|

|

市場調査レポート

商品コード

1408408

ゲーム内広告-市場シェア分析、業界動向・統計、2024~2029年成長予測In-game Advertising - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ゲーム内広告-市場シェア分析、業界動向・統計、2024~2029年成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

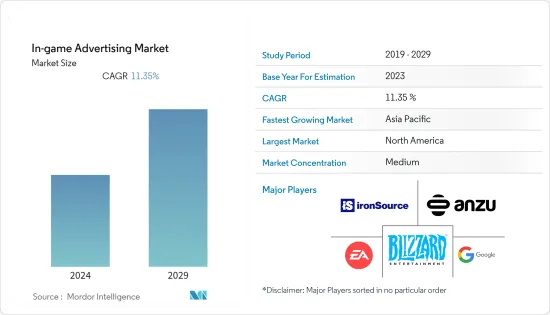

ゲーム内広告の世界市場規模は今年78億5,000万米ドルで、予測期間中のCAGRは11.35%を記録し、今後5年間で134億3,000万米ドルに達すると予測されています。

ゲーム内広告市場の成長は、ソーシャルゲームやモバイルゲームへの関心の高まりから恩恵を受けると予想されます。デスクトップとモバイルゲームでは、広告を含め、コマーシャル、ビルボード、背景グラフィックが使用されることがあります。さらに、これらの広告が邪魔にならないため、ゲーマーはよりシームレスにゲームを体験することができます。ゲーム内コマーシャルは、オーディオビジュアルにより大きなインパクトを与え、視聴者に肯定的かつ永続的な製品印象を残すと予想されます。

主要ハイライト

- リアルタイム入札(RTB)と人工知能(AI)は、オンラインゲームへの広告掲載に活用されています。以前は、代理店がゲーム内プロモーションの購入や対応を担当しており、コストがかかることもあった。しかし、プログラマティック広告バイイングは、死活的な関与を排除することで、このプロセスをより効率的かつ費用対効果の高いものにしました。従来の方法では、広告主はゲーム内広告を購入するために、提案、見積もり、入札、人間との交渉を経なければならなかった。逆に、プログラマティックなゲーム内広告の購入は、ディスプレイスペースを獲得するためにアルゴリズムを採用しています。

- 技術の進歩により、デジタル広告のプレゼンテーションは消費者のモバイルデバイスに接続し、企業のソーシャルメディアアカウントやウェブサイトに移動させることができるようになった。また、静止画広告に拡大現実(AR)を組み込んで双方向性を持たせることも可能で、企業は屋外広告でこうした技術を利用して認知度を高めることができます。ロンドンのキャンペーンでは、デジタルスクリーンに接続された拡大現実用途に、病気の患者の写真と空の血液パックが映し出されました。視覚認識により、ドナーになる可能性のある人々のモバイル画面に針とチューブが映し出され、バーチャルな血流と患者が目に見えて元気になる様子が示されました。こうした特徴は広告を魅力的にし、世界のゲーム内広告市場の成長に貢献しています。

- ソーシャルメディア、モバイルゲーム、オンラインカジュアルゲームに対する人々の関心の高まりは、予測される数年間、世界のオンラインカジュアルゲーム市場における広告セグメントの成長を促進すると予測されます。さらに、業界の主要参入企業の戦略的買収や事業拡大が、セグメントの成長を高めると予想されます。2022年5月、WPPと、フォートナイトやUnreal Engineを開発したインタラクティブ・エンターテインメント企業であるEpic Gamesは、WPPのエージェンシーがメタバースにおいて新時代のデジタル体験をブランドに提供できるよう支援する新たなパートナーシップを発表しました。フォートナイトでパーソナライズされたブランド体験を開発し、リアルタイムの3D制作とバーチャルプロダクションにUnreal Engineを使用する方法を、何千人ものWPPのクリエーターとエンジニアに教える新しいトレーニングプログラムが開始されます。

- その一方で、広告の配置はゲームの流れや文脈に沿ったものでなければならないため、ゲーム内広告の重要な側面です。広告会社にとっては、ゲーマーにとって自然に見え、広告主にとっては独占的な広告を戦略的に配置することが不可欠です。残念なことに、一部の広告会社はそれを怠り、ゲーム体験の阻害や広告主のブランドへの悪影響を示しています。例えば、食べ物をテーマにしたゲームにスポーツ関連の広告を表示するのは不適切な配置です。

