|

|

市場調査レポート

商品コード

1687759

自動車用シリンダーライナー:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Automotive Cylinder Liner - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 自動車用シリンダーライナー:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

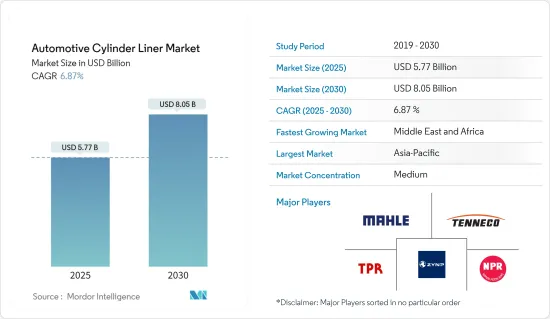

自動車用シリンダーライナーの市場規模は2025年に57億7,000万米ドルと推定・予測され、予測期間中(2025-2030年)のCAGRは6.87%で、2030年には80億5,000万米ドルに達すると予測されています。

商用車の販売台数の増加と自動車保有台数の増加は、世界の自動車産業の成長の主要な決定要因となっており、これが自動車用シリンダーライナーの需要にプラスの影響を与えています。商用車の成長は、主にeコマースの拡大や輸送のための商用車使用の増加の影響を受けています。また、自動車産業の進歩と発展を支える工業化とインフラ開発の高まりが、商用車市場の成長を促進しています。

国際自動車工業協会によると、2022年の商用車の世界新車販売台数は2,410万台に達します。

さらに、主要地域での水素電気商用車需要の高まりが、シリンダーライナーメーカーに先進技術の開発を促しています。複数の主要企業が水素電気トラック向けにシリンダーライナー技術を導入しており、市場成長を後押ししています。車両のスクラップ・プログラムや、車両の長さや積載量の制限などに関する厳しい規制基準も、市場の成長を促進すると予想されます。

アジア太平洋地域は、インドと中国における自動車産業の可能性の高まりにより、自動車用シリンダーライナーの消費を支配すると予想されます。米国など世界の多くの国では、原材料やエンジン部品を中国、日本、その他の経済圏から調達し、完全なエンジンチャンバーの下に組み立てています。自動車販売と生産の増加に伴い、この地域のシリンダーライナー需要は高水準を維持すると予想されます。

自動車用シリンダーライナーの市場動向

予測期間中に牽引力を増す乗用車セグメント

乗用車は新興国で最も一般的な交通手段です。新興国では一人当たり所得の増加に伴い乗用車の保有台数が増加しており、こうした要因が自動車用シリンダーライナー市場にプラスの影響を与えるとみられます。インドなどの新興国は、乗用車用にエタノールのようなより良い燃料を探しており、市場成長にプラスの影響を与える可能性があります。

例えば、2023年8月、トヨタInnovaは、エタノールのみで走行可能な世界初のフレキシブル燃料車となりました。トヨタ自動車は、100%エタノールを燃料とする自動車を導入する世界初の自動車メーカーになると予測されています。2023年8月、インド連邦大臣は、トヨタの最も人気のある乗用車「イノーバ」をベースにした車両を発売しました。イノーバは、フレキシブル燃料電気証明書を備えたバラット・フェーズVI車両を搭載した世界初のモデルとなりました。この発表は、日本の大手自動車メーカーが水素燃料電池を使用するMiraiを発表した1年後に行われました。

排ガス規制の強化、電気自動車の普及、内燃機関(ICE)車が環境に与える有害な影響による化石燃料の埋蔵量不足が、市場の成長に課題を与える可能性があります。しかし、新興国では電気自動車のためのインフラ整備が必要であり、充電設備が予測期間中の内燃機関市場の拡大を促進すると予想されます。国際自動車工業会(OICA)によると、2022年の世界の乗用車新車販売台数は5,740万台に達し、2021年比で前年比1.9%の伸びを記録しました。2022年の乗用車新車販売台数は、南アフリカが前年比19.5%増、タイが同10.0%増を記録しました。

都市化率の上昇と、自家用交通手段を利用する消費者の嗜好の変化は、世界中の自動車産業を牽引すると予想され、ひいては先進自動車用シリンダーライナー市場の需要を牽引すると期待されます。世界銀行によると、インドの都市化率は2018年の34%に対し、2022年には36%に達しています。新興国市場の都市部に移住する消費者が増えるにつれて、個人的な移動が好まれるようになり、それが世界全体の自動車用シリンダーライナー市場の成長につながる可能性があります。

