|

市場調査レポート

商品コード

1850256

デジタル決済:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Digital Payments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| デジタル決済:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月20日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

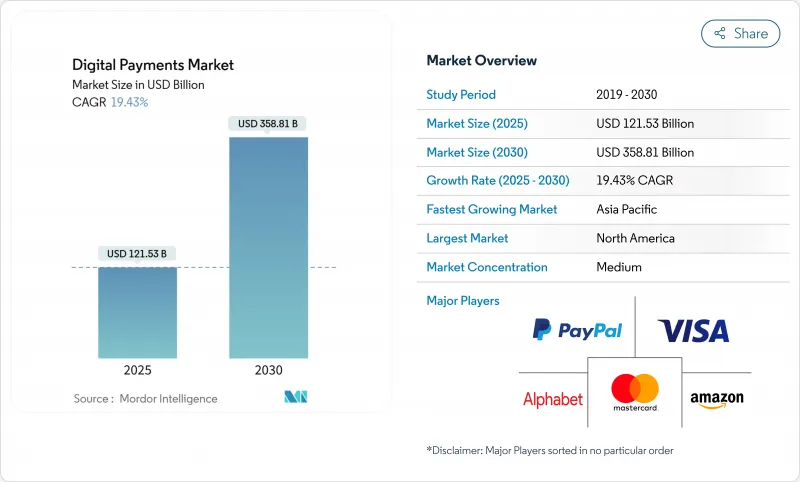

デジタル決済市場規模は2025年に1,215億3,000万米ドル、2030年には3,588億1,000万米ドルに達すると推定され、2025-2030年のCAGRは19.43%です。

この好調な見通しは、主要経済圏の規制の同期化、相互運用可能な決済レールの普及、シームレスな国境を越えた商取引に対する需要の高まりによって形成されています。大規模なカードネットワークと代替決済手段の相互作用によって競合の境界が再定義される一方、人工知能が不正防止とリアルタイムの意思決定の水準を高めています。成熟した市場では取扱高が安定し、新興地域では急速な拡大が見込まれるため、プロセッサーは効率化への投資と高成長市場への進出のバランスを取る必要があります。トークン化とインスタントペイメントに関する規制の明確化により、断片化コストが圧縮され、製品ロードマップを新たなコンプライアンステンプレートに合致させた早期参入企業が報われます。

世界のデジタル決済市場の動向と洞察

QRコード決済の標準化が東南アジアの統合を促進

標準化されたQRインフラは急速に拡大しており、インドネシアのQRISは2024年第4四半期に7億7,900万件、82兆ルピア(54億米ドル)相当の取引を処理し、5,500万人のユーザーと3,600万人の加盟店を接続しています。タイとの国境を越えた連携は、送金コストを最大50%削減できる雛形となり、ASEANを統合された決済回廊に位置づける。政府主導により、零細企業が信用履歴なしでデジタル決済を利用できるようになり、金融包摂が加速。

EUのトークン化義務化によりグローバルなセキュリティ基準が確立

2024年12月に施行された暗号資産市場(Markets in Crypto-Assets)規制は、デジタル資産のトークン化を義務付け、欧州以外のプロセッサーにも影響を及ぼしています。Visaがアジア太平洋全域で10億トークンを発行したことは、コンプライアンスがユーザー体験を向上させるスケーラブルなセキュリティ層を構築することを示しています。また、欧州中央銀行のデジタル・ユーロに関するガイダンスが相互運用性のチェックポイントを追加しています。

細分化されたカリブのKYC規則が摩擦を生む

カリブ海諸国におけるマネーロンダリング防止基準の相違により、プロセッサーは複数のコンプライアンスプログラムの運用を余儀なくされています。

セグメント分析

2024年のデジタル決済市場規模に占めるPOSチャネルの割合は57.2%だが、オンラインおよび遠隔オプションは2030年までCAGR 18.6%で拡大します。この軌跡は、欧州のモバイル決済額が2017年の40億ユーロ(44億米ドル)から2024年には1,950億ユーロ(2,126億米ドル)に増加することを反映しており、政策主導の採用が実証されています。常時モバイル決済を希望する旅行者の49.1%が挙げるコンタクトレス志向は、加盟店に受け入れインフラのアップグレードを促し続けています。インスタントペイメントレールの普及はチャネルの境界線を曖昧にするため、プロバイダーは店舗、ウェブ、アプリ内のフローをカバーする統合オーケストレーションを統合しています。AI主導のリスクエンジンによるリアルタイムの承認は、遠隔地からの決済がウォレットやペイバイバンクに移行する中で、POSベンダーに差別化をもたらします。