- InMobi Pulse PlatformがCOVID-19パンデミックの際に実施した調査によると、女性の49%がパンデミックがきっかけでゲームを始めたといいます。彼女たちは1日平均53分をゲームアプリに費やし、79%がゲームを進めるために広告を見ていました。サウジアラビアでは、STCがゲームトラフィックの300%増を記録しました。さらに、Twitchのライブストリーミングゲームプラットフォームは、パンデミックで30億時間のゲーム時間を記録し、四半期としては過去最大となった。

ゲーム内広告市場の動向

オンラインゲームの増加が市場を牽引する見込み

- オンラインゲーム市場は目覚ましい市場規模を実現しており、市場規模の主要促進要因は、都市部と農村部におけるインターネット普及率の向上と低価格モバイルの拡大であると考えられます。マネタイズは、ダウンロードごとのアプリ内課金やゲーマーによるサブスクリプションサービス、アプリ内広告、インセンティブベースの広告など、エコシステムによる収益ストリームを通じて実現されます。現在の市場シナリオでは、マネタイズはパブリッシャーと広告主によって支配されています。近年、インターネットのエコシステムは、エンドツーエンドのローカルゲーム開発によって軌道修正を始めています。例えば、Zyngaのソーシャルからモバイルへのシフトは、いくつかの厳しい年を意味したが、2022年2月には、前年同期比52%増の7億2,700万米ドルの第4四半期の収益を報告しました。

- 中国出版協会のゲーム委員会によると、2022年、中国のモバイルゲーマーは約6億5,400万人だった。カジュアルモバイルゲームの収益は340億人民元に達しました。このようなさまざまなソースからの収益創出は、ゲーマーの数の増加によるものであり、これはゲーム内広告の参入企業が新しい広告を開発し、膨大な顧客基盤にその存在を拡大するための機会を作成します。インド経済調査(Economic Survey of India 2021-22)によると、インドのインターネットユーザー数は2021年に8億3,000万人を超え、2015年から5億3,000万人以上増加します。オンラインゲームは、エンターテインメント業界において大きな足場を築いています。6億2,800万人以上のユーザーベースが予測され、経済内のゲームエコシステムを後押ししています。

- スマートフォンは最も人気のあるゲーム機器であり、広告主は広告のないプラットフォームにお金を払いそうにないカジュアルな参入企業にリーチすることができます。開発者は、リワードビデオ広告、オファーウォール広告、インタースティシャル広告など、モバイルゲームの広告収入を促進するために、さまざまなオンラインカジュアルゲーム広告戦略や広告フォーマットをゲームに統合することができます。最高のパフォーマンスと最高のeCPM(1,000インプレッションあたりの実効コスト)を提供する広告は、ゲームループに直接組み込まれ、ゲーム内経済を補完するもの、言い換えれば、ゲームのコンポーネントとして機能する広告です。

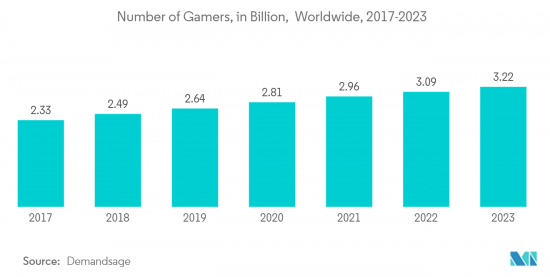

- Demandsageによると、2023年現在、世界には32億2,000万人のゲーマーがいるといわれています。ゲーム業界は、新しい技術革新にとって最もエキサイティングな場所のひとつとなっています。競合が激化するにつれ、開発者や企業はより優れたハードウェアやソフトウェアを導入し、業界全体が加速度的に前進しています。人口動態の急速な変化、地域、モバイルエコシステムとエンターテインメントの状況における消費により、ゲームスペースは業界内、伝統的な金融市場、さらには政府からの注目と投資を集めています。

