|

市場調査レポート

商品コード

1549999

アフリカの構造化ケーブリング:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Africa Structured Cabling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アフリカの構造化ケーブリング:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

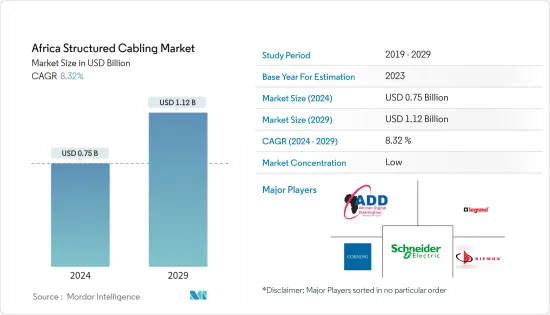

アフリカの構造化ケーブリング市場規模は2024年に7億5,000万米ドルと推定され、2029年には11億2,000万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは8.32%で成長する見込みです。

主なハイライト

- アフリカの構造化ケーブリング市場は、通信インフラへの投資拡大とデータセンター融合への動向に後押しされ、成長へと移行しています。また、高速接続機器やシステムに対する需要の高まりが市場拡大を後押ししています。

- 主要な海底ケーブルプロジェクトである2アフリカとエクイアーノは完成間近です。これらの開始により、アフリカのインターネット容量は倍増し、5G技術の迅速な導入への道が開かれると期待されています。政府と通信大手は、5Gインフラに多額の投資を行い、高速通信、遅延の削減、都市と農村の両方にまたがるカバレッジの強化などのメリットを提供しています。2Africaのような海底ケーブルシステムは、アフリカの接続性に革命をもたらし、アジア太平洋地域と欧州間の通信を多様化するような構想が計画されています。

- ネットワークのカバレッジが重要な焦点となるにつれ、国境を越えた協力体制がますます不可欠となっています。各国政府は通信事業者、ハイテク企業、開発機関と手を組んでいます。このコラボレーションは、インフラ・プロジェクトを推進するだけでなく、知識交換を促進し、最終的には大陸間の相互接続を促進します。国際金融公社(International Finance Corporation)とグーグルのデータによると、アフリカのインターネット経済は、2025年までにアフリカ大陸のGDPを1,800億米ドル成長させるといいます。このことは、市場の成長を支える強力なデジタル・インフラにとって重要な機会となります。

- アフリカの多くの地域では、データセンターや高速データネットワークの展開を促進するための、信頼できる電力供給やインターネット接続などのネットワークインフラが不足しています。また、データ構造ケーブル技術の熟練した専門家が不足していることも、市場の成長を妨げています。

- COVID-19の大流行により、各分野でデジタル変革が進み、リモートワーク、オンライン教育、遠隔医療、eコマースにおけるネットワーク接続の増加をサポートする堅牢で信頼性の高いデータ・ケーブル・インフラに対する需要が急増しています。組織は、ハイブリッドモデルや将来の不確実性に対応するため、柔軟でスケーラブルなケーブルソリューションのITインフラに投資しています。

アフリカの構造化ケーブリング市場動向

ファイバーセグメントが大きな成長を遂げる

- デジタル変革、eコマース、クラウドサービス、オンラインメディア消費による高速インターネットアクセス需要の高まりが、アフリカ全域での光ファイバーネットワークの拡大に拍車をかけています。5G技術の普及とブロードバンドインフラの強化は、構造化ケーブル市場に有利な道を開くことになります。

- 過去5年間、アフリカ諸国はモバイルインターネット接続の著しい急増を目の当たりにしてきました。この増加は主に、事業者によるモバイル・ブロードバンド・ネットワーク(3G、4G、さらには5Gに及ぶ)への投資の増加と、スマートフォンの利用増加によるものです。モバイル・ブロードバンドが人々をつなぐ上で極めて重要である一方、ラストマイルの固定ブロードバンド接続のギャップに対処することは、家庭や企業に強化された接続サービスを提供する上で極めて重要です。GSMAのデータによると、同地域における5Gの普及率は1%で、2026年には8%に達すると予想されています。

