|

市場調査レポート

商品コード

1408589

金属スクラップのリサイクル:市場シェア分析、産業動向と統計、2024~2029年成長予測Scrap Metal Recycling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 金属スクラップのリサイクル:市場シェア分析、産業動向と統計、2024~2029年成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

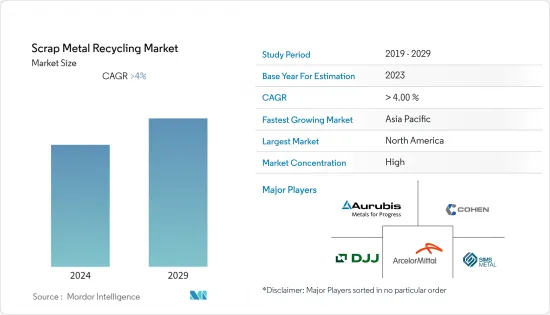

金属スクラップのリサイクル市場は今年末までに9億4,739万トンに達すると推定・予測され、今後5年間で11億6,433万トンに達すると予測され、予測期間中のCAGRは4%です。

COVID-19は金属需要にマイナスの影響を与えました。サプライ・チェーンの混乱と自動車、建設、製造業などの工業生産の落ち込みは、生産量の大幅な減少を経験し、金属スクラップの発生量の減少につながった。しかし、規制が撤廃されて以来、業界は回復しています。自動車需要の増加が市場の成長軌道を回復しつつあります。

主なハイライト

- 市場調査の主な促進要因は、自動車、建設、包装など様々な産業からの金属需要の増大です。さらに、環境意識と持続可能性が市場の成長に有利に働く可能性が高いです。

- その反面、多くの新興諸国ではインフラや回収システムが不足しているため、予測期間中の金属スクラップのリサイクル市場の成長にはマイナスに働くと思われます。

- E廃棄物リサイクルへの注目の高まり、持続可能な素材への需要の増加、循環型経済への注目は、市場に新たな成長機会を提供すると思われます。

- 予測期間中、北米地域が市場を独占すると予想されます。厳しい環境規制、強力なインフラ整備、確立されたリサイクルエコシステムがこの成長を後押しします。

スクラップメタルリサイクル市場動向

自動車産業が市場を独占

- リサイクル金属は自動車産業において重要な役割を果たし、持続可能性への取り組みと環境負荷の低減に貢献しています。

- 自動車産業におけるリサイクル鋼の主な用途の一つは、車体やフレームの製造です。これらは、ドア、フード、フェンダー、トランクリッドなど、自動車に使用される様々な板金部品の製造にも使用されます。さらに、シャーシや足回りの部品は、リサイクル・スチールから作られることが多いです。サスペンション部品や、シートフレームやセーフティ・ビームなどの安全部品の多くは、リサイクル・スチール製であることが多いです。

- アルミニウムもまた、その軽量性と強度特性から、自動車産業には欠かせない素材です。リサイクル・アルミニウムは、エンジン・ブロック、ホイール、ボディ・パネルなどの部品の製造に使用されます。アルミニウムをリサイクルするのに必要なエネルギーは、原料のボーキサイト鉱石から製造するよりもはるかに少なく、環境にやさしい選択肢です。リサイクル銅は、自動車の配線や電気部品にも使用できます。

- さらに、リサイクルされた鉛は、新しい自動車用バッテリーを作るために再溶解することができ、サイクルを最初からやり直すことができます。

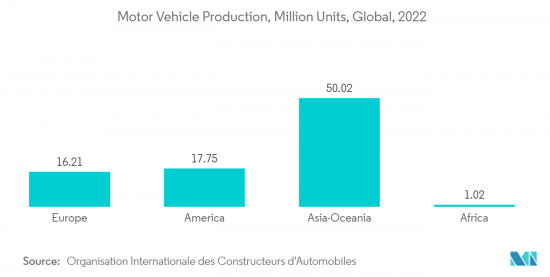

- 世界の自動車産業は2022年に自動車生産台数が大幅に増加し、世界中で8,500万台以上が製造されました。この前年比6%増は、自動車需要の高まりを示し、金属スクラップのリサイクル市場に影響を与えています。

- アメリカの自動車生産の伸びは特に顕著で、2022年には前年比10%増となります。カナダは122万台、メキシコは350万台、米国は1,006万台と、いずれも生産拡大が見られます。

- さらに、米国における国内電気自動車(EV)製造への投資は、EV生産と関連部品への注目が高まっていることを示しています。自動車メーカー各社は2022年にEV製造に合計130億米ドルを投資すると発表しており、電気自動車の開発・導入に向けた動きは明らかです。