- 2023年5月、ゲーム内広告を実現するFrameplayとゲームマーケティング会社のGamestackは、急成長を続けるインドのゲーム市場において、本質的なゲーム内広告ソリューションを提供するための提携を発表しました。この提携により、ブランドは没入感のあるゲーム内広告体験を通じて、インドのゲームコミュニティに参加する膨大なオーディエンスにリーチすることが可能になります。FrameplayとGamestackの提携は、各ブランドがインドのゲーム利用者を対象にすることを検討している重要な時期に実現しました。

北米が市場で大きなシェアを占める見込み

- 北米のゲーム内広告市場は、米国やカナダなどの国々でモバイルゲームやコンソールゲームの人気が高まっていることから、拡大が見込まれています。携帯電話やインターネットアクセスの普及率が高いことから、モバイルゲーマーが大幅に増加しています。また、ゲーム機の販売台数の増加により、ゲーム機における高度な機能を備えたAAAゲームの需要も増加傾向にあります。さらに、eスポーツの人気の高まりとスポンサーの関与も市場の成長に寄与しています。全体として、北米のゲーム内広告市場は予測期間中に拡大する見込みです。

- ESAの調査によると、米国全域で2億2,700万人以上の参入企業が最近ビデオゲームをプレイしています。参入企業の80%は18歳以上です。さらに、18歳以下のアメリカの子供の76%が参入企業です。さらに、アメリカの家庭の74%が少なくとも1台のビデオゲーム参入企業を持っています。また、パンデミックの最中、71%の親がビデオゲームが子供にとって必要な息抜きになったことに同意し、66%がビデオゲームのおかげで通信教育への移行がより身近になったことに同意しています。このようなオンラインゲーマーの大幅な増加は、研究市場の成長を可能にすると思われます。

- 携帯電話ゲームは米国で急成長している産業であり、最大のゲームパブリッシャーのひとつが米国に拠点を置いています。42Mattersによると、グーグルプレイのゲームパブリッシャー16万1,440社のうち、8,797社以上がアメリカの企業です。Lion Studios、Imangi Studios、Ivy、Play365、i6 Games、DVloper、Oppana Games、Lowtech Studios、Roblox Corporation、Niantic Inc.などがアメリカの有名パブリッシャーです。米国はグーグルプレイの全ゲームパブリッシャーの5%を占めています。このような巨大なモバイルゲームは、この地域で調査された市場が成長する機会を生み出すと思われます。

- 同様に、2022年の42mattrersカナダのモバイルゲーム統計によると、グーグルプレイで利用可能な43万817のゲームのうち、6,356以上がカナダのパブリッシャーによるものです。Real Drive 3D、Tangle Master 3D、Brain Test:トリッキーパズル」、「Move People」、「Bingo Blitz-Bingo Games」、「PAW Patrol Rescue World」、「Spider Solitaire」、「Solitaire」、「Blush」、「Sonic Dash-Endless Running」は、カナダのパブリッシャーから最もダウンロードされたモバイルゲームです。カナダのパブリッシャーは、Google Playの全モバイルゲームの1%を占めています。さらに、カナダで公開されたモバイルゲームの62%でGoogle Firebaseが使用されています。合計3,451のゲームがあった。

- 地域の参入企業は、地域でのプレゼンスを拡大するために資金を調達しています。例えば、2023年6月、ゲーム内広告会社のAnzuは4,800万米ドルのシリーズBラウンドを発表し、同社の資金調達総額は6,500万米ドルに達しました。同社は新たな資本を再投資するための当面の計画として、営業とパートナーシップの陣頭指揮を執る幹部の増員、エンジニアリングチームの拡大、米国でのプレゼンスの拡大を挙げています。

ゲーム内広告業界概要

世界のゲーム内広告市場は、Google LLC、Anzu Virtual Reality Ltd.、Blizzard Entertainment Inc.、Electronic Arts Inc.、IronSource Ltd.などの参入企業が存在し、適度に統合されています。各社は戦略的パートナーシップや製品開発に継続的に投資し、市場シェアを大きく伸ばしています。最近の市場開拓は以下の通りです。

