|

|

市場調査レポート

商品コード

1408101

飲料-市場シェア分析、産業動向・統計、2024~2029年成長予測Beverages - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 飲料-市場シェア分析、産業動向・統計、2024~2029年成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

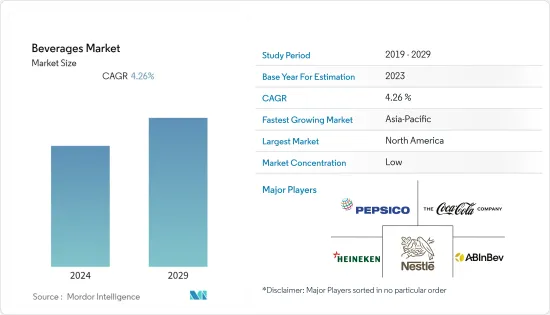

飲料市場は、2024年の3兆7,100億米ドルから2029年には4兆5,800億米ドルに成長し、予測期間中(2024~2029年)のCAGRは4.26%と予測されています。

主要ハイライト

- 健康志向の高まりと生活習慣病の蔓延が消費者に健康飲料の選択を促しました。さらに市場は、特にミレニアル世代とベビーブーム世代の間で低アルコール飲料に対する需要の高まりを目の当たりにしています。例えば、国連貿易統計によると、ハンガリーへのノンアルコール飲料輸入額は2021年の1億5,400万ユーロから2022年には1億7,400万ユーロとピークに達しました。低アルコール飲料の売上が伸びているのは、味を改善した幅広い製品ポートフォリオが入手可能になり、消費者が好みに合わせて製品を選びやすくなったためです。

- さらに、プロスポーツ、レクリエーション的なアウトドア活動、運動や体力づくりに参加する個人の増加が、エナジードリンクなどの栄養補助食品の需要を生み出しています。エナジードリンクは、エネルギーを増加させ、精神的な覚醒度や身体的なパフォーマンスを高めるのに役立つ機能性飲料です。大手企業はさらに、糖尿病やその他の慢性疾患を抱える人々のニーズに応えるため、無糖飲料の開発に注力しています。

- 例えば、2022年、オーストラリアの清涼飲料会社Nexbaは、ビタミンとプレバイオティクスを添加したカフェイン・砂糖不使用のエナジー飲料シリーズを発売しました。ネクスバ・ナチュラル・エナジードリンクは、人工的な原材料を使用しておらず、2種類のフレーバーがあり、レモンユズ味とワイルドシトラス味です。このフレーバーには高麗人参エキス、ビタミンB群、ビタミンCが含まれており、腸内環境を改善し、エネルギーレベルを高めるとしています。したがって、上記の要因は予測期間中、市場にプラスの影響を与えると思われます。

飲料市場の動向

消費者の無糖飲料への傾斜

- 消費者の全人的な健康への関心の高さから、健康的な食品の選択が注目されています。消費者は低糖質で健康増進成分を含む製品を求めています。さらに、国際糖尿病連合によると、インドには2019年に7,700万人の糖尿病患者がおり、これは世界第2位です。2030年には1億100万人に達すると予測されています。同じ情報源によると、中国では2019年に約1億1,400万人の成人が糖尿病を患っていました。世界的に糖尿病の有病率が高いことから、消費者は健康的な食事と活動的なライフスタイルの重要性を認識するようになっています。

- さらに、減糖または無糖製品に対する消費者の嗜好の変化は、飲料メーカーを製品革新に向かわせる。市場のメーカー各社は、消費者の期待に応え、消費者が求める機能性を提供するために、自社製品を効果的に発信しています。糖分の過剰摂取による弊害を防ぐため、糖分の多い飲料の摂取を積極的に避けようとする消費者の需要に応えるため、様々な斬新な製品を開発しています。

- 例えば、Shine Drinkは2022年10月、砂糖不使用の新シリーズを発売しました。この製品は「ブレイン・ドリンク」または「スマート・ドリンク」と呼ばれ、天然の機能性成分を含んでいます。ブルーベリーレモネードとピーチパッションフルーツのフレーバーがあります。さらに、飲料カテゴリーにおけるより健康的な代替品への需要に応えるため、トップブランドと競合する非公開会社も市場に参入しています。

北米が最大の市場シェアを占める

- ノンアルコール飲料に対する消費者の嗜好の変化は、北米の飲料市場における主要な市場の促進要因です。加えて、レジャースポーツ、身体活動、ジムでの激しい運動への幅広い参加により、スポーツドリンクやエナジードリンクの消費量が多いことも市場成長の要因となっています。この動向は、さまざまなスポーツ活動への学校や大学生の積極的な参加を促進するための政府のイニシアティブの高まりにより、予測期間中も続くと予想されます。