予測期間中、アジア太平洋地域が最大の市場シェアを占める

アジア太平洋地域の自動車用シリンダーライナー市場は、中国とインドの自動車セクターの拡大により、シリンダーライナー製品の販売が増加しています。両国は自動車販売に拍車をかけ、大きなエンジン需要を生み出しています。

インドは同地域の主要な自動車輸出国のひとつであり、現在のモビリティ拡大プロジェクトを見て、間もなく力強い輸出の伸びが予想されます。さらに、インド政府による自動車産業を支援する好意的な取り組みと、同国市場における大手自動車メーカーの存在が、同国を主要な自動車輸出国のひとつに発展させる一助となっています。同国の自動車産業は、2000年4月から2022年9月までの累計で約337億7,000万米ドルの直接投資を受けました。政府は、2024年までに自動車産業の規模を2倍の180億米ドルに拡大すると見込んでいます。さらに、中国は自動車産業の処理能力とエンジン生産においてアジア太平洋で圧倒的な地位を占めています。

2022年、中国での自動車販売台数は2,680万台となり、2021年の2,627万台から前年比2.2%の伸びを記録しました。同地域では、主要エンジンメーカーや相手先商標製品メーカー(OEM)による投資、拡大、開発が拡大しています。これは予測期間中、シリンダーライナーの需要を緩和すると予想されます。

例えば、2022年3月、Harbin Dongan Auto Engineは、マシニングセンター、マーキングマシン、締め付けマシン、接着マシン、およびその他の設備を含むと予想された高効率拡張レンジエンジン用の生産ラインを構築するための2022年の投資計画を発表しました。このプロジェクトは哈尓濱東安汽車発動機の子会社である哈尓濱東安汽車発動機製造が共同で整備する計画で、総投資額は7,233万人民元(1,085万米ドル)です。

このため、この地域の乗用車・商用車産業の拡大に伴い、自動車用シリンダーライナー市場の需要は今後数年で急速に急増すると思われます。しかし、政府が電気自動車の普及に重点を移していることが、アジア太平洋地域における長期的な製品成長の大きな阻害要因になる可能性があります。しかし、短期的には車両の電動化に向けた競合シフトが、これらの政府にとって大きな課題となっています。そのため、自動車用シリンダーライナーの需要は予測期間中も堅調に推移すると予想されます。

自動車用シリンダーライナー産業の概要

自動車用シリンダーライナー市場は適度な断片化を示しており、組織化されたプレーヤーと組織化されていないプレーヤーが混在して業界情勢を形成しています。シリンダーライナー市場における主要な競合企業には、Mahle GmBH、Tenneco Inc.、TPR、日本ピストンリング、ZYNPなどがあります。主要メーカーは収益性と製品効率を高めるため、自動車用シリンダーライナーの研究開発に多額の投資を行っています。

原材料調達に伴うリスクを軽減するため、各社は積極的なアプローチを採用し、主要原材料サプライヤーとの関係を拡大しています。この戦略は、シリンダーライナーの生産に必要な原材料の安定的かつ継続的な供給を確保することに成功しています。

2022年10月:ラインメタルAGの鋳物事業部門(ラインメタルと華宇汽車系統の合弁会社)は、英国の有名スポーツカーメーカーにV8エンジンブロックを供給する重要な受注を獲得しました。V8エンジンは4桁に迫る素晴らしい馬力を誇る。

2022年4月:北米トヨタは、米国の4工場に3億8,300万米ドルを投資する意向を明らかにしました。この投資は、ハイブリッドと従来のパワートレインに合わせた新しい4気筒エンジンの生産準備を目的としています。エンジン生産の範囲は、エンジンヘッド、ライナー、その他様々な部品を含むエンド・ツー・エンドの組み立てを含みます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 商用車販売の増加

- その他

- 市場抑制要因

- 電気自動車の急速な普及

- その他

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 材料タイプ別

- 鋳鉄

- ステンレス

- アルミニウム

- チタン

- 燃料別

- ガソリン

- ディーゼル

- 接点別

- 湿式シリンダーライナー

- 乾式シリンダーライナー

- 車種別

- 乗用車

- 小型商用車

- 中・大型商用車

- 地域別

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- メキシコ

- ブラジル

- アルゼンチン

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Mahle GmbH

- Tenneco Inc.

- GKN Zhongyuan Cylinder Liner Company Limited

- Melling Cylinder Sleeves

- TPR Co. Ltd

- Westwood Cylinder Liners Ltd

- Darton International Inc.

- ZYNP International Corporation

- Laystall Engineering Co. Ltd

- India Pistons Ltd

- Nippon Piston Ring Co. Ltd

- Motordetal

- Kusalava International

- Cooper Corp.

