|

市場調査レポート

商品コード

1407019

ケラトメーター:市場シェア分析、産業動向・統計、成長予測(2024~2029年)Keratometers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ケラトメーター:市場シェア分析、産業動向・統計、成長予測(2024~2029年) |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

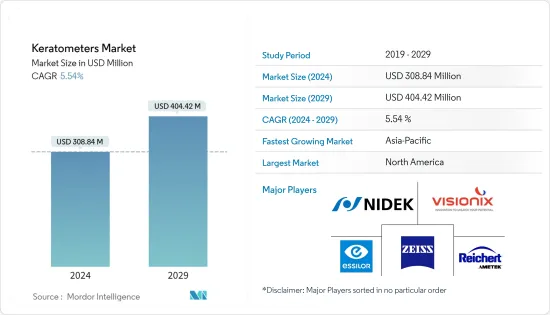

世界のケラトメーターの市場規模は、2024年に3億884万米ドルに達し、2024~2029年の予測期間中にCAGR 5.54%で成長し、2029年には4億442万米ドルに達すると予測されています。

COVID-19パンデミックは、COVID-19以外の疾患の治療・診断活動を混乱させました。これは、世界中の治療手順と医薬品および医療機器のサプライチェーンに影響を与え、調査市場に悪影響を与えました。例えば、Carl Zeiss annual report 2022によると、パンデミックの間、ケラトメーターを含む眼科医療機器戦略ビジネスユニット(SBU)の収益は-7.3%減少しました。しかし、2022年度の眼科機器戦略ビジネスユニットからの売上は17%増加しました。これは、パンデミック中にケラトメーターなどの眼科医療機器の売上高が減少したが、サプライチェーンの再開とヘルスケア施設での診断活動により回復したことを示しています。

市場を牽引する要因としては、眼疾患の負担増、投資、資金、助成金の増加が挙げられます。眼疾患の負担が大きいため、ケラトメーターの需要が増加し、大幅な成長が見込まれます。例えば、InSight Vision Centerが2021年12月に発表したレポートによると、6~12カ月の乳幼児の23%に一般的な乱視が含まれます。同様に、WHOの2022年10月の報告書によると、世界中で約22億人が近視または遠視の視力障害に苦しんでおり、そのうち約10億件の視力障害は予防が可能です。視力障害の負担が大きいことを示しています。ケラトメーターを用いた診断に対する高い需要が見込まれ、調査期間中の市場を押し上げる可能性が高いです。

さらに、市場参入企業による新たな戦略や取り組みが市場に大きな影響を与えると予想されます。例えば、2021年5月、ZEISSは、Capture 3Dを買収することで、産業品質&調査セグメントの米国における全国カバレッジを拡大しました。この買収により、顧客は最高の測定ソリューションを得るためのシームレスで統合されたエクスペリエンスの恩恵を受けることになり、スタッド期間にわたって市場を促進することが期待されます。

しかし、低開発国や新興国市場では、眼に関連する疾患に対する一次的なインフラ整備が必要であり、市場全体の成長を妨げています。

ケラトメーター市場動向

予測期間中、病院が大きな市場シェアを占める見込み

病院数の増加が市場成長の主な要因です。病院数は米国やメキシコのような様々な国で安定したペースで増加しています。例えば、米国病院協会(American Hospital Association)の2022年報告書によると、米国には6,093の病院があります。しかし、ディフィニティブ・ヘルスケアのHospitalView製品は、2022年3月現在、米国で活動中の7,308の病院を追跡しています。これらの病院施設は、40の公共、民間、および独自の情報源から収集されています。投資の増加も市場成長の要因のひとつです。

India Brand Equity Foundationが2021年12月に発表したレポートによると、産業・国内貿易振興局(DPIIT)が発表したデータによると、医薬品・製薬セクターへの外国直接投資(FDI)流入額は191億9,000万米ドルでした。病院、診断センター、医療・手術器具などの分野へのFDI流入額は、それぞれ77億3,000万米ドル、23億5,000万米ドルでした。

同じ情報筋によると、インド政府は国内のヘルスケア・インフラを強化するため、5,000億インドルピー(68億米ドル)相当の信用優遇プログラムを導入する予定だといいます。このプログラムでは、政府が保証人となり、企業が資金を活用して病院のキャパシティや医療用品を拡大することができます。このような取り組みや投資は、角膜計を含む様々な医療機器を採用することにより、エンドユーザー施設を増やすことになります。したがって、上記の要因は、予測期間中に調査セグメントの成長を促進すると予想されます。

