|

市場調査レポート

商品コード

1851261

電気自動車用バッテリーシステム:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Battery Systems For Electric Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 電気自動車用バッテリーシステム:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月02日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

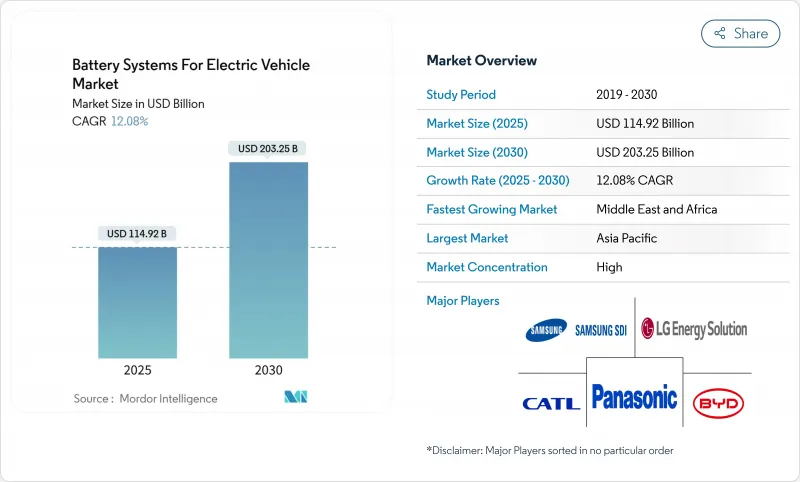

電気自動車用バッテリーシステム市場は、2025年には1,149億2,000万米ドルに達し、2030年にはCAGR 12.08%を反映して2,032億5,000万米ドルに拡大すると予測されます。

北米と欧州におけるインセンティブ主導の採用目標、リチウムイオン化学の急速なコスト低下、アジア、北米、欧州にわたる垂直統合型のギガファクトリー展開が、この拡大を支えています。また、リチウムイオンとナトリウムイオンやキャパシタを組み合わせたマルチケミストリー・パックが設計の柔軟性を広げる一方で、より高いエネルギー密度と安全性を約束するソリッドステートのブレークスルーも、この市場に利益をもたらしています。米国や欧州連合(EU)の規制枠組が現地含有量規制を強化する中でも、中国メーカーがリン酸鉄リチウムのコスト優位性を利用してシェアを獲得しているため、競合の激しさは依然として高いです。サプライチェーンの分岐、熱暴走によるリコール、重要鉱物の変動は見通しを弱めるが、持続的成長軌道を狂わせることはないです。

世界の電気自動車用バッテリーシステム市場動向と洞察

政府のインセンティブとゼロエミッション義務化

規制の枠組みは、電気ドライブトレインの最低販売台数を固定することで需要を加速させる。米国は、対象となる自動車1台につき最高7,500米ドルの税額控除を提供し、国産車比率のしきい値を毎年引き上げています。カリフォルニア州のアドバンスト・クリーン・カーⅡ規則は、2025年にゼロ・エミッション車販売台数の22%、2035年までに100%を達成することを自動車メーカーに義務付けています。英国は2030年までに80%の電気自動車販売を義務付け、カナダは2035年までに100%を目標としています。コンプライアンス違反は多額の違約金を課すことになるため、ほとんどの自動車メーカーは複数年のバッテリー引き取り契約を結び、セルメーカーに販売量の確保とキャッシュフローの可視性を提供しています。

リチウムイオンコストの低下とエネルギー密度の向上

学習曲線効果と材料代替により、コストの下降が続いています。トップクラスのセルメーカー数社は、2024年には1kWh当たり118米ドルであったパックコストを、2026年には60米ドル以下に押し下げることを目指しています。エネルギー密度は、比容量を25~50%高めるシリコンリッチ負極によって上昇し、リン酸鉄リチウムは洗練された正極コーティングによって体積密度を向上させる。コストの急速な低下により、対応可能な市場はエントリーレベルの乗用車、二輪車、コストに敏感な商用車へと拡大します。

重要鉱物の供給と価格変動

上流精製への集中は、メーカーを地政学的リスクにさらします。中国は世界のリン酸鉄リチウム正極材の80%を精製し、コバルトの大部分はある国が生産しています。リチウムの需要は2030年までに5倍に伸びると予想されているが、鉱山の承認が遅れているため、価格変動がセルメーカーの利幅を圧迫しています。多角化努力の実現には数年を要するため、有力サプライヤーへの依存度が高まり、価格の見通しが悪くなります。

セグメント分析

2024年の電気自動車用バッテリーシステム市場シェアはリチウムイオン技術が94.12%を占め、2030年まで数量リーダーであり続ける。パックレベルの急速な技術革新により、重量密度は300Wh/kgを目指す一方、コストは60米ドル/kWhを下回っています。このセグメントの製造エコシステムは、材料、セル形式、リサイクルの流れにまたがり、規模の優位性を強化し、新車OEMの参入障壁を低くしています。