- 2022年、欧州の自動車生産台数は1%微減し、合計1,621万6,888台となりました。この減少は、欧州のエネルギー危機や継続的なサプライチェーンの混乱など、いくつかの要因に起因しています。これらの課題は、欧州の自動車セクターに悪影響を及ぼし、2023年の自動車セクターの脆弱性を高めています。

- アジア地域の経済とセクターは、同地域の人口増加に牽引され、絶えず進化しています。自動車産業はこの成長の恩恵を受けているセクターのひとつであり、人口増加により効率的なモビリティ・ソリューションに対する需要が高まっています。アジアは、世界で最も価値のある自動車メーカーの本拠地として高い評価を得ています。

- 同様に、韓国でも自動車生産がプラス成長を遂げています。韓国自動車工業会(KAMA)によると、韓国の2022年の自動車生産台数は375万台で、前年の生産台数362万台に比べ9%増となった。

- 南米では、自動車産業に顕著な進展が見られ、国によって生産動向はさまざまです。コロンビアは前年比26%増の51,455台と大幅な伸びを示しました。アルゼンチンも24%増と大幅な伸びを示し、生産台数は536,893台に達しました。

- これらの要因を考慮すると、スクラップ金属リサイクル市場は、世界の自動車生産台数の増加、北米とアジアの自動車製造の急増、EV市場の拡大による自動車需要の増加から恩恵を受けると予想されます。

市場を独占する北米

- 鉄鋼やアルミニウムなどのリサイクル金属は、建設プロジェクトで一般的に使用されています。それらは構造要素、鉄筋、屋根材、ファサード・パネルを作るために利用されます。建設におけるリサイクル金属は、原材料の需要を減らし、エネルギーを節約し、炭素排出を削減します。

- 多くの電子機器には金属、特に金、銀、プラチナ、パラジウムなどの貴金属が使われています。これらの金属は、回路基板、コネクター、配線、および様々な部品に使用されています。電子廃棄物のリサイクルは、貴重な金属を回収し、有害物質が埋立地で終わるのを防ぐために極めて重要です。

- 航空宇宙分野では、アルミニウムやチタンなどのリサイクル金属が、翼、胴体、エンジン部品などの航空機部品の製造に利用されています。これらはまた、さまざまな消費財にも利用できます。椅子やベッドフレームなどの金属製家具には、リサイクルされた中身が含まれていることが多いです。家電製品では、金属ケーシング、フレーム、内部部品などの部品に使われています。

- 米国は北米最大の航空市場を有し、保有機体数も世界最大級です。フランス、中国、ドイツといった国々への航空宇宙部品の輸出が好調で、米国での個人消費も堅調なことから、航空宇宙産業における製造活動が活発化しており、同国の航空宇宙材料市場にもプラスの勢いをもたらすと期待されています。

- さらに米国では、連邦航空局(FAA)によると、民間航空機は2041年には8,756機まで増加し、CAGRは2%になると予測されています。

- 航空宇宙産業のこの成長は、航空宇宙材料の需要にプラスの影響を与え、それによって同国の金属スクラップのリサイクル市場に影響を与えると予想されます。

- 2022年の国防予算において、米国政府は国防プログラムに7,682億米ドルを認め、これはバイデン政権の当初予算要求から約2%の増加です。

- 米国国勢調査局によると、米国では住宅着工件数が顕著な伸びを示しており、住宅建設部門の繁栄を示しています。2023年5月の民間住宅着工件数は季節調整済み年率163万1,000件に達し、2023年4月の改定値と比べて21.7%の大幅増となった。2023年5月の一戸建て住宅着工戸数も18.5%の大幅増となった。これらの数字は、住宅に対する旺盛な需要と、住宅建設における調査対象市場の潜在性を示しています。

- 2022年、カナダのeコマース利用者は2,700万人を超え、カナダ人口の75%を占めました。この数字は2025年には77.6%に増加すると予想されています。国際貿易局によると、2022年3月のeコマース売上高は約23億4,000万米ドルでした。小売eコマースの売上高は、2025年までに403億米ドルに達すると推定されています。eコマースが拡大し続けるにつれて、電子機器の効率的なリサイクルと廃棄のニーズも高まると思われます。

- 上記の要因はすべて、予測期間中に北米のスクラップメタルリサイクル市場の成長を促進すると思われます。

金属スクラップのリサイクル業界の概要

金属スクラップのリサイクル市場は統合されています。主な企業(順不同)は、Aurubis AG、COHEN、The David J. Joseph Company, LLC、Sims Limited、ArcelorMittalなどです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 環境意識と持続可能性

- 省エネにつながる金属リサイクル

- 様々なエンドユーザー産業からの需要の高まり

- 抑制要因

- 多くの国におけるインフラと回収システムの欠如

- 品質と汚染の問題

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 金属の種類

- 鉄

- 鉄

- 鉄鋼

- 非鉄

- 銅

- アルミニウム

- 鉛

- その他

- 鉄

- 産業別

- 自動車

- 航空宇宙・防衛

- 建設

- 電気・電子

- 製造業および産業部門

- 家電

- その他

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- AIM Recycling

- ArcelorMittal

- Aurubis AG

- CMR Green Technologies Ltd

- COHEN

- Greenwave Technology Solutions, Inc.