- スマートフォンやモバイル機器の普及と、ビデオストリーミング、ソーシャルメディア、モバイルゲームなどのアプリケーションのためのモバイルデータ消費の増加が相まって、モバイルネットワークをサポートするためのファイバーバックホールインフラへの投資が増加しています。アフリカでは固定無線アクセス(FWA)サービスは目新しいものではなく、すでに多くの事業者が4G FWAを提供しているが、その状況は進化しています。Telkom South Africaは、同社ネットワークのデータトラフィックのうち、従来のモバイルデータサービスに割り当てられているのが39%であるのに対し、FWAサービスに割り当てられているのが57%であることを明らかにしています。

- この地域における5Gのカバレッジはまだ主要都市に集中しているが、いくつかの国では5Gの展開が著しく加速しています。しかし、エチオピア、ナイジェリア、ケニア、ガーナなどのアフリカの新興市場は、都市化とデジタルサービスの拡大により、光ファイバーケーブルの展開に大きな成長の可能性をもたらしています。

- 銀行、教育、ヘルスケア、政府など、さまざまな分野の企業がデジタルトランスフォーメーションへの取り組みを進めており、データ転送、クラウド接続、IoT展開のための信頼性の高い大容量光ファイバーネットワークへの需要が高まっています。

南アフリカが最大市場シェア

- 光ファイバーネットワークや5Gの導入を含む通信インフラへの投資が拡大していることから、南アフリカはアフリカの構造化ケーブリング市場で最大の市場シェアを占めています。GSMAのデータによると、2023年9月現在、アフリカの16市場で27の事業者が商用5Gサービスを展開しています。また、さらに10カ国の通信事業者が近いうちに5Gを導入すると表明しています。特に南アフリカでは、2023年9月までに人口の41%が5Gにアクセスできるようになった。

- 南アフリカの企業や事業者は、データ量の増加、クラウドサービスの導入、IoT(モノのインターネット)などの新技術に対応するためにITインフラを拡張しており、効率的で整ったケーブル配線ソリューションの必要性を高めています。

- 5Gデジタル接続の改善やICT(情報通信技術)の導入促進を目指す政府の取り組みが、特に教育、ヘルスケア、政府機関などの分野における構造化ケーブリング市場の成長に寄与しています。GSMAのデータによると、5Gモバイル接続は2030年までに5,820万に達すると予想されています。

- 多くの市場関係者が南アフリカでの5Gインフラ構築に投資しています。例えば、GSMAの報告書によると、2025年までにモバイル通信ネットワーク(MTN)は1,000万世帯の接続を目指しており、その75%が確立される南アフリカとナイジェリアに焦点を当てています。彼らのアプローチでは、上位30%の世帯にモバイルブロードバンドモデムを配備し、上位10%に5G固定無線アクセス(FWA)を導入し、上位1%にファイバー接続を展開します。

- データ漏洩やサイバーセキュリティの脅威に対する懸念の高まりは、南アフリカのPOPIA(個人情報保護法)に準拠したデータセキュリティと規制遵守の重視を促しています。その結果、安全でコンプライアンスに準拠したケーブルインフラへの投資が急増しています。IBMセキュリティの「データ漏えいのコスト」レポートによると、2023年、南アフリカの組織は過去最高の平均データ漏えいコスト260万米ドル(4,945万ZAR)に直面し、過去3年間で8%の増加を記録しました。

アフリカの構造化ケーブリング産業の概要

アフリカの構造化ケーブリング市場は断片化されており、現在様々な大手企業が参入しています。主なプレーヤーは、Africa Digital Distributors Limited、Corning Incorporated、Legrand Group、Schneider Electric SE、The Siemon Companyなどです。構造化ケーブリング市場の主要企業は、常に進歩をもたらす努力をしています。

たとえば2024年 6月、ネットワーク・インフラストラクチャー・ソリューションのプレーヤーであるシーモンはUltraMAXTM銅線接続システムの拡張を発表しました。この新製品はネットワークの性能と柔軟性を高めることを目的としたもので、UltraMAX 48ポート・パッチ・パネル(フラットとアングルの1U構成)、UltraMAXターボ・ツール、終端処理済みの銅線トランク・ケーブルが特徴です。シーモンの最新製品は、アフリカにおける接続規格を向上させ、設置手順を簡素化します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン

- ミクロ経済シナリオの分析(景気後退、ロシア・ウクライナ危機など)

第5章 市場力学

- 市場促進要因

- 各業界における技術進歩の加速

- データセンターの拡大

- 市場抑制要因

- 技術スキルの不足と複雑な設置プロセス

- ワイヤレスソリューションへの需要の高まり

- 技術スナップショット

第6章 市場セグメンテーション

- タイプ別

- 銅

- 銅ケーブル

- 銅コネクティビティ

- ファイバー

- ファイバーケーブル(シングルモード&マルチモード)