2024年の売上はソリューションが63.4%を占めるのに対し、サービスはCAGR20.4%で推移しており、導入に関する専門知識がウォレットシェアの原動力となっています。フィサーブは、クローバー・スタックをハードウェアからコマースイネーブルメントに再配置し、2桁のトップラインの拡大とサービスがエンゲージメントを深めることを証明しました。ストライプは2024年に1兆4,000億米ドルを処理し、開発者中心のオンボーディングにより、オーケストレーション・サービスがいかに加盟店の切り替えを促進するかを明確にしました。MiCA、インスタント・ペイメントの義務化、ISO20022への移行が複雑さを増す中、アドバイザリーおよびコンプライアンス・サービスの需要が高まっています。決済、FX、税務報告をホワイトラベルAPIにバンドルする企業には、国境を越えた大きなビジネスチャンスが存在します。

デジタル決済市場は、決済手段別(POS、オンライン/リモート決済)、コンポーネント別(ソリューション、サービス)、企業規模別(大企業、中小企業)、エンドユーザー産業別(小売、eコマース、ヘルスケアなど)、地域別に分類されています。市場予測は金額(米ドル)で提供されます。

地域別分析

北米は、カードネットワークの優位性とFedNowの展開に支えられ、2024年の売上高の38.3%を占めたが、アジア太平洋地域は2030年までのCAGRが17.3%となり、競合圧力が激化します。米国の大手銀行が支援するステーブルコイン・イニシアチブの出現は、デジタル通貨レールがカナダ・米国・メキシコの回廊における決済摩擦を軽減し、新たなサービスモデルを育成する可能性を示唆しています。

アジア太平洋地域は、中国のデジタル人民元試験運用、インドのUPI拡大、QRIS統合の地域的影響などを原動力とする主要な成長エンジンです。2024年第4四半期には、インドネシアだけで54億米ドルのQR決済が処理され、標準化されたコードのネットワーク効果が確認されました。現地のプロセッサーはグローバルゲートウェイと提携し、コンプライアンスギャップを埋めています。

欧州は規制面でのリーダーシップを発揮しています。MiCAは断片化を解消し、2025年1月に施行されるインスタント・ペイメント規制は、銀行に24時間ユーロ建て送金の提供を強制し、プロセッサー投資の優先順位を形成します。また、北欧とバルトのニッチ市場では、オープンバンキングをベースとしたペイバイアカウントのチェックアウトが試験的に導入され続けています。

南米、中東・アフリカでは、多様な導入曲線が見られます。ブラジルのPIX、メキシコのCoDi、GCCのインスタント・ペイロール・スキームはそれぞれ、国家が支援するレールが決済サイクルを短縮し、加盟店のコストを削減することを実証しています。アフリカのモバイル・マネー・エージェントは2024年に1兆6,800億米ドルを取り扱ったが、現金偏重とネットワークの信頼性の課題により、農村部での格差が残っています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 東南アジア全域でQRコード決済が急増

- EUのトークン化義務化によりオンラインセキュリティが強化される

- 南米における越境eコマースのAPM需要

- 北米におけるZ世代のBNPL導入の増加

- GCCにおける即時給与支払い制度

- 市場抑制要因

- カリブ諸国における断片化されたKYCルールが市場に課題

- アフリカの農村部における現金優先の採用拡大

- 中堅小売業者のCNP詐欺コストの上昇

- バリューチェーン分析

- 業界ステークホルダー分析

- 決済インフラと決済情勢の進化

- デジタル決済インフラ分析

- 規制サンドボックス

- 世界の規制状況

- 規制上の障害を伴うビジネスモデル

- 開発の余地vs.変化する情勢

- ポーターのファイブフォース

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 市場におけるマクロ経済動向の評価

第5章 市場規模と成長予測

- 支払い方法別

- 販売時点管理(POS)

- オンライン/リモート決済

- コンポーネント別

- ソリューション(ゲートウェイ、処理、ウォレット、不正行為、その他)

- サービス(コンサルティング、統合、サポート)

- 企業規模別

- 大企業

- 中小企業

- エンドユーザー業界別

- 小売業とeコマース

- メディアとエンターテイメント

- ヘルスケア

- ホスピタリティと旅行

- その他の業界(教育、公共事業、政府)

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- 北欧諸国

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東

- GCC

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- PayPal Holdings Inc.

- Visa Inc.

- Mastercard Inc.

- Amazon.com Inc.(Amazon Pay)

- Alphabet Inc.(Google Pay)

- Apple Inc.(Apple Pay)

- Stripe Inc.

- Adyen N.V.

- Fiserv Inc.

- Fidelity National Information Services Inc.(Worldpay)

- Block Inc.(Square and Cash App)

- ACI Worldwide Inc.

- Ant Group Co. Ltd.(Alipay)

- Tencent Holdings Ltd.(WeChat Pay)

- Paytm(One97 Communications Ltd.)

- Rapyd Financial Networks Ltd.

- Nets Group(Nexi)

- Mollie B.V.

- Verifone Inc.

- Lightspeed Commerce Inc.