, owing to the product launches the studied market is expected to have significant growth over the forecast period.

Therefore, owing to the aforementioned factors the studied market is anticipated to witness growth over the analysis period. However, the high cost of implants & Stringent Regulatory Framework is likely to impede market growth.

Smart Implants Market Trends

Orthopedic Smart Implants Segment is Expected to Witness high Growth Over the Forecast Period

Orthopedic smart implants can be used to obtain therapeutics and diagnostics benefits for knee & Hip replacements, spine fusion surgeries, and fracture among others. Smart hip Implants can detect pressure and temperature measurements, and loosening of prostheses, which is one of the most common complications of total hip arthroplasty. Moreover, the article published in March 2022 titled 'SMART' implantable devices for spinal implants' in the National Library of Medicine said these intelligent implants have been suggested for use for understanding common activities that may risk damage to implants, monitoring the progression of fusion, and early detection for potential complications such as pedicle screw loosening and interbody cage subsidence. Hence, owing to the advantages offered by orthopedic smart implants, the adoption of these products is likely to increase among the target population, ultimately driving the market growth.

Furthermore, a continuous collaboration by major players in the market is positively affecting the growth of the segment. For instance , in November 2020, Medtronic plc announced that it has completed its friendly tender offer for France-based Medicrea International, a pioneer in the transformation of spinal surgery through artificial intelligence (AI), predictive modeling, and patient specific implants. Therefore, the orthopedic smart implants segment is expected to witness significant growth over the forecast period due to the above mentioned factors.

North America is Expected to Dominate the Smart Implants Market

North America is expected to dominate the market owing to factors such as the easy availability of technologically advanced products, high awareness among consumers, improved healthcare infrastructure, and expansion of pharmaceutical and biotechnology companies in the region. For Instance, according to the data provided in Stanford Children's Health organization , Sports Injury statistics, In 2021, 30 million children and teens participate in some form of organized sports, and more than 3.5 million have injuries each year in United States. An increase in the usage of smart implants for rapid and effective results in the United States is among the key factors which contribute to the growth of the studied market in North America.

Key product launches, high concentration of market players, or manufacturer's presence in the United States are some of the factors driving the growth of the smart implants market in the country. For instance, in June 2021, Medtronic receive Food and Drug Administration (FDA) approval for its Vanta device-a recharge-free implantable neurostimulator (INS) with a device life that lasts up to 11 years. For instance, in May 2020, NuVasive, Inc. announced the expansion of its Advanced Materials Science implant portfolio with the commercial launch of the Modulus XLIF Dual Sided Plate. These continuous product launches in the region are anticipated to drive the growth of the market in the country.

Therefore, owing to the aforesaid factors the growth of the studied market is anticipated in the North America Region.

Smart Implants Industry Overview

The smart implants devices market is consolidated in nature due to the presence of few companies operating globally as well as regionally. The major market players are focusing on technological advancements to acquire maximum market share. Some of the Major Players includes Stryker, Zimmer Biomet, DePuy Synthes, Medtronic, IQ Implants USA, Canary Medical Inc., NuVasive Inc. Smart Implant Solutions, REJOINT SRL, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Defination

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Driver

- 4.2.1 Increase in the Geriatric Population with Various Chronic Disorder

- 4.2.2 Rising Incidence of Accidents and Sport Injuries

- 4.2.3 Technological Advancements in the Field of Smart Implants

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Framework

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Product Type

- 5.1.1 Orthopedics Smart Implants

- 5.1.1.1 Knee Arthroplasty

- 5.1.1.2 Hip Arthroplasty

- 5.1.1.3 Spine Fusion

- 5.1.1.4 Fracture Fixation

- 5.1.1.5 Others

- 5.1.2 Cardiovascular Smart Implants

- 5.1.2.1 Pacing devices

- 5.1.2.2 Stents

- 5.1.2.3 Structural Cardiac Implants

- 5.1.3 Opthalmic Smart Implants

- 5.1.3.1 Intraocular lens

- 5.1.3.2 Glaucoma Implants

- 5.1.4 Dental Smart Implants

- 5.1.5 Cosmetic smart Implants

- 5.1.6 Others

- 5.1.1 Orthopedics Smart Implants

- 5.2 By End User

- 5.2.1 Hospitals

- 5.2.2 Ambulatory Surgical Centers

- 5.2.3 Orthopedics Clinics

- 5.2.4 Opthalmic Clinics

- 5.2.5 Dental Labs

- 5.2.6 Others

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle-East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle-East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Stryker

- 6.1.2 Zimmer Biomet

- 6.1.3 Johnson & Johnson (DePuy Synthes)

- 6.1.4 IQ Implants USA

- 6.1.5 Canary Medical Inc.

- 6.1.6 Medtronic

- 6.1.7 NuVasive Inc.

- 6.1.8 Smart Implant Solutions

- 6.1.9 Rejoint srl

- 6.1.10 CONMED