2023年8月、Alookは最も先進的なゲーム内広告プラットフォームの1つであるAnzuと提携しました。両社は、Adlookの次世代ブランド成長プラットフォームを通じて、ブランドや代理店がゲーム内広告の大きな可能性を活用できるよう支援することを目的としています。この新しいパートナーシップにより、AlookのクライアントはIABに準拠したゲーム内動画やバナー広告を、プラットフォーム間で大規模にプログラマティックに配信し、世界中のゲーム利用者にリーチすることができます。Anzuの革新的なSDK技術はゲームに統合され、広告プレースメントとファーストパーティデータを完全にコントロールしながら、高品質のダイレクトトラフィックを提供します。

2023年4月、TransUnionは、固有のゲーム内広告を実現する世界的企業であるFrameplayと提携し、ブランドやマーケティング担当者が関連性の高いゲーム利用者に効果的にリーチできるよう、利用者ターゲティング能力を強化しました。TransUnionのTruAudience Platformとデータマーケットプレースソリューションを通じて、企業はデータ主導型のゲーム内広告手法を効果的に強化し、ゲーマーとつながることができます。TruAudience Data Marketplaceの基盤となるエンジンは、米国の8,000万世帯を超える愛着のある家庭、ほぼすべての成人と居住者のオーディエンスを決定論的に平準化したビューです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- オンラインゲームの増加

- スマートフォン普及率の伸び

- 市場の抑制要因

- ゲームと広告技術の統合の複雑さ

第6章 市場セグメンテーション

- タイプ別

- 静的

- 動的

- アドバゲーム

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- その他の欧州諸国

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- その他のアジア太平洋諸国

- 中東・アフリカ

- ラテンアメリカ

- 北米

第7章 競争環境

- 企業プロファイル

- Google LLC

- Anzu Virtual Reality Ltd.

- Electronic Arts Inc.

- ironSource Ltd.

- Motive Interactive Inc.

- Playwire LLC

- RapidFire Inc.

- Blizzard Entertainment, Inc.

- Frameplay

第8章 投資分析

第9章 市場機会と今後の動向

The Global In-Game Advertising market is valued at USD 7.85 billion in the current year and is expected to register a CAGR of 11.35% during the forecast period to reach a value of USD 13.43 billion by the next five years. In-game advertising market growth is anticipated to benefit from rising social and mobile gaming interest. Commercials, billboards, and backdrop graphics may be used in desktop and mobile games, including advertising. Additionally, because these ads aren't disruptive, gamers may experience the game more seamlessly. In-game commercials are anticipated to have a more substantial audio-visual impact and leave viewers with positive and enduring product impressions.

Key Highlights

- Real-time bidding (RTB) and artificial intelligence (AI) are utilized to place these advertisements in online games. Previously, agents were responsible for purchasing and dealing with in-game promotions, which could be costly. However, programmatic advertisement buying has made the process more efficient and cost-effective by eliminating mortal involvement. In the traditional method, advertisers had to go through proposals, quotes, tenders, and negotiations with humans to purchase in-game advertisements. Conversely, programmatic in-game advertisement buying employs algorithms to acquire display space.

- Due to technological advances, digital advertising presentations can now connect to consumers' mobile devices, shifting them to companies' social media accounts or websites. Static advertising can also incorporate augmented reality for interactivity, attracting businesses to use these technologies in outdoor advertisements to increase awareness. In a London campaign, an augmented reality application connected to a digital screen showed a picture of a sick patient and an empty blood pack. Visual recognition activated potential donors with a needle and tube on their mobile screens, showing virtual blood flow and the patient visibly enhancing. These features make advertising attractive, contributing to the growth of the global in-game advertising market.

- People's increasing interest in social media, mobile gaming, and online casual gaming is predicted to drive the growth of the advertising segment in the global online casual games market over the forecast years. Furthermore, essential industry players' strategic acquisitions and business expansions are expected to enhance segment growth. In May 2022, WPP and Epic Games, the interactive entertainment firm developer of Fortnite and Unreal Engine, announced a new partnership to assist WPP agencies in delivering a new era of digital experiences for brands in the metaverse. A new training program will be launched to teach thousands of WPP creatives and engineers how to develop personalized brand experiences in Fortnite and use Unreal Engine for real-time 3D creation and virtual production.