予測期間中、北米が市場で大きなシェアを占める見込み

北米地域は予測期間中、大きな市場シェアを占めると予測されています。投資、眼疾患の増加、調査研究などの要因が市場成長を増大させる可能性が高いです。2023年3月のCDCのNCHSによると、眼疾患と視力障害の研究資金は2021年に10億7,000万米ドルであったが、2022年には10億9,700万米ドルに増加し、2023年には11億6,300万米ドルになると推定されています。これは、眼疾患と視力障害に関する研究資金が増加していることを示しており、ケラトメーターの使用に大きな影響を与え、予測期間中の市場の成長を促進すると予測されています。

ケラトメーターは角膜の曲率を測定し、角膜乱視を角膜後乱視、水晶体後乱視と水晶体前乱視とともに算出するが、多くの場合、乱視は最小です。乱視は最も頻度の高い屈折矯正です。有病率の増加はケラトメーターの需要を増加させ、同地域の市場成長を押し上げると予想されます。例えば、NVISION Eye Centersが2022年12月に発表したレポートによると、乱視は米国では約3人に1人の割合で発生しています。また、遠視は40歳以上の人口の約8.4%に、近視は40歳以上の人口の約23.9%に発生しています。これは視力障害の負担が大きいことを示しており、ケラトメーターの使用率を高め、市場成長を促進しています。

ケラトメーター産業の概要

市場は適度に統合されており、複数の大手企業で構成されています。各社は、合併、新製品の発売、買収、提携など、特定の戦略的イニシアチブを実施しており、市場での地位強化に役立っています。さらに、主なプレーヤーによって開始された研究開発活動の増加も、市場の成長を後押ししています。現在市場を独占している企業には、Carl Zeiss AG、Essilor、Visionix(Luneau Technology)、Reichert, Inc.、NIDEKなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 眼疾患の負担増

- 眼科医療機器への投資、資金、助成金の増加

- 市場抑制要因

- 低開発国および新興諸国における眼関連疾患に対する主要インフラの欠如

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション - 市場規模:金額別(米ドル)

- タイプ別

- 据え置き型ケラトメーター

- 携帯型ケラトメーター

- エンドユーザー別

- 病院

- 眼科クリニック

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Carl Zeiss AG

- Costruzione Strumenti Oftalmici

- Essilor

- Visionix(Luneau Technology)

- Topcon Corporation

- Micro Medical Devices

- Naugra Medical

- NIDEK CO., LTD

- TOMEY GmbH

- Reichert, Inc

- SHIGIYA MACHINERY WORKS LTD GS Division

- Canon Medical Systems Corporation

第7章 市場機会と今後の動向

The Keratometers Market size is estimated at USD 308.84 million in 2024, and is expected to reach USD 404.42 million by 2029, growing at a CAGR of 5.54% during the forecast period (2024-2029).

The COVID-19 pandemic disrupted the treatment and diagnostic activities of diseases other than COVID-19. It impacted the treatment procedures and supply chain of pharmaceuticals and medical devices worldwide, adversely impacting the studied market. For instance, according to the Carl Zeiss annual report 2022, the revenue in the ophthalmic devices strategic business unit (SBU), including keratometers, decreased by -7.3% during the pandemic. However, the revenue from the ophthalmic devices strategic business unit increased by 17% in FY2022. It shows the declined sales revenue of ophthalmic devices like keratometers during the pandemic, which recovered due to a resumed supply chain and diagnostic activities in the healthcare facilities.

The factors driving the market include the increasing burden of eye disorders and growing investments, funds, and grants. The high burden of eye disorders increases the demand for keratometers, which is expected to grow significantly. For instance, as per the report published by InSight Vision Center in December 2021, 23% of infants aged 6 to 12 months would include common astigmatism. Similarly, according to the October 2022 report of the WHO, about 2.2 billion people around the world suffer from near or distant vision impairment, of which approximately 1 billion cases of vision impairment can be prevented. It shows the high burden of the cases of vision impairment. It is expected to include a high demand for the diagnosis using keratometers and likely boost the market over the study period.

Furthermore, the new strategies and initiatives by the market players are expected to significantly impact the market. For instance, in May 2021, ZEISS expanded its national coverage in the United States for its Industrial Quality & Research segment by acquiring Capture 3D. With this acquisition, customers benefitted from a seamless, integrated experience to get the best measuring solutions, and it is expected to propel the market over the stud period.

However, the need for primary infrastructure for eye-related diseases in underdeveloped and developing countries hampers overall market growth.