- ファイバーコネクティビティ

- 銅

- 用途別

- LAN

- データセンター

- 国別

- ナイジェリア

- エジプト

- 南アフリカ

- アルジェリア

- モロッコ

- エチオピア

- ケニア

- アンゴラ

- タンザニア

- ガーナ

第7章 競合情勢

- 企業プロファイル

- Africa Digital Distributors Limited

- Corning Incorporated

- Legrand Group

- Schneider Electric SE

- The Siemon Company

- Panduit Corp

- OFS Fitel LLC.

- Datwyler IT Infra GmbH

- Liranz Limited

- Techguru Garage

第8章 市場機会と今後の動向

The Africa Structured Cabling Market size is estimated at USD 0.75 billion in 2024, and is expected to reach USD 1.12 billion by 2029, growing at a CAGR of 8.32% during the forecast period (2024-2029).

Key Highlights

- The African structured cabling market is transitioning toward growth, propelled by increased investments in communication infrastructure and a trend toward data center convergence. Moreover, a surging demand for high-speed connectivity devices and systems bolsters market expansion.

- Major subsea cable projects, 2Africa and Equiano, are nearing completion. Their launch is anticipated to double Africa's internet capacity, paving the way for a swift adoption of 5G technology. Governments and telecom giants are channeling significant investments into 5G infrastructure, providing benefits like high speeds, reduced latency, and enhanced coverage, spanning both urban and rural landscapes. Submarine cable systems, like 2Africa, are planned to revolutionize African connectivity and initiatives like diversifying communications between APAC and Europe.

- As network coverage becomes a critical focus, cross-border collaborations are increasingly vital. Governments are teaming up with telecom operators, tech firms, and development agencies. This collaboration not only drives infrastructure projects but also facilitates knowledge exchange, ultimately leading to a more interconnected continent. As per the data by International Finance Corporation and Google, Africa's internet economy will grow the continent's GDP by USD 180 billion by 2025. This provides a critical opportunity for a strong digital infrastructure to support the growth of the market.

- Many regions of Africa lack network infrastructure, including reliable power supply and internet connectivity, to facilitate the deployment of data centers and high-speed data networks. The shortage of skilled professionals in data structure cabling technology also hampers the market's growth.

- The COVID-19 pandemic has led to digital transformation across sectors, leading to the surge in demand for robust and reliable data-cabling infrastructure to support the increase in network connectivity in remote working, online education, telemedicine, and e-commerce. Organizations have invested in IT infrastructure for flexible and scalable cabling solutions to accommodate hybrid models and future uncertainty.

Africa Structured Cabling Market Trends

Fiber Segment to Witness Major Growth

- The fiber segment is expected to witness growth in Africa during the forecast period, primarily due to the growing demand for high-speed internet access, driven by digital transformation, e-commerce, cloud services, and online media consumption, which has fueled the expansion of fiber optic networks across Africa. The widespread adoption of 5G technology and enhancements in broadband infrastructure are set to open lucrative avenues for the structured cabling market.

- Over the past five years, African nations have witnessed a notable surge in mobile internet connectivity. This increase is primarily attributed to increased investments by operators in mobile broadband networks (spanning 3G, 4G, and even 5G) and rising smartphone usage. While mobile broadband has been pivotal in linking people, addressing the gap in last-mile fixed broadband connectivity is crucial to delivering enhanced connectivity services to households and enterprises. As per GSMA data, 5G adoption is 1% in the region, which is expected to reach 8% by 2026.

- The proliferation of smartphones and mobile devices, coupled with rising mobile data consumption for applications like video streaming, social media, and mobile gaming, has led to increased investment in fiber backhaul infrastructure to support mobile networks. While fixed wireless access (FWA) services are not new in Africa, with many operators already offering 4G FWA, the landscape is evolving. Telkom South Africa disclosed that a significant 57% of its network's data traffic caters to FWA services, compared to 39% allocated to traditional mobile data services.

- While 5G coverage in the region remains concentrated in major cities, several countries are notably accelerating their 5G deployment. However, emerging markets in Africa, such as Ethiopia, Nigeria, Kenya, and Ghana, present significant growth potential for fiber optic cable deployments driven by urbanization and expanding digital services.