- On the flip side, the placement of advertisements is a crucial aspect of in-game advertising, as it must align with the game's flow and context. It is essential for advertising companies to strategically place advertisements in a manner that appears natural to gamers and delivers exclusivity to advertisers. Unfortunately, some advertising companies fail to do so, showing disruptions in the gaming experience and adverse effects on advertisers' brands. For example, displaying sports-related ads in food-themed games would be an inappropriate placement.

- A survey conducted by InMobi Pulse Platform during the COVID-19 pandemic suggested that 49% of women started playing games due to the pandemic. They spent an average of 53 minutes/day on gaming apps, while 79% watched an ad to progress in a game. The gaming activity skyrocketed during the enforced lockdown, with STC recording a 300% growth in gaming traffic in Saudi Arabia. Moreover, Twitch's live-streaming game platform marked up three billion hours of gaming in the pandemic, its largest quarter ever.

In-game Advertising Market Trends

Increase in Online Gaming is Expected to Drive the Market

- The online gaming market realizes impressive volumes, and the key driver of the market volume can be considered the increased internet penetration and expansion of low-cost mobiles among the urban and rural populations. The monetization is realized through revenue streams, such as in-app purchases per download and subscription services by gamers, in-app advertisements, incentive-based advertisements, etc., by the ecosystem. In the current market scenario, monetization is dominated by publishers and advertisers. In recent years, the internet ecosystem has initiated course correction by end-to-end local game development. For instance, Zynga's shift from social to mobile meant several tough years, but in February 2022, it reported Q4 revenue of USD 727 million, up by 52% year-over-year.

- As per the Game Committee of the Publishers Association of China, In 2022, there were about 654 million mobile gamers in China. The revenue of casual mobile games reached CNY 34 billion. Such revenue generation from different sources may be due to the rise in the number of gamers, and this would create an opportunity for the in-game advertising players to develop new ads and expand their presence to a vast customer base. As per the Economic Survey of India 2021-22, India's internet user base crossed 830 million users in 2021, growing by over 530 million since 2015. Online gaming has gained a significant foothold within the entertainment industry. With a projected user base of over 628 million gamers, it boosts the gaming ecosystem within the economy.

- Smartphones are the most popular gaming device, allowing advertisers to reach casual players who are unlikely to pay for ad-free platforms. Developers can integrate many different online casual game advertising strategies and ad formats into their games to drive mobile game ad income, such as rewarded video ads, offer wall ads, and interstitial ads. The advertisements that perform best and deliver the highest eCPMs (effective cost per 1,000 impressions) are the ones that are incorporated directly into the game loop and complement the in-game economy; in other words, ads that work as a component of the game.

- According to Demandsage, there are 3.220 billion gamers in the world as of 2023. The gaming industry has become one of the most exciting places for new tech innovations. As competition has ramped up, developers and companies have been introducing better hardware and software, with the whole industry moving forward at an increased pace. Due to rapid demographic changes, geography, and consumption in the mobile ecosystem and entertainment landscape, the game space is getting increased attention and investment, both from within the industry, traditional financial markets, and even governments.

- In May 2023, Frameplay, an enabler of in-gaming advertising, and Gamestack, a gaming marketing company, announced a partnership to offer intrinsic in-game advertising solutions in the Indian gaming market, which continues to grow rapidly. This collaboration will allow brands to reach a vast audience of engaged Indian gaming communities through immersive in-game advertisement experiences. The association between Frameplay and Gamestack comes at a critical time when brands are examining to target the Indian gaming audience.

North America is Expected to Hold Significant Share of the Market

- The North American in-game advertising market is anticipated to increase due to the increasing popularity of mobile and console gaming in countries like the U.S. and Canada. The high penetration of mobiles and Internet access has led to a significant increase in mobile gamers. The demand for AAA games with advanced features in gaming consoles is also on the rise, fueled by increased console sales. Additionally, the growing popularity of e-sports and the involvement of sponsors contribute to the market's growth. Overall, the North American in-game advertising market is expected to expand in the forecast period.

- According to a study by the ESA, more than 227 million players across the U.S. region have recently played video games. In total, 80% of the players are over 18 years old. Further, 76% of the American kids who are under 18 years are players. Additionally, 74% of American households have at least one video game player. Also, during the pandemic, 71% of parents agree that video games have been a much-needed break for their children, and 66% agree that video games have made the transition to distance learning more accessible. Such a huge rise in online gamers would allow the studied market to grow.