- OmniSource, LLC

- Sims Limited

- SL Recycling

- The David J. Joseph Company(Nucor Corporation)

- TKC Metal Recycling Inc.

第7章 市場機会と今後の動向

- 成長するE-wasteリサイクル市場

- 持続可能な素材への需要の高まりと循環型経済への注目

The scrap metal recycling market is estimated to reach 947.39 million tons by the end of this year and is projected to reach 1,164.33 million tons in the next five years, registering a CAGR of 4% during the forecast period.

Covid-19 negatively impacted the demand for metals. The disruption in supply chains and decline in industrial production such as automotive, construction, and manufacturing experienced a significant decline in production, leading to reduced scrap metal generation. However, since restrictions were removed, the industry has been recovering. A rise in demand for automobiles is restoring the market's growth trajectory.

Key Highlights

- A major factor driving the market studied is the growing demand for metals from various industries such as automotive, construction, and packaging. Additionally, environmental awareness and sustainability will likely favor the market's growth.

- On the flip side, the lack of infrastructure and collection systems in many developing countries will negatively affect the growth of the scrap metal recycling market during the forecast period.

- The growing focus on E-waste recycling, increasing demand for sustainable materials, and focus on circular economy will likely provide new growth opportunities for the market.

- North American region is expected to dominate the market during the forecast period. Stringent environmental regulations, strong infrastructure development, and a well-established recycling ecosystem drive this growth.

Scrap Metal Recycling Market Trends

Automotive Industry to Dominate the Market

- Recycled metals play a significant role in the automotive industry contributing to sustainability efforts and reducing environmental impacts.

- One of the primary uses of recycled steel in the automotive industry is in the production of vehicle bodies ad frames. These are also used to manufacture various sheet metal components used in vehicles, such as doors, hoods, fenders, and trunk lids. Moreover, chassis and undercarriage components are often made from recycled steel. Many of the suspension parts and safety components, such as seat frames and safety beams, are often made of recycled steel.

- Aluminum is another essential material in the automotive industry due to its lightweight and strength properties. Recycled aluminum is used to produce parts like engine blocks, wheels, and body panels. Recycling aluminum requires significantly less energy than producing it from raw bauxite ore, making it a more environmentally friendly option. Recycled copper can also be used in automotive wiring and electrical components.

- Moreover, recycled lead can be remelted to create new car batteries, starting the cycle from the beginning.

- The global automotive industry experienced a significant increase in vehicle production in 2022, with more than 85 million motor vehicles manufactured worldwide. This 6% growth compared to the previous year indicates a rising demand for automotive, influencing the scrap metal recycling market.

- The growth in America's automotive production is particularly notable, with a 10% year-on-year increase in 2022. Canada, Mexico, and the United States all witnessed production expansions, reaching production figures of 1.22 million units, 3.50 million units, and 10.06 million units, respectively.

- Furthermore, the investment in domestic electric vehicle (EV) manufacturing in the United States indicates a growing focus on EV production and associated components. With auto manufacturing companies announcing a combined investment of USD 13 billion in EV manufacturing in 2022, there is a clear push toward developing and adopting electric vehicles.

- In 2022, Europe experienced a slight decline of 1% in motor vehicle production, with a total of 16,216,888 vehicles manufactured. This decrease can be attributed to several factors, such as the energy crisis in Europe and ongoing supply chain disruptions. These challenges have had a negative impact on the European automotive sector, making it more vulnerable in 2023.

- Asia's economies and sectors, driven by the region's growing population, continuously evolve. The automotive industry is one of the sectors benefiting from this growth, as the increasing population creates a higher demand for efficient mobility solutions. Asia has gained a reputation for being home to some of the world's most valuable vehicle manufacturers.

- Similarly, South Korea has experienced positive growth in automotive production. According to the Korea Automobile Manufacturers Association (KAMA), the country produced 3.75 million vehicles in 2022, representing a notable 9% increase compared to the previous year's production of 3.62 million units.

- In South America, there have been notable developments in the automotive industry, with different countries experiencing varying production trends. Colombia witnessed a significant increase in year-on-year production, with a 26% jump, reaching 51,455 units. Argentina also experienced substantial growth, with a 24% increase and production reaching 536,893 units.