- Enterprises across various sectors, including banking, education, healthcare, and government, are undergoing digital transformation initiatives, driving the demand for reliable and high-capacity fiber optic networks for data transfer, cloud connectivity, and IoT deployments.

South Africa Holds the Largest Market Share

- South Africa holds the largest market share in the African structured cabling market due to the growing investment in telecommunications infrastructure, which includes fiber optic networks and 5G deployments. According to GSMA data, as of September 2023, 27 operators in 16 African markets had rolled out commercial 5G services. Additionally, operators in 10 more countries have pledged to introduce 5G in the near term. Notably, in South Africa, 41% of the population had access to 5G by September 2023.

- Businesses and enterprises in South Africa are expanding their IT infrastructure to accommodate growing data volumes, cloud services adoption, and emerging technologies like IoT (Internet of Things), driving the need for efficient and well-organized cabling solutions.

- Government initiatives aimed at improving 5G digital connectivity and promoting the adoption of ICT (information and communication technology) have contributed to the growth of the structured cabling market, especially in sectors such as education, healthcare, and government institutions. As per GSMA data, 5G mobile connection is expected to reach 58.2 million by 2030.

- Many market players are investing in building the 5G infrastructure in South Africa. For instance, as per a GSMA report, by 2025, the Mobile Telecommunication Network (MTN) aims to link 10 million households, focusing on South Africa and Nigeria, where 75% of these connections will be established. Their approach involves deploying mobile broadband modems to the top 30% of households, introducing 5G fixed wireless access (FWA) to the top 10%, and rolling out fiber connections to the top 1%.

- Growing concerns over data breaches and cybersecurity threats are driving the emphasis on data security and regulatory compliance in compliance with South Africa's POPIA (Protection of Personal Information Act). Consequently, there is a surge in investments directed toward secure and compliant cabling infrastructure. In 2023, South African organizations faced a record-high average data breach cost of USD 2.6 million (ZAR 49.45 million), marking an 8% increase over the preceding three years, as per IBM Security's "Cost of a Data Breach" report.

Africa Structured Cabling Industry Overview

Africa's structured cabling market is fragmented, as it currently consists of various significant players. Some key players are Africa Digital Distributors Limited, Corning Incorporated, Legrand Group, Schneider Electric SE, and The Siemon Company. Several key players in the structured cabling market are constantly making efforts to bring advancements.

For instance, in June 2024, Siemon, a player in network infrastructure solutions, unveiled an expansion of its UltraMAXTM copper connectivity system. The new products, aimed at boosting network performance and flexibility, feature UltraMAX 48-port patch panels in flat and angled 1U configurations, the UltraMAX Turbo Tool, and pre-terminated copper trunk cables. Siemon's latest offerings are set to elevate connectivity standards and simplify installation procedures in Africa.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain

- 4.3 Analysis of Micro-economic Scenarios (Recession, Russia-Ukraine Crisis, etc.)

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Acceleration of Technological Advancements Across Industries

- 5.1.2 The Growing Expansion of Data Centers

- 5.2 Market Restraints

- 5.2.1 Lack of Technical Skills and Complex Installation Process

- 5.2.2 Rising Demand for Wireless Solutions

- 5.3 Technology Snapshot

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Copper

- 6.1.1.1 Copper Cable

- 6.1.1.2 Copper Connectivity

- 6.1.2 Fiber

- 6.1.2.1 Fiber Cable (Single-mode & Multi-mode)

- 6.1.2.2 Fiber Connectivity

- 6.1.1 Copper

- 6.2 By Application

- 6.2.1 LAN

- 6.2.2 Data Center

- 6.3 By Country

- 6.3.1 Nigeria

- 6.3.2 Egypt

- 6.3.3 South Africa

- 6.3.4 Algeria

- 6.3.5 Morocco

- 6.3.6 Ethiopia

- 6.3.7 Kenya

- 6.3.8 Angola

- 6.3.9 Tanzania

- 6.3.10 Ghana

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Africa Digital Distributors Limited

- 7.1.2 Corning Incorporated

- 7.1.3 Legrand Group

- 7.1.4 Schneider Electric SE

- 7.1.5 The Siemon Company

- 7.1.6 Panduit Corp

- 7.1.7 OFS Fitel LLC.

- 7.1.8 Datwyler IT Infra GmbH

- 7.1.9 Liranz Limited

- 7.1.10 Techguru Garage