- Mobile phone gaming is a burgeoning industry in the United States, and one of the largest game publishers is based there. According to 42Matters, out of the 161,440 game publishers on Google Play, more than 8,797 are American companies. Lion Studios, Imangi Studios, Ivy, Play365, i6 Games, DVloper, Oppana Games, Lowtech Studios, Roblox Corporation, and Niantic Inc. are some of the most well-known American publishers. The United States accounts for 5% of all game publishers on Google Play. Such huge mobile gaming would create an opportunity for the studied market to grow in the region.

- Similarly, According to 42mattrers Canadian mobile gaming statistics in 2022, Out of the 430,817 games available on Google Play, more than 6,356 are from Canadian publishers. Real Drive 3D, Tangle Master 3D, Brain Test: Tricky Puzzles, Move People, Bingo Blitz- Bingo Games, PAW Patrol Rescue World, Spider Solitaire, Solitaire, Blush, and Sonic Dash - Endless Running are the mobile games with the most downloads from Canadian publishers. Canadian publishers account for 1% of all mobile games on Google Play. Furthermore, Google Firebase is used in 62% of mobile games published in Canada. There were 3,451 games in total.

- The regional players are raising funds to expand their presence in the region. For instance, In June 2023, in-game ad company Anzu announced a USD 48 million Series B round, bringing its total funding to USD 65 million. The company's immediate plans for reinvesting its new capital include hiring more executive leadership to spearhead sales and partnerships, growing its engineering team, and expanding its presence in the U.S.

In-game Advertising Industry Overview

The Global In-Game Advertising market is moderately consolidated with the presence of several players like Google LLC, Anzu Virtual Reality Ltd., Blizzard Entertainment Inc., Electronic Arts Inc., IronSource Ltd., etc. The companies continuously invest in strategic partnerships and product developments to gain substantial market share. Some of the recent developments in the market are:

In August 2023, Adlook partnered with Anzu, one of the most advanced in-game advertising platforms. Together, they aim to assist brands and agencies in harnessing the enormous potential of intrinsic in-game advertising through Adlook's next-generation brand growth platform. Due to the new partnership, Adlook's clients can programmatically serve IAB-compliant ingrained in-game video and banner ads at scale across platforms to reach the global gaming audience. Anzu's innovative SDK technology is integrated into games to deliver high-quality direct traffic with complete control over ad placements and first-party data.

In April 2023, TransUnion entered a collaboration with Frameplay, the global player in enabling inherent in-gaming advertising, to offer enhanced audience targeting abilities for brands and marketers to reach relevant gaming audiences at scale effectively. Through TransUnion's TruAudience Platform and Data Marketplace solutions, firms can effectively enhance their data-driven in-game advertising techniques to connect with gamers. The engine at the base of the TruAudience Data Marketplace is a deterministically leveled view of audiences across 80 million-plus United States attached homes, nearly all adults and residencies in the country.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increase in Online Gaming

- 5.1.2 Growth in the Smartphone Penetration

- 5.2 Market Restrains

- 5.2.1 Complexity in Gaming and Advertisment Technology Integration

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Static

- 6.1.2 Dynamic

- 6.1.3 Advergaming

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 Germany

- 6.2.2.3 France

- 6.2.2.4 Other European Countries

- 6.2.3 APAC

- 6.2.3.1 China

- 6.2.3.2 Japan

- 6.2.3.3 India

- 6.2.3.4 South Korea

- 6.2.3.5 Other APAC countries

- 6.2.4 Middle East and Africa

- 6.2.5 Latin America

- 6.2.1 North America

7 COMPETETIVE LANDSCAPE

- 7.1 Company Profile

- 7.1.1 Google LLC

- 7.1.2 Anzu Virtual Reality Ltd.

- 7.1.3 Blizzard Entertainment Inc.

- 7.1.4 Electronic Arts Inc.

- 7.1.5 ironSource Ltd.

- 7.1.6 Motive Interactive Inc.

- 7.1.7 Playwire LLC

- 7.1.8 RapidFire Inc.

- 7.1.9 Blizzard Entertainment, Inc.

- 7.1.10 Frameplay