- さらに、乳糖不耐症や乳製品アレルギーの増加により、果物や野菜ジュース、フレーバー付きコールドドリンクなどの植物性飲料が浸透しています。加えて、オーガニックやクリーンラベル製品への親近感の高まりは、主要メーカーがレディ・トゥ・ドリンク飲料カテゴリーで革新的なバリエーションを開発することに影響を与えています。

- 例えば、2022年2月、Starbucksは、キャラメルワッフルクッキーとダークチョコレートブラウニーの2つのフレーバーを持つ新しい植物由来のフラペチーノラインを発売しました。さらに、携帯性と利便性に対する消費者の強い需要が、包装形態の革新、包装材料の軽量化、フレキシブル包装の適用拡大を加速させています。このように、これらすべての要因が北米の飲料市場を牽引しています。

飲料業界概要

市場は競争が激しく、Nestle S.A.、Anheuser-Busch InBev、Heineken N.V.、PepsiCo, Inc.、The Coca-Cola Companyなどの主要企業が事業を展開しています。同市場では、世界的に消費者の嗜好が変化しているため、さまざまな企業が製品イノベーションを戦略として採用しています。各社が最も注力しているのは、さまざまなフレーバーや機能性を付加した製品を提供することで、それによって消費者の嗜好に効率的に応えることです。例えば、2022年9月、PepsiCoのブランドであるゲータレードは、アスリート向けのカフェイン入りエナジードリンク「ファストスイッチ」を発売しました。この製品は、エナジードリンクとスポーツドリンクを掛け合わせたものです。この製品は無炭酸で、砂糖を含まず、人工着色料や人工香料を使用していないです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 植物由来でクリーンラベルのRTD製品に対する嗜好

- 消費者の無糖飲料への傾斜

- 市場抑制要因

- 飲料による健康問題への懸念

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 製品タイプ別

- アルコール飲料

- ビール

- ワイン

- スピリッツ

- ノンアルコール飲料

- エナジー&スポーツドリンク

- ソフトドリンク

- ボトルウォーター

- ジュース

- RTD紅茶・コーヒー

- その他のノンアルコール飲料

- アルコール飲料

- 流通チャネル別

- オントレード

- オフトレード

- スーパーマーケット/ハイパーマーケット

- コンビニエンスストア/食料品店

- オンライン小売店

- その他のオフトレード・チャネル

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他の北米

- 欧州

- 英国

- ドイツ

- スペイン

- フランス

- イタリア

- ロシア

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- その他のアジア太平洋

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- Nestle S.A.

- PepsiCo, Inc.

- The Coca-Cola Company

- Anheuser-Busch InBev

- Heineken N.V.

- Diageo plc

- Suntory Holdings Limited

- Constellation Brands, Inc.

- Red Bull GmbH

- Keurig Dr Pepper

第7章 市場機会と今後の動向

The beverages market is expected to grow from USD 3.71 trillion in 2024 to USD 4.58 trillion by 2029 at a CAGR of 4.26% during the forecast period (2024-2029).

Key Highlights

- Rising health consciousness and the growing prevalence of lifestyle diseases encouraged consumers to choose healthy drinks. Furthermore, the market is witnessing an increased demand for low-alcohol-by-volume beverages, specifically among millennials and baby boomers. For instance, according to UN Comtrade statistics, the amount of non-alcoholic drinks imported to Hungary peaked in 2022 at 174 million euros from 154 million euros in 2021. The sales of low-alcohol drinks have been rising, with the availability of a broader product portfolio with improved taste, aiding consumers to select products as per their preferences easily.

- Furthermore, the increasing participation of individuals in professional sports, recreational outdoor activities, and exercise and physical fitness is creating demand for dietary supplements, such as energy drinks. Energy drinks are functional beverages that help increase energy and enhance mental alertness and physical performance. Leading players are further focusing on developing sugar-free drinks to cater to the needs of individuals with diabetes and other chronic illnesses.

- For instance, in 2022, an Australian soft drinks company, Nexba, launched a range of caffeine- and sugar-free energy drinks with added vitamins and prebiotics. Nexba Natural Energy drinks are free from artificial ingredients and available in two flavors: Lemon yuzu and Wild Citrus. The company claims the flavors contain ginseng extract, vitamin B complex, and vitamin C to improve gut health and enhance energy levels. Therefore, the abovementioned factors will likely influence the market positively during the forecast period.

