|

|

市場調査レポート

商品コード

1404100

自動車部品アルミダイカスト-市場シェア分析、産業動向・統計、2024~2029年成長予測Automotive Parts Aluminum Die Casting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

|

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 自動車部品アルミダイカスト-市場シェア分析、産業動向・統計、2024~2029年成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

自動車部品アルミダイカスト市場規模は2024年に276億8,000万米ドルと推定・予測され、2029年には415億5,000万米ドルに達し、予測期間中(2024~2029年)のCAGRは7%を超える成長が見込まれています。

自動車の軽量化需要の高まりや、ダイカスト自動車部品におけるアルミニウムの利用拡大といった要因が、予測期間中の市場成長を後押しすると予想されます。厳しい環境規制やCAFE基準がさまざまな地域で課され、ダイカストプロセスの採用を後押ししています。

また、電気自動車やハイブリッド車への需要の高まりにより、自動車メーカーの関心は、あらゆるタイプの自動車において、より重い鋼鉄や鉄の代替としてアルミニウムのような軽量材料を使用することに向けられました。さらに、化石燃料のコスト上昇と電気自動車の普及台数の増加が、大きな市場の促進要因となっています。同市場で事業を展開する企業は、この需要増に対応するため、生産能力の増強に注力しています。例えば

主要ハイライト

- 2022年8月、WencanGroupは中国に10億人民元(1億4,000万米ドル)を投資し、安徽省陸安経済技術開発区に新エネルギー自動車(NEV)用アルミダイカスト部品の生産基地を建設しました。

- 2022年5月には、Tamil Nadu Small Industries Development Corporationが5,800万インドルピー(約70万米ドル)を投資し、アルミ高圧ダイカストの共通設備センターを設立しました。

同市場は、国家間の制裁や貿易紛争によるアルミニウム価格の変動や、自動車産業における(3Dプリンティングなどの)新しい鋳造技術の使用の増加によって制約を受けると予想されます。

自動車部品アルミダイカスト市場動向

自動車へのアルミニウムの普及が需要を押し上げる可能性が高い

アルミニウムはダイカスト用として最も好まれる金属です。自動車用途では、ハイブリッド車や電気自動車技術が増加しています。北米を例にとると、2016年以降、自動車1台当たりのアルミニウム含有量が62ポンド(28kg)増加し、2020年には自動車全体の含有量が459ポンド(208kg)に達します。20230年には570ポンド(258kg)に達すると予想されています。主に、小型トラックとバッテリー電気自動車へのシフトがこれを後押ししています。

さらに、2026年までに小型トラックの1台当たりのアルミニウム含有量は550ポンド(250kg)になると予想されています。この増加は、主にアルミニウム車体シート、鋳物、押出材という3つの主要な材料使用分野で見られます。その好例がテスラのモデルS BEVで、構造部品、鋳物、押出材、車体全体に800ポンド(360kg)を超えるアルミニウムを使用しています。

他方、価格上昇と原材料調達に関連するリスクは、長期予測期間中の市場成長の妨げになると予想されます。ここ数週間、米国とその他の中東・アフリカとの間に迫りつつある貿易戦争のため、ベースメタル価格は圧力を受けています。米国の同盟国(欧州連合、メキシコ、カナダを含む)からのアルミニウム(10%)と鉄鋼(25%)に対する輸入関税が次期大統領によって賦課されたことで、国内のアルミニウム価格が上昇すると予想されます。

さらに、インド、タイ、インドネシア、エジプト、その他の中東・アフリカ諸国などの新興国における乗用車の生産と販売の増加が、予測期間中の自動車部品アルミダイカスト市場を牽引すると予想されます。

著しい成長が見込まれるアジア太平洋

アジア太平洋は、予測期間中に最も速い成長率を示すと予想されています。アジア太平洋では、インド、中国、日本などの主要国が予測期間中の市場開拓に大きく貢献すると予想されます。中国はダイカスト部品の主要生産国の1つであり、同地域における乗用車の普及拡大が市場に楽観的な影響を与える可能性が高いです。

例えば、中国汽車工業協会によると、2022年の中国の自動車生産台数は前年比3.4%増の2,702万台に達し、販売台数は2.1%増の2,686万台となった。

アジア太平洋は世界有数の自動車生産国であるため、大手市場メーカーが集まる傾向にあります。多くのメーカーは、この市場で競合を維持するために、地理的拡大や生産能力の拡大といった成長戦略を採用しています。例えば、

- 2022年1月、中国の部品サプライヤーがテスラのパートナーにスーパーダイカストマシンを発注し、NIOとXPengが採用する可能性を示唆しました。この機械は一体型製造を可能にし、生産時間とコストを削減し、サプライチェーンの効率化というテスラの目標に合致します。

市場を促進する要因や市場の混乱につながる要因がある中で、アルミニウム製品に対する顧客の強い嗜好とアルミニウムの使用量増加の継続的な傾向は、市場に大きな成長機会をもたらすと予想されます。

