高薬理活性原薬(HPAPI)市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

High Potency Active Pharmaceutical Ingredients Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034- 発行日

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日

- 商品コード

- 1699263

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

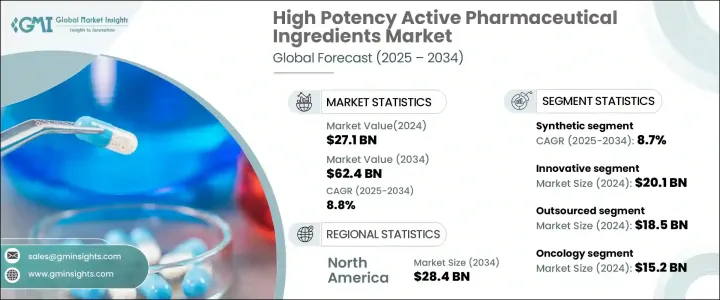

世界の高薬理活性原薬(HPAPI)市場は、2024年に271億米ドルと評価され、2025年から2034年にかけてCAGR 8.8%で成長すると予測されています。

HPAPIは、最小用量で強力な生物学的効果をもたらす特殊な医薬品化合物であり、その効力のために厳格な取り扱いと製造工程が必要となります。これらの成分は、全身毒性を抑えながらより効果的なドラッグデリバリーを可能にするため、現代の標的治療、特にがん治療において重要な役割を果たしています。精密医療への需要が高まる中、製薬会社は高度な治療へのニーズの高まりに対応するため、HPAPIの生産能力の拡大に注力しています。

市場は合成HPAPIとバイオテクノロジーHPAPIに分けられ、合成セグメントは2024年に180億米ドルの収益を上げ、CAGR 8.7%で成長すると予想されています。合成HPAPIはスケーラブルな製造プロセスのため、大規模生産に効率的であり、広く好まれています。細胞培養や発酵のような複雑な工程を必要とするバイオテクノロジーHPAPIとは異なり、合成HPAPIは確立された化学的手順で製造されるため、医薬品開発のタイムラインが短縮されます。慢性疾患の世界の蔓延が増加する中、合成HPAPIは、正確な投与量制御で標的治療効果をもたらす能力により、引き続き市場を独占しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 271億米ドル |

| 予測金額 | 624億米ドル |

| CAGR | 8.8% |

薬剤タイプにより、HPAPI市場は革新的薬剤とジェネリック医薬品に分類されます。革新的セグメントは2024年に201億米ドルを占め、市場の74.3%を占めます。がん、自己免疫疾患、その他の複雑な疾患に対する高度な治療に対する需要の高まりにより、高い有効性を持つHPAPIへの投資が増加しています。封じ込めシステムと連続製造プロセスにおける継続的な技術進歩は、厳しい規制要件へのコンプライアンスを確保しながら生産を合理化しています。さらに、持続可能な製造技術の採用により、HPAPI開発における製造コストの削減と安全性の向上が進んでいます。

市場はまた、製造業者のタイプ別に、自社生産と外部委託生産で区分されます。2024年の売上高は185億米ドルで、外部委託部門が市場をリードしています。特殊な封じ込め施設に関連するコストが高いことから、多くの製薬企業がHPAPIの製造を受託製造機関(CMO)に頼るようになっています。これにより製薬会社は、CMOの専門知識を活用して厳しい業界基準を満たしながら、医薬品の研究開発・商業化に集中することができます。その結果、アウトソーシングは生産効率を高め、費用対効果を維持するための戦略的手段となりました。

用途別では、がん領域が引き続き支配的なセグメントで、2024年の売上高は152億米ドルでした。HPAPIは、健康な組織への影響を最小限に抑えながらがん細胞を攻撃する能力を持つため、がん治療、特に化学療法や標的治療において重要な役割を果たしています。抗体薬物複合体や免疫療法を含む高度な薬剤製剤への応用が、市場の需要をさらに押し上げています。

地域別では、北米が2024年に124億米ドルを占め、2034年には284億米ドルに達すると予測されています。米国は113億米ドルの売上で同地域をリードしており、これはがん患者の増加と、高薬理活性医薬品の開発を支援する厳しい規制要件が要因となっています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- がんの有病率の上昇

- 標的療法の採用拡大

- 高活性医薬品成分の応用拡大

- 業界の潜在的リスク&課題

- 高い開発・製造コスト

- 厳しい規制要件

- 促進要因

- 成長可能性分析

- ギャップ分析

- 特許分析

- 今後の市場動向

- 規制状況

- 技術的展望

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 企業マトリックス分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 合成

- バイオテクノロジー

第6章 市場推計・予測:薬剤タイプ別、2021年~2034年

- 主要動向

- イノベーティブ

- ジェネリック

第7章 市場推計・予測:メーカータイプ別、2021年~2034年

- 主要動向

- インハウス

- アウトソーシング

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- オンコロジー

- ホルモンバランスの乱れ

- 緑内障

- その他の用途

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- Albany Molecular Research

- Agilent Technologies

- Axplora

- BASF

- Boehringer Ingelheim International

- Bristol-Myers Squibb Company

- CARBOGEN AMCIS

- Cipla

- CordenPharma

- Dr. Reddy’s Laboratories

- F. Hoffmann-La Roche

- Lonza

- Merck &Co.