- Yoosung Enterprise Co. Ltd

- Yangzhou Wutingqiao Cylinder Liner Co. Ltd

- Chengdu Galaxy Power Co. Ltd

第7章 市場機会と今後の動向

- ハイブリッドライナーの採用増加

The Automotive Cylinder Liner Market size is estimated at USD 5.77 billion in 2025, and is expected to reach USD 8.05 billion by 2030, at a CAGR of 6.87% during the forecast period (2025-2030).

The rising sales of commercial vehicles and increasing vehicle parc globally serve as major determinants for the growth of the automotive industry across the world, which, in turn, is positively impacting the demand for automotive cylinder liners. Commercial vehicle growth is primarily influenced by the expansion of e-commerce and the increasing use of commercial vehicles for transportation. Aside from that, rising industrialization and infrastructure development, which support advancement and development in the automotive industry, are driving market growth for commercial vehicles.

According to the International Organization of Motor Vehicle Manufacturers, the global sales of new commercial vehicles touched 24.1 million units in 2022.

Furthermore, rising demand for hydrogen electric commercial vehicles across major regions is pushing cylinder liner manufacturers to develop advanced technology. Several key players are introducing cylinder liner technology for hydrogen-electric trucks, boosting market growth. Vehicle scrappage programs and stringent regulatory norms for vehicle length and loading limits, among other parameters, are also expected to drive the growth of the market.

Asia-Pacific is expected to dominate the consumption of automotive cylinder liners, owing to the increased potential of the automotive industry in India and China. Many countries across the world, such as the United States, source their raw materials and engine components from China, Japan, and other economies to assemble them under complete engine chambers. With rising automotive sales and production, the region's demand for cylinder liners is expected to remain high.

Automotive Cylinder Liner Market Trends

The Passenger Car Segment of the Market to Gain Traction During the Forecast Period

Passenger cars are the most common form of transport in emerging countries. The number of passenger cars is increasing in developing countries with the rise in per capita income, and such factors are likely to impact the automotive cylinder liner market positively. Emerging countries, such as India, are looking for better fuels, like ethanol, for their passenger cars, which may positively impact the market growth.

For instance, in August 2023, Toyota Innova became the world's first flexible fuel vehicle that can run entirely on ethanol. Toyota Motor is projected to become the first automaker in the world to introduce cars powered by 100% ethanol. In August 2023, the Union Minister of India launched a vehicle based on Toyota's most popular passenger car, Innova. Innova became the first model in the world to feature a Bharat Phase VI vehicle with a flexible fuel electric certificate. The launch came a year after the Japanese auto giant introduced Mirai, which uses hydrogen fuel cells.

Increasing emission regulations, penetration of electric vehicles, and lack of fossil fuel reserves due to the toxic impact of internal combustion engine (ICE) vehicles on the environment could challenge the growth of the market. However, in emerging countries, there needs to be more infrastructure for electric vehicles, and charging facilities are expected to facilitate the expansion of the internal combustion engine market during the forecast period. According to the International Organization of Motor Vehicle Manufacturers (OICA), global new passenger car sales touched 57.4 million in 2022, recording a Y-o-Y growth of 1.9% compared to 2021. Countries such as South Africa and Thailand recorded 19.5% and 10.0% Y-o-Y growth, respectively, in new passenger car sales in 2022 compared to the previous year.

The rising urbanization rate and the shifting preference of consumers toward availing private transportation mediums are anticipated to drive the automotive industry across the world, which, in turn, is expected to drive the demand for the advanced automotive cylinder liner market. According to the World Bank, the urbanization rate in India stood at 36% in 2022, compared to 34% in 2018. As more consumers migrate to urban areas in developing nations, there will be a preference for personal mobility, which, in turn, may lead to the growth of the automotive cylinder liner market across the world.

Asia-Pacific to Hold the Largest Market Share During Forecast Period

The Asia-Pacific automotive cylinder liner market is witnessing elevated sales of cylinder liner products owing to the expanding auto sector of China and India. Both countries are fuelling vehicle sales, generating significant engine demand.

India is one of the major automobile exporters in the region, and strong export growth is expected shortly, seeing its present mobility expansion projects. Furthermore, favorable initiatives by the Indian government to support the automotive industry and the presence of major automakers in its market are assisting in developing the country into one of the major automobile exporters. The automotive industry in the country received a cumulative FDI inflow of approximately USD 33.77 billion between April 2000 and September 2022. The government expects to double the size of the automotive industry to USD 18 billion by 2024. Furthermore, China holds the dominant hand in Asia-Pacific in terms of auto industry throughput and engine production.