- Considering these factors, the scrap metal recycling market is expected to benefit from the increased demand for automobiles driven by the growing global vehicle production, the surge in North American and Asian automotive manufacturing, and the expanding EV market.

North America to Dominate the Market

- Recycled metals, such as steel and aluminum, are commonly used in construction projects. They are utilized to create structural elements, reinforcing bars, roofing materials, and facade panels. The recycled metals in construction reduce the demand for raw materials, conserves energy, and lowers carbon emissions.

- Many electronic devices contain metals, especially precious metals like gold, silver, platinum, and palladium. These metals are used in circuit boards, connectors, wiring, and various components. Recycling electronic waste is crucial for recovering valuable metals and preventing hazardous materials from ending up in landfills.

- The aerospace sector utilizes recycled metals, such as aluminum and titanium, in the manufacturing of aircraft components, including wings, fuselages, and engine parts. These can also be used in various consumer goods. Metal furniture pieces, such as chairs and bed frames, often contain recycled contents. In household appliances, these are used in components like metal casings, frames, and internal parts.

- The United States has the largest aviation market in North America and one of the world's largest fleet sizes. Strong exports of aerospace components to countries, such as France, China, and Germany, along with robust consumer spending in the United States, have been driving the manufacturing activities in the aerospace industry, which is expected to induce a positive momentum for the aerospace material market in the country.

- Additionally, in the United States, according to the Federal Aviation Administration (FAA), the commercial fleet is forecast to increase to 8,756 in 2041, with an average annual growth rate of 2% per year.

- This growth in the aerospace industry is expected to positively impact the demand for aerospace materials, thereby influencing the scrap metal recycling market in the country.

- In the 2022 defense budget, the United States government allowed USD 768.2 billion for national defense programs, which is about a 2% increase from the Biden administration's original budget request.

- According to the United States Census Bureau, housing starts have shown a notable increase in the United States, indicating a thriving residential construction sector. Privately-owned housing starts in May 2023 reached a seasonally adjusted annual rate of 1,631,000, a significant rise of 21.7% compared to the revised April 2023 estimate. Single-family housing starts also experienced a substantial growth rate of 18.5% in May 2023. These figures indicate a strong demand for housing and a potential market for the studied market in residential construction.

- In 2022, there were over 27 million eCommerce users in Canada, accounting for 75% of the Canadian population. This number is expected to grow to 77.6% in 2025. According to the International Trade Administration, in March 2022, e-commerce sales amounted to approximately USD 2.34 billion. Retail eCommerce sales are estimated to total USD 40.3 billion by 2025. As e-commerce continues to expand, there will be a corresponding need for efficient recycling and disposal of electronics.

- All the above-mentioned factors are likely to fuel the growth of North America's scrap metal recycling market over the forecast time frame.

Scrap Metal Recycling Industry Overview

The scrap metal recycling market is consolidated. Some of the major companies (in no particular order) are Aurubis AG, COHEN, The David J. Joseph Company, LLC, Sims Limited, and ArcelorMittal.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions And Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Environmental Awareness and Sustainability

- 4.1.2 Metal Recycling Leading to Energy Saving

- 4.1.3 Growing Demand from Various End-user Industries

- 4.2 Restraints

- 4.2.1 Lack of Infrastructure and Collection Systems in Many Countries

- 4.2.2 Quality and Contamination Issues

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Metal Type

- 5.1.1 Ferrous

- 5.1.1.1 Iron

- 5.1.1.2 Steel

- 5.1.2 Non-ferrous

- 5.1.2.1 Copper

- 5.1.2.2 Aluminum

- 5.1.2.3 Lead

- 5.1.2.4 Others

- 5.1.1 Ferrous

- 5.2 Industry

- 5.2.1 Automotive

- 5.2.2 Aerospace and Defense

- 5.2.3 Construction

- 5.2.4 Electrical and Electronics

- 5.2.5 Manufacturing and Industrial Sectors

- 5.2.6 Consumer Appliances

- 5.2.7 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AIM Recycling

- 6.4.2 ArcelorMittal

- 6.4.3 Aurubis AG

- 6.4.4 CMR Green Technologies Ltd

- 6.4.5 COHEN

- 6.4.6 Greenwave Technology Solutions, Inc.

- 6.4.7 OmniSource, LLC

- 6.4.8 Sims Limited

- 6.4.9 SL Recycling

- 6.4.10 The David J. Joseph Company (Nucor Corporation)

- 6.4.11 TKC Metal Recycling Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing E-waste Recycling Market

- 7.2 Increasing Demand for Sustainable Materials and Focus on Circular Economy