- Novartis

- Pfizer

- Sanofi

- Sun Pharmaceutical Industries

- Teva Pharmaceutical Industries

目次

The Global High Potency Active Pharmaceutical Ingredients Market was valued at USD 27.1 billion in 2024 and is projected to grow at a CAGR of 8.8% from 2025 to 2034. HPAPIs are specialized pharmaceutical compounds that produce strong biological effects at minimal doses, necessitating strict handling and manufacturing processes due to their potency. These ingredients play a crucial role in modern targeted therapies, particularly cancer treatments, as they enable more effective drug delivery while reducing systemic toxicity. With the rising demand for precision medicine, pharmaceutical companies are focusing on expanding HPAPI production capabilities to cater to the growing need for advanced therapies.

The market is divided into synthetic and biotech HPAPIs, with the synthetic segment generating USD 18 billion in revenue in 2024 and expected to grow at a CAGR of 8.7%. Synthetic HPAPIs are widely preferred due to their scalable manufacturing processes, making them more efficient for large-scale production. Unlike biotech HPAPIs, which require complex processes like cell culture and fermentation, synthetic alternatives are produced using well-established chemical procedures, accelerating drug development timelines. With an increasing global prevalence of chronic diseases, synthetic HPAPIs continue to dominate the market due to their ability to deliver targeted therapeutic effects with precise dosage control.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $27.1 Billion |

| Forecast Value | $62.4 Billion |

| CAGR | 8.8% |

Based on drug type, the HPAPI market is categorized into innovative and generic drugs. The innovative segment accounted for USD 20.1 billion in 2024, representing 74.3% of the market. The growing demand for advanced treatments for cancer, autoimmune diseases, and other complex conditions has led to increased investment in high-efficacy HPAPIs. Ongoing technological advancements in containment systems and continuous manufacturing processes are streamlining production while ensuring compliance with stringent regulatory requirements. Additionally, the adoption of sustainable manufacturing techniques is reducing production costs and enhancing safety in HPAPI development.

The market is also segmented by manufacturer type, with in-house and outsourced production. The outsourced segment led the market with USD 18.5 billion in revenue in 2024. The high costs associated with specialized containment facilities have driven many pharmaceutical companies to rely on contract manufacturing organizations (CMOs) for HPAPI production. This allows pharmaceutical firms to focus on drug research, development, and commercialization while leveraging the expertise of CMOs to meet stringent industry standards. As a result, outsourcing has become a strategic move to enhance production efficiency and maintain cost-effectiveness.

In terms of applications, oncology remained the dominant segment, contributing USD 15.2 billion in revenue in 2024. HPAPIs play a vital role in cancer treatments, particularly in chemotherapy and targeted therapies, due to their ability to attack cancer cells with minimal impact on healthy tissues. Their application in advanced drug formulations, including antibody-drug conjugates and immunotherapy, is further driving market demand.

Geographically, North America accounted for USD 12.4 billion in 2024 and is projected to reach USD 28.4 billion by 2034. The U.S. led the region with USD 11.3 billion in revenue, driven by increasing cancer cases and stringent regulatory requirements that support the development of high-potency pharmaceuticals.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of cancer

- 3.2.1.2 Growing adoption of targeted therapies

- 3.2.1.3 Growing application of high potency active pharmaceutical ingredients

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development and manufacturing cost

- 3.2.2.2 Stringent regulatory requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Gap analysis

- 3.5 Patent analysis

- 3.6 Future market trends

- 3.7 Regulatory landscape

- 3.8 Technological landscape

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Synthetic

- 5.3 Biotech

Chapter 6 Market Estimates and Forecast, By Drug Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Innovative

- 6.3 Generic

Chapter 7 Market Estimates and Forecast, By Manufacturer Type, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 In-house

- 7.3 Outsourced

Chapter 8 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Oncology

- 8.3 Hormonal imbalance

- 8.4 Glaucoma

- 8.5 Other applications

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Albany Molecular Research

- 10.2 Agilent Technologies

- 10.3 Axplora

- 10.4 BASF

- 10.5 Boehringer Ingelheim International

- 10.6 Bristol-Myers Squibb Company

- 10.7 CARBOGEN AMCIS

- 10.8 Cipla

- 10.9 CordenPharma

- 10.10 Dr. Reddy’s Laboratories

- 10.11 F. Hoffmann-La Roche

- 10.12 Lonza

- 10.13 Merck & Co.

- 10.14 Novartis

- 10.15 Pfizer

- 10.16 Sanofi

- 10.17 Sun Pharmaceutical Industries

- 10.18 Teva Pharmaceutical Industries

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日