自動車部品アルミダイカスト業界概要

自動車部品アルミダイカスト市場は、世界的と地域的に確立された参入企業によって統合され、主導されています。これらの企業は、市場での地位を維持するために、新製品開拓、提携、契約・協定などの戦略を採用しています。例えば

- 2023年3月、スウェーデンのアルミニウムサプライヤーであるGrangesは、中国のShandong Innovation Groupと提携し、持続可能なアルミニウムの生産を開始しました。この提携は、Grangesの持続可能な材料に関する専門知識と、Shandong Innovation Groupのリサイクルとクリーンエネルギーに関する能力を活用することを目的としています。両社は共に、環境に優しいアルミニウム鋳造製品に対する需要の高まりに応えることを目指しています。

同市場の大手企業には、Rheinmetall AG、Nemak、Linmar Corporation、Koch Enterprises、George Fischer Limitedなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 軽量材料重視の高まり

- その他

- 市場抑制要因

- 価格変動は利益率に対する恒常的な脅威

- その他

- 業界の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 生産プロセス

- 圧力ダイカスト

- 真空ダイカスト

- スクイズダイカスト

- 重力ダイカスト

- 用途タイプ

- ボディ部品

- エンジン部品

- トランスミッション部品

- バッテリーと関連部品

- その他の用途タイプ

- 地域

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- ロシア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他のアジア太平洋

- その他の中東・アフリカ

- ブラジル

- 南アフリカ

- アルゼンチン

- サウジアラビア

- アラブ首長国連邦

- その他の国

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Form Technologies Inc.(Dynacast)

- Nemak

- Endurance Technologies Ltd(CN)

- Sundaram Clayton Ltd

- Shiloh Industries Inc.

- Georg Fischer Limited

- Kochi Enterprises(Gibbs Die Casting Corporation)

- Bocar Group

- Engtek Group

- Rheinmetall AG

- Rockman Industries

- Ryobi Die Casting Ltd

- Linmar Corporation

- Meridian Light weight Technologies UK Limited

- Sandhar Group

第7章 7.市場機会と今後の動向

- プロセス自動化の増加

- 電気自動車の普及拡大

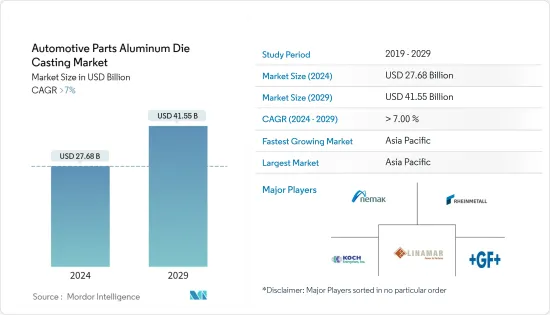

The Automotive Parts Aluminum Die Casting Market size is estimated at USD 27.68 billion in 2024, and is expected to reach USD 41.55 billion by 2029, growing at a CAGR of greater than 7% during the forecast period (2024-2029).

Factors such as the rising demand for lightweight vehicles and the growing utilization of aluminum in diecasting auto parts are expected to fuel the market's growth during the forecast period. Stringent environmental regulations and CAFE standards were imposed across various regions to support the adoption of the diecasting process.

In addition, increased demand for electric and hybrid vehicles turned automakers' focus to using lightweight materials like aluminum as a substitute for heavier steel and iron in all types of vehicles. Furthermore, the rising cost of fossil fuels and rising electric vehicle adoption are significant market drivers. Players operating in the market are focused on raising their production capacities to meet this rising demand. For instance,

Key Highlights

- In August 2022, WencanGroup Co., Ltd. Invested CNY 1 billion (USD 0.14 billion) in China to build a production base of aluminum diecast parts for New Energy Vehicles (NEVs) in Lu'anEconomic and Technological Development Zone, Anhui Province.

- In May 2022, Tamil Nadu Small Industries Development Corporation invested an amount of INR 5.8 crore (around USD 0.70 million) to establish a common facility center for aluminum high-pressure die casting.

The market is anticipated to be constrained by the volatility of aluminum pricing due to sanctions and trade disputes between nations and the growing use of novel casting technologies (such as 3D printing) in the automotive industry.

Automotive Parts Aluminum Die Casting Market Trends

Increasing Aluminum Penetration in Automobiles is Likely to Bolster Demand

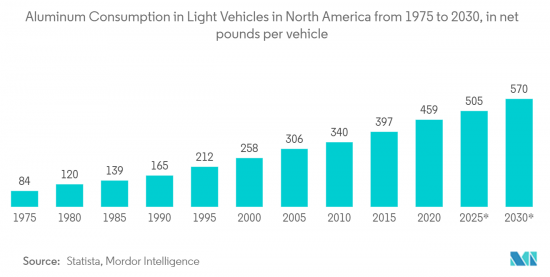

Aluminum is the most preferred metal for die casting. Within the automotive application, hybrid and electric vehicle technologies are on the rise. Taking North America as an example, since 2016, there was an increase in terms of aluminum content of 62 lbs (28 kg) per vehicle, with 2020 reaching a total vehicle content figure of 459 lbs (208 kg). It is expected to reach 570 lbs (258 kg) by the year 20230. The shift toward the light truck and battery electric vehicles primarily drives it.