Keratometers Market Trends

Hospitals are Expected to Hold a Significant Market Share Over the Forecast Period

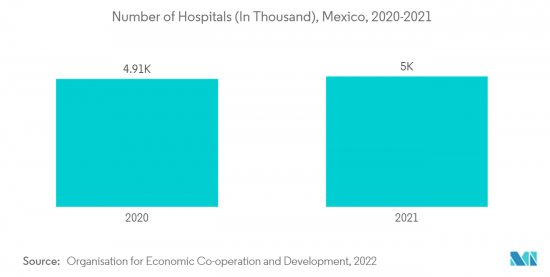

The increasing number of hospitals is the primary factor for market growth. The number of hospitals is growing at a steady pace in various countries like the United States and Mexico. For instance, according to the American Hospital Association 2022 report, there are 6,093 hospitals in the United States. However, the Definitive Healthcare HospitalView product tracks 7,308 active United States hospitals as of March 2022. These hospital facilities are curated from 40 public, private, and proprietary sources. Increasing investment is another factor for market growth.

The report published by India Brand Equity Foundation in December 2021 stated that Foreign Direct Investment (FDI) inflows for the drugs and pharmaceuticals sector stood at USD 19.19 billion, according to the data released by the Department for Promotion of Industry and Internal Trade (DPIIT). FDI inflows in sectors such as hospitals, diagnostic centers, and medical and surgical appliances stood at USD 7.73 billion and USD 2.35 billion, respectively.

The same source stated that the Indian government plans to introduce a credit incentive program worth INR 500 billion (USD 6.8 billion) to boost the country's healthcare infrastructure. The program will allow firms to leverage the fund to expand hospital capacity or medical supplies, with the government acting as a guarantor. Such initiatives and investments would increase the end-user facilities by adopting various medical devices, including keratometers. Hence, the factors mentioned above are expected to drive the growth of the studied segment during the forecast period.

North America is Expected to Hold the Significant Share in the Market Over the Forecast Period

The North American region is expected to hold a significant market share over the forecast period. Factors such as investments, increasing eye disorders, and research studies will likely increase market growth. According to the NCHS at CDC in March 2023, the research funding for eye disease and disorders of vision was USD 1,070 million in 2021, which was increased to USD 1,097 million in 2022 and is estimated to be USD 1,163 million in 2023. It shows the increasing research funding on eye disease and vision disorders, which is expected to significantly impact keratometer usage, propelling the market's growth over the forecast period.

Keratometry measures the cornea's curvature to calculate corneal astigmatism along with posterior corneal astigmatism and posterior and anterior crystalline lens astigmatism, which is minimal in many cases. Astigmatism is the most frequent ammetropia. Increasing prevalence will increase the demand for keratometers, which is expected to boost the market's growth in the region. For instance, as per the report published by NVISION Eye Centers in December 2022, astigmatism occurs in about one out of every three people in the United States. In addition, farsightedness occurs in about 8.4% of the population over 40, and nearsightedness occurs in about 23.9% of the population over 40 years old. It shows the high burden of vision impairment, which increases keratometers' usage and propels market growth.

Keratometers Industry Overview

The market is moderately consolidated and consists of several major players. The companies are implementing certain strategic initiatives, such as mergers, new product launches, acquisitions, and partnerships, that help them strengthen their market positions. Further, the increase in research and development activities initiated by the key players also favors market growth. Some companies currently dominating the market are Carl Zeiss AG, Essilor, Visionix (Luneau Technology), Reichert, Inc., and NIDEK CO., LTD.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Burden of Eye Disorders

- 4.2.2 Growing Investments, Funds, and Grants on Eye Care Devices

- 4.3 Market Restraints

- 4.3.1 Lack of Primary Infrastructure For Eye Related Diseases in Underdeveloped and Developing Countries

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Type

- 5.1.1 Stationary Type Keratometers

- 5.1.2 Portable Type Keratometers

- 5.2 By End User

- 5.2.1 Hospitals

- 5.2.2 Eye Clinics

- 5.2.3 Others

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Carl Zeiss AG

- 6.1.2 Costruzione Strumenti Oftalmici

- 6.1.3 Essilor

- 6.1.4 Visionix (Luneau Technology)

- 6.1.5 Topcon Corporation

- 6.1.6 Micro Medical Devices

- 6.1.7 Naugra Medical

- 6.1.8 NIDEK CO., LTD

- 6.1.9 TOMEY GmbH

- 6.1.10 Reichert, Inc

- 6.1.11 SHIGIYA MACHINERY WORKS LTD GS Division

- 6.1.12 Canon Medical Systems Corporation