|

|

市場調査レポート

商品コード

1913428

構造化配線市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Structured Cabling Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 構造化配線市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月16日

発行: Global Market Insights Inc.

ページ情報: 英文 185 Pages

納期: 2~3営業日

|

概要

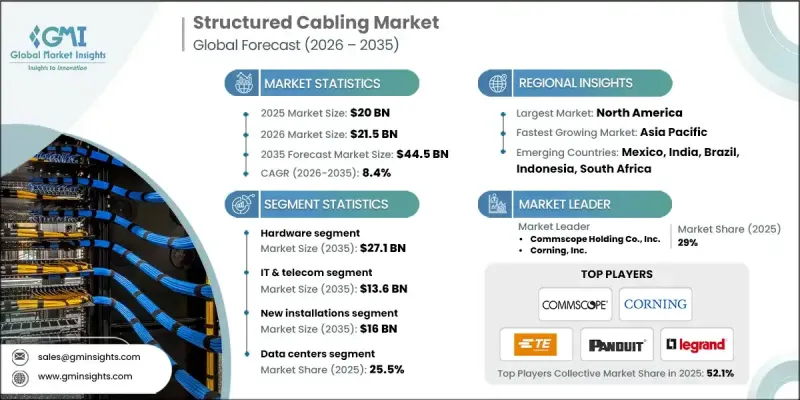

世界の構造化配線市場は、2025年に200億米ドルと評価され、2035年までにCAGR8.4%で成長し、445億米ドルに達すると予測されています。

本市場の成長要因としては、データセンターの増加、高速ネットワークの導入、IoTの統合、5Gおよびエッジコンピューティングの拡大が挙げられます。データトラフィックの増加とクラウドサービスの展開により、新興市場における企業環境や産業環境全体で信頼性の高い接続性を提供する、拡張性と高性能を備えたネットワークインフラへの需要が高まっています。企業では音声・映像・データ伝送を統合したユニファイドネットワークシステムの導入が進んでおり、これが先進的な構造化配線システムの採用を促進しています。ハイブリッドワークモデルの台頭により、分散型チーム向けの高帯域幅、安定した接続性、シームレスなアクセスを確保するため、組織は堅牢なケーブルシステムによる屋内ネットワークインフラのアップグレードを推進しています。さらに、Power over Ethernet(PoE)デバイスの導入拡大に伴い、スマートデバイス、セキュリティシステム、IoTアプリケーション向けの高電力供給をサポート可能な先進的な銅ケーブルの需要が増加しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 200億米ドル |

| 予測金額 | 445億米ドル |

| CAGR | 8.4% |

ハードウェア分野は、高速スイッチ、コネクタ、光ファイバーシステム、その他の先進的なケーブル部品への需要に牽引され、2035年までに271億米ドルに達すると予測されています。これらのソリューションは、増加するデータトラフィック、低遅延要件、および企業・産業ネットワークの近代化に対応するために不可欠です。

IT・通信セクターは、クラウド導入、5G展開、高帯域幅接続需要に後押しされ、2035年までに136億米ドルに達すると予測されています。企業はデジタルトランスフォーメーション構想を支える低遅延・高密度ネットワークをますます求めています。メーカーは次世代高性能ネットワークをサポートしつつ、将来を見据えた拡張性、容易な設置、簡素化された保守を提供するソリューションの提供に注力しています。

北米構造化配線市場は2025年に38.2%のシェアを占め、2026年から2035年にかけてCAGR 7.3%で成長すると予測されています。この地域の成長は、自動化、産業用IoT(IIoT)、スマート工場の導入、および5Gの広範な普及によって牽引されています。これらの技術は、産業および製造分野全体で、瞬時のデータ伝送、予知保全、および運用効率の向上を可能にします。同地域における先進的な無線・有線ネットワークインフラへの注力は、構造化配線への投資を継続的に支えております。

よくあるご質問

目次

第1章 調査手法

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- データセンターおよびクラウドインフラの拡大

- 高速ネットワークおよび帯域幅を大量に消費するアプリケーションの導入拡大

- IoT、接続デバイス、スマートビル導入の拡大

- 5Gインフラおよびエッジコンピューティングエコシステムの拡大

- 業界の潜在的リスク&課題

- 初期導入・展開コストの高さ

- レガシー配線インフラのアップグレードにおける複雑性

- 市場機会

- ハイパースケールおよびコロケーションデータセンターの拡大

- スマートシティおよびインテリジェントビルシステムの導入拡大

- 高速ネットワークにおける光ファイバーケーブル需要の増加

- 構造化配線とIoTおよびインダストリー4.0インフラの統合

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 新興ビジネスモデル

- コンプライアンス要件

- 特許および知的財産分析

- 地政学的・貿易動向

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 主要企業の競合ベンチマーキング

- 財務実績比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオ比較

- 製品ラインの広さ

- 技術

- イノベーション

- 地域別展開比較

- 世界展開分析

- サービスネットワークのカバー率

- 地域別市場浸透率

- 競合ポジショニングマトリックス

- リーダー企業

- 課題者

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績比較

- 主な発展, 2021-2024

- 合併・買収

- 提携および共同事業

- 技術的進歩

- 拡大と投資戦略

- デジタルトランスフォーメーションの取り組み

- 新興/スタートアップ競合の動向

第5章 市場推計・予測:構成部品別、2022-2035

- ハードウェア

- ケーブル

- 銅ケーブル

- カテゴリ5E(Cat 5E)

- カテゴリ6(Cat 6)

- カテゴリー6A(Cat 6A)

- カテゴリー7(Cat 7)

- カテゴリー8(Cat 8)

- 光ファイバーケーブル

- シングルモード

- マルチモード

- 通信アウトレットシステム

- パッチケーブル及びケーブルアセンブリ

- パッチパネル及びクロスコネクト

- ラック及びケーブル管理

- 銅ケーブル

- ケーブル

- ソフトウェア

- サービス

- コンサルティング

- 設置・導入

- 保守・サポート

第6章 市場推計・予測:設置タイプ別、2022-2035

- 新規設置

- アップグレード及び保守

第7章 市場推計・予測:用途別、2022-2035

- データセンター

- ローカルエリアネットワーク(LAN)

- 通信

- 広域ネットワーク(WAN)

- その他

第8章 市場推計・予測:最終用途産業別、2022-2035

- BFSI

- 商業用

- エネルギー

- 政府

- ヘルスケア

- 産業

- IT・通信

- 交通機関

第9章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- 世界の主要企業

- Commscope Holding Co., Inc.

- Corning, Inc.

- TE Connectivity

- Cisco Systems, Inc.

- 地域別主要企業

- 北米

- Panduit Corporation

- Anixter International

- General Cable Technologies Corporation

- 欧州

- Legrand

- Nexans S.A.

- Rittal GmbH &Co. KG

- アジア太平洋

- Fujitsu

- CA Technologies

- Reichle &De-Massari AG

- 北米

- ニッチプレイヤー/ディスラプター

- ABB Ltd.

- The Siemon Company