固体電池のCAGRは39.92%と最も高く、デンドライトの成長を抑制し、1,000サイクル後の容量低下を5%に抑えるセラミック製セパレーターに後押しされています。その優れたエネルギー貯蔵能力により、コンパクトなパック設計が可能になり、高性能モデルや長距離モデルにおいて重要な要素である車内スペースの解放や車体重量の軽量化が実現します。商業的な準備が整うかどうかは、自動焼結ラインと高圧ラミネーションラインが、10年後半までに従来のリチウムイオンと同等まで製造コストを削減できるかどうかにかかっています。

ニッケル・マンガン・コバルト化学は、2024年の電気自動車用バッテリー・システム市場規模の61.38%を占め、最大航続距離を必要とする高級乗用車や小型トラックでの地位を確立しています。継続的なコバルト含有量の削減とマンガンリッチ配合により、価格高騰や倫理的調達の懸念にさらされることが少なくなります。

リン酸鉄リチウムは、強固な安全性、豊富な原料供給量、低コストを背景に急上昇し、格安セグメントと大型商用車を惹きつける。CAGR成長率44.16%のナトリウムイオン電池は、-40℃までの低温動作が可能で、頻繁な急速充電サイクルにも耐えます。リチウム含有量が限りなくゼロに近いため、価格リスクが緩和され、リチウム埋蔵量の乏しい地域での国内資源利用が可能になります。ナトリウムイオンとリチウムイオンを組み合わせたハイブリッド・パックは、性能を維持しながらコストを最適化し、密度が200Wh/kgに達すれば、ナトリウムイオン完全移行への架け橋となるアーキテクチャを構築します。

地域分析

アジア太平洋地域は、鉱物加工からセル組立、車両製造まで一貫したサプライチェーンに支えられ、2024年の電気自動車用バッテリーシステム市場で64.32%のシェアを維持した。中国だけは、国内需要が堅調に推移し、特に東南アジアとラテンアメリカへの輸出が急増するため、2030年までの大幅な成長を支えています。日本は固体研究を進め、韓国は競争力を回復するために高マンガン化学に軸足を移します。政府のインセンティブ調整と協調的なインフラ支出は、地域のエコシステムを引き続き強化します。

北米は第2位の市場規模を記録し、インフレ削減法はクリーンエネルギー資金に3,690億米ドルを投入し、重要鉱物の基準値を引き上げ、新たなギガファクトリーと中流精製プロジェクトの強固なパイプラインを形成します。同様に、欧州はグリーン・ディール政策と欧州電池同盟を背景に、CAGR 9.40%で前進しています。戦略的自律性により、官民合弁事業が資金提供する地域密着型の正極生産とセル組立が推進されます。ドイツはシリコンリッチ負極を推進する研究パートナーシップを主導し、スペインとフランスは大衆市場向けのリン酸鉄リチウムに注力しています。

中東・アフリカ地域はCAGR 15.74%で最も高い成長を遂げています。サウジアラビアは、経済の多様化と自動車製造の川下確保のため、総合電池複合施設に60億米ドルを投資します。アラブ首長国連邦は2035年までに電気自動車普及率25%を目標に掲げ、首長国間の高速道路沿いの充電コリドー整備を進めています。ガーナ、モロッコ、ルワンダの初期段階のプロジェクトは、譲許的な資金調達と開発援助機関による技術支援の恩恵を受けており、二輪車と軽商用車の地域電化を大陸に位置づけています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 政府のインセンティブとゼロエミッション義務化

- リチウムイオンのコスト低下とエネルギー密度の向上

- OEMのギガ工場建設と供給協定

- 急速充電ネットワークの拡大

- バッテリーを収益化するビークル・ツー・グリッド・プログラム

- バッテリー・ヘルス分析と連動する保険割引

- 市場抑制要因

- クリティカルミネラルの供給と価格変動

- 熱暴走リコールと安全認識

- サプライチェーンを混乱させる貿易障壁とローカルコンテンツ規制

- LFP/Naイオンケミストリーの不確実なリサイクル経済性

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- 電池製造能力分析

- 電池リサイクルとセカンドライフ分析

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- バッテリータイプ別

- リチウムイオン

- ニッケル水素

- 鉛蓄電池

- ウルトラキャパシタ

- ソリッドステートその他

- 電池化学別

- NMC

- NCA

- LFP

- LMO

- ナトリウムイオンと新興

- 車両タイプ別

- 乗用車

- 商用車

- 推進技術別

- バッテリー電気自動車(BEV)

- プラグインハイブリッド車(PHEV)

- ハイブリッド電気自動車(HEV)

- 地域別

- 北米

- 米国

- カナダ

- その他北米地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- 韓国

- インド

- オーストラリア

- タイ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- 南アフリカ

- エジプト

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Contemporary Amperex Technology Co., Limited.(CATL)

- BYD Co. Ltd.

- LG Energy Solution Ltd.

- Panasonic Holdings Corporation

- Samsung SDI Co., Ltd.

- SK On Co., Ltd.

- AESC Group Ltd.

- CALB

- Gotion High-tech Co., Ltd.

- EVE Energy Co., Ltd.

- Farasis Energy Europe GmbH

- Northvolt AB

- ProLogium Technology Co., Ltd

- QuantumScape Battery, Inc.

- Solid Power Inc.

- StoreDot

- SES AI Corp.

- Hitachi Energy Ltd.

- Johnson Controls International plc