Further, it is expected that by 2026, 550 lbs (250 kg) of aluminum content per vehicle for light-duty trucks. This increase is seen primarily in three main areas of material usage: aluminum auto body sheets, castings, and extrusions. A good example of this is Tesla's Model-S BEV, which uses over 800 lbs (360 kg) of aluminum for structural components, castings, extrusions, and the whole body of the vehicle.

On the other side, rising prices and risks associated with raw material sourcing are expected to hinder market growth during the longer-term forecast period. Base metal prices are under pressure in recent weeks due to the looming trade war between the United States and the rest of the world. The imposition of tariffs on imports from the US allies (including the European Union, Mexico, and Canada) on aluminum (10%) and steel (25%) by the President-elect is expected to increase the domestic aluminum prices.

Moreover, the increasing production and sales of passenger cars in several emerging economies, such as India, Thailand, Indonesia, Egypt, and other Middle East & African countries, are anticipated to drive the automotive parts aluminum die casting market during the forecast period.

Asia-Pacific Region Anticipated to Witness Significant Growth

Asia-Pacific is expected to witness the fastest growth rate during the forecast period. In the Asia-Pacific region, major countries like India, China, and Japan are expected to contribute significantly to the development of the market over the forecast period. China is one of the major producers of die-casting parts, and the growing adoption of passenger cars in the region is likely to provide an optimistic impact on the market.

For instance, according to the China Association of Automobile Manufacturers, China's car production reached 27.02 million units in 2022, an increase of 3.4% year-on-year, while sales increased by 2.1% to 26.86 million units.

The Asia-Pacific region, being one of the world's largest manufacturers of vehicles, tends to attract major market manufacturers. Many players adopt growth strategies, such as geographic expansion and production capacity expansion, to stay competitive in this market. For instance,

- In January 2022, a Chinese part supplier ordered super die-casting machines from a Tesla partner, hinting at potential adoption by NIO and XPeng. The machines enable one-piece manufacturing, reducing production time and costs, and align with Tesla's goal of improving efficiency in its supply chain.

Amidst all the factors promoting the market and the factors that can lead to disruption in the market, the strong preference of the customers toward aluminum products and the ongoing trend of increased usage of aluminum is expected to provide a significant growth opportunity in the market.

Automotive Parts Aluminum Die Casting Industry Overview

The automotive parts aluminum die casting market is consolidated and led by globally and regionally established players. These companies adopt strategies such as new product developments, collaborations, and contracts and agreements to sustain their market positions. For instance,

- In March 2023, Granges, a Swedish aluminum supplier, joined forces with China's Shandong Innovation Group to produce sustainable aluminum. The partnership aims to leverage Granges' expertise in sustainable materials and Shandong Innovation Group's capabilities in recycling and clean energy. Together, they aim to meet the increasing demand for environmentally friendly aluminum casting products.

Some of the major players in the market include Rheinmetall AG, Nemak, Linmar Corporation, Koch Enterprises, and George Fischer Limited.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Increasing Emphasis towards Lightweight Material

- 4.1.2 Others

- 4.2 Market Restraints

- 4.2.1 Volatility in Prices is a Constant Threat for Profit Margin

- 4.2.2 Others

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Production Process

- 5.1.1 Pressure Die Casting

- 5.1.2 Vacuum Die Casting

- 5.1.3 Squeeze Die Casting

- 5.1.4 Gravity Die Casting

- 5.2 Application Type

- 5.2.1 Body Parts

- 5.2.2 Engine Parts

- 5.2.3 Transmission Parts

- 5.2.4 Battery and Related Components

- 5.2.5 Other Application Types

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Germany

- 5.3.2.4 Italy

- 5.3.2.5 Russia

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 Brazil

- 5.3.4.2 South Africa

- 5.3.4.3 Argentina

- 5.3.4.4 Saudi Arabia

- 5.3.4.5 United Arab Emirates

- 5.3.4.6 Other Countries

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Form Technologies Inc.(Dynacast)

- 6.2.2 Nemak

- 6.2.3 Endurance Technologies Ltd (CN)

- 6.2.4 Sundaram Clayton Ltd

- 6.2.5 Shiloh Industries Inc.

- 6.2.6 Georg Fischer Limited

- 6.2.7 Kochi Enterprises (Gibbs Die Casting Corporation)

- 6.2.8 Bocar Group

- 6.2.9 Engtek Group

- 6.2.10 Rheinmetall AG

- 6.2.11 Rockman Industries

- 6.2.12 Ryobi Die Casting Ltd

- 6.2.13 Linmar Corporation

- 6.2.14 Meridian Light weight Technologies UK Limited

- 6.2.15 Sandhar Group

7 7. Market Opportunities and Future Trends

- 7.1 Increasing Process Automation

- 7.2 Growing Electric Vehicle Adoption