In 2022, the total number of vehicles sold in China stood at 26.8 million units, compared to 26.27 million units in 2021, registering a year-on-year growth of 2.2%. The region is witnessing extended investment, expansion, and development, proliferated by key engine manufacturers and original equipment manufacturers (OEMs). This is expected to mitigate the demand for cylinder liners over the forecast period.

For instance, in March 2022, Harbin Dongan Auto Engine Co. Ltd unveiled its investment plan for 2022 for building a production line for high-efficiency extended-range engines, which was expected to involve machining center, marking machines, tightening machines, gluing machines, and other equipment. The project was planned to be jointly maintained by Harbin Dongan Automotive Engine Manufacturing Co. Ltd, the subsidiary of Harbin Dongan Auto Engine, with a total investment of CNY 72.33 million (USD 10.85 million).

Therefore, with the region's expanding passenger car and commercial vehicle industry, the demand for the automotive cylinder liner market will showcase a rapid surge in the coming years. However, shifting the government's focus to promote the adoption of electric vehicles could act as a major deterrent to the growth of these products in the long run in Asia-Pacific. However, a competitive shift toward electrification of vehicle fleets in the short run is a major challenge for these governments. Therefore, the demand for automotive cylinder liners is expected to remain strong during the forecast period.

Automotive Cylinder Liner Industry Overview

The automotive cylinder liner market exhibits moderate fragmentation, with a mix of organized and unorganized players shaping the industry landscape. Among the key contenders in the cylinder liner market, notable players include Mahle GmBH, Tenneco Inc., TPR Co. Ltd, Nippon Piston Ring Co. Ltd, and ZYNP. Significant manufacturers are channeling substantial investments into the research and development of automotive cylinder liners to enhance profitability and product efficiency.

To mitigate the risks associated with raw material procurement, companies have adopted a proactive approach, maintaining extended relationships with their primary raw material suppliers. This strategy has proven successful in ensuring a consistent and uninterrupted supply of materials necessary for cylinder liner production.

October 2022: Rheinmetall AG's Castings business unit, a joint venture between Rheinmetall and HUAYU Automotive Systems Co. Ltd, secured a significant order to supply a V8 engine block to a renowned English sports car manufacturer. Notably, the V8 engines boast an impressive horsepower output, approaching four figures.

April 2022: Toyota Motor North America disclosed its intention to invest USD 383 million in four US-based plants. This investment is aimed at preparing to produce a new four-cylinder engine variant tailored for hybrid and conventional powertrains. The scope of engine production encompasses end-to-end assembly, encompassing engine heads, liners, and various other components.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Rising Sales of Commercial Vehicles

- 4.1.2 Others

- 4.2 Market Restraints

- 4.2.1 Rapid Adoption of Electric Vehicles

- 4.2.2 Others

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value - USD)

- 5.1 By Material Type

- 5.1.1 Cast Iron

- 5.1.2 Stainless Steel

- 5.1.3 Aluminum

- 5.1.4 Titanium

- 5.2 By Fuel Type

- 5.2.1 Gasoline

- 5.2.2 Diesel

- 5.3 By Contact

- 5.3.1 Wet Cylinder Liner

- 5.3.2 Dry Cylinder Liner

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Light Commerical Vehicles

- 5.4.3 Medium and Heavy-duty Commercial Vehicles

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Spain

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Latin America

- 5.5.4.1 Mexico

- 5.5.4.2 Brazil

- 5.5.4.3 Argentina

- 5.5.4.4 Rest of Latin America

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Mahle GmbH

- 6.2.2 Tenneco Inc.

- 6.2.3 GKN Zhongyuan Cylinder Liner Company Limited

- 6.2.4 Melling Cylinder Sleeves

- 6.2.5 TPR Co. Ltd

- 6.2.6 Westwood Cylinder Liners Ltd

- 6.2.7 Darton International Inc.

- 6.2.8 ZYNP International Corporation

- 6.2.9 Laystall Engineering Co. Ltd

- 6.2.10 India Pistons Ltd

- 6.2.11 Nippon Piston Ring Co. Ltd

- 6.2.12 Motordetal

- 6.2.13 Kusalava International

- 6.2.14 Cooper Corp.

- 6.2.15 Yoosung Enterprise Co. Ltd

- 6.2.16 Yangzhou Wutingqiao Cylinder Liner Co. Ltd

- 6.2.17 Chengdu Galaxy Power Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Adoption of Hybrid Liners