Beverage Market Trends

Consumer Inclination Toward Sugar-Free Drinks

- Healthy food choices attract consumers' attention due to their vast interest in holistic well-being. Consumers are looking for products low in sugar and contain health-enhancing ingredients. Furthermore, according to the International Diabetes Federation, India was home to 77 million diabetes patients in 2019, the second-largest in the world. By 2030, the number is predicted to reach 101 million. According to the same source, around 114 million adults in China had diabetes in 2019. Due to the high prevalence of diabetes globally, consumers are becoming more aware of the importance of a healthy diet and an active lifestyle.

- Moreover, changes in consumer preferences for reduced or no-sugar products direct beverage manufacturers toward product innovation. Manufacturers in the market effectively communicate their products to live up to consumers' expectations and deliver the functionality they demand. They are developing a range of novel products to meet the consumers' demand who are actively trying to avoid consuming sugary drinks to prevent the harmful effects of excessive sugar intake.

- For instance, Shine Drink launched a new sugar-free range in October 2022. The product is called 'brain drinks' or 'smart -drinks' and contains natural functional ingredients. The product is available in blueberry lemonade and peach passion fruit flavors. Moreover, private-label companies are also entering the market to meet the demand for healthier alternatives in the beverage category, competing with the top brands.

North America Holds the Largest Market Share

- Shifting consumer preference for non-alcoholic beverages is identified as the key market driver in the beverages market in North America. In addition, the market growth can be attributed to the high consumption of sports and energy drinks owing to the widespread participation in leisure sports, physical activities, and intense gym workouts. The trend is also anticipated to continue during forecast years due to the rising government initiatives to accelerate the active participation of school and college students in various sports activities.

- Moreover, the increasing prevalence of lactose intolerance and dairy allergies led to the penetration of plant-based beverages such as fruit and vegetable juices and flavored cold drinks. In addition, increasing affinity towards organic and clean-label products is influencing key manufacturers to develop innovative variants in the ready-to-drink beverages category.

- For instance, in February 2022, Starbucks launched a new plant-based Frappuccino line with two flavors, Caramel Waffle Cookie and Dark Chocolate Brownie. Additionally, the strong consumer demand for portability and convenience has accelerated innovations in packaging shape, lighter packaging materials, and an increased application of flexible packaging. Thus, all these factors drive the beverage market in North America.

Beverage Industry Overview

The market is highly competitive, with key players operating, such as Nestle S.A., Anheuser-Busch InBev, Heineken N.V., PepsiCo, Inc., and The Coca-Cola Company. Various active companies in the market have adopted product innovation as a strategy due to changing consumer preferences worldwide. The primary focus of the companies is to offer products with different flavors and added functionalities, thereby catering to consumer preferences efficiently. For instance, in September 2022, Gatorade, a PepsiCo brand, launched a caffeinated energy drink, "Fast Switch," for athletes. The product is a cross between an energy drink and a sports drink. The product is non-carbonated, contains no sugar, and does not include any artificial colors or flavors.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Preference for Plant-based and Clean-label RTD Products

- 4.1.2 Consumer Inclination Toward Sugar-Free Drinks

- 4.2 Market Restraints

- 4.2.1 Concerns Over Health Issues Associated With Beverages

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Product Type

- 5.1.1 Alcoholic Beverages

- 5.1.1.1 Beer

- 5.1.1.2 Wine

- 5.1.1.3 Spirits

- 5.1.2 Non-Alcoholic Beverages

- 5.1.2.1 Energy & Sports Drink

- 5.1.2.2 Soft Drinks

- 5.1.2.3 Bottled Water

- 5.1.2.4 Packaged Juice

- 5.1.2.5 RTD Tea and Coffee

- 5.1.2.6 Other Non-Alcoholic Beverages

- 5.1.1 Alcoholic Beverages

- 5.2 By Distribution Channel

- 5.2.1 On-trade

- 5.2.2 Off-trade

- 5.2.2.1 Supermarkets/Hypermarkets

- 5.2.2.2 Convenience/Grocery Stores

- 5.2.2.3 Online Retail Stores

- 5.2.2.4 Other Off Trade Channels

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 Spain

- 5.3.2.4 France

- 5.3.2.5 Italy

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East & Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Nestle S.A.

- 6.3.2 PepsiCo, Inc.

- 6.3.3 The Coca-Cola Company

- 6.3.4 Anheuser-Busch InBev

- 6.3.5 Heineken N.V.

- 6.3.6 Diageo plc

- 6.3.7 Suntory Holdings Limited

- 6.3.8 Constellation Brands, Inc.

- 6.3.9 Red Bull GmbH

- 6.3.10 Keurig Dr Pepper